Introduction

Economies across the world plunged into deep contractions in the April-June quarter of 2020. For India, the fall in real GDP (Gross Domestic Product) in the quarter was the record lowest at 23.9 percent, with the Reserve Bank of India (RBI) calling it “historic technical recession”.[1] The contraction continued in the second quarter at -7.5 percent.[2] If this “technical” recession persists in the third quarter of this fiscal year, it could turn into a full-fledged recession – the fourth since independence, first since liberalisation, and possibly the worst in history.[a]

Even before the pandemic, the economy was already slowing down, with deficiencies evident in both consumption and investment demand. Unlike some other countries, consumption and investment have been the main drivers of growth in India in recent times. Though export contributed in earlier versions of India’s growth story, in the immediate aftermath of the pandemic its efficacy to boost growth needs to be closely observed.

Despite repeated attempts to bolster manufacturing, the sector failed to grow, leaving services to step up. Eventually, lack of demand hit all segments irrespective of their economic nature. The pandemic, as an external shock, has finally contracted the economy.

It is a widely held view that every crisis also presents an opportunity. Given the prevalence of inequality in Indian economy, the implementation of a fiscal stimulus across sectors will not only lift the economy out of the woods, but also address some of the existing distortions in income and wealth distribution.

This paper analyses the growth trends in broad macroeconomic fundamentals of the Indian economy since 2012-13, bringing out the issues around aggregate demand in the last few years.

Analysts have debated the nature of the downturn that was observed before the pandemic; the basic contention was whether it was cyclical or structural. The pandemic (as an external shock) and the ensuing economic crisis rendered these debates redundant – at least in the short run – as both consumption and investment demands crashed for anybody to see. This paper does not attempt to address the long-standing structural issues and bottlenecks plaguing the economy. Rather, it concentrates on immediate demand recovery and thereby a return to “normalcy” in the economy. The paper offers specific proposals for an immediate fiscal stimulus-driven recovery path, and cautions that any further delay may affect the economic structures in a chronic way.

The paper focuses on the recent slowdown that started around 2018-19, using quarterly data series with the base year 2011-12 – as provided by the Ministry of Statistics and Programme Implementation (MoSPI). The back series is consciously not used.[b] Therefore, the analysis and discussion revolve around the time period between 2011-12 and present. As growth rates are calculated by comparing with the value prevailing in the same quarter of the previous year, most of the diagrams will show the growth rates beginning 2012-13.

Pre-pandemic Economic Slowdown: An Overview

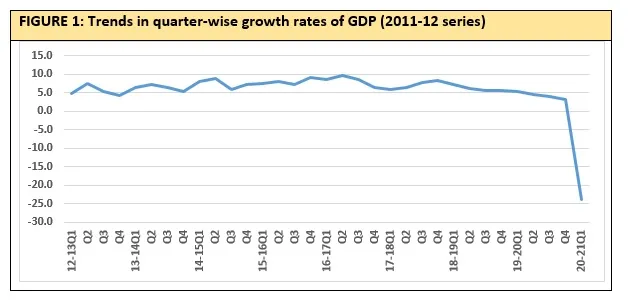

In the first quarter (Q1) of 2020-21, GDP at constant (2011-12) prices contracted by 23.9 percent while GVA (gross value added) at constant prices contracted by 22.8 percent.[3] The quarter coincided with the nationwide lockdown to arrest the spread of COVID-19, beginning at the end of March and ending in early June. Even as the contraction was largely expected, however, the nearly 24 percent fall in GDP still came as a shock to many (See Figure 1).

The COVID-19 pandemic is an external shock. For India, however, the downward slide started even before the pandemic caused a massive economic fallout. The lower panel diagram of Figure 1 excludes the GDP growth rate for the first quarter of 2020-21. The trendline tells the story: since Q1 of 2018-19, quarterly GDP growth rate (change over the same quarter in previous year) has been sliding downward. The last quarter of 2019-20 saw a growth rate of 3.1 percent, less than the 4.3 percent of the last quarter in 2012-13.

Analysts have noted such slide in GDP since 2018-19, and have offered two broad streams of explanation: one set related to structural weaknesses, and another to cyclical problems. While the first emphasised the supply-side bottlenecks, the latter focused on demand.

The structuralist paradigm held that the slowdown (before pandemic) is a continuation of the 2012-13 crisis, with lack of adequate structural administrative reform resulting in a repeat of the same crisis.[5] Former RBI governor Raghuram Rajan had also underlined structural constraints like labour and land restrictions, and governance issues.[6] Another view links the lack of consumer demand with the absence of inclusive growth and resultant income inequality.[7] Whenever the incomes of the top earners of the economy suffer, domestic demand falters; the rest of the earners’ incomes are low and thus unable to prop up domestic demand in any significant manner.[8]

Moreover, internal policy mismanagement has also been pointed as one of the possible reasons for the downturn.[9] Nobel laureate Abhijit Banerjee has said that demonetisation and implementation of the Goods and Services Tax (GST) were plausible causes of the slowdown.[10] Other economists have also drawn attention to agricultural distress. Such state of affairs has been a result of India’s failure to create higher productivity in agriculture and simultaneous inability to create higher productivity jobs in industry that could absorb surplus agricultural labour. This resulted in a fall in consumption demand in rural India.[11]

Furthermore, a higher interest rate regime, originating from inflation targeting policy of the RBI, has been periodically blamed.[12] An increasing trust deficit among the investors and the economic agents in the system about the institutions and the government have been mentioned by former Prime Minister Manmohan Singh and economist Kaushik Basu.[13]

Meanwhile, Arvind Subramanian and Josh Felman are of the view that the Indian economy has been weighed down by a combination of structural and cyclical factors. They argued that after the 2008 financial crisis, a twin balance sheet crisis arose in banks and infrastructure companies. With growth crumbling after 2018-19, the balance sheet crisis percolated in NBFCs and real estate companies. This four-balance sheet problem is pulling the economy further down.[14]

The pandemic has since made the structural-versus-cyclical debate largely redundant, at least in the short run. Around 60 percent of the global economy, which include 97 percent of advanced economies, have cut policy interest below 1 percent. As correctly pointed out by the Chief Economist of the International Monetary Fund (IMF), this implies that the world economy is now under a global liquidity trap. For all countries, boosting demand and climbing back to normalcy can only be done through the fiscal route.[15]

Already falling aggregate demand made the pandemic shock deeper

National income, or output, or GDP (Y) consists of private consumption (C), government consumption (G), investment (I) and net export — given by the difference between exports (X) and import (M). The national income identity is, thus, expressed as —

Y = C + I + G + (X-M)

This national income identity provides the level of aggregate demand existing in the economy. When aggregate supply meets this aggregate demand (of goods and services) the economy is generally said to be in an equilibrium. If the aggregate demand does not match the level of aggregate supply then output adjusts, in the next time period, to match the level of aggregate demand. In other words, if current level of aggregate demand is inadequate to buy all goods and services produced in the economy then producers will cut back their output (aggregate supply) to match the existing level of aggregate demand.[16]

This basic point is essential in the following analysis. If there is empirical evidence of a lack of aggregate demand in current Indian economy, then the only way through is via fiscal policy intervention, as we have seen in various points of the economic history of troubled economies – the last instance being in the aftermath of the 2008 financial crisis.

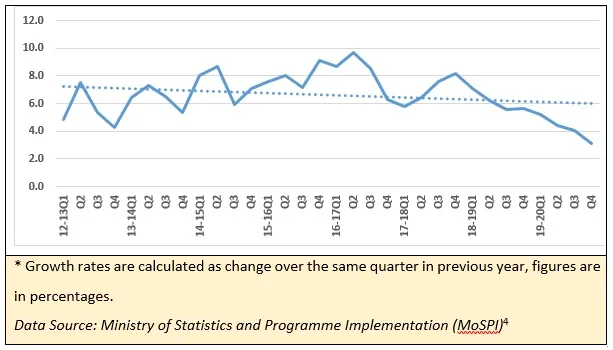

Consumption (C in the national income identity), termed as private final consumption expenditure (PFCE), is the first of the most important components of aggregate demand. Figure 2 shows a declining trendline for quarterly growth of this component. In Q1 of 2020-21, consumption growth rate has slumped by 26.7 percent, compared to the same quarter in the previous year. Excluding growth rate of Q1 of 2020-21 (lower panel of Figure 2), the line diagram reveals that long-term trend in consumption growth has stagnated in the last few years, and had fallen to 2.7 percent in the last quarter of 2019-20.

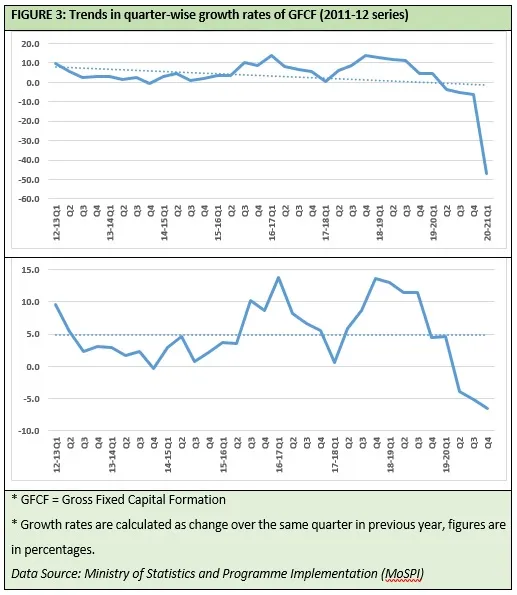

Investment (I in the national income identity), termed as gross fixed capital formation (GFCF), is the other important component of aggregate demand. The pandemic has sent investment growth crashing by 47.1 percent in the first quarter of 2020-21. Excluding this figure, the average trend value has stagnated around 5.0 percent in the last seven years (See Figure 3). The quarterly growth rate of investment started falling since first quarter of 2018-19 and has been -6.5 percent in the fourth quarter of 2019-20. This means that investment growth has been in a downslide for the last two years, even before the pandemic.

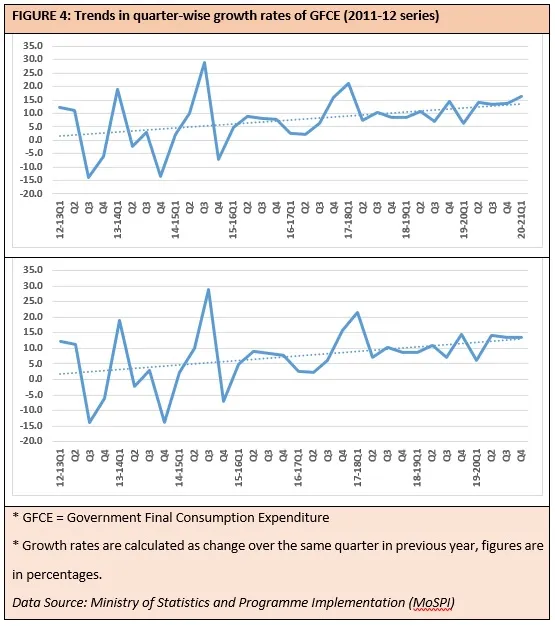

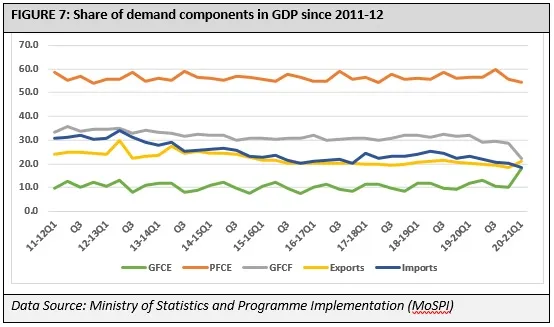

Government final consumption expenditure (G in the national income identity) is the next component in aggregate demand. Trendline of quarterly growth rate of G is increasing for the last eight years, continuing to do so in the first quarter of 2020-21 at 16.4 percent (Figure 4). This is one component that has enabled the overall quarterly GDP growth rates to be in the positive zone in the last two years or so. But the share of government expenditure in total GDP, despite continuous rise in growth, has been 18.1 percent in first quarter of 2020-21. (Figure 7) It has reached its limits, and this component alone can no longer prop up the overall GDP.

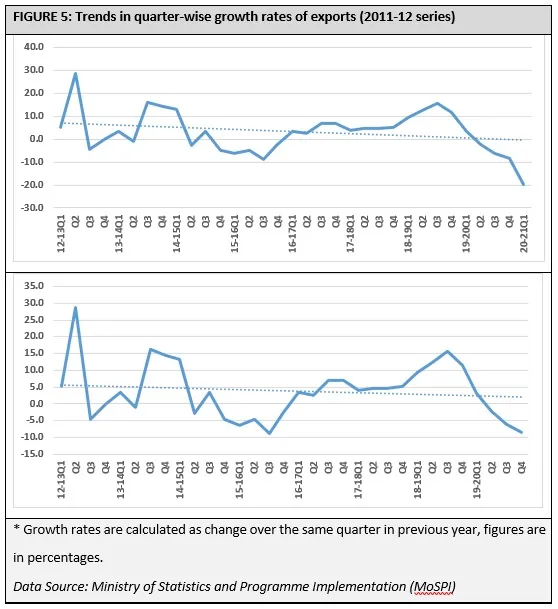

Net exports (X-M in national income identity), the difference between exports and imports, is the next important demand component of GDP. Given the last two years’ trade tension and turmoil in international trade, the exports growth was expected to decrease. Figure 5 confirms that expectation. Exports growth slumped by 19.8 percent in the first quarter of 2020-21, but even before the growth rates were negative in previous three quarters.

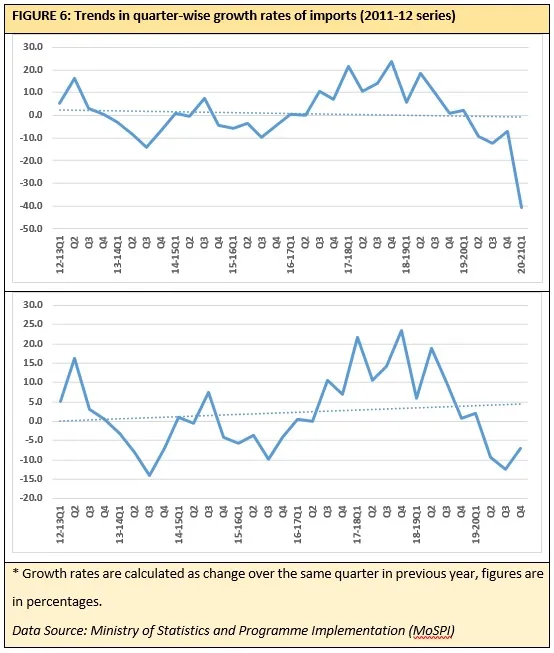

Similarly, imports were going down before the pandemic and the trend continues after (Figure 6). There may be a general perception that decreasing imports are good for an economy. It is not so for the Indian economy. Apart from crude oil imports, India imports sizeable amount of capital goods – mainly heavy machineries and equipment that are not produced in India. Indian manufacturing and other industries are crucially dependent on these capital goods. There has been no empirical evidence of large-scale import-substitution strategy in these capital goods in recent times. Unless import dependence is decisively diminished for these goods, the trendline going down does not serve Indian industry well.

Therefore, given the current composition and structure of Indian production net exports getting into positive value does not bode well for the economy. It implies lack of demand and diminishing activities in manufacturing and allied services. Any developing country needs a threshold warranted import growth to maintain sustainable output expansion, particularly in manufacturing. India is no exception. A certain amount of imports in capital goods is necessary to reboot. In that sense, imports going down and trade surplus going up right now cannot be treated as a good indication.

Subdued tendency in international trade will linger in the immediate future, making rapid growth in exports difficult – at least in the immediate short run. While it will be good if exports pick up eventually in a couple of years, banking on exports to revive the economy may not be a safe option.

As a more direct and safer intervention, domestic demand can be boosted immediately to revive the economy, and the parameters to look out for will be imports of oil and capital goods. If these parameters show an uptick soon, it will indicate a rebound in manufacturing and heavy industries.

Among the components of aggregate demand generators, consumption and investment are two largest contributors. In first quarter of 2019-20, these two contributed 88.4 percent in total GDP, in Q1 of 2020-21 their contribution is 76.6 percent. If the share of these demand components in new series of GDP are observed, then it becomes clear that consumption mainly drives the economy, followed by investment (Figure 7).

Since 2016-17, share of exports in GDP started hovering around 20 percent. Import’s shares have been slightly higher than exports. Exports can still be a growth driver in the near future, but that will require a few external factors falling in place for the Indian economy. The caveat lies in the fact that India is not in a position to sufficiently influence those external factors. While exports are not sufficient as a growth driver, an alternative strategy to keep the economy running needs to be undertaken.

Consumption and investment demand at close to 80 percent of the GDP are two most important contributors to GDP. No revival can take place if these two remain subdued or keep falling.

As earlier pointed out, net exports, as a demand driver, currently is in an uncertain zone. Though government expenditure shows steadily rising growth rates, it has contributed 18.1 percent in quarterly GDP of 2020-21 first quarter. Its contribution was 11.8 percent in the same quarter previous year. Government consumption on its own cannot revive the economy from its current contractionary phase.

To sum up this paper’s analysis of the aggregate demand components of the economy:

- Consumption demand is the largest contributor to GDP, and its growth was already stagnating before the pandemic. Any further deterioration will exacerbate the demand problem.

- Growth rates of investment demand, in a similar trend, plunged into the negative zone before the pandemic hit the economy. Before the pandemic, the economy was operating below full capacity and therefore an investment slump was largely expected.

- Government consumption expenditure rose steadily but it is not in a position to make up for the slump in previous two components.

- Net exports, as a demand driver, will not be able to revive the GDP in the short run if all other current global economic environment factors remain largely unchanged. There may be improvement in those external factors, but immediate prudence lies in not banking too much on that and subsequent miraculous revival of high export growth.

Growth Deficiencies in Key Sectors

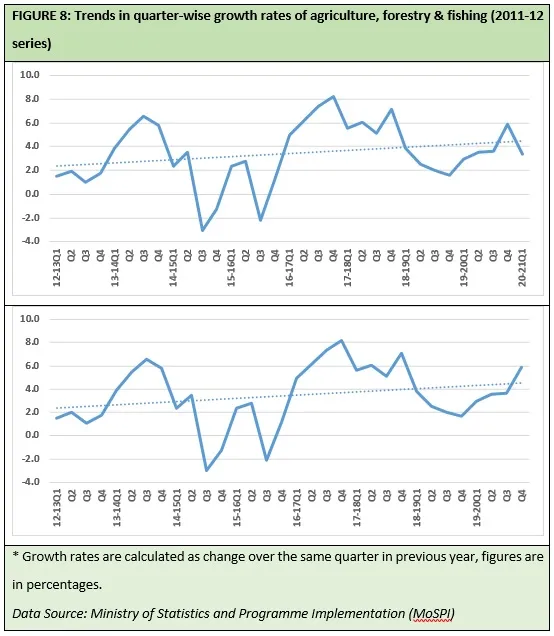

Quarterly estimates of GDP provide sectoral gross value added (GVAs) of eight principal sectors of the economy. If we look at the quarterly growth rates of agriculture, forestry and fishing, the growth trendline is steadily upwards in recent years. Though the pandemic has affected the sector adversely, it still managed to record a positive 3.4 percent growth in Q1 of 2020-21. It is the only principal sector to do so. All others have experienced negative growth rates in 2020-21 first quarter (Figure 8).

Agriculture, forestry and fishing had a growth rate of 5.9 percent in the last quarter of 2019-20. A repeat performance this year can ease the pressure on food supply chains and inflation. It is, thus, of paramount importance to let agriculture sector operate as much free of pandemic-induced restrictions as possible. Ensuring friction-free operation of logistics and supply chain of food articles will decide the movement of the future price indices.

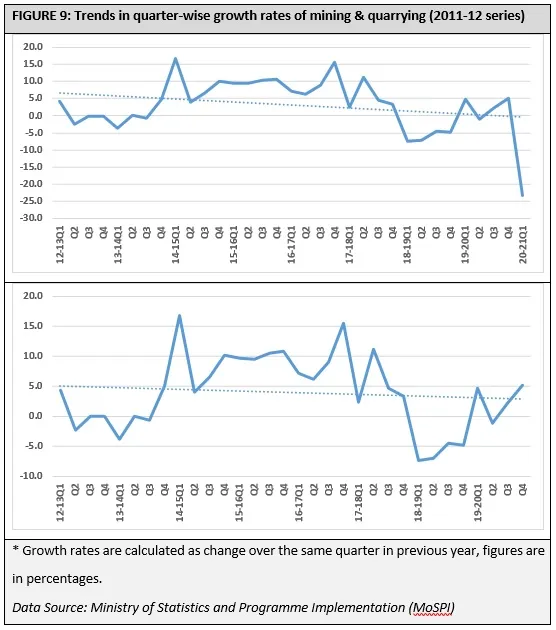

In recent times, Q4 of 2016-17 was a high point for the mining sector. Since then, the growth has gone downhill, it started crawling back towards normal growth trajectory in 2019-20 but then has been hit badly again by the pandemic and resultant restrictions (Figure 9).

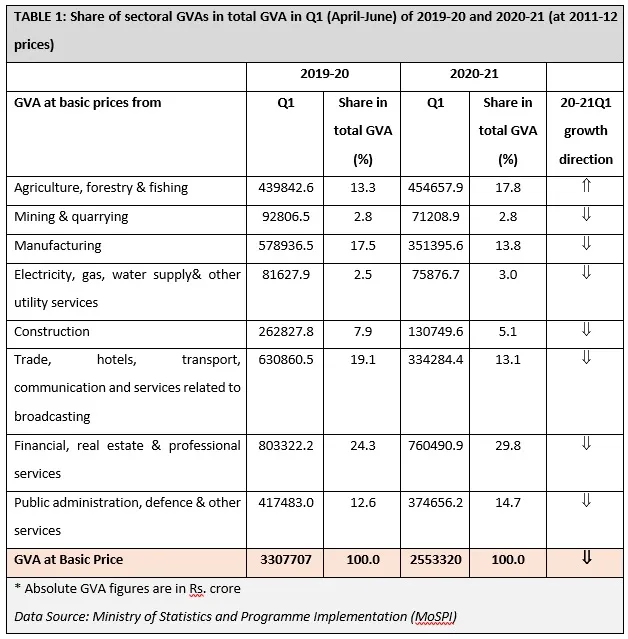

Saddled with operational difficulties and environmental concerns, the sector’s longer-term trend growth has been declining even before the pandemic started (lower panel of Figure 9). Relatively lower share in total GVA also implies its diminished ability to contribute to the revival (Table 1).

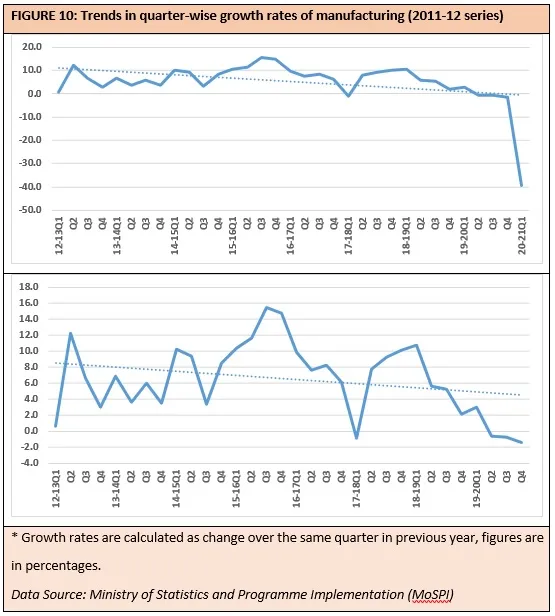

Manufacturing share in total GVA was 17.5 percent in Q1 of 2019-20 and has expectedly decreased to 13.8 percent in Q1 of 2020-21 during lockdown (Table 1). Manufacturing quarterly growth rate has plummeted to -39.3 percent in Q1 of 2020-21. For consecutive eight quarters manufacturing quarterly growth rate has declined (Figure 10). This indicates towards a lack of demand on the one hand, and a deeper structural crisis in the sector which the pandemic has sufficiently worsened.

Here the point to be noted is that manufacturing cannot be assessed only by its share in GDP. This is the sector of the economy with maximum amount of backward and forward linkages. In simple words, a good manufacturing performance propels other sectors and vice versa. That is why manufacturing growth is considered to be important for a sustained economic recovery.

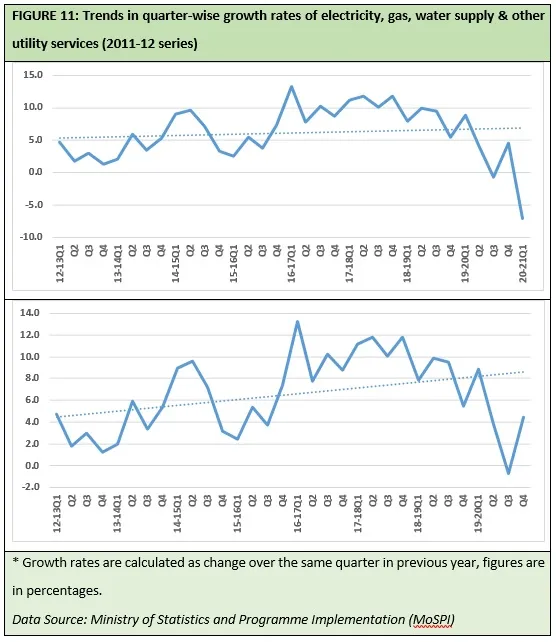

Electricity, gas, water supply and other utility services has clocked a negative quarterly growth rate of -7.0 percent in the first quarter of 2020-21 (Figure 11). National lockdown was initiated by the end of March and was only lifted in the month of June. Therefore, this negative growth in utility services was expected.

In the coming days, this sector is expected to come back to normalcy faster as the longer-term growth trendline is positive. However, given relatively lower share of the sector in total GVA utility services cannot contribute heavily to the revival (Table 1).

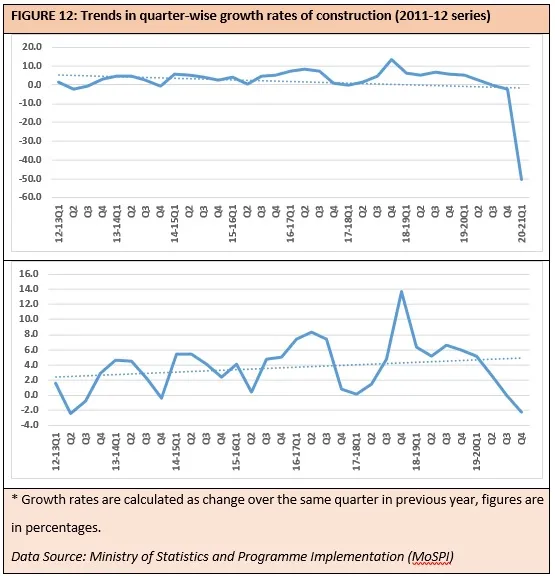

Construction sector’s share in total GVA was 7.9 percent in Q1 of 2019-20, it has fallen to 5.1 percent in Q1 of 2020-21 (Table 1). Longer-term trendline growth rate has been positive in the construction during recent years. However, the growth rates have been falling in last seven quarters and the growth rate in Q1 of 2020-21 decreased by 50.3 percent (Figure 12).

The lockdown and resultant restrictions stopped the construction work. This will be one sector where growth rate in the next quarter will be keenly watched as this is one of the sectors where there is sizeable amount of informal employment. If there are signs of immediate revival in this sector (which is quite possible), then that would help a faster recovery of the economy.

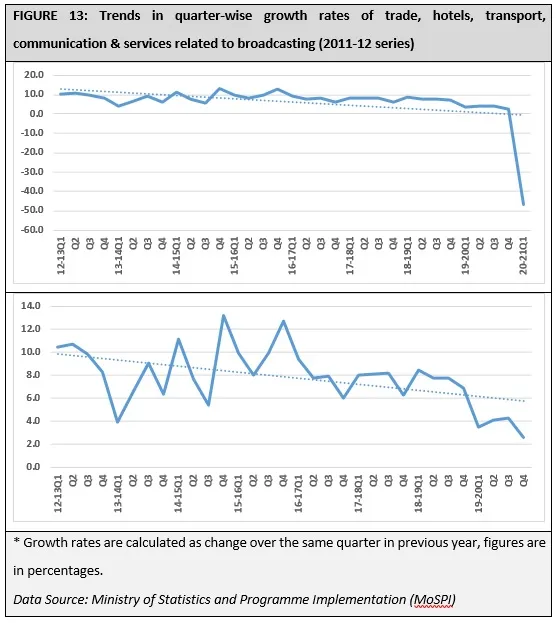

Trade, hotels, transport, communication, and services related to broadcasting is an important segment of the economy. Its share in total GVA was 19.1 percent in Q1 of 2019-20 but has fallen to 13.1 percent in Q1 of 2020-21 (Table 1). Moreover, along with financial, real estate and professional services this sector provides most of the services in the economy. Predominantly informal in nature, these two broad services segments provide employment to a vast part of the workforce of the country.

Unfortunately, this sector has slowed down in the last eight quarters, and the growth rate in Q1 0f 2020-21 has slumped by 47.0 percent (Figure 13).

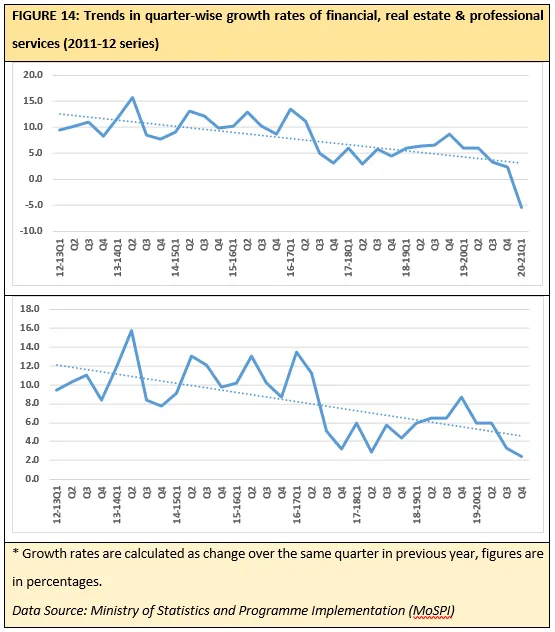

Financial, real estate and professional services is one of the principal sectors in the economy. The share of the sector in total GVA was 24.3 percent in Q1 of 2019-20, and despite clocking negative growth rates the sector has increased its share to 29.8 percent in Q1 of 2020-21 in the diminished GVA (Table 1). Therefore, revival of activity in this sector should be one of the major priorities.

The longer-term growth trendline in the last eight years or so, however, is consistently falling – even if one excludes the pandemic induced first quarter result in this fiscal year (Figure 14).

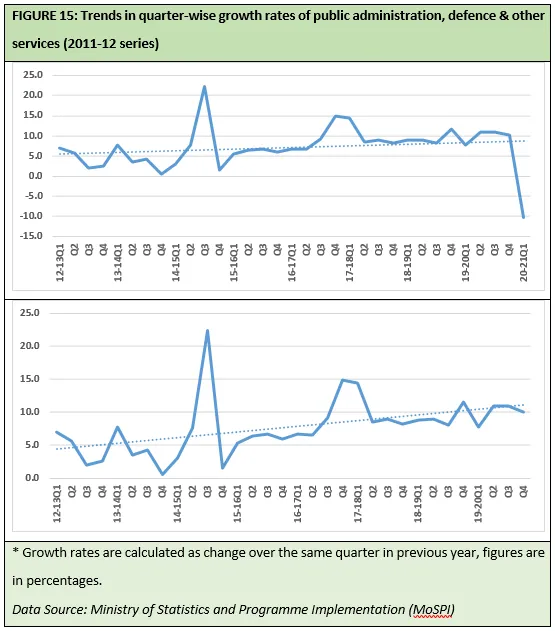

Public administration, defence and other services is another service sector segment. Unlike previous two service dominated sectors this segment consists of public sector service activities. This sector has experienced a 10.3 percent drop in growth rate in Q1 of 2020-21, but the long-term growth trend is positive. That gives rise to the expectation that after restrictions are lifted this sector should come back to normalcy faster than the others (Figure 15).

Out of principal eight sectors of the economy, only agriculture, forestry and fishing showed positive rate of growth in the first quarter of 2020-21. The fall in growth rates is relatively less for electricity, gas, water supply and other utility services, and financial, real estate and professional services sector. These are the sectors that can lead the gradual revival of the economy – particularly the financial, real estate and professional services sector. However, performance of these sectors is always intertwined with the real sector. If industrial and other productions flourish, these sectors will subsequently attain a sustainable positive trend.

As GDP shrunk by 23.9 percent in this quarter, the share of the less affected sectors in total GVA have also increased (Table 1). Some sectors like agriculture and tourism are seasonal, and therefore less impact on some of these may be owing to seasonal factors. However, manufacturing, trade, hotels, transport, communication and broadcasting services, and construction are the key sectors which have to drive the revival. Under the current structure of Indian economy, nobody would expect the revival to be driven by agriculture and/or public utility services and/or public administration services.

To sum up the evaluation of the eight principal sectors of the economy:

• Agriculture, forestry and fishing is the only sector with positive growth. This is a good development for the economy, but revival cannot be agriculture-based under current circumstances. Manufacturing has to come out of its slowdown.

• Financial, real estate and professional services are relatively less badly affected and should recover in reasonable time. But the recovery will be dependent on industrial and consumer demand recovery.

• The same is true for construction and internal trade, tourism, transport, communication sectors. Though construction shows signs of rebound, tourism is likely to suffer the most. That may eclipse some possible gains in communication during the pandemic. However, till the detailed sectoral data are available, overall revival of this bouquet of some important large sectors of the economy will be dependent on real sector activities and how these sectors cope up with periodic disruptions due to the pandemic.

• Electricity, gas, water and public utility services and public administration, defence and other services are likely to get back to normalcy sooner than other sectors. But these cannot propel economy into the desired growth path alone, and once again long-term stability in these sectors will depend upon overall revival.

The Failures of Relief Measures

Announced in May with a headline-grabbing figure of INR 20 lakh crore, India’s fiscal stimulus package did not have enough fiscal firepower to boost demand. It was evident from different estimates of the actual fiscal cost to the Central Exchequers, calculated by various banks, brokerages, and rating agencies (Table 2).

Source: The Times of India Business,[17] CRISIL[18]

Estimates of actual fiscal cost, as percentage to GDP, ranged from 0.75 percent to 1.30 percent but nowhere close to the claimed 10 percent of GDP figure. Making credit available and re-packaging existing government schemes were the highlights of the package.

In any recessionary situation, money needs to be directly pump-primed into the system – mainly to boost immediate consumption and investment. Boosting immediate economic activities by investing public capital enhances the purchasing power of the people in the economy, that purchasing power then is spent on consumption, that consumption boosts demand and instantly productions are augmented to meet that extra demand which creates more purchasing power in the economy. This cycle goes into the upper spiral and takes the economy out of recession. That is how investment multiplier works in any economy. Monetary interventions usually have little immediate effect on the economy.[19]

Even in its October monetary policy, the government stance of relying on increased credit supply instead of going for an all-out fiscal intervention has been quite evident. The central bank assured both the market and the government of creating comfortable liquidity conditions so that private and government borrowing are not hampered in any way. The following crucial liquidity enhancement announcements were made.

• To revive activities in specific sectors with both backward and forward linkages and multiplier effects on growth, the RBI has introduced on-tap targeted long-term repo operations (TLTRO) with tenures of up to three years for a total amount of up to INR 1 lakh crore, at a floating rate linked to policy repo rate. Liquidity availed by the banks under this scheme must be deployed in corporate bonds, commercial papers and non-convertible debentures issued by entities in the growth-oriented sectors.

• The liquidity availed by these TLTROs can also be utilised to extend bank loans to the growth-oriented sectors. The banks which have raised funds under earlier TLTROs will be given option of reversing these transactions before maturity. This is done to ensure smooth and seamless credit operation by the banks.

• Reacting to “feedback from market participants”, the central bank also decided to increase the size of special open market operations (OMOs) to INR 20,000 crore.

• To facilitate liquidity to state development loans (SDLs), the RBI would conduct OMOs in SDLs as a special case during the current financial year. The apex bank expects to facilitate efficient pricing by undertaking these operations.

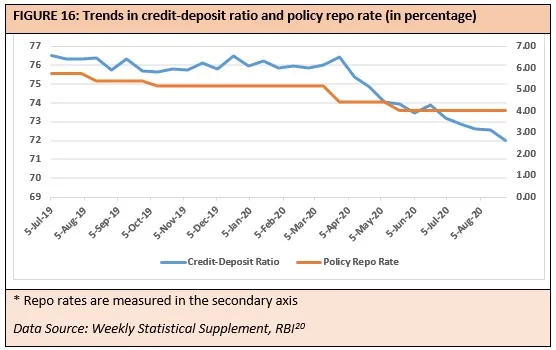

The idea that increasing credit supply will facilitate economic revival still prevails above everything else. The pandemic-induced massive GDP contraction has only accelerated the clamour. Its underlying logic is simple – making low-cost loanable fund available would increase credit offtake, those credits taken (industrial, personal, or otherwise) would then be utilised in new economic activities, and finally would result in heightened revival and growth. However, if one looks at the trends in the policy repo rates and credit-deposit ratio in the last one year, then a scepticism is bound to emerge.

The credit-deposit ratio shows how much of each rupee of deposit is extended as actual credit disbursal. Broadly, this is one of the basic credit growth indicators. Though policy repo rate has continuously fallen in the last few years, the credit-deposit ratio has remained constant and since April 2020 has plummeted during the pandemic (Figure 16). Though the cost of borrowing has consistently fallen down, and more credit were made available to the economy, there were few takers of such loans.

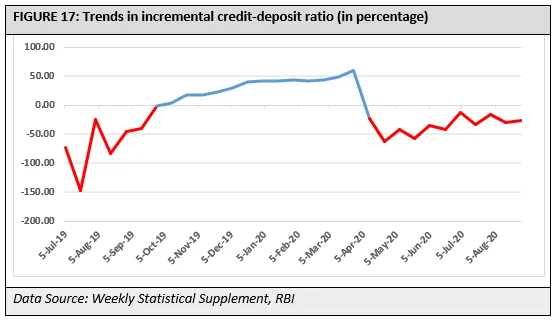

The slump in credit demand becomes prominent if we look at the trends in incremental credit-deposit ratio. As the name suggests, this ratio shows how much of new deposits are extended as new credit in the economy. This ratio was in the negative territory in the period between July and September 2019, it slowly revived to a level of around 60 percent in March 2020, and slumped thereafter to get into the negative zone once again (Figure 17). To provide a contrast, the value of this ratio was 169.70 percent on 21 December 2018, 126.29 percent on 18 January 2019, and 116.01 percent on 15 March 2019.

Deposit growth rates have been steady even during the pandemic, but there was no commensurate growth in credit. Incremental credit-deposit ratio figures only reaffirm that phenomenon. Figure 17 shows that this trend started much before the pandemic.

Therefore, credit demand is the problem, and not credit supply. If there are few economic actors in the system interested in taking credit and employ those in productive activities, no amount of additional credit supply will be able to solve that problem.

If the malady is entrenched in the demand side, then monetary supply remedies seldom work out. Fiscal solutions only can take care of the demand-side distortions. The time has come to look for those avenues.[21]

A Blueprint for Economic Revival

Prevailing global trade tensions of the last two years and the huge external shock of the COVID-19 pandemic have initiated discussions on self-reliance. Propagating a self-reliant Indian economy assumes an inward-looking future global economy. However, there is a contradiction in that proposition. If every country strives to import less and export more, then international trade would be shrinking. That further implies reduction of exports for all major exporting countries. A deeper introspection is required.

India posted the world’s third highest growth rate in overall and manufacturing exports, since the early 1990s. Contrary to popular perceptions, India did reasonably well in high-skill manufacturing exports while it underperformed in low-skill manufacturing exports.[22] The country is still in a position to gain future export opportunities, particularly in low-skill manufacturing like clothing and footwear. Grabbing those future opportunities entail more global integration and trade engagement. Overemphasis on self-reliance may be inimical to that. Losing export as an important future driver of growth would be imprudent, to say the least.[23]

However, in the revival blueprint proffered by this paper, export is largely untouched for two principal reasons. First, the WTO in October has forecasted a 9.2-percent decline in world merchandise trade volume for 2020. Though it predicts a 7.2-percent rise in 2021, October forecast about next year is more pessimistic than previous April forecast growth of 21.3 percent in 2021. The predictions also put a caveat by mentioning that “this (growth) is highly dependent on policy measures and on the severity of the disease”.[24] Therefore, this uncertainty around world trade volume growth is considered in these recommendations. As Europe and the US impose fresh lockdowns due to a second wave of the pandemic, the uncertainty grows and casts its shadow on global exports growth.

A second and more important reason for this omission is that Indian export trends are showing certain unusual characteristics, signifying distortion in production structure. Exploring those nuances is beyond the scope of this paper, and this analysis is focused on immediate revival through demand boosters. It does not imply, however, that export is ruled out as a possible driver for future growth in the long run.

The following paragraphs outline this paper’s seven-point blueprint for India’s economic revival.

1. Universalise PDS for a year

Expenditure on food, as percentage of total household consumption, was 33.2 percent in rural areas and 22.4 percent in urban areas in 2017-18.[25] The first fiscal intervention should be in making food available to as many as possible. That can free substantial amounts of purchasing power for other kind of consumptions. With inequalities remaining large within the structure of Indian economy, this pandemic can be an opportunity for redistributive measures – as argued by Amartya Sen.[26] Universalising the public distribution system (PDS) would be a good starting point.

According to Food Corporation of India (FCI) data, total stock of rice and wheat in central pool amounts to 70.03 million tonnes (MT) in September 2020. If unmilled paddy and coarse grain in the stock are added to that, grand total of foodgrains stock in central pool will be 81.11 MT.[27] Given this high level of foodgrains stock, a temporary universalisation of PDS can be undertaken. Roughly 66 MT foodgrains are needed to universalise PDS for six months, and the country has more currently.[28]

By the end of March 2020, the government announced Pradhan Mantri Garib Kalyan Ann Yojana (PMGKAY), under which additional 5 kg of grain per person and 1 kg of pulses per household were provided for free for three months. The objective was to cover 80 crore individuals under Antyodaya Anna Yojana ration cards, more commonly known as below poverty line (BPL) cards. However, that period has ended in June, and that very quarter saw almost 24 percent GDP wiped away.

Though this scheme has been extended till the end of November 2020, the restriction excludes sizeable population while the number of affected households is likely to be larger. Population estimates being currently used are outdated and there are other reasons for exclusion like lack of documents including Aadhaar, regional food disbursal quotas being reached, and issues related to logistics.[29]

In a country with monthly per capita net national income of INR 11,185.50, food security to most of the population has to be provided.[30] Expenditure on food is one of the principal expenses of any household. Covering that with universalisation of PDS can free money for other purchases.

A second reason is related to targeting cost. Instead of spending money on targeting, universalisation can sufficiently increase the coverage of the PDS for those who need it urgently. It can be assumed that those who have the wage protection will not take the trouble to queue up for a few kilograms of grains in a time of a pandemic. The leakages are also less in a universal PDS system. Tamil Nadu, with universal PDS, and Chattisgarh, with near-universalisation, are among the states with lower leakages in PDS.[31]

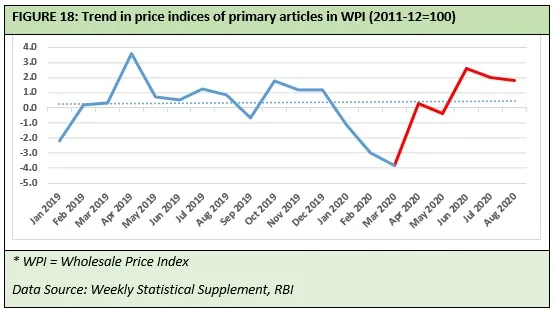

Third, given the upward movements in the prices of primary articles (mainly food), universal PDS has the capacity to keep the prices down (Figure 18). In a recessionary situation, that is an additional but no less important reason to universalise the PDS for next six months to one year.

Along with the government’s intent to launch “One Nation, One Ration Card”[32], this can go a long way to revive flagging consumer demand and ensure food security for a majority of the population.

2. Expanding employment guarantee to urban areas

After the migrant workers’ crisis during the lockdown, the focus has shifted to reverse migration. There are already reports of workers returning from their homes, where they could not find gainful employment. Incidentally, MGNREGA (Mahatma Gandhi National Rural Employment Guarantee Act) has already been used by more than 86 million people in the first half of 2020-21. This is the highest-ever utilisation of the scheme since its launch in 2006,[33] and the rural ecosystem of employment is under massive stress.

The movement of labour between urban and rural India has never been homogeneous—some migrate for the long term, while some for the short term.[34] The latter category can be called seasonal or circular. Given the sharp drop in GDP, opportunities in urban areas are also expected to shrink. It is of paramount importance that these circular migrants are absorbed into the urban employment set. But the absorption may not be an easy task when jobs are generally disappearing. Expansion of employment guarantee scheme in urban area is thus necessary to stabilise the economy.

The Odisha government has decided to bring the employment guarantee scheme in the urban areas. The state was expected to spend around INR 200 crore in 2020 for this purpose. Jharkhand and Himachal Pradesh have also announced similar urban work programmes to tackle urban unemployment.[35] However, the allocations in these state programmes are not adequate, and central government contribution can drastically improve their coverage.

Apart from boosting purchasing power and thereby consumption demand, this scheme has the potential to raise and stabilise urban wages. This can also create a stable national labour market by regularising inter-state migration that can continuously balance surplus and shortage in different labour markets. The scheme has the potential to create urban assets like environment-friendly green public spaces and can augment the existing central government endeavours like smart cities.

It is true that the scheme cannot be initiated everywhere immediately. But if there has ever been a dire need to start this measure, it is now. Around 10-15 non-metro cities can be targeted immediately on a pilot basis, with the express intent to expand it fast in next two years.

3. Direct cash transfer to affected populations

At the beginning of 2020, while introducing a bill to create a national database of informal workers in the parliament, it was mentioned that roughly 90 percent of the country’s workforce is in various informal sectors. There are other estimates projecting the number at 81 percent of workforce. If the National Accounts Statistics data is used, then there is 52.4-percent prevalence of informality in the workforce. According to World Bank data, Indian workforce size was 494,261,397 in 2019, and 52.4 percent of that would be 258,992,972. Therefore, the lockdown has affected close to 26 crore informal sector workers, in a conservative estimate.[36]

In India, roughly one-third of the population are engaged in some kind of work periodically. What it approximately means is that the remaining two-thirds are dependent on these workers. If a conservative 50 percent estimate of severely affected informal workers is made, even then 13 crore workers and another 26 crore dependents – a total of 39 crore people – would be considered under distress.[37]

The government’s March relief package of INR 1.7 lakh crore consisted of direct benefit transfer (DBT) to 80 crore population in various categories under Pradhan Mantri Garib Kalyan Yojana (PMGKY). However, out of this amount, INR 73,000 crore was the incremental amount, and the rest was already budgeted earlier in the year. SBI Ecowrap report estimated the total income loss of India’s 37.3 crore workers (self-employed, casual and regular) during the lockdown at around INR 4 lakh crore. The amount earmarked for DBT is inadequate. Moreover, some estimates put the reach of relief measures at around one-third of the country’s total migrant workers.[38]

In August 2020, the Centre for Monitoring Indian Economy (CMIE) reported a cumulative 18.9 million job loss among salaried people. In April, employment of around 403 million people have been affected, out of which 121 million lost their jobs.[39] Indeed, the stress is more widespread beyond the informal workers.

It would not be imprudent to say that more DBT is needed – covering more people. Earlier, economists like Abhijit Banerjee and Rathin Roy made strong arguments in favour of such transfer by saying that providing income support and preventing wealth disruptions are necessary to deal with this extraordinary situation. The pandemic has hit not only the poor, but also a sizeable section of the workers who do not have any kind of social security.[40] While it is true that identifying affected population is a difficult task, it will not be impossible, either, using Aadhaar and a coordinated effort between central and state governments. A temporary income support for six months through DBT can further augment consumption and aggregate demand in the economy.

4. Provide input tax relief to producers in selected sectors

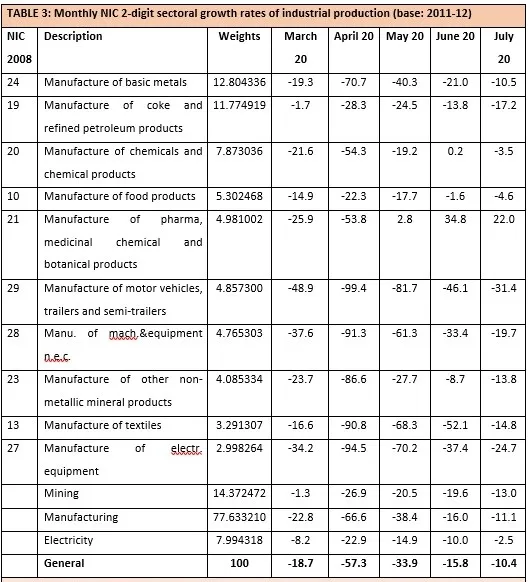

Quick estimates of Index of Industrial Production (IIP) and use-based index for the month of July 2020 reaffirms the fact that industrial production of the country remains in distress. The only large manufacturing segment that shows consistent positive growth rate in May–July period is pharmaceuticals. This was expected; tobacco is the only other sector that shows a positive growth in July 2020 (6.1 percent). All other sectors continue to show substantial contraction in production growth. The top 10 manufacturing sectors in terms of weightage in the index, totalling close to 63 percent, are mostly still showing double-digit growth contraction in the month of July (Table 3).

* n.e.c. = not elsewhere classified

* Figures for May20, June20 and July20 are provisional

Data source: Ministry of Statistics and Programme Implementation (MoSPI)

The problem is that the weightage of pharma in IIP is close to 5 percent and that of tobacco is 0.8 percent. Expecting these two sectors to pull up overall industrial production is like expecting roughly 6 people to pull up 94 others. If overall production has to improve, other sectors need to be revived as quickly as possible.

In these trying times for industry, the usual clamour is for corporate tax concessions. It will not work this time. The most important point to note is that the contraction has started in March 2020 – signifying already existing distress in Indian industrial production. The pandemic amplified it many times. Adverse unemployment consequences are also likely to increase in the coming days.

Therefore, the possible way through this recessionary trend in industry is to provide input tax concessions. Reducing or abolishing input taxes for some time (say, initially for a year) can be a starting point. It is quite comprehensible that the government is in no position to provide input subsidies to all sectors. The process may start with the top five manufacturing in terms of weightage – metals, oil, chemicals, processed food and automobile. Pharma can be, for the time being, kept out of this scheme. Once some of the initial beneficiary sectors revive themselves, those can be taken out and replaced by others – machinery & equipment, textiles, electrical equipment being the prominent among those.[41]

This can be an effective supply-side augmentation in addition to the demand inducing measures like DBT and urban employment guarantee. In totality then it can revive a good part of the investment demand.

5. Public investment in physical and social infrastructure

When the economy is suffering from lack of overall demand, it will be futile to expect that private investment will come to the rescue. Therefore, public investment – at least for some time – is necessary to crowd in private investment. India has a lack of infrastructure facilities that has been often cited as one of the major reasons behind the failure of industry, particularly manufacturing, to take off and reach a desired level.

Infrastructure has also been a key issue in the inability to attract sizeable amount of foreign direct investment. This crisis time may have created an opportunity to bridge that long-standing gap. Aggressive public investment on infrastructure for a year or two can help the efforts to revive the economy.

There have been expectations to attract manufacturing companies, which are leaving China, towards India. A growing infrastructure environment has the potential to add to that effort. Additionally, it will have a positive influence on future exports. Building infrastructure creates immediate employment and purchasing power, infusing demand into the system. Through multiplier effect, it can then feed into the future investment cycle as well. In the short to medium term, India has to rely on debt financing to boost public investment in order to revive the economy. Limited fiscal space will not allow India to go for a tax-financed model, which may adversely affect already flagging demand. A recent IMF report on infrastructure has mentioned this.[42]

Trends and nature of infrastructure investment is going to decide how fast the Indian economy can revive itself. The central government recognised this even before the pandemic when it unveiled the $1.5 trillion National Infrastructure Pipeline, based on Infrastructure Vision 2025, in December 2019. Strengthening and augmenting health infra, urban planning, roads, rural infra and digital infrastructure are going to be the key drivers even in the long run.[43]

A faster revival entails immediate public investment in all these areas of infrastructure.

6. Suspend FRBM for two years

At this juncture, quick decision making, and timely implementation of those decisions are the most important factors to get the economy back to the road of revival. To provide fiscal push to the economy, FRBM (Fiscal Responsibility and Budgetary Management) Act needs to be put on hold for two years.

The government has already made use of the flexibility enshrined in the FRBM Act under exceptional circumstances in 2019-20 and 2020-21 budgets, with targeted budget deficits put 0.5 percent (of GDP) higher than the FRBM mandated ones. Conforming with the FRBM leaves almost no fiscal space for any stimulus now. But there is always a case for suspension of the FRBM Act, as had been done during the 2008 global financial crisis.[44]

Latest estimates show that India has already breached the fiscal deficit target in 2019-20. It is currently estimated at 4.6 percent of GDP, well above the mandated target of 3.8 percent of GDP.[45] Therefore, it does not make economic sense not to undertake a stimulus programme because of FRBM. Currently the growth concerns clearly outweigh worries about future macro stability risks.

Suspending FRBM for two years should be the initial step to finance any fiscal revival attempt.

7. Monetise the central fiscal deficit

The fiscal element of the government’s economic package turned out to be a fraction of the announced figure. Estimates of actual fiscal stimulus by different entities like banks and credit rating agencies show the size of the economic package in the range of 0.8 percent to 1.3 percent of GDP. SBI Research has put the direct fiscal cost of the package at around INR 2 lakh crore or around 1 percent of GDP (Table 2).[46]

Back in April 2020, former CEA Arvind Subramanian, and John Hopkins University Professor Devesh Kapur have argued for a direct fiscal stimulus to the tune of INR 10 lakh crore, or 5 percent of GDP.[47] This was later endorsed by the FICCI Director General,[48] and the business newspaper Mint reiterated that proposition in their editorial.[49] The INR 10 lakh crore figure of direct fiscal stimulus subsequently found approval from a host of economists and public-policymakers.

If SBI fiscal cost estimate to government for March and May stimulus—at INR 2 lakh crore—is assumed as the real approximation of announced stimulus, then INR 8 lakh crore more needs to be provisioned. After fiscal spending measures announced in March (actual cost estimated to be roughly INR 1 lakh crore), the central government revised its borrowing requirement to INR 12 lakh crore in early May from the budgeted INR 7.8 lakh crore.[50]

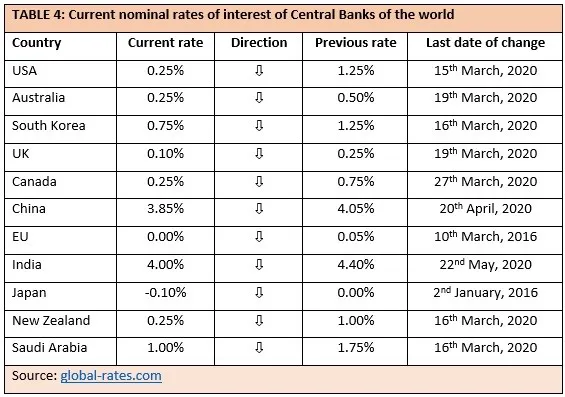

This analysis further assumes that this increased borrowing requirement, mostly from the open market, would take care of the March stimulus of roughly INR 1 lakh crore. That means INR 1 lakh crore more from the existing May stimulus needs to be funded, along with the proposed additional INR 8 lakh crore. To raise this additional INR 9 lakh crore, three fundamental methods can be undertaken. Before that, however, it would be helpful to take a look at the interest rate direction in major economies of the world (Table 4).

Except for Japan and the EU (both of which lost interest rate manoeuvrability long back), all other economies have slashed their rates substantially amidst the COVID-19 spread. For most of the developed countries and potential international debt markets, the rates are generally hovering near-zero level.

Therefore, an attempt can be made to tap these debt markets by the government; the NRIs can also be offered COVID bonds at floating rates – with the assumption that rates will be at lower level for some time. Rupee worsening in the foreign exchange market is indeed a risk—but one worth taking at this juncture. In the domestic market, however, there is a larger possibility of mobilisation of finance because many large funds, institutional and high net worth individuals, may opt for an assured return (guaranteed by government of India) COVID bond – even at a relatively lower rate of interest. An attempt to mobilise INR 2 trillion each in these three categories of overseas debt market and COVID bonds is a plausible option.

The remaining INR 3 trillion can be monetised – borrowed from the RBI at a fixed rate lower than the repo rate (ideally around 3.5 percent) and with longer duration (at least 10-year period). Till 1997, government deficit used to be automatically monetised at a rate much lower than the market rate. Now is the time to take a leaf out of that, albeit temporarily.

If the economy has to be revived, then a stimulus of this magnitude is necessary. Abiding by FRBM-mandated targets now may damage the economy badly, and then a lower fiscal deficit would not be able to help anybody next year.

References

Kabir Agarwal, “Six Charts Show that India Needs to (and Can Afford to) Universalise PDS”, The Wire, April 18, 2020.

Pulapre Balakrishnan, “Financial stability and the RBI”, The Hindu, October 15, 2019.

Kaushik Basu, “India and the Mistrust Economy”, The New York Times, November 6, 2019.

“India Fiscal Deficit Breaches Target to Hit 4.6% in FY20”, BloombergQuint, May 29, 2020.

“Covid-19: Experts seek income support, cash transfer for those affected”, Business Standard, June 3, 2020.

“Job losses among salaried employees likely to get worse”, Business Standard, August 22, 2020.

Samiran Chakraborty, “Suspend FRBM Act to allow fiscal stimulus”, Financial Express, March 23, 2020.

Shoumitro Chatterjee and Arvind Subramanian, “India’s Export-led Growth: Exemplar and Exception”, Working Paper no. 1, 2020, Ashoka Centre for Economic Policy

Shoumitro Chatterjee and Arvind Subramanian, “India’s Inward (Re)Turn: Is it warranted? Will it work?”, Policy Paper No. 1, 2020, Ashoka Centre for Economic Policy

CRISIL, “Minus Five”, May 26, 2020.

Harish Damodaran, “This is India’s first ever slowdown at a time of political as well as macroeconomic stability”, The Indian Express, November 30, 2019.

S Mahendra Dev and Ashima Goyal, “GDP measurement and the slowdown”, Business Standard, August 20, 2019.

“Reviving Indian economy: Does infrastructure hold the key”, ET Government, July 12, 2020.

Gita Gopinath, “Global liquidity trap requires a big fiscal response”, Financial Times, November 2, 2020.

“India needs stimulus package like US and direct cash transfer”, India today, May 5, 2020.

Shagun Kapil, “Cash, on delivery: How India has taken up DBT in the times of COVID-19”, Down To Earth, July 12, 2020.

Devesh Kapur and Arvind Subramanian, “Fiscal space: Not if but how”, Business Standard, April 12, 2020.

Ashok Kotwal and Pronab Sen, “What should we do about the Indian economy?”, The India Forum, October 17, 2019.

J Krishnamurty, “An Employment Guarantee for the Urban Worker”, Indian Journal of Labour Economics, 8 September (2020): 1-5.

Varun B Krishnan, “How much do Indians spend on food and other basic amenities?”, The Hindu, November 27, 2019.

Ministry of Consumer Affairs, Food & Public Distribution, Government of India, August 19, 2020.

Asit Ranjan Mishra, “Building infra via debt funds can revive India”, The Mint, September 28, 2020.

Ministry of Statistics & Programme Implementation, Government of India, May 29, 2020.

Ministry of Statistics & Programme Implementation, Government of India, August 31, 2020.

Ministry of Statistics & Programme Implementation, Government of India, November 27, 2020.

Andy Mukherjee, “India Has People. It Needs Consumers”, BloombergQuint, November 16, 2019.

Abhijit Mukhopadhyay, “India’s informal workers need at least a Rs. 1.5 trillion relief package to survive Covid19 lockdown”, Observer Research Foundation, April 23, 2020.

Abhijit Mukhopadhyay, “Atmanirbhar package a feeble fiscal straw to sinking economy”, Observer Research Foundation, May 29, 2020.

Abhijit Mukhopadhyay, “Industrial production remains in contraction zone, needs urgent support”, Observer Research Foundation, September 16, 2020.

Abhijit Mukhopadhyay, “Supplying more credit will not solve the problem of credit demand”, Observer Research Foundation, October 13, 2020.

Raghuram Rajan, “Where do we go from here?”, O.P. Jindal Lectures, Brown University, 2019.

Rathin Roy, “Demand, supply and growth slowdowns”, Business Standard, December 6, 2019.

Amartya Sen, “A better society can emerge from the lockdowns”, Financial Times, April 15, 2020.

Mihir S Sharma, “Three dangerous myths”, Business Standard, December 8, 2019.

Manmohan Singh, “The fountainhead of India’s economic malaise”, The Hindu, November 18, 2019.

Dipa Sinha, “Food for All During Lockdown: State Governments must universalise PDS”, The Wire, April 20, 2020.

Ajai Sreevatsan, “The growing clamour for an urban jobs scheme”, The Mint, October 5, 2020.

State Bank of India, “Ecowrap”, No. 2 (FY21), May 18, 2020.

Arvind Subramanian and Josh Felman, “India’s Great Slowdown: What Happened? What’s the Way Out?”, Centre for International Development Faculty Working Paper No. 370, December 2019

“India in historic technical recession, signals RBI in its first-ever nowcast”, The Economic Times, November 12, 2020.

“Fiscal strain: FY21 govt borrowing pegged at Rs. 12 lakh crore, up 53% from BE”, The Indian Express, May 9, 2020.

“It’s time to go for broke with a Rs. 10 trillion plan”, The Mint, March 29, 2020.

“Chorus grows for Rs. 10 trillion stimulus as lockdown ravages economy”, The Mint, April 10, 2020.

“Government’s economic package only 1% of GDP, say analysts”, The Times of India, May 20, 2020.

Rohan Venkataramakrishnan, “Abhijit Banerjee’s prescription for Indian economy”, Scroll.in, October 14, 2019.

World Trade Organization, “Trade shows signs of rebound from COVID-19, recovery still uncertain”, October 6, 2020.

Endnotes

The views expressed above belong to the author(s). ORF research and analyses now available on Telegram! Click here to access our curated content — blogs, longforms and interviews.

PDF Download

PDF Download