-

CENTRES

Progammes & Centres

Location

অতিমারির অর্থনৈতিক প্রভাব, অভ্যন্তরীণ রাজনৈতিক অস্থিরতা বা ইউক্রেন-রাশিয়া দ্বন্দ্ব যাতে দেশের ভবিষ্যতের উপর চিরস্থায়ী প্রভাব না ফেলে তা নিশ্চিত করার জন্য অবিলম্বে ব্যবস্থা নেওয়া দরকার।

শ্রীলঙ্কায় ব্যালান্স অফ পেমেন্টের ব্যবধান মেটানো

সাম্প্রতিক অতীতে দ্বীপরাষ্ট্রটি যে অভূতপূর্ব অর্থনৈতিক সংকটের মধ্যে পড়েছিল তার পরিপ্রেক্ষিতে শ্রীলঙ্কা বিশ্বজুড়ে সংবাদ-শিরোনাম হয়েছে। তারপর ১৮ আগস্ট ২০২২ তারিখে শ্রীলঙ্কার কেন্দ্রীয় ব্যাঙ্কের গভর্নর বলেছেন যে রপ্তানি বৃদ্ধি ও আমদানি বিল হ্রাসের কারণে চলতি খাতের ঘাটতি ধীরে ধীরে সংকুচিত হচ্ছে, এবং ‘ফরেক্স পরিস্থিতি এখন উন্নত হয়েছে এবং আমরা (শ্রীলঙ্কার অর্থনীতি) পেট্রোল, ডিজেল ও ওষুধের মতো প্রয়োজনীয় জিনিসগুলির জন্য অর্থ প্রদান করতে সক্ষম হয়েছি’। যাই হোক, এই ক্যালেন্ডার বছরে সঙ্কটবিধ্বস্ত অর্থনীতি ৮ শতাংশ সঙ্কুচিত হবে বলে আশঙ্কা করা হচ্ছে, যা ২০২০ সালে অতিমারি ছড়িয়ে পড়ার সময়কার ৩.৬ শতাংশ সঙ্কোচনের দ্বিগুণেরও বেশি। এই পটভূমিতে, শ্রীলঙ্কার ব্যালান্স অফ পেমেন্টস (বি ও পি) বা আদান–প্রদান সংক্রান্ত আয়ব্যয়ের ভারসাম্যের প্রবণতা এবং গত কয়েক বছরে পুনরাবৃত্ত ঘাটতি যেভাবে দেশটির সামষ্টিক অর্থনৈতিক স্থিতিশীলতাকে কাঠামোগতভাবে দুর্বল করেছে তা বিশ্লেষণ করা আকর্ষণীয় হবে।

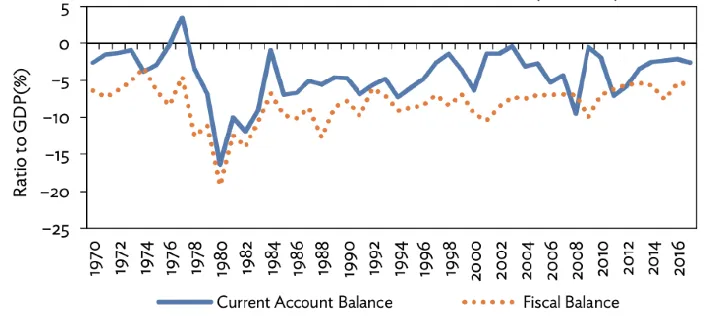

শ্রীলঙ্কা হল ‘টুইন ডেফিসিট’’ বা যমজ ঘাটতি হাইপোথেসিসের একটি ধ্রুপদী উদাহরণ, যে হাইপোথেসিস অনুযায়ী একটি দেশের চলতি ও আর্থিক খাতের ভারসাম্য একই অভিমুখে চলে। অভ্যন্তরীণ ও আন্তর্জাতিক উভয় ক্ষেত্রে উচ্চ মাত্রার ঋণজর্জরিত উপভোগচালিত অর্থনীতির বিকাশের ক্ষেত্রে এই ঘটনাটি সাধারণত সত্য। যেহেতু দেশে অতিরিক্ত চাহিদা থাকে, তাই উপভোক্তাদের চাহিদা মেটাতে আমদানি বাড়াতে হয় এবং তা মূল্যস্ফীতিকে আরও চড়া করে তোলে—যেমনটা শ্রীলঙ্কার ক্ষেত্রে ঘটেছে— আর এই অবস্থায় দেশের ভেতরে উৎপাদিত পণ্যগুলিকে প্রায়শই বিশ্ব রপ্তানি বাজারে কম প্রতিযোগিতামূলক হিসাবে দেখা হয়।

চিত্র ১: শ্রীলঙ্কার চলতি খাতের ভারসাম্য এবং আর্থিক ভারসাম্যের প্রবণতা (১৯৭০-২০১৬)

এর দুটি প্রধান কারণ আছে। প্রথমত, কেইনসিয়ান পদ্ধতি অনুসরণ করে বলা যায়, ক্রমবর্ধমান বাজেট ঘাটতি দেশের মধ্যেই শোষিত হয়ে যাওয়ার পথে পরিচালিত করে, এবং তার ফলে আমদানি বেড়ে যায়, যা চলতি খাতের ঘাটতিকে বাড়িয়ে তোলে। আবার এর উল্টোটাও সত্য। দ্বিতীয়ত, মুন্ডেল–ফ্লেমিং মডেল থেকে বলা যায়, বাজেট ঘাটতি বৃদ্ধির ফলে সুদের হার ঊর্ধ্বমুখী হয়, এবং এর বিপরীতটিও সত্য। সুদের হার বাড়ার সঙ্গে সঙ্গে দেশীয় অর্থনীতি বিদেশি বিনিয়োগকারীদের কাছে আরও আকর্ষণীয় হয়ে ওঠে, যার ফলে মূলধনী খাতে উদ্বৃত্ত বেড়ে যায়। তার ফলে আবার চলতি খাতের ঘাটতি বৃদ্ধি পায়। মূলধনী খাতের উদ্বৃত্ত চলতি খাতের উপর বিরূপ প্রভাব ফেলতে পারে, যেখানে বর্ধিত তারল্য উপভোগের চাহিদা বাড়ায়। তার ফলে আবার আরও বেশি আমদানির প্রয়োজন হয়, যার ফলে চলতি খাতে আরও ঘাটতি হয়। বিকল্পভাবে, মূলধনের প্রবাহ অভ্যন্তরীণ মুদ্রার দাম বাড়িয়ে দিতে পারে, যা আমদানিকে সস্তা করে তুলবে, অভ্যন্তরীণ চাহিদা তৈরি করবে, এবং রপ্তানিকে ব্যয়বহুল করে তুলবে। ফলস্বরূপ সেগুলির মূল্য হ্রাস পাবে, এবং এইভাবে আবার চলতি খাতের ঘাটতি বাড়বে।

শ্রীলঙ্কার সামনে সামষ্টিক অর্থনৈতিক সমস্যার ক্ষেত্রে যুক্তি দেওয়া হয় এই ধরনের দ্বৈত ঘাটতি বিদেশি ঋণের উপর নির্ভরতা বাড়িয়ে চলেছে। কয়েক দশক ধরে দেশটি তার চলতি খাতের ঘাটতি এবং গুরুত্বপূর্ণ উন্নয়নমূলক কর্মসূচির অর্থায়নের জন্য বহুপাক্ষিক ও দ্বিপাক্ষিক ঋণের উপর নির্ভরশীল। এই সমস্যাটি অতিমারির মতো বহিরাগত ধাক্কাগুলির ক্ষেত্রে অর্থনীতিকে ঝুঁকিপূর্ণ করে তুলতে সরাসরি অবদান রেখেছে, এবং তার ফলে আন্তর্জাতিক বাজারে ঋণের প্রাপ্যতার পথ অবরুদ্ধ হয়ে গেছে।

অতিমারির আগে ২০১৯ সালের করহ্রাস ইতিমধ্যেই দেশের কর রাজস্বকে কমিয়ে দিয়েছিল এবং রাজস্ব ঘাটতি আরও বাড়িয়ে দিয়েছিল। যখন অর্থনীতি ইতিমধ্যেই ব্যাপক কর ফাঁকির কারণে ভুগছিল, সেই সময় ২০২০ থেকে ২০২২–এর মধ্যে প্রায় এক মিলিয়ন করদাতা কমে যাওয়ার কথা জানা গিয়েছিল। অতিমারির আকস্মিকতা এবং সে কারণে প্রবর্তিত বিধিনিষেধের ফলে অনিবার্য সামাজিক নিরাপত্তা ব্যবস্থাগুলিকে সচল করার জন্য জাতীয় কোষাগারের অনেক খরচ হয়েছে, এবং তা রাজস্ব ঘাটতিকে আরও বাড়িয়ে তুলেছে।

এগুলি ছাড়াও, ২০২১ সালের এপ্রিলে সম্পূর্ণরূপে জৈব চাষে চলে যাওয়ায় ফসলের উৎপাদনশীলতা হ্রাস এবং কৃষি ক্ষেত্রে অতিরিক্ত চাহিদা ইত্যাদির কারণে শ্রীলঙ্কার কিছু শক্তিশালী কৃষিক্ষেত্র ধ্বংস হয়ে যায়। অর্থনীতির ধান উৎপাদনে স্বয়ংসম্পূর্ণতা পুরোপুরি নষ্ট হয়ে যায়, এবং শ্রীলঙ্কাকে মায়ানমার ও চিনের মতো দেশ থেকে চাল আমদানি করতে হয়। উপরন্তু দেশের অপরিকল্পিত কৃষি সংস্কারের কারণে ক্ষতিগ্রস্ত হয়েছিল চা, যা রপ্তানির একটি প্রধান পণ্য ছিল। ডিসেম্বর ২০২১ এবং মার্চ ২০২২–এর মধ্যে বাণিজ্য ঘাটতি ১০৮৫ মিলিয়ন ডলার থেকে ৭৬২ মিলিয়ন ডলারে নেমে এসেছে। হ্রাসপ্রাপ্ত বৈদেশিক মুদ্রার সঞ্চয় শ্রীলঙ্কার রুপির মূল্যকেও ক্ষতিগ্রস্ত করেছে। ২০২১ সালে মুদ্রার দাম প্রায় ৭.৩ শতাংশ কমেছে, এবং আমদানি খরচ বিরাটভাবে বেড়েছে, যা মূল্যস্ফীতির ঊর্ধ্বগতির সূচনা করে। এরপরে আসে সামাজিক অস্থিরতা। ফলে আর্থিক ও চলতি খাতের উপর অতিরিক্ত চাপ শ্রীলঙ্কার পরিস্থিতিকে আরও খারাপ করে।

শ্রীলঙ্কায় চলতি ও মূলধনী খাতের ভারসাম্য ঐতিহাসিকভাবে একে অপরের বিপরীত দিকে চলে গেছে। যদিও প্রথমটি কিছু সময়ের জন্য বিপর্যয়কর পরিসংখ্যানের মধ্যে আটকে ছিল, মূলধনী খাতগুলি উদ্বৃত্ত স্তরে রয়েছে। বোধগম্যভাবে, অর্থনীতিকে সচল রাখতে সরকার চিননির্মিত কলম্বো পোর্ট সিটিকে পরবর্তী ৪০ বছরের জন্য একটি বিশেষ করছাড় ব্যবস্থার অধীনে কাজ করার অনুমতি দিয়ে অতিরিক্ত বিদেশি বিনিয়োগ আকৃষ্ট করার চেষ্টা করেছিল, যা বিদেশি বিনিয়োগকারীদের উপর সরকারের নির্ভরতার আরেকটি উদাহরণ। কিন্তু বিদেশি বিনিয়োগকারীরা এই ধরনের নড়বড়ে ভিতের উপর দাঁড়িয়ে থাকা একটি অর্থনীতিতে বিনিয়োগ করতে দ্বিধাগ্রস্ত ছিল।

চিত্র ২: শ্রীলঙ্কার চলতি এবং মূলধনী খাতের ভারসাম্যে ঐতিহাসিক প্রবণতা (মিলিয়ন মার্কিন ডলারে)

নিম্নমুখী চলতি খাতের সঙ্গে তুলনামূলকভাবে ধীর গতিতে ক্রমবর্ধমান মূলধনী খাত যুক্ত হয়ে বিশেষ করে গত বছর বি ও পি ঘাটতির ক্ষেত্রে একটি বিশাল সমস্যা সৃষ্টি করেছিল। দেশটি এখনও জনগণের প্রয়োজনীয় পণ্যের চাহিদা পূরণ করতে অক্ষম। অতিমারির অর্থনৈতিক প্রভাব, অভ্যন্তরীণ রাজনৈতিক অস্থিরতা বা ইউক্রেন–রাশিয়া দ্বন্দ্ব যাতে দেশের ভবিষ্যতের উপর চিরস্থায়ী প্রভাব না ফেলে তা নিশ্চিত করার জন্য অবিলম্বে ব্যবস্থা নেওয়া প্রয়োজন।

চিত্র ৩: শ্রীলঙ্কার সাম্প্রতিক ব্যালান্স অফ পেমেন্টস (বি ও পি) প্রবণতা (মিলিয়ন মার্কিন ডলারে)

শ্রীলঙ্কা জাপানকে দ্বিপাক্ষিক ঋণ পুনর্গঠন নিয়ে সম্ভাব্য আলোচনার জন্য চিন ও ভারতের মতো ঋণদাতা দেশগুলোকে আমন্ত্রণ জানানোর দায়িত্ব নিতে বলতে চলেছে। অবিলম্বে আন্তর্জাতিক মুদ্রা ভান্ডার (আইএমএফ)–এর বেলআউট অপরিহার্য, কারণ এটি সরকারকে বিশেষভাবে প্রয়োজনীয় তহবিল জোগাড়ের সুযোগ করে দেবে। আর সেই সঙ্গেই তা এই বছরের শুরুতে আনুষ্ঠানিকভাবে বকেয়া অর্থপ্রদান বন্ধ করে শ্রীলঙ্কা ঋণখেলাপি হওয়ার পর থেকে আন্তর্জাতিক আর্থিক বাজারে দেশটি সম্পর্কে যে অনীহা দেখা দিয়েছে, তা থেকে বেরোবার পথ তৈরি করে দিতে পারে।

মতামত লেখকের নিজস্ব।

The views expressed above belong to the author(s). ORF research and analyses now available on Telegram! Click here to access our curated content — blogs, longforms and interviews.

Soumya Bhowmick is a Fellow and Lead, World Economies and Sustainability at the Centre for New Economic Diplomacy (CNED) at Observer Research Foundation (ORF). He ...

Read More +