-

CENTRES

Progammes & Centres

Location

India’s population is 26 times larger than that of South Korea, but its economy—valued at US$2.7 trillion (as of 2020)—is less than twice South Korea’s—valued at just over US$1.6 trillion (as of 2018).<1> South Korea’s per-capita income is US$31,000, 15 times that of India. However, despite the enormous economic gap, the two countries share some attributes in the energy sector.

South Korea and India are heavily dependent on fossil fuels, i.e. coal, oil and natural gas, which poses a critical challenge to their efforts to decarbonise their energy systems. Simultaneous reduction of urban pollution at the local level and greenhouse gas (GHG) emissions at the global level are urgent challenges that both countries face. This involves balancing short-term economic costs of reducing GHG emissions (e.g. the cost of new technologies) with long-term benefits, such as the stimulation of the economy and better health outcomes. Both South Korea and India are heavily dependent on imports to meet their energy demand, which exposes them to the vagaries of geopolitics and geo- economics. They have also invested heavily in nuclear energy to diversify their energy baskets, but this has meant grappling with the inherent contradictions of nuclear power.

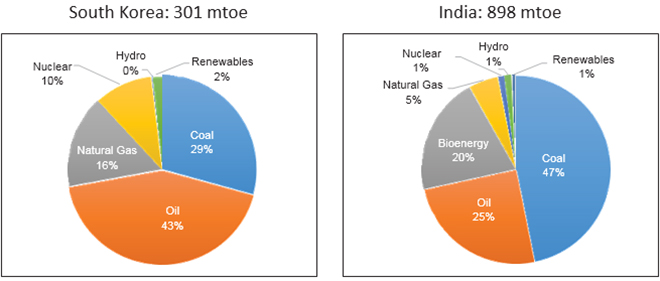

In 2016, 83 percent of South Korea’s primary energy was derived from fossil fuels (coal, oil and natural gas); the proportion was 75 percent for India.<2> India is relatively less dependent on fossil fuels because unprocessed biomass (firewood and dried animal dung) that accounts for 22 percent of energy consumption is used for cooking in poor rural households. However, if biomass that is not commercially traded on a national scale is excluded, the share of fossil fuels in India’s commercial energy basket<3> is a staggering 95 percent (See Figure 1).<4>

Over 95 percent of South Korea’s energy is imported as the country has poor resource endowments for coal, oil and gas.<5> India’s abundant coal reserves give it a lower import share of 34 percent, but for crude oil—associated with critical economic and geopolitical risks—the share of imports is 84 percent.<6>

South Korea and India share geopolitical risks in importing oil, which includes a volume-risk component and a price-risk component.

Figures 1a and 1b. Primary Energy Consumption by Fuel Share 2018

Source: BP Statistical Review of World Energy 2019; for India, the figure for biomass is taken from the World Energy

Source: BP Statistical Review of World Energy 2019; for India, the figure for biomass is taken from the World Energy

The volume risk component arises from supply disruptions caused by conflict in oil producing countries or on account of US sanctions on them. Such disruptions can upset long-term contractsfor oil supply by South Korea and India, which would, in turn, require changes in prices as well as refinery output. The price-risk component arises from the volatility in crude oil prices and its impact on the domestic economy and on external trade. The Indian economy is more exposed to both dimensions of oil- price risk due to the country’s “twin deficit” problem.<7> High crude prices push up the fiscal deficit of India’s domestic budget and increase the cost of subsiding the consumption of certain oil-derived products. It also increases the magnitude of India’s trade deficit with the rest of the world.

In 2017, coal accounted for 40 percent of South Korea’s electricity and 74 percent of India’s.<8> The use of coal for power generation is a challenge in the context of meeting goals set in the nationally determined contributions (NDCs) to the Paris Agreement. According to the international energy agency (IEA), carbon dioxide (CO2) emitted from coal combustion was responsible for over 0.3°C of the 1°C increase in global average annual surface temperatures above pre-industrial levels.<9> Activist organisations that oppose investments in fossil fuels are likely to leverage this observation, to portray South Korea and India as climate-change offenders. Within the framework of climate change, multilateral obligations can also create pressure on the two nations to accelerate the phasing out of coal use. This will necessarily mean an increase in short-term economic, social and political costs for both countries.

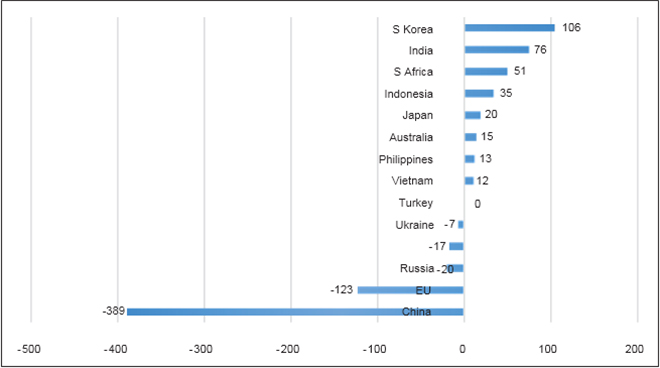

A recent report by the “Carbon Tracker Initiative,” a non-governmental agency opposing the use of fossil fuels, concludes that South Korea has the highest stranded asset risk of US$106 billion from existing and future coal- based power plants amongst the 34 countries modelled. India comes second, with a stranded asset risk of $76 billion (See Figure 2).<11>

Figure 2. Stranded Asset Risk in US$ Billion

Source: Matt Gray and Durand D’souza, 2019.

Source: Matt Gray and Durand D’souza, 2019.

These narratives present South Korea and India in poor light, coercing them to reconfigure their energy baskets. However, such measures would alter the global economic competitiveness of both countries. For South Korea, especially, this is a huge risk since it is a highly industrialised export-oriented economy.

South Korea’s NDCs include a target of reducing GHG emissions, excluding land use, land-use change and forestry (LULUCF). By 2030, the country aims to reduce emissions by 37 percent below “business as usual” (BAU) emissions (or 18 percent below the 2010 level), and increase the share of renewable energy to 20 percent.11

As part of its NDCs, India aims, by 2030, to reduce the emissions intensity of its gross domestic product (GDP) by 33–35 percent compared to the 2005 level; achieve 40 percent cumulative installed capacity for electric power generation from non-fossil fuel energy, through transfer of technology and low-cost international finance, including support from the Green Climate Fund (GCF); and create an additional carbon sink of 2.5–3 billion tonnes of<12> CO2 equivalent through additional forest and tree cover.

The NDC commitments of South Korea and India are likely to help decarbonise the global energy system. However, organisations that rate and track country- wise NDCs describe them as not “sufficiently ambitious” to limit the global average temperature increase to 1.5°C. For example, the “Climate Action Tracker” observes that more stringent policies would be required to meet even the “weak” target in South Korea’s NDC.<13>

While the agency is more favourable towards India, it is critical of the country’s plans to build coal-based power plants.<14> Both South Korea and India have been accused of continuing with the use of coal for power generation, despite the availability of what the agency suggests are “cheaper” renewable energy options.<15> Under the framework of the NDC commitments, countries that are dependent on coal are singled out as climate offenders. This narrative not only oversimplifies the complexity of reducing carbon emissions, but also ignores the economic and social cost of implementing the relevant policies.

Currently available empirical studies from South Korea show that introducing low-carbon technological solutions will mean significant economic costs. For example, under a BAU scenario projected by the Korea Energy Economics Institute (KEEI) in 2016, even by 2050, fossil fuels will continue to account for over 81 percent of South Korea’s primary energy demand. The relative shares of oil, gas and coal will increase only marginally, compared to 2014.<16>

By 2050, fossil fuels will account for 49 percent and 45 percent of the primary energy supply, under the “Moderate Transition Scenario” and the “Advanced Transition Scenario,” respectively. Under the “Visionary Transition Scenario” (VTS), both fossil fuels and import dependence can be eliminated from South Korea’s energy supply. However, “job creation”—a parameter that may be considered a proxy for economic growth—is lowest under the VTS, as overall energy consumption reduces.

A study on reducing urban air pollutants, e.g. particulate matter < 2.5 micro-meter (PM2.5) and GHGs, concludes that the effort could cost 0.34–1.75 percent of South Korea’s GDP and impose asymmetric damage on emission- intensive industries such as primary metals, chemicals and transportation, with outputs from these sectors falling by 2 to 30 percent.<17> For an industrial economy such as South Korea, the implication of this is uncertain. However, the experience of Germany, a frontrunner in implementing low-carbon energy policies, offers some clues.<18> Germany, along with other countries in the European Union (EU), has high household electricity tariff account of levies, which have been included to finance the cost of renewable energy.<19>

The much-acclaimed EU market for carbon does not apply to emissions from transport, industry and buildings that are energy- and emission-intensive, to sustain the industrial competitiveness of EU economies.<20> Moreover, Germany faces protests against the phasing out of lignite (the dirtiest form of coal), by workers employed in its lignite industry. Studies have found that Germany’s continued use of lignite will compromise its climate goals for 2030.<21> South Korea’s own experiment with green growth, briefly discussed in a latter section of this article, highlights similar challenges.

In the case of India, projections by the Planning Commission (renamed NITI Aayog in 2014) estimate the cumulative cost of “inclusive” low-carbon growth (increase access to energy for poor households) to be about US$834 billion (in 2011 prices) between 2011 and 2030. The loss in economic output in the same period is projected to be about US$1.3 trillion.<22> The low-carbon growth scenarios envisaged by the Planning Commission results in an overall increase in CO2 emissions on account of increase in energy consumption, but the analysis foresees a reduction in CO2 emission intensity (CO2 emission per unit GDP).

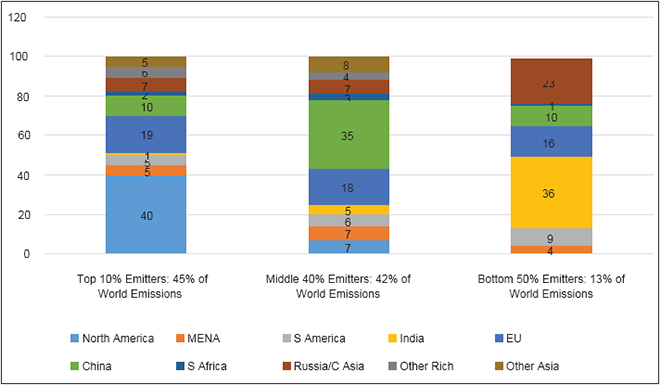

Inequality in access to energy and, consequently, inequality in CO2 emissions further raise serious distributional questions regarding the implementation of low-carbon policies. Only one percent of the global top 10 percent of CO2 emitters and five percent of the top 10 percent CO2 emitters—who account for<23> 45 percent and 42 percent of CO2 emissions globally—are in India. However, 36 percent of the bottom 50 percent of CO2 emitters (with emissions lower than world average), who account for the remaining 13 percent of emissions, are in India. This is the largest share of low CO2 emitters from any country in the world.

These low emitters are part of the energy-poor of the world, with marginal or no access to basic energy services such as lighting for electricity. Distributing the cost of decarbonisation amongst the poor (“socialisation of costs of decarbonisation”) who have not contributed to CO2 emissions raises serious questions over equity. This points to the political complexity of decarbonising economies at the cost of distributional equity. The case of the “gilets jaunes” (yellow vests) protests in France illustrates this complexity.<24>

To mediate this conflict between the pursuit of distributional equity and that of environmental security, many development funding agencies have promoted decentralised solar-energy solutions, which can provide access to<25> modern lighting without increasing the CO2 emissions in India. However, despite the efforts of these often well-funded programmes, the grid (coal)-based electrification programme of successive federal and state governments in India have been more successful in increasing electricity access to rural India than the decentralised solar solutions.<26>

Studies in villages that have been electrified with decentralised solar systems have demonstrated an unambiguous preference for grid-based power because of lower tariff, higher quality of service (availability of higher-quality lighting for longer periods) and lower demand for their time and intervention (lower transaction costs).<27> Even wealthier electricity consumers in California, who routinely signal a strong commitment to reducing their carbon footprint, have reportedly turned to petrol (gasoline)-based standby and portable generators during power outages caused by wildfires.<28>

Figure 3. Distribution of Global Carbon Emitters

Source: Iddri Lucas Chancel and Thomas Piketty, 2015.

Source: Iddri Lucas Chancel and Thomas Piketty, 2015.

Thus, the behavioural choices of both the affluent in California and the poor in India are based on economic self-interest rather than national/global climate-change considerations. Are consumers hiding their true preference behind the so-called political inertia? This is a critical policymaking challenge, especially for South Korea and India. Can the governments in these countries be blamed for inaction (or slow action/lack of political will) when consumers signal a preference for the status quo? Can the South Korean government choose decarbonisation over economic competitiveness and the Indian government socialise economic costs of decarbonisation amongst the poor? Sectors such as telecommunications and information technology have clearly demonstrated that when consumers shift to alternatives (albeit due to self- interest, i.e. lower costs and higher convenience and utility), government policy has little choice but to follow.

South Korea’s experiment with “green growth” offers useful insights on the complexities of decarbonising the energy system of a country. Following a decade of slow growth, shrinking middle class and growing income inequality, South Korea embraced the idea of green growth in the late 2000s, to invigorate its economy.<29>

The 2010 Seoul G-20 Summit, where the concept of green growth was first introduced formally, knowledge and innovation in clean, low-carbon technologies were promoted to accelerate growth, create new competencies and stimulate job creation, without compromising on the environment.<30> Under the green growth initiative, aggressive targets were set for 2030—of reducing energy intensity, the share of nuclear energy, oil dependence and energy poverty; while increasing the share of renewable energy and green jobs.<31>

However, an analysis of the trajectory of green growth policy outcomes in 2016 showed a departure from the trajectory required to achieve these goals.<32> Despite substantial investment in the sectors selected for green growth, compared to the levels in 2006, only marginal improvements were achieved in areas such as energy intensity, utility-scale solar photovoltaic (PV), the share of low carbon renewables, oil dependency and green jobs. Moreover, energy poverty rates increased from about seven percent in 2006 to about 10 percent in 2016.

The reasons identified by empirical studies for the failure of South Korea’s “green growth” initiative include: (1) the “more is better” ideology on energy consumption; and (2) the technological optimism of large-scale systems managed by experts. The first reason raises a much larger question regarding capitalism as the guiding philosophy of the global economic system, which is beyond the scope of this paper. The second reason is discussed in the following sections.

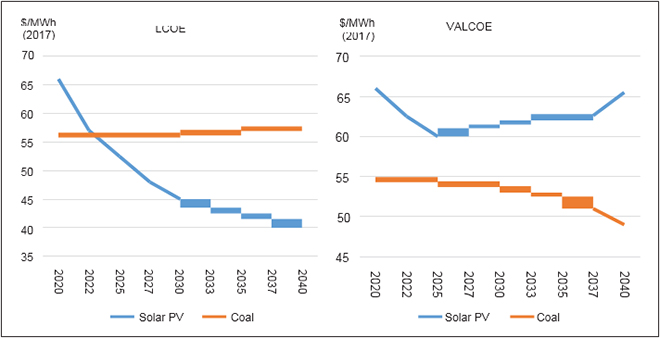

The Government of India has set a target of 175 GW renewable power installed capacity by the end of 2022.<33> This includes 60 GW from wind power, 100 GW from solar power, 10 GW from biomass power, and 5 GW from small hydro-power. The targets are routinely revised upwards by political leaders.<34> This is based on the premise that the cost of renewable energy is lower than that of conventional energy, even when health benefits of the former are not monetised, along with technological optimism over an exponential decline in the costs of renewable energy in the future.<35> The IEA has stated that the cost of electricity generated by solar energy is not necessarily lower than that of the electricity generated from fossil fuels at the system level for uninterrupted supply of electricity.<36> It also estimates that the costs of integrating intermittent energy is likely to increase with higher shares for renewable energy.

Figure 4. Solar PV Levelised Cost of Electricity vs. Value-Adjusted Cost of Electricity

Source: IEA, 2018

Source: IEA, 2018

According to the IEA, the value-adjusted levelised cost of electricity (VALCOE), which takes into account the cost of managing intermittency and unpredictability of solar and wind energy, is still well above the cost of coal-based power generation (existing and planned). This is true in India as well, where the balance of system (BOS) costs of solar projects (excluding the cost of solar panels) is low due to low labour costs.<37> While the estimation of renewable-energy integration<38> costs vary, according to one of the most authoritative papers on this subject, integration costs (costs that do not occur at the plant level but at the system level) are quite high, in the range of 35–50 percent of generation costs at 30–40 percent renewable energy penetration levels.<39>

This is an important observation for South Korea and India. The dominant (popular) technologically optimistic narratives narrowly focus on shifts at the supply end—where low-intensity energy sources (e.g. solar energy) replace high-intensity energy sources (e.g. fossil fuels), ignoring the need for spatial, temporal, economic and individual behavioural changes that are required at the demand end.<40> Technological substitution of high-carbon fossil fuels with low-carbon renewables at the supply end that ignore changes required at the demand end is likely to fail. Technological optimism is again invoked in the ability of smart grids, smart devices and the blockchain to mediate and substitute the complex social, temporal and behavioural changes required. Can South Korea and India afford to make substantial investments based on technological optimism? Or should they instead take technology-agnostic policy paths towards decarbonisation?

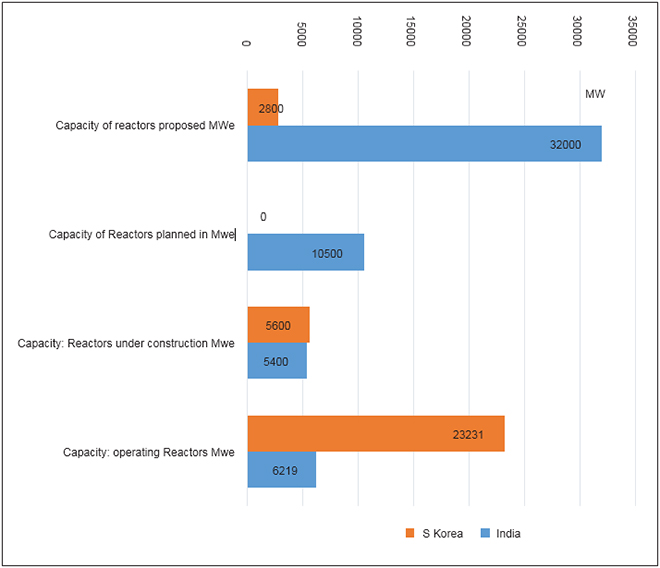

South Korea is amongst the prominent users of nuclear energy and a key exporter of nuclear technology. Nuclear power generated from 24 reactors, with a total capacity of about 23 GW, meet about 23 percent of South Korea’s electricity needs.<41> South Korea exports its nuclear technology widely and is currently involved in the building of four reactors in the UAE, under a US$20- billion contract.<42> India’s nuclear energy generation capacity is much smaller in comparison, with 22 reactors of total capacity 6,219 MW that meet only about three percent of the country’s electricity needs.<43>

After the nuclear accident in Japan in 2011, the South Korean public expressed concerns regarding the safety of nuclear plants. In response, the South Korean Government decided to phase out nuclear energy. In India, too, there is anxiety amongst those living in the vicinity of nuclear plants. However, the Government of India is pressing ahead with plans to expand its nuclear power generation capacity. Despite government-led push, the pace of progress in nuclear-energy capacity addition in India has been slow. In this context, the key question for both South Korea and India is whether the two countries can afford to limit the role of nuclear energy in decarbonising their energy systems.

In 2018, the combustion of fossil fuels emitted 33.7 billion tonnes (bt) of CO2. To reduce those emissions to zero, about 12 billion tonnes of oil equivalent (btoe) of energy needs to be replaced. To reduce emissions to zero by 2050, about 1.6 million tonnes of oil equivalent (mtoe) of zero carbon energy must be deployed every day for the next three decades (to meet current and future increase in energy demands).<44>

This would require either the building of a nuclear plant of about 1,600 MWe capacity every two days for the next three decades or putting up wind turbines of 2,500 MW capacity every day for the next three decades. Apart from the technological and financial complexities of making these investments, there is the question of whether adequate land will be available for the wind energy option, which would also require space for arrays of batteries. Between the two, the nuclear option is more effective in terms of energy generation, affordability and resource use (land in particular).

Figure 5. Nuclear Capacity in South Korea and India

Source: World Nuclear Association.

Source: World Nuclear Association.

South Korea and India can explore opportunities presented by small modular reactors (SMR) to meet the growing demand for decarbonised, safe and competitive electricity generation, leveraging years of nuclear experience in both countries. South Korea has recently signed an agreement with Saudi Arabia to work together on the commercialisation of the Korean SMART SMR design.<45> South Korea and Saudi Arabia are also planning a joint nuclear energy research centre. If the former successfully implements SMR contracts with the latter, it can convince its own citizens that such reactors are safe and affordable. For India, the challenges include not only safety concerns, but also questions regarding additional nuclear-capacity creation when there is already surplus capacity in coal-based generation and plans for over 400 GW of renewable energy capacity. Apprehensions about the liability of nuclear technology suppliers also inhibit investment, which is an impediment to attracting foreign investment in the sector. SMR technology can simultaneously address Indian concerns over economic, environmental and safety issues. Moreover, it can substantially reduce investors’ concern over liability.

According to the IEA, the use of energy for space cooling is growing faster than any other form of energy use in buildings, having tripled between 1990 and 2016.<46> Since 1990, the sale of air conditioners (ACs) has quadrupled to 135 million units. ACs consume over 2,000 Terawatt hours (TWh) of electricity every year, which is 2.5 times the total electricity use of Africa. CO2 emission from cooling has tripled since 1990 to 1,130 million tonnes (Mt), equivalent to the total emissions of Japan.<47> According to estimates, a 1°C increase in temperature in the future will increase electricity consumption for cooling by around 15 percent.<48>

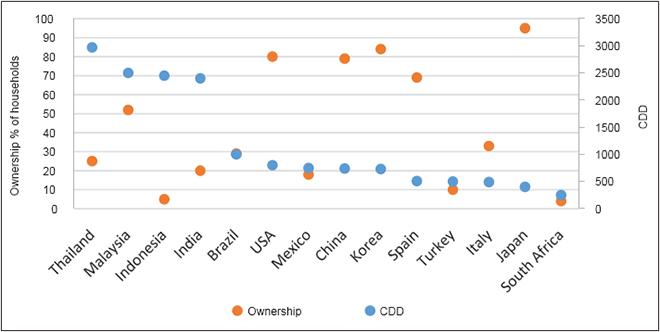

There are enormous disparities in access to space cooling across the world, with the poorest countries located in tropical parts of the world having the lowest share of space-cooling technologies. India, which has more than 3,000 cooling degree days (CDD)<49> consumes only 70 kilowatt hours (kWh) for space- cooling, compared to 800 kWh in South Korea that has only 750 CDDs (See Figure 6).<50>

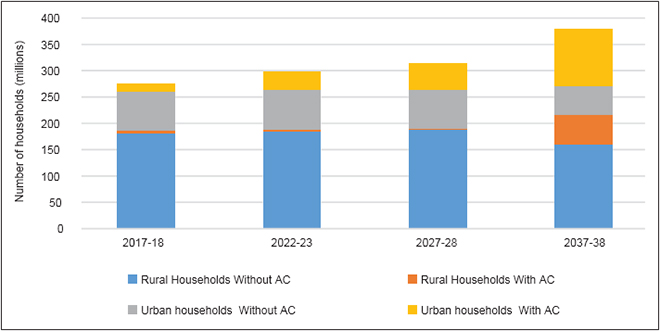

This disparity is mainly due to the low affordability of AC use in India. Currently, only about six percent of India’s households own ACs, but demand is growing rapidly with a 15-fold increase since 1990 (See Figure 7). By 2050, India, China and Indonesia are projected to account for most of the growth in energy use for space cooling.

Figure 6. AC Ownership and Climate: Select Countries

Source: Bruno Lapillonne, 2019

Source: Bruno Lapillonne, 2019

Figure 7. Number of Households with Room ACs in India

Source: MOEF&CC, 2018, India Cooling Action Plan (Draft).

Source: MOEF&CC, 2018, India Cooling Action Plan (Draft).

As global average temperatures increase, AC use in India and elsewhere is likely to become more of a necessity than a luxury. Therefore, improving the efficiency of AC systems is the only means to substantially reduce electricity consumption and, consequently, GHG emissions from space-cooling systems. The average efficiency of ACs in India is relatively low, given the cost-sensitive nature of the Indian market.

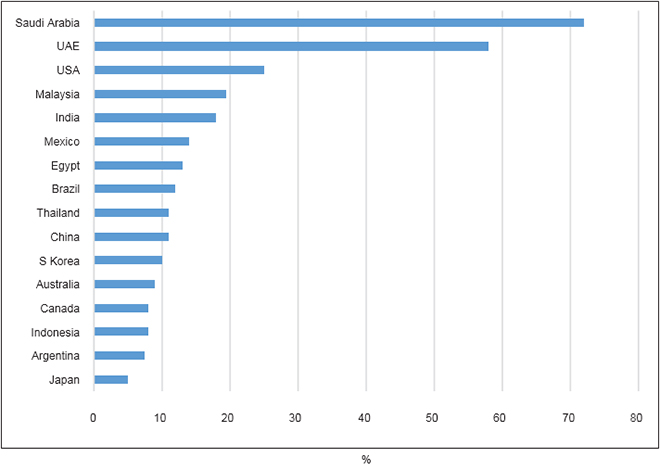

In this regard, South Korean companies active in the Indian market for space cooling can play an important role. The market for household space cooling is near saturation in South Korea, but the Indian market is just beginning to take off (See Figure 8). South Korean companies meet roughly a quarter of the demand for room ACs in India. As a large country with a growing demand for space cooling, India presents a great opportunity for suppliers from South Korea to introduce highly efficient but affordable space-cooling systems based on low-carbon technologies.

Figure 8. Share of ACs in Household Energy Use

Source: World Nuclear Association.

Source: World Nuclear Association.

Despite wide economic and social differences, South Korea and India share challenges in their efforts to decarbonise their energy systems. For South Korea, the critical challenge is to find a balance between maintaining industrial competitiveness and decarbonising. For India, the challenge is to balance between industrialising and decarbonising. By working together, the two countries can formulate technology-neutral policies for decarbonisation that are not only politically effective but also economically beneficial.

This essay originally appeared here

<1> In current US Dollars, World Bank Database.

<2> For South Korea, “Energy Info, Korea 2017”, Korean Institute of Energy Economics; for India, World Energy Outlook, International Energy Agency, Paris.

<3> Biomass is not included in the commercial energy basket.

<4> BP Statistical Review of World Energy, British Petroleum, 2019.

<5> Jong Ho Honga et al., “Long-term Energy Strategy Scenarios for South Korea: Transition to a Sustainable Energy System,” Energy Policy 127 (2019): 425–437.

<6> Niti Aayog, Draft Energy Policy, Government of India, 2017.

<7> Arjun Srinivas, “Why Oil Remains Central to India’s Twin Deficits,” Livemint, 5 September 2009.

<8> Korean Institute of Energy Economics, Energy Info, Korea, 2017.

<9> “Global Energy & CO2 Status Report: The Latest Trends in Energy and Emissions in 2018,” International Energy Agency, Paris.

<10> Matt Gray and Durand D’souza, “Brown is the New Green: Will South Korea’s Commitment to Coal Power Undermine its Low Carbon Strategy?” Analyst Note, March 2019.

<11> “South Korea”, Climate Action Tracker, 2019.

<12> “India’s Intended Nationally Determined Contribution is Balanced and Comprehensive: Environment Minister,” Press Information Bureau, Forest and Climate Change, Ministry of Environment, Government of India, 2 October 2015.

<13> Climate Action Tracker, “South Korea,” 2019.

<14> Climate Action Tracker, “India”, 2019.

<15> Matt Gray and Durand D’souza, op. cit.

<16> “Long Term Energy Outlook,” Korean Energy Economics Institute, 2016, quoted in Jong Ho Honga, et al., op. cit.

<17> Inha Oh, Wang-Jin Yoo and Yiseon Yoo, “Impact and Interactions of Policies for Mitigation of Air Pollutants and Greenhouse Gas Emissions in Korea,” International Journal of Environmental Research and Public Health 16, no. 1161 (2019): 1–17.

<18> “Thousands Protest German Coal Phaseout,” Deutsche Welle, 25 October 2018.

<19> David Robinson, “Prices Behind the Meter: Efficient Economic Signals to Support Decarbonisation,” The Oxford Institute of Energy Studies Energy, Insight 61, November 2019.

<20> Climate Home News, “Germany to Miss 2030 Climate Goal without Coal Phase-out”, 16 May 2019.

<21> Chiara Spinelli, “The EU ETS and the European Industry Competitiveness: Working towards post 2020,” Renewable Energy Law and Policy Review 7, no. 3 (December 2016): 25–34.

<22> “The Final Report of the Expert Group on Low Carbon Strategies for Inclusive Growth,” Planning Commission, Government of India, 2014.

<23> Iddri Lucas Chancel and Thomas Piketty, “Carbon and Inequality: from Kyoto to Paris Trends in the Global Inequality of Carbon Emissions (1998–2013) and Prospects for an Equitable Adaptation Fund,” Paris School of Economics, 3 November 2015.

<24> Simone Tagliapietra and Zachmann Georg, “What the ‘Gilets Jaunes’ Movement tells us about Environment and Climate Policies,” Bruegel, 30 November 2018.

<25> “Energy Sector Management Assistance Program, Annual Report 2018,” World Bank, 2018.

<26> “India Likely to Achieve 100% Household Electrification by January end,” Press Trust of India, 20 January 2019.

<27> Aditya Ghosh, “India’s Grid Expansion Erodes Island Solar Scheme,” Thomson Reuters Foundation, 24 October 2012.

<28> Kat Eschner, “California Power Outages Hit Small Businesses—but Bolster Generator Companies”, Fortune, 8 November 2019.

<29> Yoon-Hee Ha and John Byrne, “The Rise and Fall Of Green Growth: Korea’s Energy Sector Experiment and its Lessons for Sustainable Energy Policy”, Wire’s Energy and Environment 8, no. 4 (July/August 2019).

<30> K. Devis et al., “The G-20 Los Cabos Summit 2012: Bolstering the World Economy amid Growing Fears of Recession”, Brookings, June 2012.

<31> Yoon-Hee Ha and John Byrne, op. cit.

<32> Ibid.

<33> “Year End Review 2017 –MNRE”, Press Information Bureau, 27 December 2017.

<34> “PM Modi Vows to more than Double India’s Non-Fossil Fuel Target to 450 GW”, India Today, 24 September 2019.

<35> Manu Karan, “How India in a short period of time has become the Cheapest Producer of Solar Power,” Economic Times, 22 July 2019.

<36> “World Energy Outlook 2018,” International Energy Agency, Paris, 2018.

<37> Ibid.

<38> Costs that do not occur at the plant level but at the system level.

<39> Lion Hirth, Falko Ueckerdt and Ottmar Edenhofer, “Integration Costs Revisited – An Economic Framework of Wind and Solar Variability,” Renewable Energy 74, 925–939 (2015).

<40> Christopher Caldwell, “The Problem with Greta Thunberg’s Climate Activism: Her Radical Approach is at Odds with Democracy,” New York Times, 2 August 2019.

<41> “Country Profiles: Nuclear Power in South Korea”, World Nuclear Association, September 2019.

<42> Amena Bakr and Cho Mee-young, “South Korea Wins Landmark Gulf Nuclear Power Deal", Reuters, 29 December 2009.

<43> “Country Profiles: Nuclear Power in India”, World Nuclear Association, February 2019.

<44> Roger Pielke, “Net-Zero Carbon Dioxide Emissions By 2050 Requires A New Nuclear Power Plant Every Day,” Forbes, 6 December 2019.

<45> “French Consortium Enters SMR Race; Saudi Arabia and South Korea Sign SMR deal,” Nuclear Energy Insider, 25 September 2019.

<46> “The Future of Cooling Opportunities for Energy Efficient Air Conditioning”, International Energy Agency, Paris, 2018.

<47> Ibid.

<48> Bruno Lapillonne, “The Future of Air-Conditioning”, Executive Briefing, Enerdata, September 2019.

<49> They represent the number of degrees and number of days that the outside air temperature at a specific location is higher than a specified base temperature (or balance point). This indicates how much cooling will be required in the building.

<50> Bruno Lapillonne, op. cit.

The views expressed above belong to the author(s). ORF research and analyses now available on Telegram! Click here to access our curated content — blogs, longforms and interviews.

Ms Powell has been with the ORF Centre for Resources Management for over eight years working on policy issues in Energy and Climate Change. Her ...

Read More +