Virtual Digital Assets Regulation in G20 Countries: Finding Common Ground for the Development of a Global Governance Framework

Meghna Bal

Mohit Chawdhry

Statements made by public officials in certain G20 member states as well commentaries by financial analysts suggest that emerging market economies stand on a different footing from developed counterparts in their regulation of virtual digital assets. They attribute these differences to the distinct institutional, demographic, and economic vulnerabilities of developing countries. This paper examines this notion by presenting a quantitative analysis of the positions taken by G20 member countries on different facets of virtual digital assets regulation. Members were divided into two groups—G7 and non-G7 advanced economies, and emerging economies—to understand whether a country’s economic profile influences its regulatory policies on virtual digital assets. The paper finds that regulatory approaches to virtual digital assets do not vary significantly between G20 advanced and emerging market economies. It identifies gaps in regulatory approaches across member nations, and offers a useful guide for creating a global regulatory framework.

Attribution:

Meghna Bal and Mohit Chawdhry, “Virtual Digital Assets Regulation in G20 Countries: Finding Common Ground for the Development of a Global Governance Framework,” ORF Occasional Paper No. 402, April 2023, Observer Research Foundation.

Introduction

The G20 under India’s Presidency is aiming to devise a global framework for the governance of virtual digital assets (VDAs)[a]—an urgent imperative, given concerns surrounding the rapid rise of VDAs, the cross-border nature of VDA exchange and trading activity, and the implications they may have for financial stability and “increasing interconnectedness with the traditional financial system”.[1]According to the Financial Stability Board (FSB),[b]a global governance framework for VDAs would seek to comprehensively address the risks posed by them and related market activities, while harnessing the benefits of the underpinning innovation.[2]

The scope of the term “virtual digital assets” in this paper includes all types of digital assets except central bank digital currencies (CBDCs). The authors have excluded CBDCs because they are distinct from other types of digital assets as they are a form of legal tender and a liability on the Central Bank. However, some of the official documents referenced in this paper include CBDCs within their scope as they do not, for the purposes of certain types of policy, distinguish between CBDCs and other VDAs.

Most G20 states already have some form of legislation in place for the supervision of VDA activities. This paper examines the regulatory positions taken by G20 member countries, makes a quantitative assessment of policy positions, and identifies points of confluence and divergence across two groupings—emerging market, and G7 and Non-G7 advanced economies. The paper divides the G20 into these two groups because some scholars in international organisations as well as government officials from member countries have postulated that the economic circumstances of countries—such as fiscal stability or approach to foreign capital flows—would necessarily inform varied approaches to digital asset regulation.[3]

This analysis finds that approaches between emerging market and advanced economies in the G20 do not vary significantly. Using a quantitative assessment of qualitative factors, the paper also seeks to understand the gaps, if any, in approaches to VDA regulation across emerging and advanced G20 economies. The aim is to guide G20 members as well as the experts enlisted by them towards the creation of a global framework for VDA regulation.

Quantitative Assessment of VDA Regulation in G20 Countries

1. Motivations for Virtual Digital Asset Regulation

The framework used in this section is adapted from the United States (US) Executive Order on Ensuring Responsible Development for Digital Assets (Digital Asset EO).[4]The Digital Asset EO was issued by President Joe Biden on 9 March 2022, serving as a statement of policy on VDA governance in the US. The topics covered provide a comprehensive set of regulatory motivations addressing the risks posed by VDAs, as well as the innovation opportunities they present.[c]

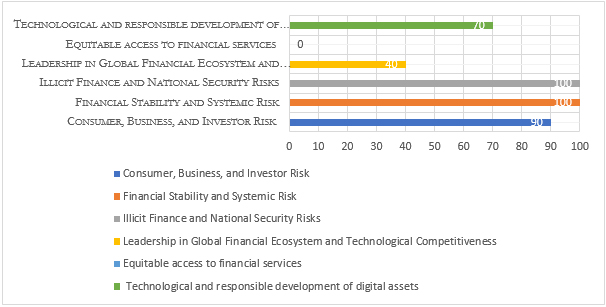

Figure1: Factors Cited as Drivers by G20 EMEs to Regulate VDAs(%)

Emerging market economies are primarily motivated to regulate VDAs to safeguard financial stability and mitigate systemic risk, protect consumers, mitigate money laundering, and arrest financing for terrorist activities. Not one of these nations are motivated to regulate to promote access to finance. This could mean that these countries either do not believe that there are linkages between VDAs and financial inclusion, or do not see regulation as a means to facilitate financial inclusion through VDAs.

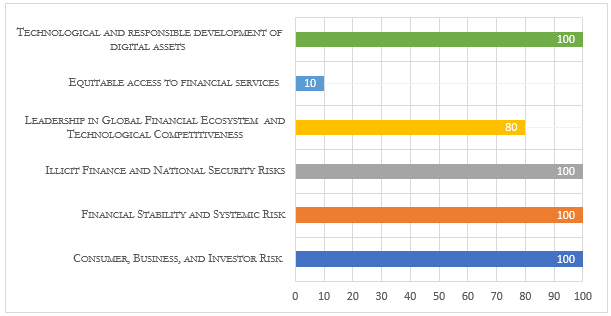

Figure2: Factors Cited as Drivers by G20 Advanced Economies to Regulate VDAs (%)

Overall, there are considerable parallels between the motivations of emerging markets and those of advanced economies in regulating VDAs. Consumer protection, financial stability, anti-money laundering (AML), and terror-financing risks appear to be the primary drivers of regulation in both groups. Similarly, most advanced countries, with the exception of the US, like their emerging market counterparts do not see VDA regulation as a lever for promoting access to finance.

However, there is divergence on one motivating factor. Eighty percent of advanced economies in the G20 place greater emphasis on the role of regulation to enable technological innovation and consolidate the positions of a majority of these economies as leaders in the global financial ecosystem. The proportion is a far lower 40 percent for emerging market economies.

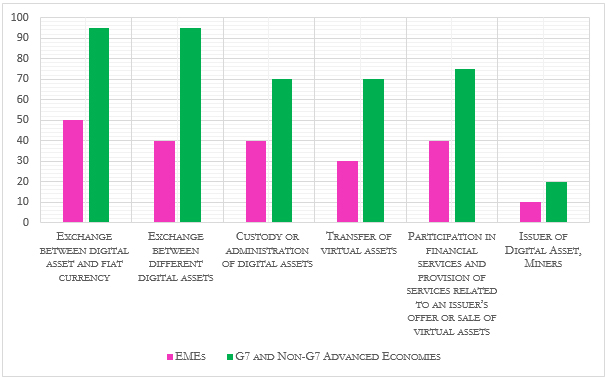

2. Legal Recognition of Virtual Digital Assets

Most G20 states have either formally or informally recognised the legality of VDAs within their jurisdictions. Formal recognition occurs where a member nation explicitly specifies the legality of VDAs through laws or regulations; informal recognition is where the legality of VDAs is inferred from a country’s actions and statements. Informal recognition is an important consideration as there are several G20 countries that permit VDA business activities but have yet to adopt an official position on their legal status.[d]

Similar to formal recognition, defining an activity as “illegal” requires an act of law or regulation. China is the only member of the G20 that has banned the trade, sale, and purchase of VDAs domestically. However, it is not illegal to hold VDAs in China.[5]

Figure3: G20 Advanced and Emerging Market Economies Favouring the Legalisation of VDAs (%)

Note:This figure shows the percentage of emerging market economies and G7 and non-G7 advanced economies in the G20 that have formally or informally recognised the legality of VDAs.

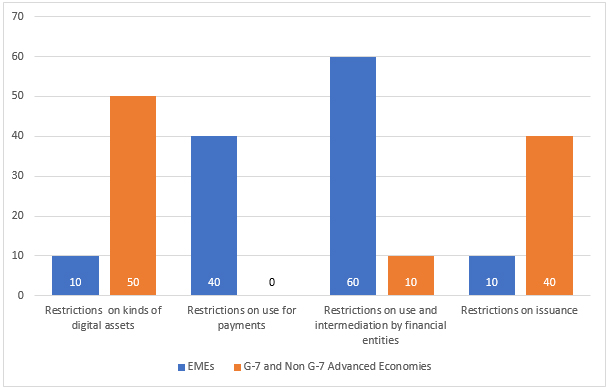

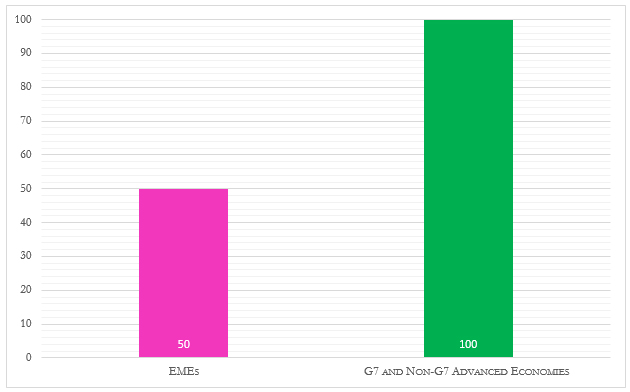

3. Restrictions on VDAs

The majority of G20 members across emerging and advanced economy groupings impose some form of restrictions on VDA activities. Seventy percent of emerging market economies, and the same proportion of the advanced economies, have put in place different restrictions on VDAs. These include bans on certain types of VDAs and restrictions on their issuance and intermediation by financially regulated bodies.

Figure4: G20 Advanced and Emerging Market Economies That Have Restrictions on VDA Activities (%)

Fifty percent of the G20 advanced economies have imposed restrictions on particular types of VDAs, most notably privacy coins. The reason is likely because privacy coins are almost completely anonymous, making transactions difficult to trace and therefore raising concerns around illicit financing.

Restrictions on the issuance of VDAs through initial coin offerings (ICOs) are imposed in France and South Korea, among the advanced economies. Initial coin offerings allow projects to raise funds from investors by issuing tokens in exchange for the capital they receive, usually in the form of a VDA or fiat currency.[6]South Korea banned raising funds through ICOs in 2017 due to the increased risk of financial scams.[7]

In France, only ICOs that have obtained approval from the financial regulator, the Financial Markets Authority (AMF in the vernacular) can be marketed to French citizens. For an ICO to be approved, the issuer must be incorporated in France, publish a white paper describing the VDA being offered, establish procedures for monitoring and safeguarding funds raised through the ICO, and comply with anti-money laundering requirements.[8]

The approach to restrictions on ICOs adopted by South Korea differs from that of France, but their underlying motivation is consumer protection. South Korea has opted for a ban to safeguard consumer interest,[9]and France imposed restrictions through regulation to protect consumers while also promoting the development of its local VDA industry.

Several emerging economies have imposed restrictions on the use of VDAs for payments (30 percent) and by financial entities (50 percent). In Saudi Arabia[10]and Mexico,[11]financial institutions are barred from providing VDA-related services, including using VDAs for settlement of payments. Only unregulated non-financial entities can provide VDA-related services, such as their purchase, sale and issuance. Statements from regulators in these countries indicate that these restrictions are aimed at reducing risks posed by VDAs to the overall financial system.[12]

Turkey, for instance, prohibits financial institutions from providing any intermediation services related to the use of VDA for payments.[13]In Indonesia, only commodities exchanges approved by the regulator can provide VDA-related services and all other financial services are barred from offering and facilitating the sale of VDAs.[14] In comparison, only one among the G7 and non-G7 advanced economies (i.e., Italy) restricts financial institutions from dealing with VDAs. There is no G20 advanced economy that imposes restrictions on the use of VDAs for payments.

Figure5: Types of Restrictions Placed on VDA Activity by G20 Advanced and Emerging Market Economies With Restrictions on VDAs (%)

4. Licensing

According to the International Monetary Fund (IMF), the creation of licensing, authorisation, and registration mechanisms is a critical element of an effective VDA policy framework as it allows financial regulators to exercise oversight and supervision of these markets.[15]The Financial Stability Board also recommends prior registration and approval requirements as an effective policy tool to ensure robust governance of VDA markets.[16]While all advanced G20 economies have some form of licensing in place for virtual digital assets service providers (VDASPs), only about half of the G20 emerging market economies have such provisions in place.

Figure6: G20 Advanced and Emerging Market Economies That Require Licensing for VDASPs (%)

Overall, fewer G20 countries have introduced licensing and authorisation requirements for custodial and other service providers such as miners, brokerage/investment/ICO advisers, and token issuers. The rationale may be the considerable interdependencies between exchanges and other VDASPs. Exchanges provide a concentration of activity and enable centralised platform governance of a decentralised set of actors. As such, countries may seek to regulate related service providers through intermediaries like exchanges. For instance, an exchange’s listing criteria would indirectly govern token issuers. This is similar to how intermediary social platforms are used to regulate the activities of their users through due diligence requirements under intermediary liability frameworks. However, it would be useful for countries to investigate where gaps may lie in such an exchange-led enforcement approach.

Figure7: G20 Advanced and Emerging Market Economies That Impose Licensing on Different VDASPs (%)

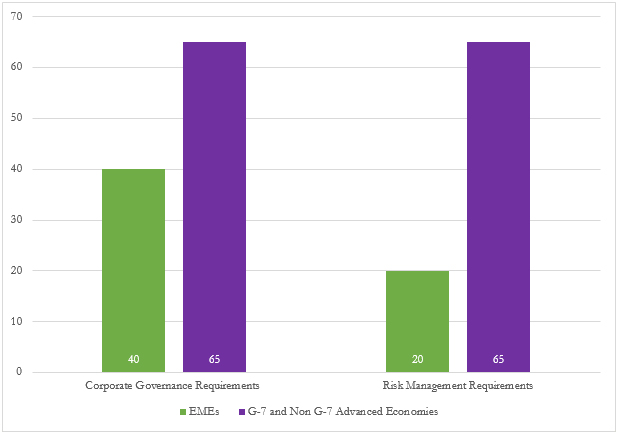

5. Corporate Governance and Risk Management

Over the past year, some of the world’s leading VDASPs suffered a series of corporate governance failures and bankruptcies. Among the most notable cases is that of FTX—a VDA platform based in the Bahamas—which lost more than US$32 billion in value and at least US$1 billion in consumer funds over the course of one year.[17]The upheaval in the VDA markets has cast the spotlight on the absence of effective internal governance and control measures as well as risk management mechanisms aimed at protecting user funds. As a result, the imposition of effective governance and risk management requirements has become a hot-button issue for regulators globally. The International Organization of Securities Commission,[18]FSB,[19]and IMF[20]have all recommended that governance measures such as fit and proper tests and conflicts of interest resolution mechanisms, as well as risk management requirements—including the segregation of user funds and safe custody measures—should be applied to VDASPs.

There is a notable divergence in the application of corporate governance and risk management requirements to VDASPs between the emerging and advanced G20 economies. Sixty-five percent of advanced economies have introduced or extended governance and risk management requirements to VDASPs. In contrast, only 40 percent of emerging market economies have introduced governance requirements, and only 20 percent have risk management requirements in place.

Figure8: G20 Advanced and Emerging Market Economies That Require VDASPs to Comply With Corporate Governance and Risk Management Regulations (%)

The divergence between the two groupings can be attributed to the fact that a number of advanced economies classify certain types of VDAs as financial products in keeping with the “same risk, same regulation” principle. Thus, regulatory requirements applicable to traditional financial instruments also apply to entities dealing with VDAs that resemble other financial products. For instance, Germany,[21]Canada,[22]and the United Kingdom (UK)[23]brought certain VDAs under regulations that apply to banks and other financial service providers. Such regulations usually include corporate governance and risk management requirements. Conversely, South Africa is the only emerging economy in the G20 that has classified VDAs as a financial product.[24]

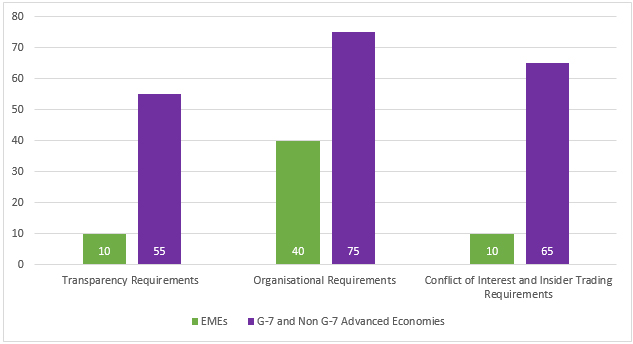

Seventy-five percent of G20 states have instituted organisational requirements, such as minimum qualifications for executives and board constitution, and incorporation formalities, for VDASPs. Only 55 percent of advanced economies and 10 percent of emerging economies require VDASPs to comply with transparency and disclosure requirements. This is likely to change if the G20 accepts recommendations on VDA regulation made by the FSB and IMF. Both bodies recommend that VDASPs should disclose information regarding their operations, risk profiles, financial conditions, and products offered to users and other stakeholders.[25]

Figure9: G20 Advanced and Emerging Market Economies That Require VDASPs to Comply With Corporate Governance Measures (%)

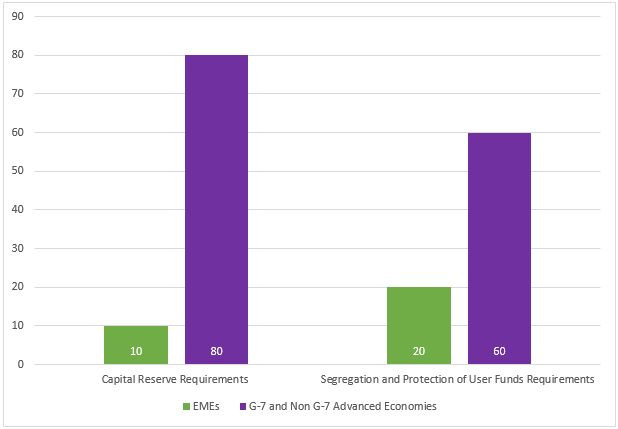

Nearly 80 percent of G7 and non-G7 advanced economies in the G20 require VDASPs that offer VDAs classified as financial products to maintain minimum capital reserves and implement prudential reserve management policies.[e]Such requirements have predominantly been suggested in the context of stablecoins. A stablecoin is a VDA that aims to maintain a stable value relative to a specified asset or a pool or basket of assets.[26]Some notable examples of stablecoins are USDC—issued by the American financial services company Circle—and USDT, minted by Hong-Kong based Tether Inc. Indeed, the FSB’s 2020 High-Level Recommendations on Global Stablecoin Arrangements call for the imposition of capital reserve requirements on issuers of stablecoins to address run-risks.[27]The FSB is expected to publish revised recommendations for global stablecoin arrangements by mid-2023. The completion of this review process could provide added impetus to national regulatory authorities, particularly in emerging economies, to impose reserve management requirements on VDASPs, especially stablecoin issuers.

There could also be an uptick in regulations requiring VDASPs to segregate user assets i.e., the storage of user assets separately from those of the service provider to ensure their sanctity and prevent commingling. Several instances of such commingling by VDASPs came to light in 2022, with the most notable example being the use of consumer funds by FTX, an exchange and trading platform, to fund its sister entity Alameda Research—a VDA hedge fund.[28]Some G20 members have already implemented regulations to limit such market conduct. Asset segregation regulations in Indonesia and Japan, for instance, require VDASPs to store a large percentage of user funds in a cold wallet, i.e., on an offline wallet that is not used for active trading, to prevent the mixing and diversion of user funds.

Figure10: G20 Advanced and Emerging Market Economies That Require VDASPs to Comply With Risk Management Measures (%)

6. Anti-Money Laundering (AML) and Combating Financing of Terrorism (CFT)

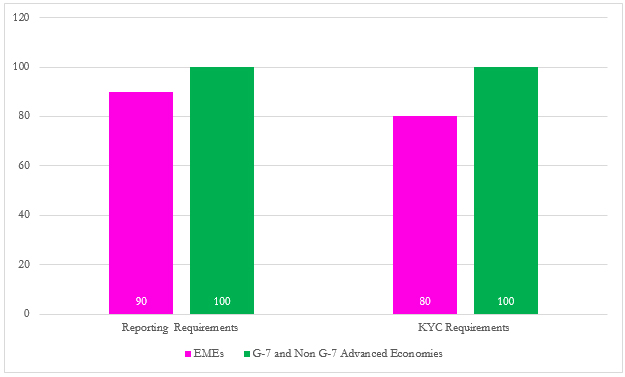

Many VDA transactions are pseudonymous (or anonymous in the case of privacy coins). While each transaction is recorded on the blockchain, the identities of the parties transacting are not captured. Instead, parties to the transaction are identified by their wallet addresses. Pseudonymous VDA transactions are a potential vehicle for money laundering and terrorist financing. Therefore, preventing the use of VDAs for illicit financing activity is a top priority for countries. As such, almost all G20 member nations require VDASPs to comply with AML/CFT regulations. China is the only G20 member yet to extend AML/CFT regulations to VDAs. However, transactions involving VDAs are banned in the country. Argentina—the only other country yet to introduce KYC obligations for VDASPs—is considering the introduction of a law that would require these providers to comply with a comprehensive AML/CFT framework.[29]

Figure11: G20 Advanced and Emerging Market Economies That Impose AML/CFT Reporting and KYC Requirements on VDASPs (%)

The Financial Action Task Force (FATF), the global anti-money laundering watchdog,[f]brought out AML standards for VDASPs[g]in 2018.[30]G20 member countries committed to the implementation of these FATF standards on AML/CFT for VDAs at the Finance Ministers and Central Bank Governors’ Meetings in 2018.[31]

However, member states have achieved only marginal progress in implementing the standards, which include risk assessment of VDASPs, targeted financial sanctions compliance, and preventive measures such as the Travel Rule and licensing/registration of VDASPs. Illustratively, the FATF’s latest targeted update on the implementation of its standards, though not specific to G20 countries, notes that only 23 percent of evaluated jurisdictions arelargely compliantwith its recommendations while 63 percent arepartially compliant.[32]

The unanimous compliance by G20 members with the FATF recommendations on AML is necessary because some standards are rendered ineffective if there are gaps in implementation. For example, the Recommendation 16 of the FATF standards, colloquially known as the “Travel Rule” requires VDASPs to collect and share relevant originator and beneficiary information associated with VDA transactions. The cross-border nature of VDA transactions makes it difficult to meet travel rule compliance standards in cases of transfers to or from VDASPs where there are no regulations requiring the collection and provision of transaction counterparties. The situation leaves many cases where information is unavailable. The agenda of the G20, therefore, should include the resolution of cross-border issues that arise in travel rule implementation. Another key point would be to create a standard for personally identifiable information on users that is acceptable, attainable, and available in all member countries. A final point would be to consider how to encourage G20 non-members to comply, to reduce the opportunity for arbitrage in a global AML framework.

7. Taxation

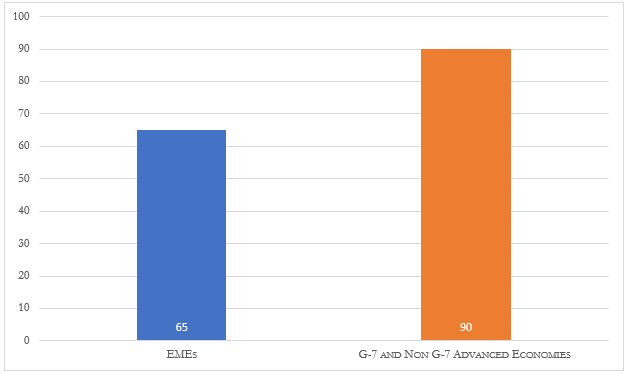

The increasing value and market capitalisation of VDAs along with the associated windfall gains for investors, has prompted governments around the world to tax VDAs in a bid to bolster their own revenues. Ninety percent of advanced economies in the G20 have imposed either direct or indirect taxes on VDAs. The only exception is the European Union (EU), where there is currently no continent-wide tax proposal for VDAs. However, media reports suggest that the EU has already begun work on creating a uniform tax policy for its member states.[33]Among the emerging economies in the G20, only 65 percent have taxed VDAs so far.

Figure12: G20 Advanced and Emerging Market Economies That Tax VDAs (%)

A higher percentage of both advanced and emerging market G20 economies have implemented direct taxes, such as corporation tax or capital gains tax, on VDAs when compared to indirect taxes, such as value-added tax or goods and services tax. A 2022 study by the Organisation for Economic Cooperation and Development (OECD) on the tax treatment of VDAs suggests that this difference can be attributed to how VDAs are classified under direct and indirect tax legislation.[34]Most member countries, both emerging and advanced, have classified VDAs as some form of property, including intangible assets, under direct tax legislation. Gains made by individuals and companies from holding and trading such assets are therefore considered income from property, which is taxable.

Conversely, VDAs are classified as currency under indirect tax statutes by several countries in the G20, most notably EU members.[35]Therefore, their issuance and exchange are usually exempt from indirect taxes. However, the provision of services related to VDAs, such as wallet custody, may be included under the scope of indirect taxation in such countries.[36] The same OECD study also states that taxing VDA transactions is complex as their value is prone to fluctuation and determining their tax incidence in fiat currency can be a challenge.[37]

The issue of tax is important from the perspective of offshoring and arbitrage. A 2023 study by the Esya Centre found that the introduction of high tax rates on VDAs in India prompted offshoring trade volumes worth INR 32,000 crores (US$ 3.8 billion).[38]G20 member countries may consider coming together to bring out harmonised tax structures to discourage offshoring of volumes to countries with more permissive tax environments.

8. Advertising Regulations

Globally, the growth of the VDA market has been accompanied by aggressive advertising by VDASPs, promising guaranteed high returns or making it appear that their products were officially licensed by regulatory authorities. For example, the Anchor Protocol—a VDA lending and borrowing service—advertised 20 percent returns to their investors on deposits of a specific stablecoin (i.e., TerraUSD).[39]Consequently, many retail investors used their savings to purchase TerraUSD and deposit it with the protocol.[40]However, in May 2022, the TerraUSD stablecoin suffered a liquidity crisis and lost almost all of its value. Retail investors who had purchased TerraUSD due to the guaranteed returns suffered significant losses.[41]

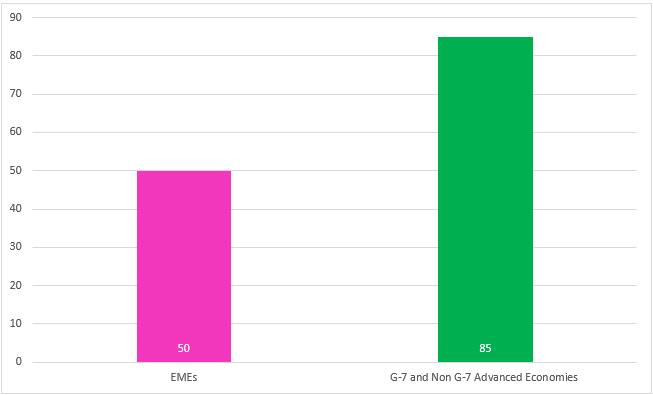

The prevalence of misleading and speculative promotion of VDAs has led to increased regulatory scrutiny. Eighty-five percent of advanced economies in the G20 have enacted rules that prevent VDASPs from making false or misleading statements in advertising or marketing materials. Fifty percent of emerging economies have also introduced similar rules to clamp down on misleading and false advertisements.

Figure13: G20 Advanced and Emerging Market Economies With Regulations on Advertising of VDAs and VDA-Related Activities (%)

Two reports by the IMF in 2022 also highlight the importance of transparent and clear communication and marketing by VDASPs.[42]The reports recommend the incorporation of requirements for the publication of a white paper for issuers of VDAs—this would provide potential investors with relevant information on the investment product and prevent false and misleading statements.

The views expressed above belong to the author(s). ORF research and analyses now available on Telegram! Click here to access our curated content — blogs, longforms and interviews.

PDF Download

PDF Download