-

CENTRES

Progammes & Centres

Location

ভারত তার আর্থিক বাজারে লিঙ্গবৈষম্যের অবসান ঘটানোর প্রতিশ্রুতি দিলেও অধ্যয়নগুলি থেকে অন্য ছবি উঠে আসছে।

ভারতের জন্য অন্তর্ভুক্তিমূলক আর্থিক বাজার: লিঙ্গ–সংবেদনশীল পদ্ধতি গ্রহণ

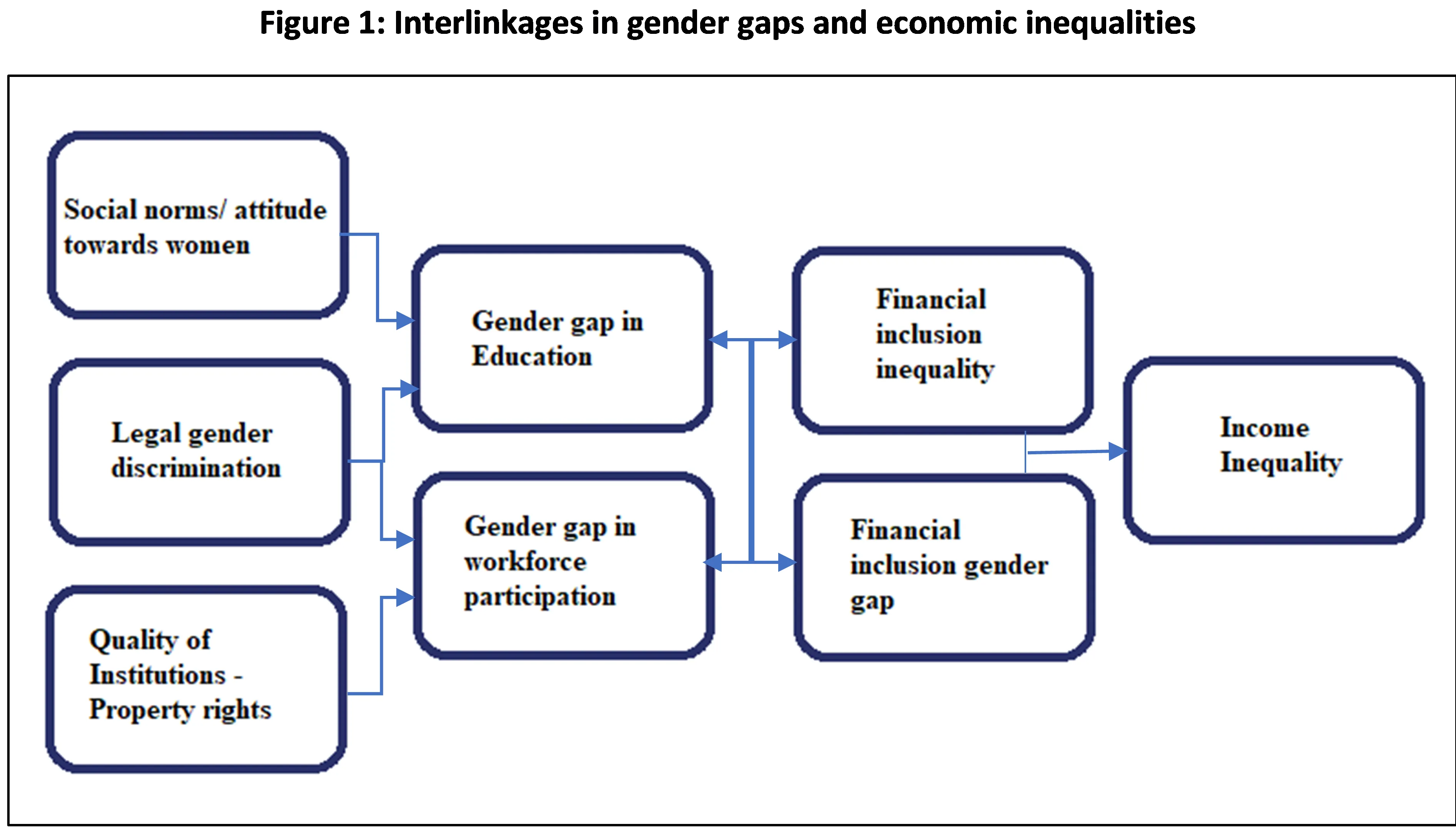

লিঙ্গভিত্তিক দৃষ্টিকোণ থেকে অর্থনৈতিক সমতাকে এগিয়ে নিয়ে যাওয়া প্রত্যাশাপূর্ণ ফলাফল দিতে পারে; এবং তা যেমন অর্থনৈতিক বৃদ্ধিতে অবদান রাখতে পারে, তেমনই সামাজিক উন্নয়নের ক্ষেত্রে সুদূরপ্রসারী প্রভাব ফেলতে পারে। মহিলাদের আর্থিক ক্ষেত্রে অধিকতর অংশগ্রহণের ব্যবস্থা শ্রমবাজারে নতুন কর্মীদের নিয়ে আসবে, যা বাজারটিকে আরও প্রতিযোগিতামূলক করে তুলবে, উৎপাদনশীলতা বৃদ্ধির দিকে নিয়ে যাবে, এবং ভৌত পুঁজিতে অতিরিক্ত বিনিয়োগকে উৎসাহিত করবে। আর এ সবের ফলে আয়বৃদ্ধিও হবে। অধিকন্তু, নারীর অর্থনৈতিক ক্ষমতায়ন আর্থ–সামাজিক অগ্রগতির দিকে নিয়ে যাবে, যার মধ্যে থাকবে নারী ও কিশোরীদের জন্য খাদ্য ও পুষ্টি, স্বাস্থ্যসেবা ও শিক্ষার মতো মৌলিক চাহিদাগুলিতে আরও বেশি অধিকার প্রতিষ্ঠা। এগুলি এস ডি জি ৫ (লিঙ্গ সমতা)–এর অনুসারী সামগ্রিক অগ্রগতির ইঙ্গিতবাহী। সমীক্ষায় দেখা গেছে যে উদীয়মান বাজার অর্থনীতিতে (ই এম ই) কর্মজীবী মহিলাদের ক্ষেত্রে পুষ্টি, স্বাস্থ্যসেবা ও শিক্ষায় বিনিয়োগ তাঁদের মোট আয়ের ৯০ শতাংশ। এই অতিরিক্ত সুযোগগুলিতে অবদান রাখা সত্ত্বেও পুরুষ ও মহিলাদের মধ্যে আয় বৈষম্য কিন্তু প্রকট রয়ে গেছে। বিশ্বব্যাপী, নারীরা একই কাজের জন্য তাঁদের পুরুষ সমকক্ষদের তুলনায় ২৩ শতাংশ কম বেতন পান। ভারতে চিত্রটি আরও খারাপ, কারণ এখানে পুরুষদের তুলনায় মহিলাদের ৩৪ শতাংশ কম বেতন দেওয়া হয়।

গবেষণায় দেখা গেছে যে উদীয়মান বাজার অর্থনীতিতে (ই এম ই) কর্মজীবী মহিলাদের ক্ষেত্রে পুষ্টি, স্বাস্থ্যসেবা ও শিক্ষায় বিনিয়োগ তাঁদের মোট আয়ের ৯০ শতাংশ।

ক্রমাগত মজুরি ব্যবধান ছাড়াও শ্রমবাজারের লিঙ্গগত পৃথগীকরণ প্রায়শই মহিলাদের আর্থিক ক্ষেত্রে অংশগ্রহণকে বাধাগ্রস্ত করে, এবং শেষ পর্যন্ত বিদ্যমান বৈষম্যগুলিকে পুষ্ট করে। ভারতে শ্রমশক্তিতে অংশগ্রহণে লিঙ্গ সমতার লড়াই একটি কঠিন কাজ, যার প্রতিধ্বনি শোনা গিয়েছে ২০২১–এর গ্লোবাল জেন্ডার গ্যাপ রিপোর্টে। দেশের মহিলা কর্মীবাহিনী আর্থিক ক্ষেত্রে অংশগ্রহণ ও সুযোগের ক্ষেত্রে সবচেয়ে মারাত্মক লিঙ্গ ব্যবধানের উদাহরণগুলির একটির সম্মুখীন৷ গত এক দশকে, ভারতে শ্রমশক্তিতে নারীর অংশগ্রহণ ২৩ শতাংশ (২০১২ সালে) থেকে ১৯ শতাংশে (২০২১ সালে) নেমেছে। নিঃসন্দেহে, এই আয় বৈষম্যগুলি সম্পদের মালিকানার বৈষম্য এবং পুরুষ ও মহিলাদের মধ্যে সম্পদের বৈষম্যকেও জোরদার করে। এই অর্থনৈতিক বৈষম্য এবং তার প্রভাব মোকাবিলায় অতীতে বেশ কিছু সামাজিক নিরাপত্তা প্রকল্প চালু করা হয়েছে, বিশেষ করে দরিদ্র ও অন্যান্য প্রান্তিক গোষ্ঠীকে লক্ষ্য করে। তবে, সেগুলি প্রায়ই নারীদের পর্যাপ্ত অংশগ্রহণ নিশ্চিত করতে ব্যর্থ হয়েছে।

প্রকৃতপক্ষে, ভারতীয় জনসংখ্যার জন্য সামাজিক সুরক্ষা সুবিধাগুলিকে সর্বজনীন করার প্রয়াসে ভারত সরকার ২০১৫–১৬ সালের বাজেটে পেনশন, জীবন বিমা ও ঝুঁকি বিমার উপর দৃষ্টি নিবদ্ধ করে একটি ত্রিত্ব ঘোষণা করে। প্রধানমন্ত্রী জীবন জ্যোতি বিমা যোজনা (২০১৫) ১৮–৫০ বছর বয়সী দরিদ্র ও সুবিধাবঞ্চিতদের জন্য একটি সামাজিক নিরাপত্তা ব্যবস্থা তৈরি করার লক্ষ্যে চালু করা হয়েছিল। কিন্তু এই কর্মসূচিতে মহিলাদের কার্যকর অংশগ্রহণ দেখা যায়নি। একইভাবে প্রধানমন্ত্রী সুরক্ষা বিমা যোজনায় (২০১৫), যা দরিদ্র এবং সুবিধাবঞ্চিতদের জন্য একটি বিমা প্রকল্প, নথিভুক্ত মহিলা সুবিধাভোগী মাত্র ৪১.৫ শতাংশ ৷ এমনকি প্রাথমিকভাবে ভারতে অসংগঠিত ক্ষেত্রকে সরকার সমর্থিত পেনশন প্রদানের লক্ষ্যে অটল পেনশন যোজনা (এ পি ওয়াই) (২০১৫)–র মতো সরাসরি হস্তান্তর প্রকল্পের ক্ষেত্রেও মহিলাদের নথিভুক্তিকরণ মাত্র ৪৪ শতাংশ৷

এই অর্থনৈতিক বৈষম্য এবং তার প্রভাব মোকাবিলায় অতীতে বেশ কিছু সামাজিক নিরাপত্তা প্রকল্প চালু করা হয়েছে, বিশেষ করে দরিদ্র ও অন্যান্য প্রান্তিক গোষ্ঠীকে লক্ষ্য করে।

এই পটভূমিতে, পুরুষ ও মহিলাদের মধ্যে অর্থনৈতিক বৈষম্য কমানোর জন্য আর্থিক বাজারে অন্তর্ভুক্তি আরও বেশি গুরুত্বপূর্ণ হয়ে ওঠে। আর্থিক পণ্যের নাগাল পাওয়া এবং তা ব্যবহারে লিঙ্গগত ব্যবধান প্রত্যক্ষ ও পরোক্ষভাবে অর্থনৈতিক বৈষম্যকে প্রভাবিত করতে পারে, এবং তা প্রায়শই উৎপাদনশীল সম্পদ অধিগত করার পথের অন্তরায় হয়ে ওঠে, স্বল্পমেয়াদে ব্যবসা সম্প্রসারণের সুযোগ সীমিত করে এবং মধ্য ও দীর্ঘ মেয়াদে শিক্ষা ও শ্রমশক্তির অংশগ্রহণে লিঙ্গ ব্যবধান স্থায়ী করে। আর্থিক বাজারে নারীদের অন্তর্ভুক্তি তাদের আয় প্রদানকারী জীবিকা সংক্রান্ত কর্মকাণ্ডে নিয়োজিত হওয়ার ক্ষমতা বাড়াতে পারে, যা পরিবার ও সম্প্রদায়ে তাদের সামাজিক মূলধন বৃদ্ধি করে। সম্পদ সৃষ্টি, পোর্টফোলিও বৈচিত্র্যকরণ এবং ঝুঁকি ব্যবস্থাপনার জন্য নারীদের দক্ষ আর্থিক সরঞ্জাম সরবরাহ নারীর ক্ষমতায়ন এবং দারিদ্র্য হ্রাস করতে পারে।

যদিও ভারত তার আর্থিক বাজারে লিঙ্গ বৈষম্য বন্ধ করার প্রতিশ্রুতি দিয়েছে, এবং সেগুলিকে ডেনারাউ অ্যাকশন প্ল্যান বাস্তবায়নের মাধ্যমে অন্তর্ভুক্তিমূলক করে তুলেছে, প্রকৃত ফলাফলের ক্ষেত্রে অগ্রগতি কিন্তু পিছিয়ে রয়েছে। প্রধানমন্ত্রী জন ধন যোজনা (পি এম জে ডি ওয়াই)–র অধীনে জন ধন ব্যাঙ্ক অ্যাকাউন্টের বৃদ্ধি আর্থিক পরিষেবাগুলিতে প্রবেশ প্রসারিত করেছে, এবং ভারতীয় জনসাধারণের আর্থিক স্বাধীনতাকে উন্নত করেছে। ২০১৭ সালে ভারতে যত মহিলা জানিয়েছিলেন তাঁদের একটি ব্যাঙ্ক বা অন্য কোনও আর্থিক প্রতিষ্ঠানে অন্তত একটি অ্যাকাউন্ট আছে, তাঁদের শতাংশ ছিল ৭৭ ৷ অল ইন্ডিয়া ডেট অ্যান্ড ইনভেস্টমেন্ট সার্ভে (এ আই ডি আই এস) অনুযায়ী ভারতজুড়ে প্রায় ৮১ শতাংশ মহিলার ব্যাঙ্কে ডিপজিট অ্যাকাউন্ট আছে। অ্যাকাউন্টের মালিকানায় লিঙ্গের ব্যবধান কমে গেলেও অ্যাকাউন্টগুলির ব্যবহারের ক্ষেত্রে ব্যবধান বেশি ছিল। অনেক ক্ষেত্রে মহিলারা ব্যক্তিগত অ্যাকাউন্টের মালিক হলেও সেগুলি নিয়মিত ব্যবহার করেন না। রিপোর্ট অনুযায়ী ৫৫ শতাংশ মহিলা এখনও সক্রিয়ভাবে তাদের পি এম জে ডি ওয়াই অ্যাকাউন্ট ব্যবহার করেন না। ভারতীয় মহিলাদের ডিজিটাল আর্থিক পরিষেবাগুলি ব্যবহারে ধীরগতির জন্য ডিজিটাল অ্যাক্সেস এবং ব্যবহারের ক্ষেত্রে বড় ধরনের লিঙ্গ ব্যবধানকে দায়ী করা যেতে পারে। পুরুষদের তুলনায় মহিলাদের ব্যক্তিগত মোবাইল ফোনের মালিকানা ২০ শতাংশ কম, এবং ইন্টারনেট ব্যবহারও ৫০ শতাংশ কম। মাত্র ১৪ শতাংশ ভারতীয় মহিলা স্মার্টফোন ব্যবহার করায় মহিলাদের ডিজিটাল আর্থিক পরিষেবার ব্যবহার উল্লেখযোগ্যভাবে প্রভাবিত হয়।

তবে সম্পদের মালিকানায় বড় লিঙ্গগত ব্যবধান, ক্রমাগত বেকারত্ব, কম মজুরি, সীমিত বছর স্কুলে পড়াশোনা, অবৈতনিক যত্নের কাজে সময় বিনিয়োগ, নিরাপত্তার উদ্বেগ এবং সামাজিক–সাংস্কৃতিক সীমাবদ্ধতার মতো কাঠামোগত সমস্যাগুলিও মহিলাদের আর্থিক অন্তর্ভুক্তির ক্ষেত্রে বড় বাধা তৈরি করে। বন্ধক রাখার মতো সম্পদের অভাব নারীদের আনুষ্ঠানিক ব্যাঙ্কগুলির কাছে উচ্চ–ঝুঁকিপূর্ণ ঋণগ্রহীতায় পরিণত করে, এবং তাদের মধ্যে ঋণ দেওয়ার অনীহা তৈরি করে। চাহিদার দিক থেকে, নারীর ক্ষমতায়ন ও সচেতনতা এখনকার মতো কম থাকার পরিবর্তে যদি বেড়ে যায়, তবে তা আর্থিক পণ্য ও পরিষেবার ক্রয় বাড়াতে পারে।

উন্নয়নশীল ভারতীয় আর্থিক বাজারে একটি লিঙ্গ সংবেদনশীল পদ্ধতি অবলম্বন করা হলে তা আরও বেশি নারীকে মূলধারায় আনতে সাহায্য করতে পারে। প্রথম পদক্ষেপ হিসাবে, মহিলা ব্যাঙ্কিং সংবাদদাতাদের একটি সুস্থ নেটওয়ার্ক বজায় রাখা, এবং তার পরিপূরক হিসাবে উপযুক্ত সহায়ক পরিকাঠামো তৈরি করা হলে তা ব্যাঙ্কগুলিতে মহিলাদের গতিশীলতাকে উৎসাহিত করবে। গতিশীলতার সমস্যাগুলি আরও ভাল করে সমাধানের জন্য মোবাইল আর্থিক পরিষেবাগুলি ক্রমবর্ধমানভাবে উপলব্ধ করা এবং ব্যবহারযোগ্য করা যেতে পারে, যাতে মহিলারা তাঁদের বাড়ি থেকে লেনদেন পরিচালনা করতে পারেন।

আরেকটি বড় উদ্বেগ হল ভারতীয় মহিলাদের দ্বারা ডিজিটাল আর্থিক পরিষেবাগুলির ব্যবহারে ধীরে ধীরে এগনো৷ মোবাইল ও টেলিকম ব্যবসার ব্যাপক ও গভীর অনুপ্রবেশের জন্য পরিপূরক ব্যবস্থা গ্রহণ করা উচিত, যাতে আরও ভাল ডিজিটাল পরিষেবাগুলিতে মহিলাদের অন্তর্ভুক্তি আদর্শ স্তরে নিয়ে যাওয়া যায়।

গতিশীলতার সমস্যাগুলি আরও ভাল করে সমাধানের জন্য মোবাইল আর্থিক পরিষেবাগুলি ক্রমবর্ধমানভাবে উপলব্ধ করা এবং ব্যবহারযোগ্য করা যেতে পারে, যাতে মহিলারা তাঁদের বাড়ি থেকে লেনদেন পরিচালনা করতে পারেন।

তৃতীয়ত, নারীদের লক্ষ্য করে আর্থিক পণ্য ডিজাইন করার জন্য একটি ক্লায়েন্ট–কেন্দ্রিক পদ্ধতির প্রয়োজন হবে, তবে তার জন্য নারীদের উপর গবেষণা চালিয়ে তাঁদের অর্থ, আর্থিক পণ্য এবং প্রযুক্তির সঙ্গে ক্রিয়া–প্রতিক্রিয়া ও সম্পর্ক অধ্যয়ন করতে হবে, এবং তার মধ্যে আঞ্চলিক ও সামাজিক–সাংস্কৃতিক বৈচিত্রের বিষয়টিও মাথায় রাখতে হবে। আঞ্চলিক ভাষায় যোগাযোগ, এবং ভয়েস ও ভিডিও এনেবলারের মতো উপাদান ডিজাইন করা গেলে তা নারী এবং প্রযুক্তির মধ্যে বিদ্যমান দূরত্ব কমাতে পারে।

চতুর্থত, প্রাতিষ্ঠানিক স্তরে জেন্ডার বাজেটিং এবং লক্ষ্যমাত্রা নির্ধারণ সরকারি প্রকল্পগুলির নকশা পরিবর্তনে সক্ষম করতে পারে, যা মহিলাদের নির্দিষ্ট চাহিদা এবং পছন্দগুলির খেয়াল রাখবে এবং আর্থিক পণ্যগুলিতে তাদের অধিকার বাড়াবে। এই ধরনের আর্থিক পণ্যগুলিতে আয় ও খরচজনিত সিদ্ধান্ত সম্পর্কিত নিয়ন্ত্রণ এবং গোপনীয়তার একটি বৃহত্তর মাত্রা থাকা উচিত।

পঞ্চম, ডিজিটাল সাক্ষরতার পাশাপাশি ব্যাঙ্কিং সচেতনতা আরও ব্যাপক হওয়া দরকার। ব্যাঙ্কিং সচেতনতা ক্ষুদ্র সঞ্চয়কে একত্রিত করতে এবং দূরতম মহিলা ব্যবহারকারীদের কাছে তা পৌঁছে দিতে সাহায্য করতে পারে। এই কর্মসূচিকে এগিয়ে নিয়ে যেতে ভারতীয় রিজার্ভ ব্যাঙ্ক (আর বি আই) ইতিমধ্যেই একটি ‘আর্থিক শিক্ষা উদ্যোগ‘ চালু করেছে।

সবশেষে, নীতি সংস্কার এবং পণ্য ও পরিষেবা তৈরির জন্য, এবং বিশেষ করে তা নিম্ন আয়ের পরিবারের মহিলাদের উপযোগী করার জন্য, লিঙ্গভিত্তিক ডেটা উপলব্ধ করা এবং ব্যবহার করা জরুরি। উদাহরণস্বরূপ, লিঙ্গভিত্তিক ডেটার ব্যবহার আর্থিক পরিষেবা প্রদানকারীদের প্রধানমন্ত্রী জন ধন যোজনা (পি এম জে ডি ওয়াই) –র অধীনে বিশেষভাবে মহিলাদের উপর দৃষ্টি নিবদ্ধ করতে সাহায্য করতে পারে, বিশেষত প্রান্তিক অংশের মহিলাদের উপর৷ তাই আর্থিক অন্তর্ভুক্তির বিভিন্ন মাপকাঠিগুলির উপর এই ধরনের তথ্যের পর্যায়ক্রমিক প্রকাশ নীতিনির্ধারকদের নীতি নকশা ও তার বাস্তবায়নের সময় লিঙ্গ ব্যবধানের হদিশ রাখতে সাহায্য করবে। আর্থিক পরিষেবা প্রদানকারীদের নারীকেন্দ্রিক পণ্য তৈরি করতেও তা সাহায্য করবে।

প্রাতিষ্ঠানিক স্তরে জেন্ডার বাজেটিং এবং লক্ষ্যমাত্রা নির্ধারণ সরকারি প্রকল্পগুলির নকশা পরিবর্তনে সক্ষম করতে পারে, যা মহিলাদের নির্দিষ্ট চাহিদা এবং পছন্দগুলির খেয়াল রাখবে এবং আর্থিক পণ্যগুলিতে তাদের অধিকার বাড়াবে।

উপযুক্ত সংস্কার, উদ্ভাবন ও অনুশীলনের মাধ্যমে ভারতে আর্থিক অন্তর্ভুক্তিতে লিঙ্গ ব্যবধান হ্রাস কিন্তু অর্থনৈতিক বৈষম্য মোকাবিলায় একটি গুরুত্বপূর্ণ ভূমিকা পালন করতে পারে, এবং তার ফলে মহিলারা বৃদ্ধি ও উন্নয়নের অগ্রগতিতে আরও সক্রিয় ভূমিকা পালন করতে পারেন৷ অধিকন্তু, এস ডি জি কাঠামোর অন্তর্নিহিত আন্তঃসম্পর্কের মধ্যে দেখা যাচ্ছে যে এস ডি জি ৫–এর উন্নতিগুলি দারিদ্র্যমুক্তি (এস ডি জি ১), খাদ্য ও পুষ্টি নিরাপত্তা (এস ডি জি ২), সুস্বাস্থ্য (এস ডি জি ৩), শিক্ষা (এস ডি জি ৪), উন্নত স্যানিটেশন (এস ডি জি ৬) ও পরিচ্ছন্ন শক্তির (এস ডি জি ৭) ক্ষেত্রে উন্নয়ন নিয়ে আসবে, এবং অর্থনৈতিক প্রবৃদ্ধি ও বৈষম্যের মাত্রাকে সরাসরি প্রভাবিত করবে। মহিলাদের বর্ধিত সক্রিয়তা এবং অর্থপূর্ণ অংশগ্রহণ নিশ্চিত করা সমস্ত টেকসই উন্নয়ন লক্ষ্যগুলির অনুসারী সামগ্রিক অগ্রগতির বিকাশে মুখ্য ভূমিকা পালন করতে পারে, এবং তা ভারতের জন্য একটি শক্তিশালী এবং আরও স্থিতিস্থাপক ভবিষ্যৎ গড়ে তুলতে পারে।

মতামত লেখকের নিজস্ব।

The views expressed above belong to the author(s). ORF research and analyses now available on Telegram! Click here to access our curated content — blogs, longforms and interviews.

Debosmita Sarkar is an Associate Fellow with the SDGs and Inclusive Growth programme at the Centre for New Economic Diplomacy at Observer Research Foundation, India. Her ...

Read More +