Impact Investments in India: Towards Sustainable Development

Renita D'souza

Conventional investments cater to investors who intend to gain financial returns. Other investors whose aim is to generate a positive social or environmental impact at a decent rate of return, turn to “impact investments” for their purpose. Mobilised to finance social enterprises, impact investments assume three primary forms: embedded, integrated, and external. This paper discusses the ideas of impact investment and social enterprises, and outlines India’s impact investment landscape. The paper illustrates the footprint generated by impact investment funds in India, describes the challenges facing the sector, and offers recommendations for a blueprint for an impact investment ecosystem in the country.

Attribution:

Renita D’Souza, “Impact Investments in India: Towards Sustainable Development”, ORF Occasional Paper No. 256, June 2020, Observer Research Foundation.

Introduction

Neoclassical economic theory models human behaviour on their pursuit of self-interest. A fundamental characteristic of thehomo economicusis narrow self-interest. The consumer maximises their utility, the producer maximises profit, and the investor maximises the rate of return, subject to the minimisation of risks. However, observed economic behaviour has conformed to other motivations: fairness, reciprocity, altruism and impure altruism, generating a warm glow effect and adherence to social norms.[1]Behavioural economics has produced rich literature to account for behaviour that deviates from pure self-interest. Although standard economic theory postulates that people will readily exploit others for their selfish gains, individuals across diverse contexts invest in avenues that generate income for them in a manner that does not yield unproductive outcomes for others. Much of the resources in the form of time and money are also spent on public goods.

Conventional investment opportunities that seek to maximise the rate of return cater to narrow self-interests. What about those who wish to invest in positive social impacts and outcomes without desiring market rates of return? Catering to this segment of the population gives birth to a new space of investment avenues, which in turn expands the size of total investible resources. This new space is known as ‘impact investing’ or ‘social impact investing’.[a]

However, the desirable level of sustained progress has not been achieved in the past decades. The progress and advancement seen in the 20thcentury and the first half of the 21stcentury came at the expense of rising inequality—making the poor even poorer, giving rise to health disorders and disease, eventually leading to environmental degradation and ecological imbalance. Such progress will not only have diminishing returns, but the returns will eventually turn negative. To keep the flow of returns positive, sustainability must be incorporated into growth and development, an objective compatible with the UN Sustainable Development Goals (SDGs), which the international community agreed to fulfil by 2030. The pursuit of these goals as the global drivers of growth and development has changed the philosophy of progress.

This has also changed the way investments are construed. After all, investments are nothing but the point of commencement of any growth or development trajectory by determining how resources will be utilised. Therefore, an investment that corresponds to sustainable development should be a ‘sustainable investment’. Social impact investment meets this requirement.

Just as all future development is expected to be sustainable, so should all investment. The UN estimates that to achieve the SDGs by 2030, developing nations must invest about US$3.9 trillion annually, while the private and public sectors must invest only US$1.4 trillion, implying an investment gap of US$2.5 trillion.[2]Social impact investments are expected to fill this gap. Impact investments pre-empt changes in the way financial decisions were made in the past to now incorporate social and environmental concerns in generating financial returns. By examining India’s progress on the various SDGs through the NITI Aayog’s SDG India Index (see Conclusion), this report reiterates the need for impact investments to complement the government’s efforts towards achieving the goals by 2030.

This report explores the challenges faced by impact investments in the space of debt and equity and recommends ways to deal with them. Evaluating the problems of and potential solutions to social and development impact bonds is beyond the scope of this report.

Exploring Impact Investment

Although the term impact investment has gained currency in the last decade, its roots can be traced back to the compulsion of economic activity being driven by religious concerns of ethics and morals.[3]For instance, the Quakers of the 18th century consciously avoided investing in firms and commodities that oppressed humankind in any way.[4]Impact investments have gained momentum in the aftermath of the 2007-08 financial crisis.[5]This has been ascribed to the transition of values, with Generation X and millennials seeking greater accountability and responsibility towards society and the environment in investment decision-making.[6]The concept of impact investment was born in affluent societies like the US and Europe, where philanthropic choices are more accessible to a larger segment of the population as compared to developing nations with poorer populations. According to the Global Impact Investment Network, impact investments are equal to a small fraction of commercial investments and are still in their nascent stages of development.[7]

Definition

Impact investment can be defined as “the use of for-profit investment to address social and environmental problems. The Monitor Institute defines the term as “making investments that create social and environmental value as well as financial return.””[8]

The idea of impact investment is based upon three precepts:[9]

A conscious aversion towards investing in initiatives that are harmful to social and environmental concerns

Development of a new source of investment capital for social and sustainable enterprises and entrepreneurs

Taking the first rule further to bring about positive transformation (either social or environmental). This precept distinguishes impact investment from sustainable and responsible investment, and puts impact investment closer to philanthropic/non-profit finance on the continuum between this form of funding and conventional finance. Impact investments may receive muted returns. This return differential accounts for the social or environmental impact that compensates for the muted returns.

For an investment to qualify as impact investment, it must satisfy all three precepts simultaneously.[10]

Features

Impact investment strategy is often conflated with an asset class. Asset classes that are used to channel impact investments include impact equity, impact fixed income and impact alternative assets (private equity, venture capital, debt). Impact investment funds are invested as seed or early-stage capital, as well as debt and growth capital.[11]

The motivation underlying philanthropy/donations and impact investments are somewhat similar but differ in the operational sense. Impact investments are outcomes/performance-driven and seek to deliver measurable social/environmental impact. The latter compulsion introduces accountability and transparency in the way impact investments utilise resources. This is not to say that pure philanthropy is not accountable. One intends to emphasise the role of measurability in enhancing such accountability. Social/environmental outcomes accompanied by financial returns can be more effective in achieving such results.[12]

Philosophical foundations

As a dual bottom line approach aspiring for financial and social returns, the impact investment paradigm is underpinned by both consequentialism and Kantian deontological ethics.[13]In espousing consequentialism, the impact investment approach is concerned with the consequences of the investing exercise. Here the outcomes relate to an increase or decrease in social welfare without concerns about how this welfare was brought about. The moral character of the consequences is considered by the consequentialist view. The way in which these consequences have been generated may very well violate morals and ethics. This is corrected by an espousal to the deontological school of morality, which focuses on the intrinsic moral character of the activity or operation generating the outcome. This moral character is inherently altruistic, such that the action needs to rightly be placed in terms of ethics and values (whether the action is right or wrong matters), and consequently, generate a positive impact for all. Nobody should benefit at the cost of others. Being underpinned by both concerns of maximum welfare and intrinsic morality of actions undertaken make impact investment attractive from a sustainability viewpoint as well.[14]

The ‘Creating Social Value’ proposition

Impact investments resonate strongly with the thesis ofCreating Social Value(CSV) propounded by Michael Porter and Mark Kramer. CSV advocates a transformation of capitalism to accommodate the synergies of economic value and social progress. Businesses must be driven not by the exclusive concerns of shareholder returns but also by the need to solve societal and environmental challenges. A business governed by this proposition incorporates sustainability and unmet social needs as the constraints to a profit maximisation problem. In doing so, the firm considers and minimises its long-term costs to maximise its long-term profits. This transformation in a business’s philosophy can be founded upon impact investments. The CSV proposition can be envisioned as the theoretical underpinning of an impact investment enterprise.[15]

According to Porter and Kramer, “The concept of shared value…. recognizes that societal needs, not just conventional economic needs, define markets. It also recognizes that social harms or weaknesses frequently create internal costs for firms—such as wasted energy or raw materials, costly accidents, and the need for remedial training to compensate for inadequacies in education. And addressing societal harms and constraints does not necessarily raise costs for firms, because they can innovate through using new technologies, operating methods, and management approaches—and as a result, increase their productivity and expand their markets.”[16]

Porter and Kramer go on to emphasise the relationship between a profiteering enterprise and a developed and vibrant community. While the community is the source of demand for the business and the provider of crucial public infrastructure and ecosystem, the business provides employment and access to income generation opportunities for the community. In this new version of capitalism, the normal functioning and operation of the enterprise amount to social gain and impact. Profit is now to be seen as a complement to social progress.[17]

Porter and Kramer see three ways to create shared value—“by reconceiving products and markets, redefining productivity in the value chain, and building supportive industry clusters at the company’s locations.”[18]

Reconceiving products and markets:The CSV proposition prompts businesses to seek opportunities to launch new products and tap new markets by focussing on the unmet social needs and the underserved communities of the global economy.[19]

Redefining productivity in the value chain:There is a symbiosis between social progress and productivity, which was traditionally undermined. Productivity influences and is influenced by natural resources, working conditions of employees, health and safety. Identifying social harms in the value chains becomes an opportunity for innovation in operation and increased productivity. The CSV thesis is now manifesting in concerns about energy efficiency, prudent uses of scarce resources, sustainable ways of procurement and distribution, and investing in employee productivity. The rationale for locating activities is becoming more local in nature.[20]

Building supportive industry clusters:Firms thrive on geographic concentrations, or ‘clusters’, which include supporting industries, services and logistics providers, academic institutions, and trade and standards enforcements institutions. The role played by each of these entities is crucial to the firms’ productivity. The CSV thesis proposes the creation of shared value by investing in the supporting infrastructure and ecosystem. Since this is a gigantic task, firms may enrol other stakeholders to collaborate on the task.[21]

The ultimate goal of the CSV mandate is to kickstart “a positive cycle of company and community prosperity, which leads to profits that endure.”

Social Enterprises

Social enterprises are entities that put the impact investment funds into action, and can be classified in a variety of ways (see Table 1).

Table 1: Classification of social enterprises

Type

Meaning

Examples

Embedded social enterprise

In this form of enterprise, the business operations and activities coincide with social impact endeavours. Social initiatives rely on the finances (revenues and profits) of the enterprises, which allow them to operate as self-sustaining entities. The social outcome is the objective of the business and therefore the clients of the business are none other than the beneficiaries of the social outcome. The financial and social returns are achieved simultaneously. This is the strongest instantiation of the impact investment mandate. Typically, an embedded social enterprise takes the form of a non-profit structure to prevent mission drift; it may also assume a for-profit structure contingent on the legal circumstances.[22]

TheEntrepreneur Support Modelinvolves the provision of business support and financial facilities to the clientele. The clients are self-employed or firms, such as microfinance institutions or SMEs. Example: Pro Mujer.[23]

TheMarket Intermediary Modelrefers to providing value-added services such as production, marketing and credit facilitation, and product enhancement to small producers. Such producers include cooperatives, and fair trade, agriculture and handicrafts organisations. The final objective is to sell the product produced by the client in high-margin markets at a mark-up.

Example: TOPLA[24]

TheEmployment Modelinvolves providing employment opportunities, skill and job training and a conducive working environment for the clientele. Clients are usually low-income individuals, especially women, the handicapped, reformed juveniles and the homeless. The businesses that generate such employment include bookshops, cafes, and carpentry and repair.

Example: Digital Divide Data[25]

TheFee for Service Modelis popularly used by schools, museums, hospitals and other such institutions to commercialise the social services provided by them.

Example: Bookshare.org[26]

Examples in India: SKS Microfinance, Amul, SEWA

Integrated social enterprises

Such enterprises have an overlap between their social and business mandates. Both sets of activities share costs and resources, and leverage tangible and intangible resources such as competencies, brands, goodwill, relationships and infrastructure. In this sense, the social and business activities are symbiotic.[27]

TheService Subsidisation Modelinvolves the enterprise selling self-produced goods and services on the external market, and utilising the proceeds to finance its social impact mandate.

Example: Associacao Nacional de Cooperacao Agricola (ANCA)[28]

Examples in India: Scojo India, Aravind Eye Care

External social enterprises

The social activities of such enterprises are clearly distinct from their business operations. Generally, a non-profit sets up an external enterprise to generate finance to sustain its social programmes and operating expenses. To that extent, the business is detached from the social mission of the parent non-profit.[29]

TheOrganisational Support Modelsells products on the external market to generate net revenues that are used to finance the social agenda of the parent non-profit.

Example:Parla La Salud[30]

Examples in India:

1. Financial arm: Waste Wise Corporation; Social arm: Waste Wise Trust 2. Financial arm: Industree Crafts Pvt. Ltd. (Mother India); Social arm: Industree Crafts Foundation

Source:The Four Lenses Strategic Framework: Towards an integrated social enterprise methodology

Behavioural finance and impact investments

Conventional investment thinking might create barriers to the off take of impact investments. Investing in embedded social enterprises is apparently at loggerheads with making mainstream investments in a profit maximising firm. Given the potential of impact investments to achieve the SDG goals, it is pertinent to think about how to remove barriers to the rise in such investments. The principles of behavioural finance in terms of the three Fs—familiarity, framing and fear—need to be incorporated in the way impact investment is approached. The three Fs apply to the decisions made by individuals who seek to assume the role of impact investors but shy away from doing so due to an overestimation of risks.

Creating familiarity with the impact investments by appropriately framing them to iterate the similarities with usual forms of investments is the first rule. The second rule is to tackle irrational fear that has risen from looking at sectors that have discouraged other investors since they did not find the right opportunities. Such fear needs to be tackled by distinguishing between seeking and finding. In contrast to mainstream investors, impact investors need to be warned about underestimating risks associated with impact investments. There is a difference in the way risk is perceived in the context of impact investments in the behavioural framework. It is just as much about the probability of missed goals of financial and social returns as it is about volatility.[31]

Understanding impact investors’ decision-making

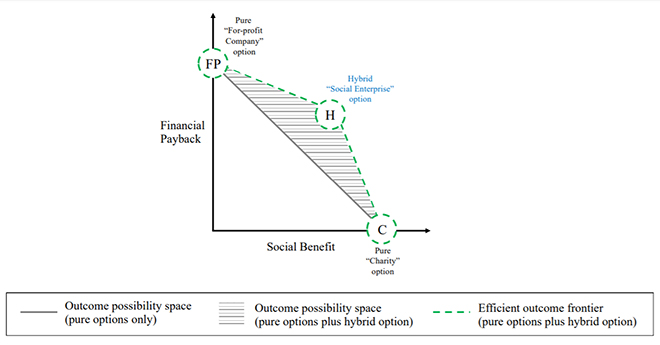

The economic rationale for impact investing is the joint optimisation of financial and social returns rather than separate optimisation exercises for each.[32]Impact investors work with hybrid options, such as social enterprises, for such joint optimisation exercises. Instead of the conventional “efficient frontier” of the traditional portfolio theory, which is a locus of risk-return combinations, the impact investors work with the “efficient outcome frontier” defined by the greatest financial return for each specific level of social return.[33]

Impact investors are not just driven by self-interest, they are altruistic and have pro-social preferences. The utility function of an impact investor is: U=U(Xf,Xs), where Xfrepresents financial returns and Xsstands for social returns. Further, [34]

Before the introduction of a social enterprise, the investor must decide how to allocate a sum across two “pure” options. For simplicity, assume a risk-free scenario. The investor can allocate the entire amount to the first pure option, a charity, to obtain a constant social benefit per unit of investment with nil financial return. The second pure option is to invest in a for-profit company, to accrue a consistent financial return per unit of investment with no social increments. The investor’s “outcome possibility space” is defined by the set of combinations available to invest entirely in either the charity or the for-profit company, plus all non-negative linear combinations thereof (indicated in Figure 1 as points FP (a for-profit company) and C (charity)). The impact investor who seeks to maximise output should choose a point on the segment (FP, C) that maximises their utility function, U = U = U (Xf(FP),Xs(C) ).[35]

Now consider the entry of a social enterprise that represents a hybrid of the pure charity option and the pure profit option. This results in an expansion of the outcome possibility space from a line FP-C to a triangle FP-H-C. The impact investor who seeks to maximise output will then choose a point in the space of triangle (FP-C-H), and the corresponding utility function will be U= U(Xf(FP, H),Xs(C, H)).[36]

Figure 1:Outcome possibility space and efficient outcome frontier for a stylised impact investing decision

Source:Outcome Efficiency in Impact Investing Decisions, INSEAD Working paper series 2018/32/STR, July 2018

If the marginal outcomes following from investing in the social enterprise dominate the convex combination of the pure options, then the outcome possibility space and the efficient outcome frontier should bulge outwards. If the marginal outcomes following from investing in the social enterprise are dominated by the convex combination of the pure options, then the outcome possibility space should bulge inward, and the efficient outcome frontier remains the same.[37]

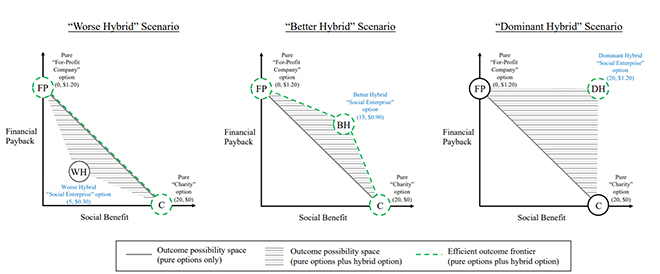

An impact investor must make decisions in three key scenarios (See Figure 2):

Figure 2:Three task scenarios with varied hybrid options

Source:Outcome Efficiency in Impact Investing Decisions, INSEAD Working paper series 2018/32/STR, July 2018

Worse hybrid case: This represents a scenario wherein the marginal outcomes following from investing in the social enterprise are dominated by the convex combination of the pure investment options.[38]Optimal choice zone:Not the hybrid option and the associated marginal outcomes; instead, any point on the linear combination of the pure investment options would be chosen.[39]In this case, the outcomes associated with investing in social enterprises are inferior in terms of both financial and social returns. This implies that rather than opting for impact investment, the economic agents prefer to separate their investments for generating a financial return from charitable donations.

Better hybrid case: In this case, one of the pure investments exceeds that of the levels achieved by the marginal outcomes of the social enterprise, and the other pure investment option is lower than the levels achieved by marginal outcomes of the social enterprise.[40]Optimal choice zone:Not the line produced by the convex combinations of pure investment option; instead, investing partially in one of the pure investment options and the remaining in the social enterprise.[41]Here the economic agents split their resources in making impact investments along with either investing in a profit-making enterprise or donating to charity.

Dominant hybrid Case: In this case, the levels achieved by marginal outcomes of the social enterprise are equal to or greater than the outcomes achieved by the pure investment options.[42]Optimal choice zone:Investment in the social enterprise itself. Here the entire sum is invested in social enterprises/impact investments. Investing entirely in impact investment is unambiguously the optimal choice.

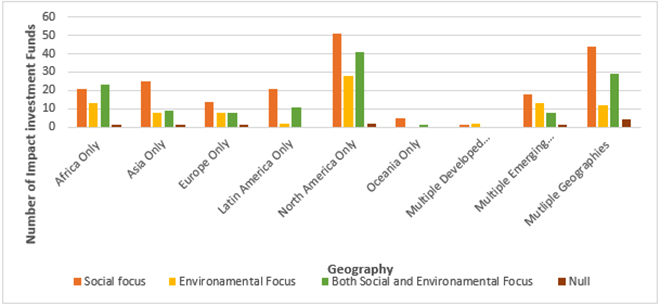

The Global Impact Investment Landscape

The highest number of impact funds are invested in North America (129), followed by Africa (58) and Asia (43).[43]If fund investments in the ‘multiple emerging markets’ category were to be added to the number of funds located in Africa and Asia, the figure will be substantial, indicating the interest in impact investments in emerging economies. Most impact investment funds are driven by the motivation of generating positive social outcomes. There is also a focus on creating positive social and environmental results. The least focus, though quite impressive in absolute terms, is on producing an exclusive environmental impact.

Figure 3: Distribution of impact investments by geography and theme

Source:Impact Base Data[44]

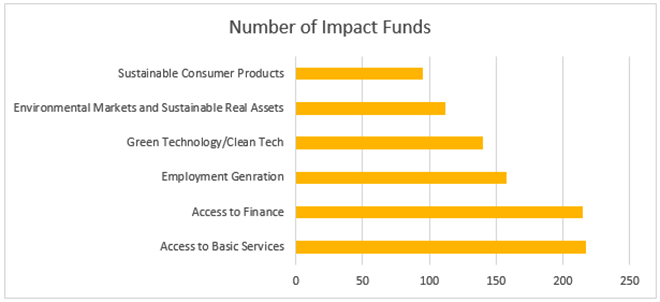

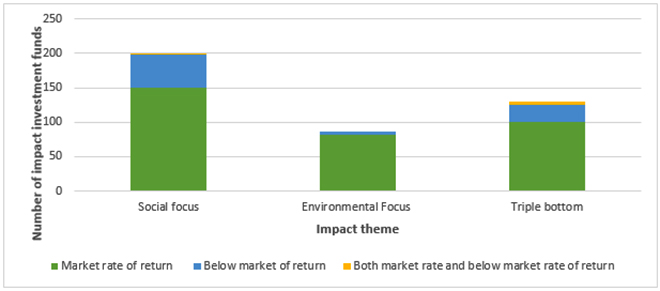

Social focus drives impact investments, which includes the focus on access to basic services, and finance and employment generation (See Figure 4).

Figure 4: Distribution of impact investment funds across impact themes

Source:Impact Base Data

Most impact investments funds across categories earn a market rate of return, which is contrary to the conventional belief that seeking a positive social or environmental return involves forgoing a portion of the financial gain.

Figure 5: Classification of impact investment funds according to the earned rate of return

Source:Impact Base data

A Survey of India’s Impact Investment Landscape

The birth of India’s impact investment sector can be traced to the launch of the milk co-operative Amul and the priority lending exercise by the banking sector. Impact investment emerged as a systematic investment strategy when Aavishkaar and Acumen were set up in 2001. Soon, India became one of the most active destinations for impact investment in South Asia.

The Impact Investors’ Council is the central organisation representing impact investors in the country. This council currently consists of 30 members, including Aavishkaar, Acumen, Ankur Capital, Asha Impact, Ananya Finance, Omidyar Network, Unitus Ventures, Elevar Equity, MacArthur Foundation, KKR, Oiko Credit and Tata Capital.

India has about two million social enterprises and at least 75 active impact investors.[45] India’s impact investors can be classified into three categories: fund managers (such as Aavishkaar, Acumen and Elevar); development finance institutions (such as National Bank for Agriculture and Rural Development and FMO Entrepreneurial Development Bank); and foundations, high-net-worth individuals and family offices (such as Omidyar Network, Michael and Susan Dell Foundation).

India’s impact investment sector garnered over US$5.2 billion between 2010 and 2016.[46] As of 2015, development finance institutions (DFIs) accounted for over 90 percent of impact investments in India, determining the sector’s trends in the process.[47]DFIs have invested nearly US$5 billion in India, as of 2015, while other impact investors have invested only US$438 million. Impact investments from non-DFI sources rose substantially since then. As of 2017, endowment funds (US$5.5 million), DFIs (US$5.3 million) and banks (US$4.6 million) are the dominant sources of impact investments in the country. Surprisingly, charitable organisations and donor-advised funds have hardly contributed to impact investments in the country.[48]The impact investment sector has failed to attract domestic funds.[49]

The value of total assets under management ranges from US$0.15 million to US$88.97 million.[50]About half of all impact investors invested an amount greater than US$20 million in 2018, of which three-fourths were in equity, 17 percent exclusively in debt, and 8 percent in debt, equity and blended instruments.[51]About 67 percent of India’s impact investors accrued a rate of return higher than 15 percent, eight percent earned about 10-15 percent, while the remaining 25 percent received about five to 10 percent.[52]Equity remains the popular instrument in the asset class representing impact investments.[53]The average deal size of investments lies between US$1,00,000 and US$10 million. Impact investments are mainly made in social enterprises located in Western and Southern India.[54]

The venture approach is the most common business model for impact investments. The underlying principle for such funds is to invest at early stages in for-profit enterprises operating in markets catering to the vulnerable, weaker and underserved sections of society, to demonstrate their investible potential and unlock mainstream capital for these enterprises. However, mainstream investors have invested significantly at early stages and the first round in the venture initiatives, obscuring the distinction between them and the impact investors.[55]

Three key issues plague India’s impact investment landscape:[56]

Lack of appropriate capital across the risk-return continuum

Lack of suitable exit options

Lack of sound impact measurement methods

Table 2: Percentage of impact investments and expected rate of return across sectors in India

Sector

Percentage of impact investors investing in the sector(in percent)

Rate of return expected by impact investors (in percent)

Agriculture

67

>20

Education

67

5-20

Health care

58

15-20

Financial Services (excluding microfinance)

58

10-15

Housing

33

5-10

Skilling

25

5-10

Source:The promise of Impact Investment in India, Brookings Institution Report.[57]

As of 2016, the sectors that attracted large amounts of impact investments were, in the order of preference, financial inclusion, clean energy, education, agriculture and healthcare. The investment trends have changed with agriculture and education at the top, followed by healthcare. Impact investors invest heavily in sectors they expect will allow them to earn a higher rate of return (See Table 2). This is not compatible with the philosophy of impact investments. Conventionally, larger the size of investments, higher the rate of return. In impact investments, the investor seeks positive social and environmental outcome, even at the cost of reduced financial returns. The data in Table 2 can either be interpreted as suggesting that investments are coming from mainstream investors who behave like impact investors by investing in social and environmental sectors, or that impact investors are finding it difficult to invest in these sectors due to some constraints. Solutions to the first case are discussed later in the report. As for the second, the government must ease the limitations faced by prospective investors.

Impact generated by impact investment funds

There is no single method of measuring impact. Utilising information provided on the websites and annual reports of the Aavishkaar Group (2018), Asha Impact (2019), Caspian (2019) and Oiko Credit (2019), an attempt has been made to briefly survey the effect some impact investment enterprises have had in India. The survey is only illustrative and by no means exhaustive.

It highlights how the four companies have chosen to quantify their impact. It also highlights the kind of activities that are being financed under impact investment. The four firms were selected because they have the most comprehensive and detailed reports on annual performance and are unambiguous on their progress. They have also articulated the impact generated by them in terms of their contribution to various SDGs.

Table 3: Impact generated by impact investment firms

Name of the enterprise

Impact generated since inception

Aavishkaar Group[58]

(The group incubates social entrepreneurs to create beneficiaries across 13 SDGs)

· Of the companies assisted,

– 85 percent were set up by first time entrepreneurs

– 78 percent operate in low income states and frontier markets

– 30 percent were founded by women or have women on the board

– 87 percent were assisted during seed or growth stage

· There were 105 million end beneficiaries, of which 55 percent were women

· 93 million enjoyed access to education, health, financial services.

· Several livelihoods created and huge economic value generated

· More than 43,000 MT of waste recycled

· 1.4 million MT of carbon emissions reduced.

Asha Impact[59]

(Affordable housing, healthcare, education, waste management, agricultural and rural distribution and financial services)

· Investments worth US$13 million in 12 companies

· Over 4.9 billion beneficiaries

· 33,399 loans disbursed; 29 percent first time borrowers

· 1,596 houses and 7,800 toilets constructed

· 29,500 tons of waste collected; 386 waste pickers employed; over 50 percent increase in waste pickers’ annual income; 38 percent women waste pickers employed

· 150,000 farmers reached; 120,000 lakh small holder farmers impacted; US$100-million estimated increase in farmer net income; 750,000 acres of area covered

· 150,000 jobs supported through financial institutions assisting SMEs

· 528,000 farmers reached, 28 percent of which were women

· 167 agricultural partners; 42,000 people employed by them

· 69 partners are agricultural cooperatives, 58 are trade certified and 46 are organic certified

· Agricultural partners pay 19 percent above market price on average to their farmers

· 72,000 households and 13,000 businesses with access to clean energy; 178,000 tons of carbon emissions avoided

Resolving Challenges to India’s Impact Investment Ecosystem

Legal challenges faced by social enterprises

Social enterprises have not been defined as separate legal entities in India, which means they do not have a legal definition. This restricts social enterprises from realising their desired objectives. So vague is the articulation of a social enterprise that many cannot distinguish it from a non-governmental organisation (NGO). Social enterprises are burdened with greater compliance costs and difficulty in raising funds than NGOs.[62]

Impact investment funds and social enterprises have been accommodated within the domain of Alternative Investment Funds (AIFs) as Social Venture Funds and social ventures. These funds are “those established in India to pool capital from Indian and foreign investors for investing as per a pre-decided social impact policy.”[63]According to the AIF regulations, a social venture fund is defined as “an alternative investment fund which invests primarily in securities or units of social ventures and which satisfies social performance norms laid down by the fund and whose investors may agree to receive restricted or muted returns.” Social venture means a trust, society or company or venture capital undertaking or limited liability partnership formed to promote social welfare or solve social problems or providing social benefits and includes:[64]

Public charitable trusts registered with Charity Commissioner

Societies registered for charitable purposes or for the promotion of science, literature, or fine arts

A company registered under Section 25 of the Companies Act, 1956

Microfinance institutions

Social Venture Funds are subject to the following regulations:[65]

Mandated to have at least 75 percent of their investible funds invested in unlisted securities or partnership interest of ‘social ventures’

Allowed to accept grants so long as they are utilised as per the above regulation

Allowed to receive grants as long as the same is appropriately mentioned in the placement mechanism.

The AIF regulations, which govern India’s impact investment space, implicitly characterise such investment as a not-for-profit proposition. Except for venture capital undertakings and limited liability partnership, all other entities defined as social ventures are not-for-profits such as trusts, societies, section 25 company under the Companies Act 1956. The regulations appear to be misplaced in their understanding of impact investment.

The AIF regulations allegedly do not allow investors to accrue market-level returns, restricting them to accept muted or nil returns.[66]In reality, this clause is only permissive and does not in any way prohibit accrual of market returns.[67]This supposed restriction defeats the objective of impact investment, which seeks to mobilise capital across various risk-return preferences. While there may be individuals at the extremes— driven by pure self-interest and no concern for social good on one end and driven exclusively by pure philanthropy on the other—there may very well be people who occupy positions in between these extremes. There could be individuals who prioritise the market rate of returns above social good but prefer such returns along with some social gains rather than without them. Such misinterpretation crowds out investment preferences. The misplaced interpretation of the clause of muted returns may explain why domestic funds barely participate in the impact investment activity in the country. This could be one of the reasons why there is a lack of appropriate capital across the risk-return spectrum.

The trusts, societies and other entities that are defined as social ventures are not only governed by the AIF regulations but are also subject to other laws that often contradict the AIF regulations. For instance, while the AIF regulations appear to allow not-for-profits to issue returns, the entity-specific rules do not. Furthermore, the Foreign Contributions Regulation Act (FCRA) and the Income Tax Act (ITA) also contradict the AIF regulations. While the ITA allows for-profit organisations to receive foreign grants and donations, its provisions, as well as those of the FCRA, envision only not-for-profits receiving grants and donations. This has obscured the impact investment space with ambiguity.[68]As a result, social enterprises choose to become either not-for-profit entities or for-profit enterprises, and no organisation functions in the grey area of social ventures, as under the AIF. Existing social enterprises also do not access the allowances made under the AIF regulations. For instance, no for-profit firm seek to receive grants, although permitted under the AIF regulations. This has punctured the take-off of Social Venture Funds and the intermixing of capital, which is the core thesis of impact investments.[69]

Recommendations

There is a need to assign legal status in terms of revenue models, whether donation-based models or social business revenue models, with the latter being referred to as social enterprises. The three distinct models of social enterprises must be taken into consideration to develop a classification of various legal forms of social enterprises. Taking a cue from the AIF definition, a social enterprise may be defined as one formed with the purpose of promoting social welfare or solving social problems or providing social benefits, while satisfying certain social performance norms and which simultaneously generates a financial return. These performance norms need to understand the dynamics of different social sectors and how they operate. These dynamics need to be generalisable before one proceeds to create a standard set of performance norms that applies to a set of entities. It is essential to determine if the dynamics are generalisable across sectors or industries before choosing the collective for which a standard set of performance norms can be articulated. Also, what falls in the domain of the social sector needs to be demarcated clearly. A social issues framework, which identifies problems to be tackled and the solutions to be provided, needs to be developed across sectors. This is a formidable task that will require the collaboration of the government, the private sector, the social sector, the entrepreneurial class, lawyers and so on. The SDG framework is an appropriate benchmark for performance norms for social enterprises since they are engaged in contributing to these goals. All of the different laws governing different entities that qualify as social enterprises and the AIF regulations need to be harmonised to arrive at a unified legal protocol for the impact investment space.

The CSV proposition could be considered as the theoretical underpinnings for a social enterprise.

The formulation of a legal definition of social enterprises may borrow insights from other countries. However, a large number of countries do not have legal definitions for social enterprises.[70]Although the US does not have a legal definition of social enterprises, certain legal forms have been launched to allow social enterprises to operate seamlessly. Social purpose corporations and benefit corporations have been created to ensure transparency in the corporation’s commitment to the cause of the social mission and to protect the social enterprise from being penalised for upholding the social mandate above shareholder returns. Low-profit limited liability companies have been created to receive tax-exempt finance from private foundations.[71]

Although some countries do have legal definitions, the clauses of these definitions are not conducive to the growth of impact investments. For instance, although the UK, Italy and South Korea impose restrictions on the number of returns that can be distributed among the shareholders, the limits are well defined. In the UK and South Korea, no more than 50 percent and 33 percent, respectively, of the profit or surplus can be distributed among the owners or shareholders. In Italy, social enterprises cannot distribute earnings to owners and must invest it in the business or increasing assets.[72]India will have to strike a balance between shareholders’ returns and a financial commitment to the social mandate without depressing impact investments. Capping the profits going to shareholders goes against the CSV thesis. This thesis deserves to be put in practice to see whether its promises hold true. If they do, then there will be no need to cap the shareholder returns since the economic value will go hand in hand with social progress.

Also, by requiring that a large part of the turnover of the enterprise come from trading goods and services,[73]several early-stage enterprises, who may rely heavily on grants and donations, may not qualify as social enterprises. This defeats the purpose of intermixing of capital.

There are some positive aspects of the definition as well. No legal form is prescribed for social enterprises in the UK and Italy, while in South Korea, a social enterprise can assume a range of legal forms. Although no prescription of a legal way allows flexibility, the formulation of an entirely new legal way is also advisable with non-conflicting statutes governing the dynamics of a social enterprise. Even though the UK does not prescribe any legal form, it has created a special legal form called Community Interest Company for social enterprises.[74]The conflicting legal statutes can be avoided by following the UK’s example.

Further, the UK’s definition of social enterprise mandates the legal protection of assets of an enterprise for the permanent utilisation for the good of the community. Similarly, in Italy, if the social enterprise gets liquidated, the assets are to be distributed to non-profits, foundations and the like.[75]

Other Challenges faced by social enterprises

Lack of a standardised legal structure governing social enterprises

In the absence of a definite legal space and definition for a social enterprise, there is a lack of standardised legal structure governing social enterprises. This has entailed high costs in terms of, among other things, registration, compliance and seeking of approvals.[76]This implies higher transaction costs and the costs of doing business. This discourages potential entrepreneurs from taking up social businesses as well as investors from invest in such businesses.

Recommendation:Setting up of a single-window regulatory body

There is a need for a large-scale regulatory platform that is a one-stop-shop for compliance, registration, incorporation, and all forms of approval for social enterprises. This regulatory forum must be dedicated to providing services required by social enterprises only.

Recommendation:Self-regulation

Impact investments are at such a nascent stage that self-regulation is a better option in terms of monitoring performance. The harmonisation of performance standards will require some application of generalisation, which may be misguided at this juncture. There is a need to distinguish between performance norms at the level of defining social enterprises and those at the level of assessing their impact.

As far as measuring social impact is concerned, the Impact Investors Council can take it upon itself to bring together various stakeholders to deliberate upon standards and methods for social impact assessment. Such exercises must use the globally developed Impact Management Project, a five-point framework that demarcates the notion of “impact”[77]and metrics such as Impact Investment Reporting Standards as benchmarks.[78]Internal committees within organisations must be set up to assume responsibility for undertaking the measurement task and presenting the report in the public domain.

Lack of a sympathetic taxation system

The most significant advantage of registering as a not-for-profit is to be eligible for tax benefits under the Income Tax Act, 1961. This advantage is not available to those operating in the for-profit space. All income needs to be shown as sales, and there is no consideration of income that has gone to generating social outcomes. There is no distinction between for-profits with a social mission and those without such a purpose. Currently, both entities are being taxed in the same manner.[79]

Recommendation:Streamline taxation for social enterprises

For-profit social enterprises with a social mission complement the government’s efforts to redistribute wealth and maximise social welfare. That social enterprises are focused on achieving the SDGs is enough reason to consider tax exemptions and benefits for this class. While taxing income that is to be issued as dividends, the investor’s choices involving the philanthropic component must be rewarded by some sort of tax concession. This will attract more domestic investments in social enterprises and impact investment funds.

Unfavourable regulations around receiving philanthropic and foreign funds

While the not-for-profits cannot issue equity or debt, the for-profits find it difficult to receive grants or donations. Furthermore, the latter find it difficult to raise funds from CSR and foreign funds as well. No special recognition is given to the need and importance of such fundraising activity by for-profits. The idea of for-profits with a social mission has not really arrived in India yet. Charitable organisations that provide grants or donations to for-profit social enterprises are not eligible for tax deductions. Hence, such organisations are averse to doing so. It is exceedingly difficult to convince the authorities that for-profit social enterprises are set up for charitable purposes.[80]

The central bank’s approval is required to access foreign capital, for which an entity becomes eligible only after three years of existence. The FCRA places restrictions on access to grants and donations.[81]It requires any organisation in India to seek permission from the Ministry of Home Affairs to receive grants and donations from foreign sources.[82]

In the not-for-profit domain, investments or sales proceeds are treated as a ‘donation’, and the investor cannot attain a return on investment. There is no clarity on whether this has changed under the AIF’s muted returns clause.[83]

Recommendation:Allow tax breaks on grants/donations made to for-profit social enterprises, make for-profit enterprises eligible for CSR funds and relax foreign fund guidelines

New social enterprises generally experiment with innovative revenue and business models. The market for their goods and services is usually non-existent. As such, social enterprises find it difficult to generate substantial profits and consequently to lure investors into financing risky early-stage operations. A grant becomes essential to showcase the profitability of a new business model or provide it time to develop a profitable strategy.[84]This has been proven in case of many microfinance institutions, which, riding on grants, have evolved into profitable banks. For instance, SKS Microfinance in India, Equity Bank in Kenya, and Compartamos Banco in Mexico.[85]Furthermore, once the definition of social enterprise and the related notions are well-articulated, irrespective of their revenue model, there is a need to make them eligible to receive CSR funds. Also, the restrictions on foreign funds need to be relaxed for the case of social enterprises.

Equity is the dominant investment instrument for impact investment

Debt is relatively expensive for early-stage and growth enterprises, in the absence of sufficient collateral and because the debtor is charged as much as a 25 percent rate of interest due to the prevalent regulatory regime.[86]As a result, several small firms that have the ability to become sustainable and scalable are starved for funds.[87]

Recommendation:Rationalisation of interest rates on debt instruments

The rules and regulations governing investments in social enterprises must be determined by the proposed new regulatory body, which needs to study the circumstances and realities of the sector before formulating such rules. If appropriate mobilisation techniques are used in consultation with experts to appeal to the philanthropic side of investors, impact investors who are willing to make high-risk low returns investments will be found on the continuum of risk-return preferences. In such cases, debt can be acquired at cheaper rates.

Lack of capital across the risk-return spectrum

Higher levels of impact investment have gone into those sectors that yield higher rates of return (See Table 2). While this may be interpreted as impact investment catering to those who prioritise financial returns but also care about social performance, evidence suggests that mainstream investors are being attracted to make investments into early and growth stage venture firms as well. Given that a large number of social enterprises self-identify as regular or mainstream enterprises, it appears that mainstream investors are interested in such enterprises for the profit motive and not the social impact motive.[88]There is evidence that India has failed to garner resources earmarked for charity into social enterprises. The impact investment thesis will be actualised when investors who are willing to bear high risk for low returns are also mobilised.

Recommendation:Create awareness about impact investment and social enterprises

This challenge also includes the lack of a standardised legal structure and a sympathetic tax system for social enterprises. Due to the lack of a separate legal identity and a standardised legal structure, the notion of social enterprises is not as well-known as much as it should be to mobilise capital across the entire risk-return spectrum. The nuanced study of social businesses and their models must be made part of the educational syllabus of postgraduate courses in business management, social work and allied fields. Social enterprises must run internship programmes that are endorsed by educational institutions. The government can collaborate with these social enterprises to provide large-scale advertising services at no or little cost to ease the burden on early- and growth-stage companies. Once the business becomes sustainable, the government can claim an advertising fee from the enterprises. The government must also create greater awareness and sensitise those interested in impact investments by articulating the dynamics of the space in a simplified manner, from registration norms to taxation protocol and monitoring mechanisms.

Lack of suitable exit options

One of the parameters of success for the impact investment sector is the ability to yield returns via fruitful exits. But since impact investing in India in a relatively nascent stage and there is considerable flux around the sector, it is no wonder that there is a lack of suitable exit options. The consequent lack of liquidity can adversely affect the prospects of impact investment in the country.

Recommendation:Setting up of the Social Stock Exchange

In the 2019 Budget speech, Finance Minister Nirmala Sitharaman announced the launch of a Social Stock Exchange (SSE), a platform for social enterprises to raise funds through equity, debt and mutual funds.[89]But the SSE is yet to be established. Once set up, it will allow social enterprises to acquire greater liquidity by getting listed on the stock exchange and issuing initial public offerings, allowing for profitable exits. The process of establishing an SSE in India must be expedited, and the platform must utilise a screening process to determine which enterprises are eligible to get listed and enjoy its benefits. `

Conclusion

The 2019 iteration of NITI Aayog’s SDG India Index suggests that although there has been progress in achieving the SDGs, there is great scope for improvement and, as a result, space for social enterprises to contribute. India’s score rose marginally from 57 in 2018 to 60 in 2019, through progress made in sectors like clean water and sanitation (88); peace, justice and strong institutions (72); and affordable and clean energy (70). The country still has a long way to go from achieving these goals.[90]

India registered its worst performance on the goals of zero hunger (35) and gender equality (42). Progress on achieving zero hunger (SDG 1), sustainable cities and communities (SDG 11), and sustainable consumption and production (SDG 12) lags behind the desired outcomes.[91]

The performance of states points towards unbalanced regional development. Kerala ranked first among all states in the overall assessment. Himachal Pradesh, Sikkim and the other southern states scored more than 65 out of a possible 100. Bihar was last, with Jharkhand and Arunachal Pradesh rounding out the bottom position. Among union territories, Chandigarh occupied the top spot, with a score at par with Kerala.[92]

The performance varies across regions and across goals. For instance, on zero hunger, Kerala, Goa, Mizoram, Nagaland, Arunachal Pradesh, and Sikkim scored above 65 points. Twenty-two states and union territories scored below 50. What is worse, Jharkhand, Madhya Pradesh, Bihar and Chhattisgarh scored below 30, throwing light on heightened starvation and malnutrition in these states. On gender equality, almost all states registered a dismal performance, with only Jammu and Kashmir, Himachal Pradesh and Kerala achieving a score greater than 50.[93]

These rankings highlight the immense role that social enterprises and impact investment can play in India’s balanced regional and sustainable development story. Relying completely on the government sector will put too much pressure on the state machinery on achieving the SDGs by 2030. The government must consider providing impetus to the impact investment endeavour in the country as a quick-win alternative. All of the potential solutions to the problems facing the impact investment sector in India require effective decision-making by the government. This will enable the country’s impact investment sector and social enterprises to play a complementary role to that of the government in reaching the SDG milestones and achieving balanced regional development.

Endnotes

[a]Although impact investments can be traced back to biblical times, it received impetus post the 2007-08 financial crisis. Impact investments originated in the US and UK since these nations are home to affluent societies that have access to philanthropic choices.

[1]NeerajHatekar, Savita Kulkarni and Renita D’Souza,Experimental Investigation of Pro-Social Preferences, Working paper no. UDE 40/03/2012.(Department of Economics, University of Mumbai, 2012)

[2]China Social Impact Investment Report 2016, China Development Research Foundation.

[3]The promise of impact investment,(International Finance Corporation, 2019),

[4]Ibid.

[5]Ibid.

[6]Georgette Fernandez Laris, “Philosophical Foundations of Impact Investing”, sevenpillarsinstitute.org, 30 September 2017.

[7]Jing Zhou, “The Development of Impact Investing and Implications for China”, (Master’s diss., MIT, 2017).

[8]Manuel Stagars,Impact investment funds for frontier markets in Southeast Asia: Creating a platform for institutional capital, high-quality foreign direct investment, and proactive policy making(Springer, 2015)

[9]Ibid.

[10]Ibid.

[11]Ibid.

[12]Ibid.

[13]Georgette Fernandez Laris, op.cit.

[14]Ibid.

[15] Michael E. Porter and Mark R. Kramer, “Creating Shared Value”, Harvard Business Review, January -February 2011.

[16]Ibid.

[17]Ibid.

[18]Ibid.

[19]Ibid.

[20]Ibid.

[21]Ibid.

[22]Stagars, op.cit;The Four Lenses Strategic Framework: Towards an integrated social enterprise methodology, the website of 4lenses.org.

[23]The Four Lenses Strategic Framework: Towards an integrated social enterprise methodology, the website of 4lenses.org.

[24]The Four Lenses Strategic Framework: Towards an integrated social enterprise methodology, the website of 4lenses.org.

[25]The Four Lenses Strategic Framework: Towards an integrated social enterprise methodology, the website of 4lenses.org.

[26]The Four Lenses Strategic Framework: Towards an integrated social enterprise methodology, the website of 4lenses.org.

[27]Stagars, op.cit;The Four Lenses Strategic Framework: Towards an integrated social enterprise methodology, the website of 4lenses.org.

[28]The Four Lenses Strategic Framework: Towards an integrated social enterprise methodology, the website of 4lenses.org.

[29]Stagars, op.cit;The Four Lenses Strategic Framework: Towards an integrated social enterprise methodology, the website of 4lenses.org.

[30]Ibid.

[31]John Kuo, “Do Behavioral Finance and Impact Investment make good bedfellows?” nerdwallet.com.

[32]Matthew Lee, Arzi Adbi and Jasjit Singh, “Outcome Efficiency in Impact Investing Decisions”, INSEAD Working paper series 2018/32/STR, July 2018.

[33]Ibid.

[34]Ibid.

[35]Ibid.

[36]Ibid.

[37]Ibid.

[38]Ibid.

[39]Ibid.

[40]Ibid.

[41]Ibid.

[42]Ibid.

[43]Impact Base Data.

[44]Ibid.

[45]Saahil Kejriwal,Impact Investing, the website of India Development Review, 25 September 2019.

[46]

[47]Ibid.

[48]Ibid.

[49]Ibid.

[50]Shamika Ravi, Emily Gustafsson-Wright, Prerna Sharma, and Izzy Boggild-Jones,The Promise of Impact Investing in India.(Brookings Institution, 2019).

[51]Ibid.

[52]Ibid.

[53]Ibid.

[54] N. Dutt, U. Ganesh, P. Chandrasekaran, P. Agarwal, S. Patil, and A. Gupta,Invest catalyze mainstream: The India impact investing story. (Mumbai: Intellecap, 2013).

[55]Ibid.

[56]Shamika Ravi, Emily Gustafsson-Wright, Prerna Sharma, and Izzy Boggild-Jones, op.cit.

[57]Ibid.

[58]Aavishkaar group’s Impact Report 2018.

[59]Asha Impact Annual Report 2019.

[60] Caspian Impact Investments Social Performance Report 2018-19.

[61]The Oiko Credit Impact Report 2019.

[62]Should Social Enterprises Be Regulated By New And Separate Laws?The website of Centre for Advancement of Philanthropy, 2 November 2016.

[63]Meyyappan Nagappan, Rahul Rishi and Anuja Maniar,Impact Investing Simplified: A Guide to Making and Receiving Impact Investments in India(Nishith Desai Associates, 2019).

[64]Ibid.

[65]Ibid.

[66]Unstructured Interview with Ranjna Khanna, Director, Impact Investors Council

[67]Unstructured Interview with Meyyappan Nagappan, Nishith Desai Associates

[68]Ibid.

[69]Unstructured Interview with Ranjna Khanna, Director, Impact Investors Council

[70]Emily Darko,Social Enterprise Policy Landscape in Bangladesh(British Council, 2015); Jessica Sandford, Liu Yi, Cecile Mazourine, Magali Menanta and Katja Hellkoetter,Social Enterprise in China,(Constellations International, 2015), Tamako Watanabe,Study of Social Entrepreneurship and Innovation Ecosystems in South East and East Asian Countries: Country Analysis-Japan, ( The Japanese Research Institute, 2016)¸

[71]Anna Triponel and Natalia Agapitova,Legal Frameworks for Social Enterprise: Lessons from Comparative Study of Italy, Malaysia, South Korea, United Kingdom and United States, The World Bank.

[72]Ibid.

[73]Ibid.

[74]Ibid.

[75]Ibid.

[76]Should Social Enterprises Be RegulatedBy New And Separate Laws? The website of Centre for Advancement of Philanthropy, 2 November 2016.

The views expressed above belong to the author(s). ORF research and analyses now available on Telegram! Click here to access our curated content — blogs, longforms and interviews.

Renita DSouza is a PhD in Economics and was a Fellow at Observer Research Foundation Mumbai under the Inclusive Growth and SDGs programme. Her research ...

PDF Download

PDF Download