-

CENTRES

Progammes & Centres

Location

এই জোড়া ধাক্কা উপার্জন পিরামিডের একেবারে নিচের তলায় থাকা মানুষজনের সামনে প্রতিবন্ধকতা হয়ে দাঁড়াবে।

মুদ্রাস্ফীতি ও আই আই পি মন্থরতার জোড়া বিপদ

ইন্টারন্যাশনাল মনিটারি ফান্ড (আই এম এফ) ২০২২-২৩ অর্থবর্ষের জন্য ভারতের বৃদ্ধির সম্ভাব্য হার ৬.৮ শতাংশে নেমে আসার কথা ঘোষণার অব্যবহিত পরেই ভারতীয় অর্থনীতি ২০২২ সালের সেপ্টেম্বর মাসে ক্রমবর্ধমান খুচরো বা রিটেল মুদ্রাস্ফীতি এবং ২০২২ সালের আগস্ট মাসে ইনডেক্স অফ ইন্ডাস্ট্রিয়াল প্রোডাকশনের (আই আই পি) এক অপ্রত্যাশিত সঙ্কোচনের জোড়া ধাক্কার সম্মুখীন হয়।

সেপ্টেম্বর মাসের আনুমানিক পরিসংখ্যান অনুযায়ী কম্বাইনড কনজিউমার প্রাইস ইনডেক্স (সি পি আই) বৃদ্ধি পেয়ে ৭.৪১ শতাংশ হয়েছে। এই মাসে দু’টি উদ্বেগজনক প্রবণতার উত্থান লক্ষ করা গিয়েছে। প্রথমটি হল, গ্রামাঞ্চলের সি পি আই শহরাঞ্চলের সি পি আই-এর তুলনায় সামান্য হলেও বেশি বৃদ্ধি পেয়েছে, যা গ্রামীণ ভারতে মুদ্রাস্ফীতির অধিকতর প্রভাবকেই দর্শায়। দ্বিতীয়টি হল, এই মাসে কনজিউমার ফুড প্রাইস ইনডেক্স (সি এফ পি আই) ইয়ার অন ইয়ার বা বছরভিত্তিক ভাবে বৃদ্ধি পেয়ে দাঁড়িয়েছে ৮.৬ শতাংশে (তালিকা / সারণি ১)। এর অর্থ হল মূল্যবৃদ্ধির নেপথ্যে রয়েছে খাদ্যদ্রব্যের মূল্য। জনসংখ্যার প্রান্তিক অংশের মানুষজনের বেঁচে থাকার নিরিখে এটি অত্যন্ত ক্ষতিকারক।

সারণি ১: সি পি আই (জেনারেল) এবং সি এফ পি আই-এর ভিত্তিতে সর্বভারতীয় মুদ্রাস্ফীতির হার (শতাংশে)

| সূচক | সেপ্টেম্বর ২০২২ (অস্থায়ী) | আগস্ট ২০২২ (স্থায়ী) | সেপ্টেম্বর ২০২১ | ||||||

| গ্রামীণ | শহুরে | মোট | গ্রামীণ | শহুরে | মোট | গ্রামীণ | শহুরে | মোট | |

| সি পি আই (জেনারেল) | ৭.৫৬ | ৭.২৭ | ৭.৪১ | ৭.১৫ | ৬.৭২ | ৭.০০ | ৪.১৩ | ৪.৫৭ | ৪.৩৫ |

| সি এফ পি আই | ৮.৫৩ | ৮.৬৫ | ৮.৬০ | ৭.৬০ | ৭.৫৫ | ৭.৬২ | ০.৬৯ | ০.৬৭ | ০.৬৮ |

· সি পি আই = কনজিউমার প্রাইস ইনডেক্স, সি এফ পি আই = কনজিউমার ফুড প্রাইস ইনডেক্স

· সূচকগুলির গণনা করা হয়েছে ২০১২ সালের ভিত্তি = ১০০র নিরিখে

· মুদ্রাস্ফীতির হার পয়েন্ট টু পয়েন্ট ভিত্তিতে নির্ধারিত অর্থাৎ বর্তমান মাসের সঙ্গে গত বছরের একই মাসের নিরিখে

সূত্র: মিনিস্ট্রি অব স্ট্যাটিস্টিক্স অ্যান্ড প্রোগ্রাম ইমপ্লিমেন্টেশন (এম ও এস পি আই), ভারত সরকার

এমনকি সি পি আই এবং সি এফ পি আই-এর মাসিক পরিবর্তনের দিকে নজর দিলেও এই দু’টি প্রবণতা স্পষ্ট বোঝা যায়। ২০২২ সালের আগস্ট মাসের পরিসংখ্যান তুলনা করলে দেখা যাবে, সেপ্টেম্বর মাসে শহরাঞ্চলের তুলনায় গ্রামাঞ্চলে সি পি আই এবং সি এফ পি আই… উভয়ই বৃদ্ধি পেয়েছে। (সারণি ২)

খাদ্য মুদ্রাস্ফীতি সি পি আই বাস্কেটের প্রায় ৩৯ শতাংশ জায়গা জুড়ে রয়েছে (অ্যালকোহলবিহীন পানীয় এবং প্রস্তুত করা খাবার, জলখাবার, মিষ্টি ইত্যাদি বাদ দিয়ে)। সেপ্টেম্বর মাসের সি পি আই মুদ্রাস্ফীতি বৃদ্ধির নেপথ্যে ছিল প্রধানত শাকসবজি (১৮.০৫ শতাংশ), মশলা (১৬.৮৮ শতাংশ) এবং খাদ্যশস্য ও পণ্য (১১.৫৩ শতাংশ)। এ বছর সেপ্টেম্বর মাসে খাদ্যশস্য এবং পণ্যের মুদ্রাস্ফীতির পরিমাণ ২০১৩ সালের সেপ্টেম্বর মাসের পর থেকে এখনও সর্বোচ্চ। সর্বাধিক গুরুত্বপূর্ণ খাদ্যশস্যের অর্থাৎ পি ডি এস (গণবণ্টন ব্যবস্থা) বহির্ভূত চাল এবং গমের এ বছর সেপ্টেম্বর মাসে যথাক্রমে ৯.২ শতাংশ এবং ১৭.৪ শতাংশ মুদ্রাস্ফীতি হয়েছে। এটি অত্যন্ত উদ্বেগজনক।

সারণি ২: সি পি আই (জেনারেল) এবং সি এফ পি আই-এর ভিত্তিতে সর্বভারতীয় মাসিক পরিবর্তন (শতাংশে): ২০২২ সালের আগস্ট মাসের সঙ্গে ২০২২ সালের সেপ্টেম্বর মাসের তুলনা

| সূচক | গ্রামীণ | শহুরে | মোট | |||||||

| সূচকের মান | শতাংশ পরিবর্তন | সূচকের মান | শতাংশ পরিবর্তন | সূচকের মান | শতাংশ পরিবর্তন | |||||

| সেপ্টেম্বর ২০২২ | অগস্ট ২০২২ | সেপ্টেম্বর ২০২২ | অগস্ট ২০২২ | সেপ্টেম্বর ২০২২ | অগস্ট ২০২২ | |||||

| সি পি আই (জেনারেল) | ১৭৬.৪ | ১৭৫.৩ | ০.৬৩ | ১৭৪.১ | ১৭৩.১ | ০.৫৮ | ১৭৫.৩ | ১৭৪.৩ | ০.৫৭ | |

| সি এফ পি আই | ১৭৪.৪ | ১৭২.৭ | ০.৯৮ | ১৮০.৮ | ১৭৯.৫ | ০.৭২ | ১৭৬.৭ | ১৭৫.১ | ০.৯১ | |

· সি পি আই = কনজিউমার প্রাইস ইনডেক্স, সি এফ পি আই = কনজিউমার ফুড প্রাইস ইনডেক্স

· সূচকগুলির গণনা করা হয়েছে ২০১২ সালের ভিত্তি = ১০০র নিরিখে

· মুদ্রাস্ফীতির হার পয়েন্ট টু পয়েন্ট ভিত্তিতে নির্ধারিত অর্থাৎ বর্তমান মাসের সঙ্গে গত বছরের একই মাসের নিরিখে

সূত্র: মিনিস্ট্রি অব স্ট্যাটিস্টিক্স অ্যান্ড প্রোগ্রাম ইমপ্লিমেন্টেশন (এম ও এস পি আই), ভারত সরকার

এই ঘটনার দু’দিন পর হোলসেল প্রাইস ইনডেক্স (ডব্লিউ পি আই) বা পাইকারি মূল্য সূচক সংক্রান্ত পরিসংখ্যানও ঘোষণা করা হয়। ২০২২ সালের সেপ্টেম্বর মাসে ডব্লিউ পি আই ১০.৭ শতাংশ বৃদ্ধি পেয়েছে যা আগস্ট মাসের ১২.৪ শতাংশ বৃদ্ধি হারের তুলনায় কম। যেমন ডব্লিউ পি আই-এর প্রাথমিক উদ্দেশ্য হল উৎপাদনকারীদের দ্বারা ধার্য করা মূল্যের উপর নজর রাখা, ঠিক তেমনই সি পি আই-এর কাজ হল দেশের অর্থনীতি্র অংশস্বরূপ একটি সাধারণ গৃহস্থালিকে যে বাজারদরের সম্মুখীন হতে হয়, তার পরিমাপ করা। অর্থাৎ ডব্লিউ পি আই মুদ্রাস্ফীতির সামান্য হ্রাসের অর্থ হল দু’মাস আগে উৎপাদনকারীদের দ্বারা ধার্য মূল্য সর্বোচ্চ পর্যায়ে পৌঁছেছিল। কিন্তু সমস্যাজনক বিষয়টি হল এটি এখনও উচ্চ দুই অঙ্কের স্তরেই স্থায়ী রয়েছে। ডব্লিউ পি আই মুদ্রাস্ফীতি এই স্তরেই স্থায়ী হলে তা মোটেও সুখকর হবে না।

অর্থনীতিবিদদের দ্বারা পরিচালিত একটি ব্লুমবার্গ সমীক্ষায় খুচরো মুদ্রাস্ফীতির মাত্রা ৭.৩৬ শতাংশ পর্যন্ত বৃদ্ধি পেতে পারে বলে অনুমান করা হয়েছে, যা প্রধানত ৭.৪১ শতাংশের প্রকৃত মাত্রার কাছাকাছি। যদিও ব্লুমবার্গের পূর্বাভাস আই আই পি-এ মন্থরতা অনুমানে ব্যর্থ হয়, সংশ্লিষ্ট ক্ষেত্রে তাঁরা ১.৭ শতাংশ বৃদ্ধির অনুমান করেছিলেন।

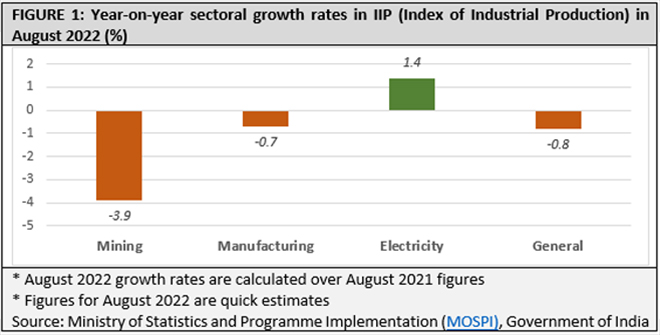

৭৭ শতাংশ আই আই পি সব ধরনের উৎপাদন কার্যের সঙ্গে যুক্ত হওয়ার ফলে আগস্ট মাসের ০.৮ শতাংশ সঙ্কোচন অর্থনীতির নিরিখে ইতিবাচক পূর্বাভাস দেয়নি। উৎপাদন ০.৭ শতাংশ সঙ্কোচনের পাশাপাশি খনিক্ষেত্রে ৩.৯ শতাংশ সঙ্কোচনও সামগ্রিক পতনের নেপথ্যে অন্যতম গুরুত্বপূর্ণ কারণ (চিত্র ১)। বর্ষার ফলে খনন ও নির্মাণ কার্য প্রভাবিত হওয়া এবং বৈশ্বিক মন্থরতার দরুন রফতানির পরিমাণ হ্রাস… সঙ্কোচনের নেপথ্যে এ দু’টিই প্রধান কারণ।

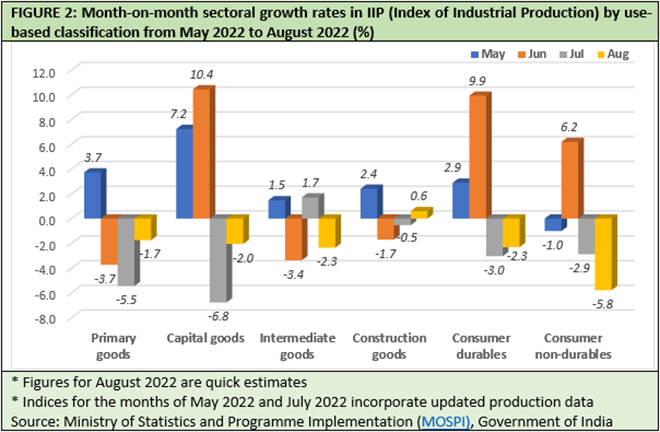

মন্থরতার জন্য খনন কার্যের সঙ্কোচন তাৎপর্যপূর্ণ ভাবে দায়ী হলেও ব্যবহারভিত্তিক শ্রেণিবিন্যাস দ্বারা করা মান্থ অন মান্থ বা মাসিক সেক্টোরাল আই আই পি বৃদ্ধি হারের তুলনা করলে সংশ্লিষ্ট সঙ্কোচনের অন্যান্য প্রেক্ষিত স্পষ্ট হয়ে ওঠে। প্রাথমিক পণ্য জুন মাস থেকে সঙ্কুচিত হচ্ছে; মূলধনী পণ্য সূচক বা ক্যাপিটাল গুডস ইনডেক্স জুলাই ও আগস্ট মাস নাগাদ ঋণাত্মক হয়ে পড়ে; মধ্যবর্তী পণ্য উৎপাদন আগস্ট মাসে ঋণাত্মক হয়ে যায় এবং মে ও জুন উভয় মাসেই ঋণাত্মক ক্ষেত্রে থাকার পর নির্মাণ পণ্যগুলি আগস্ট মাসে ০.৬ শতাংশের সামান্য বৃদ্ধি প্রত্যক্ষ করে (চিত্র ২)। বাস্তবিক ভাবেই, বিগত প্রায় তিন মাস যাবৎ ক্ষেত্র নির্বিশেষে মন্থরতা এবং / অথবা সঙ্কোচনের এক অভিন্ন প্রবণতা লক্ষ করা গিয়েছে।

যদিও এই আলোচনায় ভোক্তা স্থিতিশীল ও অস্থিতিশীল… উভয় ক্ষেত্রেরই জুলাই ও আগস্ট মাসের মাসভিত্তিক সঙ্কোচনের তুলনা করা হয়েছে। ভোক্তা অস্থিতিশীল পণ্যের ক্ষেত্রে আগস্ট মাসে অধিকতর সঙ্কোচন পরিলক্ষিত হয়েছে। উৎসবের মরসুমের ঠিক আগে এ হেন প্রবণতা উদ্বেগজনক। আগামী দুই থেকে চার মাসের মধ্যে উৎসব সংক্রান্ত কেনা-বেচা ক্ষেত্রভিত্তিক বা সেক্টোরাল বৃদ্ধিকে সাহায্য করতে পারে। তবুও উৎপাদনের পরিপ্রেক্ষিতে এ ধরনের সঙ্কোচন, বিশেষ করে ভোক্তা অস্থিতিশীল পণ্যের ক্ষেত্রে (-৫.৮ শতাংশ), ভবিষ্যতে বৃদ্ধির সম্ভাবনা সংক্রান্ত সরকারি আশাবাদকে ভুল প্রমাণ করে।

ব্যবহারভিত্তিক শ্রেণিবিন্যাস দ্বারা কৃত ক্ষেত্রগত বা সেক্টোরাল মাসিক বৃদ্ধিহারের তুলনা একটি দুশ্চিন্তাজনক প্রবণতাকেই দর্শায়। আগামী কয়েক মাসের মধ্যে এই ধারার পরিবর্তন হোক বা না হোক, এটিকে সম্পূর্ণ রূপে অবহেলা করা দীর্ঘমেয়াদে মারাত্মক আকার ধারণ করতে পারে।

উচ্চতর খুচরো মুদ্রাস্ফীতি এবং উৎপাদনে মন্দার ফলে আয় বণ্টনের সর্বনিম্ন অংশের জন্য বেঁচে থাকার প্রতিবন্ধকতা বৃদ্ধি পাবে। পি এম গরিব কল্যাণ যোজনার মতো বিদ্যমান জনকল্যাণমূলক প্রকল্পের পরিসর বৃদ্ধি করে এবং সেটিকে সচল রেখে মৌলিক খাদ্য নিরাপত্তা সুনিশ্চিত করা প্রয়োজনীয়। আর কিছু না হোক, সরকার দ্বারা অর্থায়িত এই উদ্যোগগুলি জনসংখ্যার একটি উল্লেখযোগ্য অংশের বেঁচে থাকা সুনিশ্চিত করতে পারে।

মতামত লেখকের নিজস্ব।

The views expressed above belong to the author(s). ORF research and analyses now available on Telegram! Click here to access our curated content — blogs, longforms and interviews.

Abhijit was Senior Fellow with ORFs Economy and Growth Programme. His main areas of research include macroeconomics and public policy with core research areas in ...

Read More +