-

CENTRES

Progammes & Centres

Location

RMG निर्यातीच्या एकाच श्रेणीवर अत्याधिक अवलंबित्वामुळे देशाच्या वाढीच्या ट्रेंडला बाधा येणार आहे.

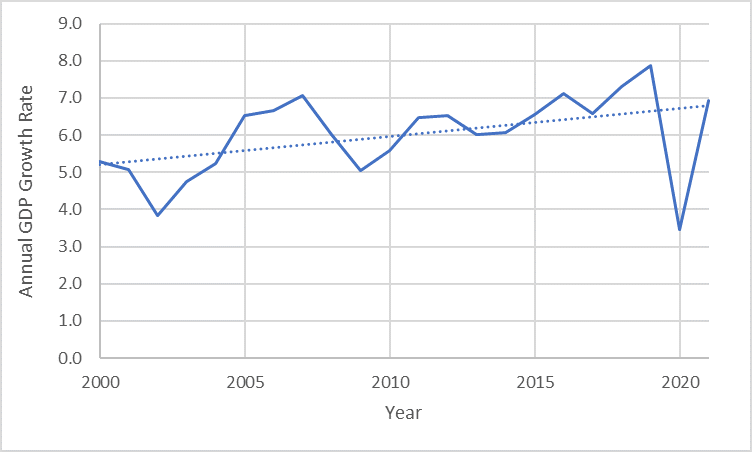

2021 मध्ये बांगलादेशने स्वतंत्र राष्ट्र म्हणून 50 वा वर्धापन दिन साजरा केल्यामुळे, देशाने आपल्या प्रवासाकडे मागे वळून पाहण्याची गरज आहे – 1971 च्या युद्धात दक्षिण आशियातील सर्वात गरीब राष्ट्रांपैकी एक असण्यापासून, 1970 च्या महा चक्रीवादळानंतर, ज्याने सुमारे अर्धा दशलक्ष बांगलादेशींचा बळी घेतला, तयार गारमेंट्स (RMG) पासून फार्मास्युटिकल्सपर्यंतच्या आर्थिक क्षेत्रात देशाच्या अभूतपूर्व प्रगतीवर प्रकाश टाकणारे सध्याचे आशियाई वाघ. बांगलादेशने अनेक वर्षांपासून कमी विकास दर अनुभवला – 1970-1980 दरम्यान सरासरी वाढीचा दर सुमारे 2 टक्के होता. तथापि, त्यानंतरच्या वर्षांत ते वाढले, 2004 मधील 5-टक्के पातळी ओलांडले, जे देशाच्या कृषी अर्थव्यवस्थेपासून उद्योग आणि सेवा-आधारित अर्थव्यवस्थेत स्थिर संरचनात्मक परिवर्तनाचा परिणाम होता. त्याच्या दक्षिण आशियाई समकक्षांच्या तुलनेत, बांगलादेशच्या विकास दराने 2006 मध्ये पाकिस्तानला मागे टाकले आणि 2011 पासून देशाने सातत्याने 6 टक्क्यांहून अधिक वाढ केली आहे.

आकृती 1: बांगलादेश जीडीपी विकास दर (वार्षिक टक्केवारी) (2000- 2021)

१९७१ च्या स्वातंत्र्ययुद्धापूर्वी, सध्याच्या बांगलादेशच्या अर्थव्यवस्थेत शेतीचे वर्चस्व होते. कृषी क्षेत्राचा वाटा 1970 च्या सुरुवातीच्या 60 टक्क्यांवरून 1990 च्या दशकात 30 टक्क्यांपर्यंत घसरला आणि अलिकडच्या वर्षांत तो सुमारे 12 टक्क्यांवर स्थिरावला. ही घसरण उद्योग आणि सेवा क्षेत्रातील समभागांच्या वाढीमुळे होते. सध्या, उद्योगाचा जीडीपीमध्ये सुमारे 33 टक्के वाटा आहे, तर सेवा क्षेत्र हे जीडीपीच्या सुमारे 55 टक्के वाटा असलेले प्रमुख क्षेत्र आहे. बांगलादेशच्या सेवा क्षेत्राने 1980 च्या दशकात वेगवान वाढ दर्शविली आणि 1990 च्या दशकाच्या सुरुवातीस अर्थव्यवस्थेचे व्यापार उदारीकरण झाल्यानंतर, सेवा क्षेत्रात आणखी वाढ झाली. तथापि, 2000-2010 मधील 10 वर्षांच्या डेटाचा वापर करून अर्थमितीय विश्लेषण दर्शविते की जरी सेवा क्षेत्राने (6.17 टक्के) कृषी क्षेत्रापेक्षा (3.21 टक्के) वेगाने वाढ केली असली, तरी उद्योगांच्या वाढीने (7.49 टक्के) सेवांना मागे टाकले आहे. 2010 ते 2021 दरम्यान, GDP च्या टक्केवारीच्या रूपात सेवांद्वारे जोडलेले मूल्य देखील 2.2 टक्क्यांनी कमी झाले आहे.

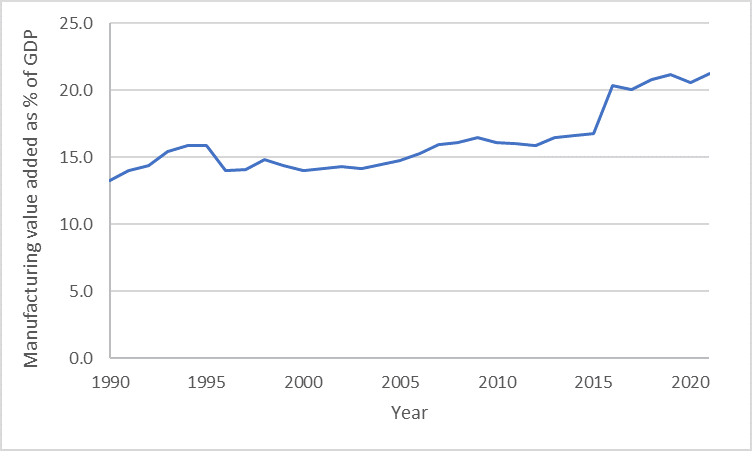

उद्योगांच्या क्षेत्रामध्ये, उत्पादनाचा वाटा सतत वाढत आहे – नंतरच्या काळात 1990 च्या दशकात वाढीचा उच्च दर दिसून आला आणि गेल्या दोन दशकांपासून वाढीचा कल दिसून आला. तथापि, मॅन्युफॅक्चरिंगच्या वाढीचे श्रेय प्रामुख्याने RMG ला दिले जाते—जागतिक बँकेच्या आकडेवारीनुसार, उत्पादन क्षेत्रात एकूण मूल्यवर्धित मूल्याच्या सुमारे 57 टक्के वाटा कापड आणि कपड्यांचा आहे, तर मध्यम आणि उच्च-तंत्र उत्पादन मूल्याचा वाटा आहे. 1990 च्या 24 टक्क्यांवरून 2019 मध्ये सातत्याने 7 टक्क्यांवर घसरले.

आकृती 2: बांगलादेशचे उत्पादन मूल्य जोडले गेले (जीडीपीची टक्केवारी) (1990-2021)

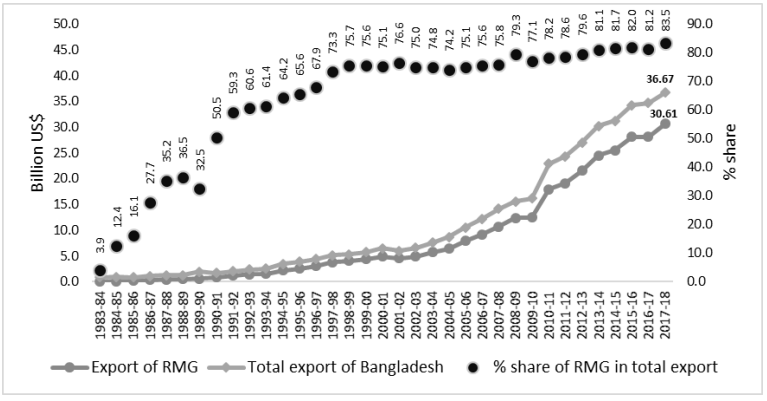

RMG मधील प्रगती देशाच्या विस्कळीत व्यापार पद्धतींशी एकरूप आहे. एकूण निर्यात कमाईपैकी RMG निर्यात सुमारे 84 टक्के आहे, आणि निर्यात 7 टक्क्यांच्या चक्रवाढ वार्षिक वाढ दराने वाढली आहे- 2011 मध्ये US$14.6 बिलियन वरून 2019 मध्ये US$33.1 बिलियन पर्यंत. आयात टोपलीच्या रचनेत बदल झाला आहे. कृषी कच्च्या मालापासून कच्च्या मालाच्या निर्मितीपर्यंत, बांगलादेशचे निर्यात-केंद्रित औद्योगिकीकरण, मुख्यत्वे RMG वर अवलंबून, देशासाठी स्थूल आर्थिक धोके निर्माण करतात. GDP मधील निर्यातीचा वाटा 2012 मधील 20.2 टक्क्यांवरून 2021 मध्ये 10.7 टक्क्यांपर्यंत घसरला आहे, इतकेच नाही तर स्टील, रासायनिक आणि वाहतूक उपकरणे यांसारख्या जटिल उत्पादन उत्पादनांमध्ये विविधता न आणता RMG निर्यातीच्या एकाच श्रेणीवर जास्त अवलंबित्व. देशाच्या वाढीच्या ट्रेंडला बाधा आणणे निश्चित आहे.

आकृती 3: एकूण निर्यातीमधील निर्यात आणि RMG चा वाटा (1983 – 2018)

प्रथम, बांगलादेश निर्मित RMG च्या जागतिक मागणीतील अस्थिरता हे चिंतेचे प्रमुख कारण आहे. समान मूल्य साखळीच्या वरच्या भागात किंवा इतर विभागांमध्ये पुरेसे वैविध्य न ठेवता कमी-मूल्याच्या कपड्यांच्या उत्पादनावर बांगलादेशचे लक्ष केंद्रित केल्यामुळे वाढीचा नमुना कोविड-19 साथीच्या रोगासारख्या बाह्य धक्क्यांसाठी अत्यंत संवेदनशील बनला आहे. 2019 च्या उत्तरार्धात या क्षेत्रातील मंदीची चिन्हे दिसू लागली आणि 2020 मध्ये जेव्हा साथीच्या आजारामुळे लॉकडाऊन सुरू झाले, तेव्हा ऑर्डर रद्द करण्यापासून ते पेमेंट विलंबापर्यंतच्या समस्यांमध्ये आणखी वाढ झाली. व्यापारावरील प्रारंभिक निर्बंध हटवल्यानंतर जागतिक बाजारपेठ उघडल्यानंतर RMG द्वारे समर्थित उत्पादन क्षेत्र लवकरच सावरले. तथापि, रशिया-युक्रेन संघर्षामुळे RMG ची मागणी कमी होत चालली होती, जेथे रशियाने SWIFT (जागतिक पेमेंट मेसेजिंग नेटवर्क) वापरण्यास बंदी घातली तेव्हा मोठ्या प्रमाणात कपड्यांचे व्यापारी निर्यात पावत्या प्राप्त करू शकले नाहीत.

दुसरे म्हणजे, बांगलादेश आपल्या RMG पैकी 80 टक्के युरोप आणि अमेरिकेतील बाजारपेठेत निर्यात करतो, या क्षेत्रात व्हिएतनामचा उदय मोठा धोका. एकीकडे, व्हिएतनाम आणि EU यांच्यातील प्राधान्य व्यापार करार (PTA) बांगलादेशच्या RMG निर्यात EU ला मागे टाकू शकतो, तर दुसरीकडे, अमेरिकेने चीनला पर्याय म्हणून सामग्री सोर्सिंगसाठी व्हिएतनामची जोरदार निवड केली आहे. अमेरिकेला व्हिएतनामी पोशाखांची आयात बांग्लादेशच्या अमेरिकेला होणाऱ्या आयातीपेक्षा २.५ पट असल्याचा अंदाज आहे.

आकृती 4: अमेरिका आणि युरोपमधील बांगलादेश आणि व्हिएतनाममधून पोशाख आयात मूल्याची वाढ (2011 – 2020)

तिसरे म्हणजे, RMG च्या पुरवठ्याच्या बाजूने, वाढत्या इंधनाच्या किमती हा या क्षेत्रातील एक अतिरिक्त भार आहे जेथे गारमेंट कंपन्यांच्या खर्चाच्या अंदाजे 10 टक्के इंधनाचा वाटा आहे. याव्यतिरिक्त, बांगलादेशच्या अर्थव्यवस्थेतील चलनवाढीच्या दबावामुळे RMG च्या इनपुट खर्चात आणखी वाढ झाली आहे ज्यामुळे तयार उत्पादनांच्या किंमतींमध्ये वाढ झाली आहे – अशा प्रकारे, जागतिक बाजारपेठेतील वस्तूंच्या किंमतींची स्पर्धात्मकता कमी होते. किंबहुना, RMG क्षेत्र देखील मोठ्या प्रमाणावर स्वस्त अकुशल कामगारांवर अवलंबून आहे, जे या क्षेत्राला स्पर्धात्मक फायदा देते; क्षेत्रे आणि भौगोलिक क्षेत्रांमध्ये श्रमिक गतिशीलता वाढल्याने हे दीर्घ क्षितिजामध्ये टिकाऊ असू शकत नाही. शेवटी, देशातील पायाभूत सुविधांच्या समस्या आणि सोर्सिंग कंपन्यांमधील वेग आणि लवचिकतेमुळे निअरशोअरिंगला वाढती पसंती यामुळे RMG क्षेत्राला गंभीर धोका निर्माण होऊ लागला आहे. 2012 ची ताजरीन फॅक्टरी आग आणि 2013 राणा प्लाझा आपत्ती हे कापड उद्योगातील अत्यंत कामाच्या परिस्थितीची आठवण करून देणारे आहेत – ज्यामुळे अनेक आंतरराष्ट्रीय खरेदीदारांनी बांगलादेशातून सोर्सिंग थांबवले.

नॉन-आरएमजी क्षेत्रांना भेडसावणारा निर्यात-विरोधी पक्षपात केवळ निर्यात क्षेत्रांमधील स्पर्धा मर्यादित ठेवत नाही तर उत्पादनातील फरकांना अडथळा आणण्यासाठी जबाबदार आहे. RMG क्षेत्रातील निर्यात-क्षेत्रातील वैविध्य आणि पायाभूत सुविधा वाढवणे या दोन्ही गोष्टींना खाजगी क्षेत्रातील कमकुवत गुंतवणुकीमुळे बाधा येत आहे, कारण अलीकडच्या काळात व्यवसायाचे वातावरण बिघडत चालले आहे आणि विशेषत: लघु आणि मध्यम उद्योगांसाठी कर्ज उपलब्ध होण्यात अडचणी येत आहेत. याव्यतिरिक्त, वाढत्या हवामान बदलाच्या दरम्यान, जागतिक मागणी अधिक शाश्वत उत्पादनांकडे वळत आहे. विविधीकरणाचा अभाव आणि हवामान-तटस्थ उत्पादनांच्या क्षेत्राचा विस्तार करण्यासाठी R&D मध्ये कमी केलेली गुंतवणूक देशाला कमी झालेल्या निर्यातीसह खोल पाण्यात टाकू शकते आणि इतर समष्टि आर्थिक मापदंडांवर त्याचा परिणाम होऊ शकतो.

The views expressed above belong to the author(s). ORF research and analyses now available on Telegram! Click here to access our curated content — blogs, longforms and interviews.

Soumya Bhowmick is a Fellow and Lead, World Economies and Sustainability at the Centre for New Economic Diplomacy (CNED) at Observer Research Foundation (ORF). He ...

Read More +