This is the 135th article in the series–The China Chronicles.

This is the 135th article in the series–The China Chronicles.

The Biden administration on August 25 this year issued an

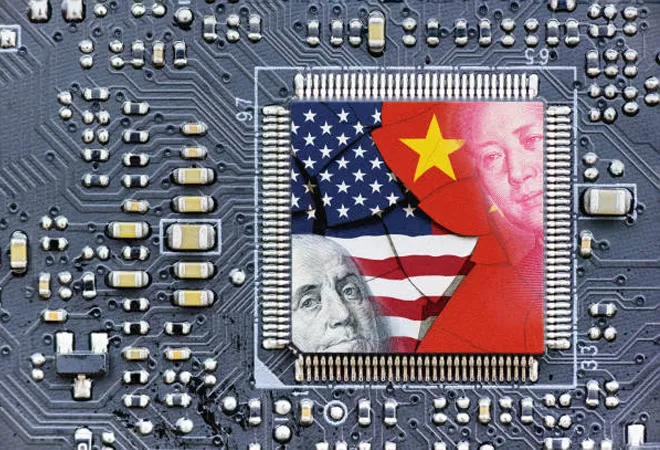

Executive Order on the implementation of the Chips Act of 2022, unleashing a slew of export control measures which are reckoned to impact the Chinese semiconductor industry in unprecedented ways. Most conspicuously, the decision will stop supply of high-end semiconductor chips to China; halt China’s ability to get machines which manufacture chips globally; and stop US citizens (including Green Card holders) from working for a Chinese semiconductor company or provide support and knowhow to them. This step by the US government firmly establishes Washington’s decision to decouple from China, especially in the technology sector. Strategically, the US seeks to obtain two main objectives—slowing China’s technology-related advances and containing China’s economic and military ambitions.

The Biden administration has doubled down on competition with China, resulting in a four-fold increase in Chinese companies in the Entity List from 130 in 2018 to 532 as of March 2022.

The Biden administration has taken a serious view of the long-term threats in the tech sector from China. The use of export controls to blunt China’s competitiveness in the technology sector has been consistently employed by the US administration and has

grown since 2017. These restrictions have affected the exchange of technology across various sectors between China and the US. The Bureau of Industry and Security (BIS), U.S. Department of Commerce is at the heart of this tech shift in US policy. The US Entity List brought out by the BIS, which contains names of individuals, companies, businesses and institutions which require specific license for the ‘

export, reexport and/or transfer (in-country) of specified items’ has considerably expanded in the last five years. The Trump administration’s trade war with China had already seen many new names being added to the Entity List. Notably, the Biden administration has doubled down on competition with China, resulting in a four-fold

increase in Chinese companies in the Entity List from 130 in 2018 to 532 as of March 2022. Most of the prominent Chinese companies related directly or indirectly to the chip and semiconductor industry have been put on the US Entity List. Importantly, the BIS has also

added some important companies to the list even though they deal with non-sensitive product manufacturing, making any circumvention to export controls by China extremely difficult.

Apart from the expanded list, the latest export control measures by the US are punitive, as opposed to being just restrictive earlier. What makes the latest round of export control restrictions by the US extraordinary is the extension of the ‘

foreign direct product rule’ to almost all Chinese companies in the semiconductor, supercomputing, quantum computing and related fields, making it almost impossible for Chinese companies to avail technology imports from other leading global companies in the field. The foreign direct product rule

stipulates that manufacturing outside the US, which makes direct use of US software or technology, may be subject to US re-export control laws under the Export Administration Regulations (EAR) as ‘foreign-direct products’.

The impact of this great tech-decoupling between China and the US is expected to be felt in China across a range of sectors for two main reasons: First, Chips are China’s

biggest import at close to US $400 billion, even more than crude oil. As such, the export control restrictions will force China to look inward for filling the gap in the chip industry and related technological sectors that are dependent on these imports. However, any prospect of developing such capabilities commensurate with the gigantic domestic demand in the short term remains remote. Second, behind China’s massive import of semiconductors underlies the interconnectedness of these imports with other related sectors, which has scripted China’s phenomenal advances in technology in the past decade. As a result of the export control implementation, the use of Artificial Intelligence (AI) and automation is expected to slow down in China. It is

assessed that other sectors that are going to be impacted as a result of the latest US export control measures include research and development in the drug industry, cybersecurity, medical imaging, advances in climate science, autonomous vehicles, hypersonic weapons, and supply chain automation, among other fields.

The export control restrictions will force China to look inward for filling the gap in the chip industry and related technological sectors that are dependent on these imports.

The US-China competition is, perhaps, at the peak of a cycle involving measures and countermeasures in the tech-security interface. China has so far shown a muted response to the Biden administration’s export control salvo. However, a calculated Chinese strategy to tackle the incoming technological crisis should be anticipated. China could use a combination of external influence and domestic capacity building capacity building to in its attempt to overcome the crisis. The US is expected to work with its other partners to sustain its global leadership in the semiconductor industry and increase the tech-gap with China.

What US export control measures mean for other players

How will the current set of export control measures sit with the US’s other partners globally and in the Indo-Pacific? Amidst this lingering question, it will be critical for the US to forge a grand semiconductor consensus along with the Netherlands and Japan—the three countries which together

produce 90 percent of global semiconductor manufacturing equipment. It will also be important to see how the US negotiates the necessary operational space for its new restrictions with other Indo-Pacific partners, including its closest allies in the Chip 4 group – Japan, South Korea, and Taiwan. Already, the US has

struggled to mobilise its Chip 4 alliance. Beyond its partners in the Chip 4 group, the US may have to work with other partners in the Indo-Pacific to harmonise regional tech policies in the future.

For many in the Beltway, US’s policy towards China has divided the engagers (those who want to keep China engaged) and restrictionists (those who want to accelerate decoupling with China) in the Biden Administration. With the implementation of the Chips Act, the Biden government clearly seems to have lurched away towards the restrictionists’ side. Politically, the approaching midterm elections in the US has also played as a suitable backdrop for the political move against China. President Biden has also pandered to the broader political consensus against China in the US, both inside and outside the Congress.

With little or no external options and on the back of the just concluded 20th National Congress of the Chinese Communist Party, Xi Jinping may well give a national call linking the necessity to build a strong domestic semiconductor industry with the ‘great rejuvenation’ of the Chinese nation.

Finally, the move by the US to enforce the harshest export control measures on China has its own set of risks, including ushering an unprecedented momentum inside China in its semiconductor industry. With little or no external options and on the back of the just concluded 20

th National Congress of the Chinese Communist Party, Xi Jinping may well give a national call linking the necessity to build a strong domestic semiconductor industry with the ‘great rejuvenation’ of the Chinese nation. The emerging Chinese discourse is already

playing at the phrase “

ke jiao xing guo” (“to invigorate the country through science and education”)—emphasising its status as a country underpinned by technology, science, and education. China’s narrowing options in external technological imports could very well be its inflection point to invoke a reinforced techno-nationalism at home.

The views expressed above belong to the author(s). ORF research and analyses now available on Telegram! Click here to access our curated content — blogs, longforms and interviews.