Nation-wide lockdown from the last week of March 2020 has expectedly taken its toll on industrial productions. Quick estimates of Index of Industrial Production (IIP) and use-based index for the month of July 2020 reaffirms the fact that industrial production of the country remains in distress.

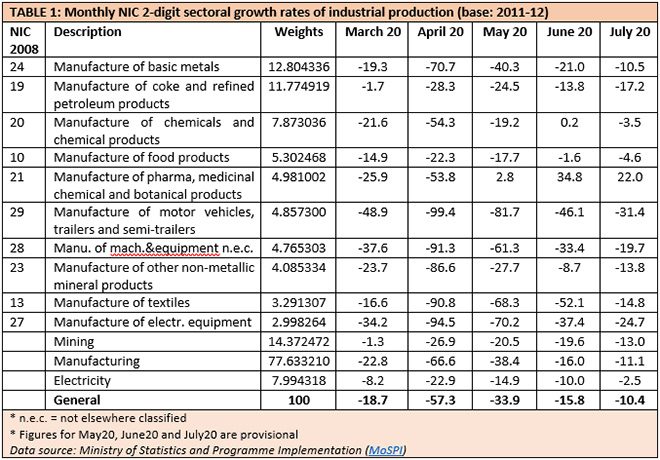

General index of industrial production continues to show negative growth rate at -10.4% in July (Table 1). In the current fiscal year 2020-21, the index remained in the red zone in the first four months — overall average contraction being close to 30%. An optimistic near future projection would expect the growth rates to improve in next five months and finally be in the zero or positive growth zone in the last quarter of the current fiscal, that is in January–March 2021.

If the gradual recovery is slower (or worse, deteriorates) then industrial production, particularly in the manufacturing, will be in serious trouble.

But, even then the overall annual contraction in industrial production would be in double digit figure — possibly in the region of 15% to 20%. To bring back the industrial production on a respectable growth path would then require at least a couple of years. If the gradual recovery is slower (or worse, deteriorates) then industrial production, particularly in the manufacturing, will be in serious trouble. Returning to a sustainable positive industrial growth, in that case, may take years.

Only major manufacturing segment that shows consistent positive growth rate in May–July period is pharmaceuticals. This was expected; tobacco is the only other sector that shows a positive growth in July 2020 (6.1%). All other sectors continue to show substantial contraction in production growth. The top 10 manufacturing sectors in terms of weightage in the index, totaling close to 63%, are mostly still showing double-digit growth contraction in the month of July (Table 1).

Only major manufacturing segment that shows consistent positive growth rate in May–July period is pharmaceuticals. This was expected; tobacco is the only other sector that shows a positive growth in July 2020 (6.1%). All other sectors continue to show substantial contraction in production growth. The top 10 manufacturing sectors in terms of weightage in the index, totaling close to 63%, are mostly still showing double-digit growth contraction in the month of July (Table 1).

The problem is that the weightage of pharma in IIP is close to 5% and that of tobacco is 0.8%. So, expecting these two sectors to pull up overall industrial production is like expecting roughly six people to pull up 94 others. If overall production has to improve, many other sectors need to be revived as quickly as possible.

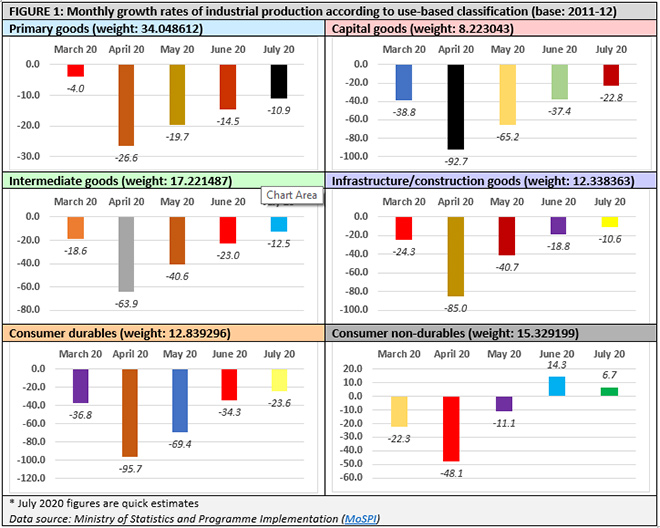

Monthly growth rates of industrial production according to the use-based classification underlines this desperate situation (Figure 1). Only consumer non-durable segment is showing positive growth rates since June 2020 — the growth rate though declined from 14.3% in June to 6.7% in July. The worst hit sectors are consumer durables and capital goods (mostly heavy machinery and equipment). One may take hope in decreasing contraction in primary and intermediates goods sectors, but getting into positive zone definitely would take some more time.

The contraction started in March — signifying already existing distress in Indian industrial production. The pandemic amplified it many times.

In these trying times for industry, the usual clamour is for corporate tax concessions, but that will not work this time. The most important point to note here is that the contraction has started in March — signifying already existing distress in Indian industrial production. The pandemic amplified it many times. Adverse unemployment consequences are also likely to increase in coming days.

Therefore, the possible way out of this recessionary trend in industry is to provide input tax concessions. Reducing or abolishing input taxes for some time (say, initially for a year) can be a starting point. It is quite comprehensible that the government is in no position to provide input subsidies to all sectors. The process may start with the top five manufacturing in terms of weightage — metals, oil, chemicals, processed food and automobile. Pharma can be, for the time being, kept out of this scheme. Once some of the initial beneficiary sectors revive themselves, those can be taken out and replaced by others — machinery & equipment, textiles, electrical equipment being the prominent among those.

Widespread public investment in infrastructure projects across the nation remains an option to boost demand and production. That can provide immediate income and purchasing power in the hands of consumers, revive demand, and in turn boost other sectors of industrial production. A proactive approach in that direction has the potential to make industrial recovery sufficiently faster.

Any delay in taking a proactive approach on the part of the government can prove to be fatal for the industry, and may result into chronic imbalance in the sectoral composition of the economy. The industry needs urgent help.

The views expressed above belong to the author(s). ORF research and analyses now available on Telegram! Click here to access our curated content — blogs, longforms and interviews.