The international community has been engaged in negotiations around climate finance for three decades now, and working definitions continue to assign the role of funder to advanced economies, and that of recipient, to emerging ones. This brief makes a case for expanding such narrow definitions. It calls on countries such as India to re-imagine not only the idea of climate finance but also the mechanisms of raising funds and the channels for disbursing them. The aim should be to ensure that India builds financial resilience to serve its development needs, enabling the country to be a frontrunner in global efforts to decarbonise.

Attribution:

Charmi Mehta, “Re-imagining Climate Finance,”ORF Issue Brief No. 575, September 2022, Observer Research Foundation.

Introduction

Recent global and macroeconomic stress episodes have underlined the importance of crisis preparedness and resilience-building. The COVID-19 crisis, for one, has demonstrated how ‘tail events’ can cause extensive disruptions of economic activity that are otherwise taken for granted. The repercussions of the war in Ukraine have also made evident the urgency in cutting dependency on carbon-intensive energy and accelerating the transition to alternative sources such as renewables.

Upon the release of the Sixth Assessment Report of the Intergovernmental Panel on Climate Change (IPCC)[1]on 4 April 2022, India highlighted its justification of the country’s stance on promoting “equity at all scales” in climate action. The report appeared to echo India’s views on the necessity of public finance flows for developing countries and the need for scale, scope, and speed in climate finance extension and disbursement.

After two consecutive years of the Covid-19 pandemic, the COP26 in Glasgow shifted global focus back to climate change. Present warming projections[2]predict a 2.7°C rise over the next 80 years at current policy levels, indicating the need for enhanced measures and a carbon-neutral growth track for economies from hereon. COP26 and other consecutive reports are putting greater emphasis on the need for developed nations to actualise their climate finance commitments. This is an essential requirement to ensure developing nations are on-track to achieving their commitments. The issue is more complicated, however.

To begin with, the international community remains divided over the definition of ‘climate finance’. Absent a universally accepted definition, the United Nations Framework Convention on Climate Change UNFCCC has operationalised only a working definition so far. This has created widespread ambiguity in both the funding of climate projects[a]and, consequently, the determination of the amounts that must be mobilised. Therefore, ‘climate finance’ is one of the most loosely used terms when referring to initiatives that can catalyse decarbonisation. Compounding the challenge is that goal-posts often shift and commitments are not strong: indeed, the international community evaded commitments on climate finance disbursals for 17 years, from Rio (1992) to Copenhagen (2009).[b]The US$100-billion annual target set at Copenhagen, for mobilisation by 2020, was pushed to 2025 at Paris 2015. This seems to be the pattern on other elements of climate action as well, whether on global temperature limits, mitigation priorities, and technology transfer.

There are also concerns with what the mechanism of climate finance technically implies. Climate finance is generally known as financial flows mobilised by governments of industrialised countries and private entities that support climate change mitigation and adaptation in developing countries.[3]This means that funds allocated by national governments for energy/climate transition activities do not count as ‘climate finance’.

In the absence of a universally accepted definition for ‘climate finance’, it is all the more important to understand its role, and its rather limited context. This brief asks some key questions on the institutions, actors, and mechanisms that comprise the process. The aim is to challenge the notion that climate finance is the panacea to all global climate challenges.

International Negotiations on Climate Finance

From an early stage of climate negotiations, developed countries drew on existing official development assistance (ODA) budgets[c]to raise climate finance and have often opted to channel funds through bilateral institutions rather than multilateral funds. Only in 2001 did countries agree on the need for further funding and institutional arrangements, establishing three new funds: the Least Developed Countries Fund and the Special Climate Change Fund under the UNFCCC, and the Adaptation Fund under the Kyoto Protocol.[d],[4]Capitalising on these funds, however, has been difficult from the start and climate finance only rose to the top of the agenda in more recent rounds of negotiations, starting with the Bali Action Plan in 2007. Although the 2009 Copenhagen Summit may be seen as a failure in many ways, the Copenhagen Accord’s provisions on climate finance are widely viewed as a breakthrough. These include the target of mobilising jointly US$100 billion a year by 2020 ‘‘from a wide variety of sources, public and private, bilateral and multilateral, including alternative sources of finance,”[e],[5]—which would form the benchmark for the formal pledges made at Paris 2015.

At COP16 in Cancun in 2010, Parties established the Green Climate Fund (GCF; the second operating entity of the UNFCCCs financial mechanism) with the expectation that a significant share of climate finance would be channelled through this new fund.[f],[6]Despite the pledges at Paris to the Fund, and for climate finance more broadly, the US$100-billion target for mobilising public and private finance by 2020 is yet to be achieved. Estimates of current flows of both public and private finance use widely varying definitions and thus generate divergent conclusions.[7]Concerns remain that some pledged funding has not reached its intended beneficiaries[8]and is not clearly additional to existing aid flows or targets. These concerns can be broadly classified as problems of access to finance, as their disbursement has been resisted by a number of developed countries on grounds that they are unable to fund climate action overseas.

How have these problems of access arisen? Are the mechanisms of finance itself a problem, or is it another example of the lack of commitment to financing climate action? The succeeding sections of this brief will delve deeper into the channels of finance, the modes of finance, the nature of finance, and the quantum of it.

Global Mechanisms for Financing Climate Actions

Climate finance comes from four different sources: bilateral, multilateral, public, and private. A substantial portion of these funds is coordinated by four multilateral institutions: theGreen Climate Fund(GCF);Adaptation Fund; World Bank’sClimate Investment Funds(CIF); and theGlobal Environment Facility(GEF).[9]Developed nations can either extend financial support bilaterally or choose an institution through which they can channel their funds. These institutions, in turn, invest the funds committed, to projects that aid climate action and climate-induced disaster risk resilience and control. One of the key provisions of the 2015 Paris Agreement is facilitating access to financial assistance for mitigation and adaptation efforts. At COP15 in Copenhagen in 2009,[10]member nations committed to making US$100 billion available annually, in public and private resources to be raised by 2020, to aid climate action efforts.

Which projects receive funding

According to data gathered by Oxfam[11]and OECD,[12]nearly 70 percent of all climate finance between 2016 and 2018 went to middle-income countries. The least developed countries (LDCs) group received 14 percent of the total funding and small island developing states (SIDS) received 2 percent. Sixty-six percent of the total financing[13]has gone to mitigation projects,[g]and a far lower 24 percent to adaptation-based projects.[h]

Instances of priorities being solely concentrated on adaptation, as demonstrated often by private sector statements, lead to the assumption that the prioritisation and large volumes of expenditure on mitigation action (moving away from coal-based energy) are unwarranted and over-emphasised. The latest IPCC report also warns that warming is exceeding the ability of most systems to adapt.[14]

The nature of funding

International financial assistance is a complex field of study that can often be misleading. The mode of credit extension plays a dominant role in the net financial value of that credit. For example, grants have a higher net financial value than concessional loans, which in turn are more financially valuable than non-concessional loans.According to OECD,[15]between 2013 and 2018, the share of loans in climate finance grew from 52 percent to 74 percent, while that of grants decreased from 27 percent to 20 percent. Oxfam estimates that the annual average grant equivalent of reported climate finance in 2017–18 was US$25 billion.

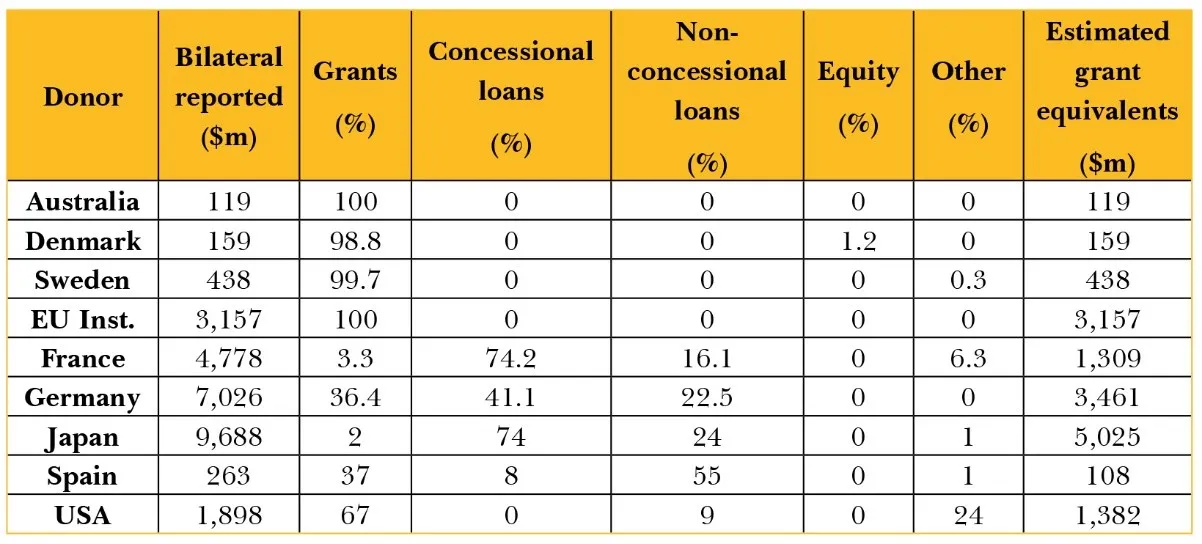

Table 1: Contributions of Big Donors, 2017-18 (in US$ million)

As Table 1 shows, apart from EU Institutions, larger contributing nations have extended more than 50 percent of their financing as non-grant equivalent.[i]Scandinavian countries such as Sweden and Denmark contributed close to 90 percent of their funds as grant equivalent.[j]Japan, Germany, and France were found to have contributed larger total amounts, but as non-grant. TheFourth Biennial Reportspublished by the OECD (2020) show that of the 80 percent climate finance that was extended as loans, over 40 percent was non-concessional, effectively lent at market rates. This implies that even in the scenario of financing for climate action coming through, it is not a grant but most likely a concessional or non-concessional loan.

The question of reporting the quantum of climate finance

Climate financing covers projects across sectors such as energy, infrastructure, and agriculture. The larger projects often have certain climate-sensitive objectives and features, despite the project overall not being green/climate-compliant. It is essential to identify whether climate action is the primary objective of a project, or one amongst many—and count only the former as climate finance. These objectives are tagged on the Rio Marker,[17]and some analysts say donor nations could be over-reporting their contributions by including large infrastructure projects with remote carbon-cuts as part of their climate finance investments.[18]

For example, in 2017–18, Japan reported over US$700 million[19]in climate finance towards its Matarbari Ultra Super Critical Coal-Fired Power Project in Bangladesh. Japan called the loan, ‘climate finance’ as the plant produces less GHG emissions than a similarly sized fossil-based plant. However, most analysts agree that coal plants are not climate-sensitive.[20]The overall lack of transparency makes it difficult to assess whether other countries have also reported similar coal-fired projects to the UNFCCC in 2017–18. If unchecked, this trend will only end up benefiting fossil-based energy giants. Indeed, it is difficult to ascertain actual amounts being channelled to climate finance because of gaps in data that could otherwise allow for a systematic verification of projects. Some analysts theorise that global climate finance flows could be around one-third lower than what is usually calculated.[21]

Re-imagining Climate Finance

The last two decades have witnessed a number of shocks including wars, cross-border skirmishes, disease outbreaks, and a pandemic, that warranted the emergency diversion of critical funds earmarked for climate action. COVID-19 deeply impacted the fiscal capacities of most nations, with significant resources being diverted to post-pandemic recovery through 2020-2021. The Russia-Ukraine war has added to growing global anxieties, likely to provoke increased defence spending. Countries like India are experiencing extreme weather events such as successive heatwaves and super-cyclones. The global climate refugee crisis has arrived far earlier than predicted, and funds will be needed for humanitarian relief across developing countries where large populations are vulnerable. While the Paris climate pact acknowledged the ‘common but differentiated responsibilities and capabilities’ of wealthier and emerging economies, it was only the first step.

The current understanding of climate finance is more procedural than substantive. It lays out the scope of transfer of funds—i.e., from the developed to the developing world—but it does not clearly lay out what should be, or what can be, financed. India must lead the way in re-imagining climate finance. The following paragraphs outline the fundamental elements of such a redefinition.

Building financial resilience

India has integrated various elements of its climate agenda within its national development priorities through ministry-level budgets and state-sponsored schemes at the central and state levels. These include the push for electric public and private transport (FAME scheme),[22]supplementing fossil-based fuels with renewables in the energy mix,[23]and incentivising micro-irrigation through interest-free loans (PM-Krishi Sinchai Yojana).[24]These efforts need to be expanded to each ministry across all tiers of governments, most importantly at the local levels, to ensure that climate action needs are fully serviced through domestic budgetary allocations. Mobilising climate capital at scale has always been a challenge, particularly in the Global South, as these countries’ financial systems are ill-equipped to account for climate risks in their capital allocation and disbursement processes, and at applying a climate justice prism in their investment decision-making.[25]

Harnessing existing modes of public finance and budgetary allocations to achieve climate goals will enable India to be autonomous from international obligations. Building this capability will allow the country to define its own priorities for climate action.

Table 1 highlights how loans are the predominant means of climate financing, and not grants being doled out to the developing world. These loans come with terms and conditions to be fulfilled, and interest to be paid. The question is whether it is in India’s best interest to chase funds that are no different from other loan facilities that the government obtains from international financial institutions. It is also imperative to determine whether other means exist by which such capital can be generated and mobilised by re-aligning existing public finance expenditure being handled by the line ministries. Nurturing financial autonomy for climate action will be a critical step in India’s foreign policy of multi-alignment as well, as it seeks to remain equidistant from all.[26]

Using monetary policy to incentivise green investments

Climate change poses systemic risks to the financial systems of a country by way of climate calamities, environmental degradation, or carbon-driven pollution. Green finance is a mechanism that has the potential to mitigate risks if promoted and appropriated rightly.

In recent times, central banks have used micro and macro prudential tools, market development techniques, and financial governance-based initiatives to promote, nurture and incentivise green finance lending. Central Banks in countries as varied as China, Lebanon, Brazil, and Bangladesh, are increasingly veering towards this route, taking a more incentives-based approach to encouraging green investments. In 2006, China introduced credit restrictions on domestic companies based on their environmental compliances.[27]Lebanon, meanwhile, implemented a policy of differential reserve requirement for commercial banks in 2010, wherein the banks with larger shares of green projects in their loan portfolio are required to hold less reserves.[28]

In 2011, Brazil embedded environmental considerations into the banks’ Internal Process of Capital Adequacy Assessment by considering lending exposure to the projects containing environmental and social risks.[29]Eventually, Brazil recommended that banks outline their risk assessment methods and exposure to social and environmental damages in their annual reports in 2017. India needs to urgently explore similar financial-regulatory interventions that effectively encourage and incentivise and influence/promote green finance.[30]A 2022 report by the RBI on climate risks and sustainable finance highlights findings from its survey of 34 banks. For one-third of the banks surveyed, responsibility for overseeing climate-related risks was yet to be assigned. Additionally, only a few banks have ESG considerations[k]during performance evaluation. While banks are transitioning to low-carbon exposure by tapping into green lending and investment and green deposits, almost none of the commercial banks have aligned their climate disclosure policies to any internationally accepted framework.[31]In another survey conducted in early 2022, none of the banks analysed (34 scheduled Indian banks) have assessed the resilience of their portfolios in the face of climate change. Only two of them have committed to stop funding new coal power plants.[32]

Exploring bilateral over multilateral channels

Multilateral efforts to mobilise large funds have seldom worked, due to an obvious distrust for the very idea of contributing money to a pool that can fund any type of country, with the financing nation losing any controls over the country being financed. On the sidelines of the COP26, the Just Energy Transition Partnership (JETP)[33]was inked between South Africa, on one side, and the US, UK, France, and Germany (and EU)The latter countries pledged US$ 8.5 billion over the next five years to fund South Africa’s ‘just energy transition’ from coal to renewables. This is an example that other developing countries could emulate. Just as the ODA mechanisms at one point were successfully used for climate projects, India must learn from the shortcomings of multilateral processes and mobilise its existing relationships with countries that can be partners to the country’s development goals.

Effective private sector incentive structures

Large global institutional funds are investing in India at present.[34]However, Indian banks and financial institutions are not keeping up with their global counterparts on green finance lending. A 2019 report by FairFinance found that Indian banks do well on the metrics of financial inclusion, but poorly on those of environment, nature and climate, human rights, and labour rights.[35]

Banks can have a positive impact on environmental sustainability and reduce risks of climate change by screening for companies that are committed to protecting biodiversity, reducing their GHG emissions, and supporting a just transition to a low-carbon economy.[36]Funds for climate action in India contribute only around 0.05 percent of the global assets in sustainable funds.[37]

The US Securities Exchange Commission in March 2022, made climate risk disclosures mandatory for listed companies.[38]In 2012, SEBI mandated the top 100 listed entities by market capitalisation to file Business Responsibility Reports (BRR) as part of their annual report, as per the disclosure requirement emanating from the ‘National Voluntary Guidelines on Social, Environmental and Economic Responsibilities of Business’ (NVGs).[39]The requirement for filing BRRs was progressively extended to the top 500 listed entities by market capitalisation in 2015, and to the top 1000 listed entities in 2019. This needs to expand to cover sustainability and ESG-linked disclosures, which must become a norm for financial and non-financial companies in India rather than a voluntary ‘good’ practice.

Institutionalising climate finance domestically

India holds tremendous potential for harnessing climate action funding. Green finance flows in India reached INR 1,11,000 crores (USD 17 billion) for FY 2017 and INR 1,37,000 crores (USD 21 billion) for FY 2018. The average stands at INR 1,24,000 crores (USD 19 billion) per annum, while the total tracked green finance for the years 2016-2018 is pegged at INR 2,48,000 crores (USD 38 billion). Of this, 85 percent was raised domestically.[40]This demonstrates an existing capacity within the country’s financial sector to mobilise funds for climate action.

Public procurement accounts for nearly 15-20 percent of GDP in India, holding the power to greatly influence manufacturing processes through market signalling.[41]Green procurement is being increasingly adopted and explored, for its ability to incentivise Indian manufacturers to shift to greener processes, and prepare domestic manufacturing sectors to face restrictions such as CBAs (carbon border adjustments) which have been legislated by the EU last year.[42]

Investing in capacities for climate action will have percolating development benefits which, in turn, will lead to an improved economic world order with strengthened financial capacities of the developing nations. A green and inclusive economic recovery will positively influence all forms of capital[43]—physical, human, natural, and social. Trends in the extension of financial aid and support for climate action will be key in determining the course of climate action undertaken across the range of low- and middle-income countries.

Conclusion

When thinking about climate action, the finance, economics and politics of the network are key components to account for. First, the strong positive relationship between climate protection and macroeconomic performance and financial stability, make it critical tostrengthen the climate information architecture, so that it can inform climate-related macro-financial policies and enablecentral banks and financial regulators to systematically integrate climate risk assessments into their financial stability frameworks. Second, the quality of the finance and its economic implications will shape the kind of projects and programmes that countries put in place, and the extent to which they go.

Third, the political and international narratives around climate action must evolve. Global dialogues and negotiations must no longer attempt to coerce developing nations into promising greater actions. This will only hamper consensus built so far. As access to finance continues to be a barrier in many economies, incremental efforts towards mobilising public and private finance must be explored, first, domestically. In some economies, climate finance flows need to increase by four to eight times until 2030, according to latest estimates from the Intergovernmental Panel on Climate Change.[44]The time is right to move away from global thinking on this subject, and develop a resilient and independent thought process on climate action financing.

Endnotes

[a]It is not clear, for instance, what type of projects classify as ‘climate projects’.

[b]At the Rio Earth Summit or Rio Convention (June 1992), the UNFCCC formally lanched the Conference of Parties Dialogue, which has come to be commonly known as COP. The Copenhagen Summit took place in December 2009.

[f]UNFCCC 2010: Decision 1/CP.16, paragraphs 100 and 102.

[g]Mitigation entails the reduction of emissions into the atmosphere, by increasing the share of renewable energy, or establishing electrified mobility systems, for example.

[h]Adaptation includes large-scale infrastructure changes, such as building resilient structures to withstand the impacts of sea-level rise, as well as undertaking behavioural modification through actions such as waste management through treatment and mainstreaming recycled products. Adaptation projects focus on capacity-building and form the keystone of minimising climate-induced losses and damages in the future.

[i] These include non-concessional loans and equity.

[j] Though the contributions as a share of the total climate finance flows were lower in value, when compared to other countries such as Germany, France and Japan, which contributed hugely to fund flows, but with less that 40% being a grant component.

[k]‘ESG’ refers to Environmental, Social and Governance parameters that govern an ‘ESG’ audit. This is done to determine and assess companies’ adherence to principles of environmental compliances, social justice and integrity, and sound governance.

[3]Stadelmann M, Michaelowa A, Roberts T, Difficulties in accounting for private finance in international climate policy.Climate Policy13(6): 718–737 (2013).

[9]Clapp C, Ellis J, Benn J, Corfee-Morlot J,Tracking Climate Finance: What and How? Organisation for Economic Co-operation and Development.Paris (2012).

[27]Feng Wang, Siyui Yang, Ann Reisner and Na Liu, Does Green Credit Policy Work in China? The Correlation between Green Credit and Corporate Environmental Information Disclosure Quality, MDPI, 2019.

[30]Sourabh Ghosh, Siddhartha Nath and Abhishek Ranjan,Green Finance in India: progress and challenges,Strategic Research Unit of Department of Economic and Policy Research (DEPR), Reserve Bank of India (2021).

The views expressed above belong to the author(s). ORF research and analyses now available on Telegram! Click here to access our curated content — blogs, longforms and interviews.

Charmi Mehta is a Research Consultant with the Asian Development Bank and the Chennai Mathematical Institute. Her research interests lie at the intersection of public ...

PDF Download

PDF Download