India is at a crossroads. It has the largest young workforce anywhere in the world, and is the fastest growing economy today. At the same time, the economy is not creating enough jobs, and therefore not fully harnessing its “demographic dividend” in preparation for the “Fourth Industrial Revolution”. To create more and better jobs, certain fundamental realities need to be recognised – the untapped opportunities in the services sector, the imperatives of policy and regulatory stability, and the welfare needs of a new workforce. After briefly analysing the supply-side context (the characteristics of the so-called “demographic dividend”), this paper outlines a basic strategic roadmap for the demand side with a focus on constituents of the new economy (the industries that will have to generate new employment). It concludes with recommendations that can help bridge supply-side gaps, and demand-side imperatives.

Characteristics of the Indian Workforce

The Indian workforce has three distinct characteristics: (a) It is a young workforce; (b) the skills base of this workforce remains underdeveloped; and (c) most jobs are being created in the informal economy. These supply-side characteristics are explained first.

The Indian workforce is young and will remain young in future decades – a trend that immediately separates India from advanced economies; in which ageing workforces have to carry the mantle for the “Fourth Industrial Revolution”, characterised by “a range of new technologies that are fusing the physical, digital and biological worlds, impacting all disciplines, economies and industries, and even challenging ideas about what it means to be human”.[i]According to the National Sample Survey (NSS) of 2011-12, around 36 percent of India’s total population are under the age of 17, and approximately 13 percent are between 18 and 24 years (Table 1). While over 41 percent of the population between 18 and 24 years are already part of the workforce, the others will be joining the workforce in the next two decades.

Table 1: Age Groups and Breakdowns of Population and Workforce, 2011-12, (%)

Age Group (in years)

Percentage of Total Population in Each Group

Workforce as Percentage of Total Population in Each Group

0-17

35.91

3.01

18-24

12.7

41.49

25-59

43.22

63.09

>= 60

8.17

34.48

Total

100

36.43

Source:68th Round, National Sample Survey @ Observer Research Foundation’s India Data Labs

By 2030, when most countries around the world will have middle-aged or elderly workforces, India will still be young. For instance, according to the European Commission, without migration, the European Union (EU) workforce will shrink by 96 million workers by 2060.[ii]The demographic problems of other Organisation for Economic Cooperation and Development (OECD) countries are also well documented.[iii]Not only is the Indian labour force young, it is also characterised by low participation in the economy, with a participation rate of only 53.8 percent. This can partially be explained by low female participation and high youth unemployment.

Given its implications for policy planning, it is imperative to briefly disaggregate the sector-wise distribution of the young workforce (Table 2). For instance, despite the fact that the agriculture sector accounts for only around 16 percent of gross value added (GVA), close to 45 percent of those who are part of the workforce and are aged between 18 and 24 are engaged in it (Reserve Bank of India, 2013-14). Conversely, while the services sector accounts for over 60 percent of GVA, only around 23 percent of the workforce in the same age group are engaged in the sector. The services sector is much less labour-intensive and simultaneously more productive than the primary and secondary sectors.

Table 2: Share of Employment by Sector, 2011-12 (%)

Agriculture

Manufacturing and Mining

Services

0-17

52.44

33.32

14.23

18-24

44.75

31.79

23.46

25-59

47.24

23.67

29.09

>= 60

67.77

14.62

17.62

Total

48.66

24.38

26.96

Source:Source: 68th Round, National Sample Survey @ Observer Research Foundation’s India Data Labs

This cleavage between value addition and job creation is perhaps best exemplified by the fact that the number of ‘direct’ jobs created by the Information Technology (IT) and Information Technology Enabled Services (ITES) sub-sectors was only around three million as of 2013.[iv]Though the IT and ITES sub-sectors are the backbone of the services sector, they are understandably not as labour-intensive as factory floors (which in turn are also becoming increasingly automated). This partly explains why successive governments have tried to reinvigorate the manufacturing sector, even though it accounts for only 18 percent of the total GVA. The latest effort in this regard is the Modi government’s “Make in India” initiative.

India will find it increasingly hard to navigate the Fourth Industrial Revolution, which is capital intensive, and is already catalysing a new wave of high-end manufacturing in the West. One of the central challenges to the development of high-technology industries in India has been the lack of capital formation, as evidenced by the lack of capital market depth, and increasingly skewed patterns of wealth aggregation. These are also empirically validated trends, and therefore, observations on capital deficits in India will be limited to echoing the findings of Bosworth and Collins (2008), who suggest that the contribution of capital to India’s growth over 1993-2004 “remained well below those evident during the investment-led rapid growth experiences of the East Asia miracle…(and) in contrast, China achieved a rate of capital deepening comparable to that for East Asia in the 1978–1993 sub-period, and a substantially higher rate more recently”.[v]

Intuitively, a low-end manufacturing focused policy planning framework is not temporally consistent with the Fourth Industrial Revolution. In this context, the Indian services sector seems nimbler than manufacturing. This is primarily because it is not necessarily capital intensive and can harness India’s large young workforce and absorb previously excluded workers. This workforce can arguably adapt to technological changes – if it can be exposed to useful educational content, and adaptive learning. While India is often seen as the bastion of engineers and technology-savvy entrepreneurs, most of the country’s young workforce is ill-equipped to be part of a services sector-led transformation that can harness technology – this is the second key characteristic of the workforce. Only around a quarter of the workforce aged 18 to 24 have achieved ‘secondary’ and ‘higher secondary’ education, and close to 13 percent are illiterate (Table 3). Job-related skills, even after higher education, are often missing.

Table 3: Levels of Education by Age Group, 2011-12 (%)

Age Group (in years)

Illiterate

Up to Primary

Middle

Secondary & Higher Secondary

Diploma & Certificate Courses

Graduate & above

0-17

26.0

45.5

20.3

7.9

0.3

0.0

18-24

13.1

25.7

24.0

26.4

2.4

8.3

25-59

29.1

23.0

16.0

19.1

1.6

11.2

>= 60

54.5

23.7

8.2

9.3

0.6

3.8

Total

28.7

24.1

16.7

19.1

1.6

9.9

Source:68th Round, National Sample Survey @ Observer Research Foundation’s India Data Labs

There are unique technological phenomena that policymakers can exploit to address the skill development deficits in the country. For instance, there are nearly one billion mobile phone users in India.[vi]Despite the fact that millions of them are at the bottom of the socio-economic pyramid, and may not know how to read or write, they are “keypad literate”—meaning that they are able to use their mobile phones to access basic services and recall visual patterns. This has tremendous implications in different supply chains where information asymmetry erodes value generation. For instance, Dinesh Katre (2010) suggests that there is a large “opportunity for designing innovative mobile applications for an entirely new segment of (low income, illiterate and semi-literate) users like fishermen, farmers, carpenters, electricians, fabricators, vegetable merchants, shopkeepers, drivers, transport managers, traffic controllers, factory workers, building contractors…”.[vii]

The agricultural supply chain is perhaps the most obvious example, where imperfect information on weather phenomena and market prices are major reasons for suppressed agrarian incomes. While it is outside the scope of this paper to discuss how agrarian incomes can be brought back on track, it is clear that the means to affect changes that can enable greater value generation in agriculture are now within India’s grasp. Given the scale of telecommunications penetration (discussed later), it is safe to assume that a large part of the agrarian workforce already has the means to access information. Therefore, the question is: how should India leverage technological dispersion and close the gap on information asymmetries?

There are also many ways in which the advent of telecommunications on a large scale can be leveraged to overcome traditional service delivery challenges. The Indian government’s ‘JAM trinity’, of the Jan Dhan Yojana (a ‘banking for all’ scheme), Aadhaar number (a unique identification number for each citizen) and mobile phones, aims to do just this: use the potential of technology to enhance financial inclusion. Even if its implementation success or ethos is a matter of debate, the penetration of telecommunications technology is an added tool in the hands of policymakers to affect changes that can make India more future-resilient.

Related to this telecommunications opportunity is the potential of upgrading broadband technology, which is currently defined in India as internet download speeds above 512 Kbps. The National Telecom Policy, 2018, currently on the anvil, is likely to focus on achieving higher speeds in the broadband ecosystem. There are several constraints to the quality provision of broadband in the country including Right of Way restrictions that impact operators who lay optic fibre, and inconsistencies in telecom policies and regulations that have led to a congested wireless network and misalignment of economic incentives. Even countries such as the US, with legacy challenges in delivery of high-quality broadband services, define a minimum threshold of 25 Mbps for downloads and three Mbps for uploads.[viii]

However, India has close to 350 million broadband users, which is higher than most other major countries in the world as an absolute number. Therefore, in terms of penetration, the country is already well poised to harness the returns to increasing technological access from a low base. Much of the growth in internet access is driven by an increase in mobile phone penetration (wireless consumers in Table 4), which has led to India being called a “mobile-first” jurisdiction. If India can get its quality of broadband provision right – by focusing on addressing barriers to access and usage at the last mile – there will be a commensurately large opportunity for governments, private sector and civil society institutions to leverage the power of audio and video content, towards skill upgradation.

Table 4: Telecom Subscription Data, December 2017

Particulars

Wireless

Wire-line

Total

Total Telephone Subscribers (million)

1167.44

23.33

1190.67

Urban Telephone Subscribers (million)

668.44

19.81

688.25

Rural Telephone Subscribers (million)

499

3.42

502.42

Urban Tele-density (%)

163.44

4.84

168.29

Rural Tele-density (%)

56.28

0.39

56.66

Broadband Subscribers

345.01

17.86

362.87

Source:Telecom Regulatory Authority of India

The third key characteristic of the young Indian workforce is that the informal economy (characterised by the absence of social security) still accounts for a large share of employment creation, in both the organised and unorganised sectors of the economy (Table 5). It is simultaneously characterised by the prevalence of micro businesses and low value addition. This is related to legacy challenges such as the lack of capital market depth and consequent impact on long-term capital formation, limited natural resources, low levels of savings and wealth accumulation in absolute terms, and various other confounding developmental, infrastructural and institutional deficits.

Table 5: Prevalence of Informal Economy, 2011 -12 (%)

Sector

Formal

Informal

Total

Organised

47.52

52.48

100

Unorganised

5.82

94.18

100

Total

11.23

88.77

100

Source:68th Round, National Sample Survey @ Observer Research Foundation’s India Data Labs

In fact, the labour market has “become increasingly dominated by informal enterprises or informal employment” which is “traditionally characterised by low levels of productivity and low wages”, which is in turn reflected in the fact that close to 90 percent of the population is engaged in informal economic activities, yet their output only accounts for 50 percent of the nation’s gross domestic product (GDP).[ix]

An examination of the key productivity metrics of the Indian economy also points to the fact that there is large variance between the relative contributions of productivity growth to sectoral output (Table 6). Total Factor Productivity (TFP), generally defined as “the portion of output not explained by the amount of inputs used in production” is the measure of productivity used in Table 6 (the numbers are inclusive of the contribution of the informal economy).[x]TFP growth accounts for about one-fourth of the growth in GVA. The variation between sectors illustrated in Table 6 indicates that growth in the services sector, which accounts for the largest share of value within the GDP, has been in part driven by productivity gains, but there is still scope for improvement. One can reasonably infer that much scope also lies in the informal economy.

If India can improve productivity metrics in the informal services sector, there will be surpluses that can be channelled towards new business opportunities in the Fourth Industrial Revolution. As observed by Ghani, 2011, the “globalization of services provides many opportunities for late-developing countries to find niches, beyond manufacturing, where they can be successful”.[xi]

Table 6:Trend Growth Rate in Real Value Added and Contribution of Factor Inputs and TFP to GVA growth by Sector, 1980 to 2008 (%)

*Includes the contribution of land; **sectors as defined by the Reserve Bank of India report

The responsibility for the creation of productive and secure jobs for a workforce characterised by young demographic, low skill intensity and informal jobs, cannot be shouldered by the government alone. The private sector has an intrinsic role to play in generating value and creating the surpluses that can be reinvested in job creation through competitive industries and sectors. The primary role of government, therefore, is to allow for the requisite value creation in an economy characterised by high volume and low value markets. This is evidenced by sectors such as telecommunications, where the average revenue per user is among the lowest in the world, but the user base is among the largest in the world. The next sections discuss such demand-side imperatives.

Building Sectoral Focus

Some of the key supply-side characteristics of the workforce have been discussed briefly. It is equally important to assess demand-side characteristics. To do this, this paper first adopts a services-sector lens. The World Bank has highlighted the relatively larger contribution of growth in the services sector to poverty reduction compared to that of agriculture or manufacturing.[xii]The Indian government also expects a large part of GDP growth to be driven by the services sector.[xiii]Moreover, globally, trade in services has demonstrated greater resilience to economic shocks, in terms of lower magnitude of decline, less synchronicity across countries, and earlier recovery.

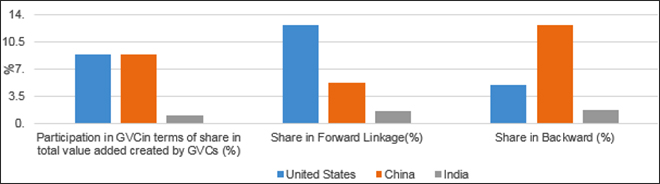

The current Foreign Trade Policy places emphasis on service trade exports and aims to grow this segment to US$300 billion – close to double the current levels. The uptake of the policy, however, remains limited at the level of small business. Owing to scale-related challenges across the board, participation of Indian businesses in international service markets remains below par, despite large opportunities. The “servicification” of manufacturing processes is one such opportunity. Producers and exporters of manufactured goods have become more reliant on services, such as design, marketing, distribution, banking, telecommunications and insurance to remain competitive.[xiv]Such value-added services are often disaggregated across geographies. This is a characteristic of production through global value chains (GVCs), which have become a prominent feature of trade over the last two decades.[xv]However, the level of India’s forward and backward integration into these GVCs leaves a lot to be desired (Figure 1).

Figure 1: Comparative Participation in GVCs, 2009

Source:OECD Stat and OECD-WTO TIVA, May 2013

Services account for almost half (46 percent) of value-added in exports globally. This share is higher in developed countries (50 percent) than in developing countries (38 percent).[xvi]There is little doubt that as progressive trade liberalisation and technological advances increase the fragmentation of production, GVCs will inevitably become a dominant feature of many industries within developing countries. India currently runs the risk of remaining locked into relatively low valued-added export activities. In order to leverage new global trade realities, Indian policies and businesses must rethink a manufacturing-centred narrative on employment creation.

India has to become a solutions provider to the world if it is to play a greater role in GVCs. It can capture a greater part of the value chain through integration of its robust services sector with regional value chains and GVCs. India’s vibrant export-oriented services market is relatively open in several sub-sectors (such as computers, audio-visual and engineering). There is visible improvement in policies in other traditionally closed sub-sectors such as telecommunications, broadcasting, legal and air transport services, although there is scope for further liberalisation that can aid competitiveness and integration with GVCs. For instance, while the broadcasting sector is allowed 100 percent foreign direct investment (FDI), there are cross-holding restrictions that prohibit broadcasters from owning more than 20 percent in distribution platforms such as Direct-to-Home and Headend-in-the-Sky. Similarly, while single-brand retail trading policy allows for 100 percent FDI, there are various prohibitive conditions attached to this, including a limited window for offsetting domestic procurement requirements through exports.

A major challenge for India’s integration into intra-regional value chains and GVCs is inefficiencies in the supply chain and the lack of supply chain standards – which is also connected to the competencies of the workforce. However, the actualisation of better supply chain standards will also require both demand side pull and supply side push factors. The demand side is clear – better integration in the GVCs as well as adherence to the stricter standards regimes that are emerging as a result of the proliferation of Regional Trade Agreements (RTAs). India has itself signed some 20 such RTAs over the last decade. As mega RTAs such as the Regional Comprehensive Economic Partnership (RCEP) become operationalised, the importance of standards setting in GVCs will become self-evident.

It is incumbent upon both the public and private sectors to build awareness and capacity at the level of small businesses, to improve product and service standards. The government needs to put nodal agencies such as the Bureau of Indian Standards (BIS) to work on new technologies, and services standards in particular. Currently there is asymmetric attention given to product standards in India compared to service standards. The BIS has issued approximately 3,000 manufacturing standards and 100 service standards. Moreover, most standard-setting bodies in India operate like a black box, allowing for very little industry feedback in the standards setting process, whereas they should actually be setting an example in terms of promoting multi-stakeholder interactions.

Additionally, much more initiative will have to be taken by “lead firms” across different supply chains, which have the wherewithal to understand and match regional and global standards requirements. Traditionally, investments by lead firms within their supply chains have been nominal, perhaps partly due to concerns around monitoring and evaluation of the proceeds of such investments. Consequently, the ability of Indian supply chains to match global standards has been in doubt. However, with increasing digitalisation, and easily available enterprise solutions, it would be reasonable to expect far greater supply chain investments in the future if large businesses see clear rationale in upgrading their own supply chains, so that their final products or services meet quality requirements of whichever market they want access to.

In sum, the convergence of digitalisation and supply chains is where India can claim its share of the GVC and simultaneously generate employment for its young, informal workforce. By becoming more competitive in non-manufacturing industries, such as design, content, new media, data analytics, logistics and other digital services, India can leverage digital technology so that its companies can interact seamlessly with the global economy. Needless to say, skill generation and upgrade will have to be juxtaposed against the creation of new jobs (i.e., the demand-side paradigm).

Regulating the New Economy

This section elaborates on demand-side drivers for job creation in India, with a focus on the nature of the largest regulatory challenges to the growth of the economy. Though the Modi government has shown that it is serious about making progress on Ease of Doing Business rankings, as seen in India’s progression in the World Bank’s annual estimates, such rankings do not sufficiently capture demand-side realities. Are Indian businesses better able to unlock value today because of an empathetic government that is sending the right signals to the market? One area to look for answers is in the domain of regulators – which are responsible for day-to-day oversight of most major markets, including technology markets that drive the new economy.

Regulatory uncertainty has been a persistent problem in Indian markets. This is because regulatory decisions in India are inconsistent, undermining the business environment. The lack of uniformity in decisionmaking has been identified as a key issue by the 13th Report of the Second Administrative Reforms Commission, which has delineated that regulators are established to help fulfil the overarching policy objective of the government. The report has further identified challenges in (a) consistency with respect to powers and functions of the regulators; (b) independence of the regulatory agencies; (c) uniformity in terms of appointment, tenure and removal of regulatory authorities; and (d) a legal framework that can direct the interface between the regulators and the government.

The persistent level of regulatory uncertainty in India can be inferred on several counts. In terms of the institutional landscape, the Modi government’s Finance Bill, 2017, prescribed the alteration of 19 regulatory tribunals and dissolution of several others, overnight. The Cyber Appellate Tribunal (CyAT) under the Information Technology (IT) Act, 2000, was one such tribunal, whose powers now reside within the Telecom Disputes Settlement Authority of India (TDSAT). In 2016, the Comptroller and Auditor General of India reported that the position of the CyAT chairperson had remained vacant since 2011. This had led to an immense amount of pendency in the system. However, the wider point to consider is whether the TDSAT, a tribunal that adjudicates telecom and broadcasting matters, is suitably equipped to handle cases under the IT act.

Similarly, the merger of the Copyright Board with the Intellectual Property Appellate Board (IPAB) last year, which was originally established under the Trade Marks Act, 1999, has raised doubts within industry about the ability of the IPAB to deal with cases linked to copyright, since it already has a large amount of pendency in matters related to patents and trademarks, and copyright is governed by another parent act.[xvii]

Regulatory uncertainty is also exacerbated by the fact that, in several markets, there is now increasing convergence between technologies and modes of distribution of products and services, which has been met with ad hoc government responses. The telecom and broadcasting industries constitute one such market, where through the spread of Over-the-Top (OTT) services, a new form of content delivery has been made possible over the internet. This content, unlike broadcast content, is largely based on the willingness of consumers to “pull” such content towards them. This fundamental distinction from receiving what is ostensibly “push” content – pushed to consumers by broadcasters through intermediaries like cable operators – reorganises the way in which governments should think about concepts such as consumer choice, certification, and economic protections for distributors.

The traditional way for governments to control new technologies has been through licensing – however, the proliferation of internet-based devices (exemplified by the term, “Internet of Things”) and content makes it impossible to think of such a paradigm without imposing strict restraints on innovation and even infrastructure development. For instance, without the virtuous cycle of content consumption, wherein new content available over the internet spurs new consumption, there would not be any logic in expanding network infrastructure. Part of the problem in India’s universal broadband provisioning under its “BharatNet” programme has been the lack of emphasis on the demand side and the last mile.

Therefore, like many other jurisdictions, India will have to invest in regulatory capacity building, and new models of regulating converging industries. This does not mean that India should necessarily create the equivalent of a digital industrial policy, with inbuilt protections for domestic industry, as the European Commission is aiming to do through its Digital Single Market strategy.[xviii]Rather, multi-stakeholder consultations must be used to find the right answers. While a few regulators have begun using public consultations as a tool for gathering multi-stakeholder inputs, which has led to greater decisionmaking transparency, much more can be done to engage with civil society and industry on such issues on a dynamic basis. New regulatory models like co-regulation with industry and civil society, as pioneered by Australia, can allow the government to solve complex challenges and dynamically respond to technological changes.[xix]

In fact, there are several digital domains that are currently being governed by legacy institutions that are not necessarily equipped to do so. A far greater degree of strategic thought is needed before imposing reactive regulations. E-commerce is one such realm, which does not have a parent ministry, meaning that various aspects of it are governed by different institutions, with a lack of overall policy vision for the industry. To wit, issues related to FDI in ecommerce are dealt with by the Department of Industrial Policy and Promotion, those related to consumer protection are dealt with by the Ministry of Consumer Affairs, those related to the IT Act such as intermediary liability and personal data are dealt with by the Ministry for Electronics and IT, those related to taxes are dealt with by the Ministry of Finance, and issues related to logistics and movement of goods are dealt with by a bevy of departments at the central and state government levels. While this may make some degree of intuitive sense to the reader, the challenge is that owing to a lack of overall policy vision for the industry, different arms and bodies of government will pull it in separate directions. The consumer perspective for instance, may be divergent from the tax administrators’, which may in turn diverge from the industry perspective, leading to suboptimal policy-making and regulation.

There is an additional element that adds to policy uncertainty – which is the participation of government entities in markets, wherein they play the roles of both operator and regulator. For instance, the Indian government operates its own debit cards and payments instruments. This is the case even as a largely government-run entity, the National Payments Corporation of India, plays a role akin to a regulator’s in the digital payments space. This inconsistency has been pointed out by several experts, including a high-level government committee constituted in 2016.[xx]Such operator-regulator conflicts were also pointed out in the past, in other related areas, by the seminal Financial Sector Legislative Reforms Committee in 2013, which explicitly stated that India needs better regulation “to encourage independent payment system providers, which are not linked to payment participants, thereby minimising moral hazard through conflict of interest…”.[xxi]

The overarching challenge for government is to create requisite capacities to think holistically about new industries that are attracting high volumes of investments and are among the fastest growing digital sub-sectors.

Towards a New Formality

The increasing avenues of connectivity – including through mobile phones – provide an opportunity for India’s young and dynamic workforce to enhance its skills and “digital literacy”. This paper has also sought to highlight why the Indian government must undertake key regulatory reforms and build standards capacity, and why the private sector must invest in supply chains to promote “services-led” growth. However, the success and transformative potential of the digital economy in India is also tied to the inclusion and welfare of a new workforce. Thus the supply side needs to be looked at again.

A “new workforce”, could imply two things:first, aworkforce that is proficient in the digital economy sub-sectors; andsecond, a workforce that is digitally integrated into the development fold. The first element has been briefly discussed earlier. Taking up the second, to have a digitally integrated workforce, efforts are needed to bring previously excluded groups into the digital economy. This includes, in particular, women, who continue to face barriers to access and usage of digital technologies.

The digital economy has few parallels in governance, as it brings together a host of stakeholders who are invested quantitatively and qualitatively in its output. The “quantitative” output of a digital economy may be measured by indicators such as the number of successful businesses that constitute India’s nascent start-up ecosystem, the number of intellectual property (IP) applications filed annually, and the number of new consumers it draws into digital spaces. “Qualitative” aspects are less tangible, and therefore, more difficult to discern, even as they may be as important. Consider, for instance, the following question: will India’s workforce enjoy better standards of living and better work in the future?

Skills training and awareness schemes contribute directly to the capacities of the digital workforce. Similarly, the growing digital economy also contributes – in an organic fashion – to enhancing job prospects for a young and dynamic population. Regulatory reforms on areas like IP rights, net neutrality and competition, therefore, become all the more important as they will calibrate the consumption of knowledge by India’s digital workforce and create a new production economy in the digital sector. A key additional area for public and private sector partnerships and interventions will be the assurance of a greater degree of social security in the future.

It has been argued earlier that the private sector will play a crucial role in providing, through technological gateways, the “cover” that governments in the past offered to the formal sector – whether it is insurance, healthcare or other forms of financial inclusion. This act of providing formal social cover to the informal economy using digital devices, digital identity and digital last mile, is itself a new growth sector that can create new employment in services.”[xxii]Concomitantly, it is important that government does not regulate these technological gateways with a heavy hand, and applies an innovation-centric lens with requisite safeguards and constitutional principles in mind.

For instance, the financial sector, including banks and insurance firms, will likely be among the first-mover industries to use artificial intelligence and machine learning to enhance service delivery, and to develop innovative products that are highly individualised.[xxiii]This will require that government gives them enough regulatory space, through the use of instrumentalities such as regulatory sandboxes, and co-regulation. Government will also have to ensure, in concert with the private sector and some specialist civil society bodies, that standards-setting in such new service domains keeps up with international developments, so that the solutions derived in India are applicable elsewhere.

A formal job is characterised by welfare protections and legal oversight by the state. Conversely, according to the International Labour Organisation, the informal economy constitutes “workers and economic units that are – in law or in practice – not covered or insufficiently covered by formal arrangements. Their activities are not included in the law, which means that they are operating outside the formal reach of the law; or they are not covered in practice, which means that – although they are operating within the formal reach of the law, the law is not applied or not enforced; or the law discourages compliance because it is inappropriate, burdensome, or imposes excessive costs.”[xxiv]By implication, the ability of the state to provide welfare and regulate diversified sets of economic activities, will determine the future of formality in India if this conventional lens is used.

However, an unconventional, and as yet untested, version of a new formality could be developed in India’s case. This new formality could “essentially provide each worker with income security (minimum wages), availability of health, retirement and life insurance cover (critical needs), and safe and congenial working conditions (safety)”.[xxv]Informal workers can be offered this support only if value generation and innovation by the private sector are encouraged – therefore, if government can adopt a dynamic, consultative and light-touch approach and provide infrastructural support. As it moves towards a new context for formality of a young workforce, India can begin to construct qualitative benchmarks that can serve its purpose.

This is no doubt a contentious approach as it goes against the grain of most literature and views on informality, that suggest that nothing short of a transition from informal to formal is desirable. However, in India’s case, the expanding digital economy is going to lead to the technological mobilisation of the informal workforce at an absolute scale that may be unprecedented, creating an opportunity for inclusive growth. It is therefore argued that this may mirror some of the trends that the OECD countries, such as the US, saw in the early parts of the 20thcentury, wherein there was “greater mobilisation of the informal workforce alongside the positive effect on gender gap in employment”, with the advance of technology.[xxvi]Moreover, technology will help identify each worker, and assure the worker of the benchmarks for a new formality, through better targeting and flexible delivery.

Technology will also allow for a certain degree of cross-subsidisation, as higher-end users will underwrite lower-end usage, as is being done in the case of the telecom sector’s infrastructure development (wherein higher-end users are paying many multiples of what the large base of the user-pyramid is paying per unit of data consumed). It is worth reiterating that the government will therefore have to ensure that the private sector is allowed to generate surpluses that can be reinvested in new infrastructure for targeting and delivery.

The relationship between India’s digital workforce and the digital economy is clearly symbiotic. Multi-stakeholder models of governance must account for India’s unique developmental concerns – especially the need to absorb communities at the margins into the economic mainstream – as they deliberate and implement digital economy policies. For state and central governments, as well as regulators, the twin goals of promoting affordable digital connectivity while ensuring healthy competition in the digital market is therefore important. The Indian state is wont to regulation, but the digital economy requires a nimble approach. Understanding that policies will not only affect economic output but also shape the skills and welfare of the digital workforce in the long run, is essential. The growth in India’s services sector, for the most part of the last two decades, has been organic – it has been shaped by the skills and knowledge of educated Indians. The digital economy holds the potential to further facilitate this flow of knowledge, and thereby absorb hundreds of thousands of Indians as effective contributors to the country’s workforce.

Conclusion

It is clear from the preceding sections that India requires a balanced approach to harness the potential of the digital economy. India’s unique workforce is young, under-skilled and largely informal. Appropriate focus is needed on both the supply side and demand side considerations outlined here. The services sector will have to be at the centre of this demand-supply matchmaking – given its structural importance in the economy, the prospects of greater integration with various value chains, and potential for job creation. This will require greater supply chain efficiency and improved standards. The scale of the challenge is daunting and exciting at the same time. It reflects an opportunity to upgrade supply chains, industrial and regulatory efficiencies, and of course, the young, under-skilled and informal workforce.

Specific recommendations towards this include the following:

Servicing ‘Make in India’: The Indian government’s flagship ‘Make in India’ policy of promoting indigenous manufacturing is premised on the assumption that there is no alternative for large scale employment generation. However, given that the services economy is an intrinsic part of manufacturing processes, and that there is an increasing “servicification” of trade globally, policy-makers must consider adding a strong service component to this policy vision. One concrete step towards this could be to build private sector awareness about the importance of supply chain standards, and for the government to develop a large range of service sector standards. Requisite infrastructure expansion (including digital infrastructure) will also have to accompany this focus, and so will forward and backward integration into GVCs.

Policy Stability and Innovation Centricity by Design:The Indian government will have to get serious about stability in policies and regulations, particularly those targeted at industries and sectors that constitute the digital economy. In practice, this would mean that India must conceive of a long-term digital economy vision, which balances imperatives of public access, innovation and growth, in a way that is fundamentally different from how this balancing act has panned out for traditional sectors that are no longer competitive in the global economy context. Regulatory institutions will also need to build capacities to scale with the digital economy, and will need to adopt a nuanced, light-touch approach as new markets develop. Towards this, there is no substitute to establishing inclusive multi-stakeholder processes, such as co-regulation, and regulatory sandboxes, that can also help counteract any hasty decisions.

Policy processes must also respond to uniquely Indian conditions. India’s expanding digital economy will touch many areas that are unregulated. The temptation of burdening such areas with adapted templates from legacy regulations and licensing frameworks will have to be resisted. These areas would include critical aspects such as data protection or regulation of services delivered through the internet. Policy-makers and regulators will have to juxtapose the imperatives of creating reasonable safeguards for citizens, preserving national security and institutions, with the need to propel innovation that can underwrite future infrastructure as well as generate the conditions for a new formality of the Indian workforce. India’s integration with regional value chains and GVCs will also be premised on this.

Reimagining the Digital Workforce:In 2009, the erstwhile government had set a skill development target of training 500 million people by 2022. The approach was premised on private sector participation. Many years since, the Modi government has actualised a new skill development policy with a similar private-sector oriented approach. Indeed, it is here that the large private sector’s intervention is desperately needed, and the government must allow for it to have the bandwidth to respond. For instance, the private sector has historically under-invested in preparing workers for responding to global supply chain standards. The result has been an inability to cope with new norms and compete in GVCs. The government has a role to play in reversing this vicious cycle, by allowing for creation of surplus value that can be reinvested in capacity building of workers, through adaptive learning and other available means discussed earlier.

Overall, a new approach is required to address new challenges linked to the future of the Indian workforce, and improving both quantitative and qualitative benchmarks through which future “work” itself is measured. India must adopt a policy approach that is holistic. It cannot afford anything less at this critical stage in its development trajectory, where there is a clear risk of institutions, and the overall political and administrative machinery, being overwhelmed by the sheer scale of the employment challenge. This means giving space to multiple stakeholders, fresh perspectives, and as inclusive a policy approach as possible, without diluting the impetus for an urgent response.

About The Authors

Samir Saranis Vice President of the Observer Research Foundation, New Delhi. He spearheads ORF’s outreach and business development activities. He curatesRaisina Dialogue, India’s annual flagship platform on geopolitics and geoeconomics, and chairsCyFy, India’s annual conference on cyber security and internet governance. His academic publications includeIndia’s Climate Change Identity: Between Reality and Perception(Palgrave 2016); “New Norms for a Digital Society” (ORF Special Report, 2016); and “India’s Contemporary Plurilateralism” inOxford University Press Handbook on India’s Foreign Policy(2016). Samir’s doctoral studies were on Indian attitudes towards climate change at the Global Sustainability Institute, UK. He is Commissioner, The Global Commission on the Stability of Cyberspace, and member of the South Asia advisory board of the World Economic Forum.

Vivan Sharanis a Partner at the Koan Advisory Group, New Delhi. He is an economist with diverse experience in the policy circuit. He has previously served as the Chief Executive of the Global Governance programme at the Observer Research Foundation (ORF), and as the Business Head of a sustainability company that ran India’s first energy efficiency index on the Bombay Stock Exchange. His subject interests include technology, markets, and competition. He is a Visiting Fellow at ORF where he is involved with research on the digital economy and is a Member of the National Committee on Media & Entertainment, constituted by the Confederation of Indian Industry.

Endnotes

[i]Shwab, Klaus, “The Fourth Industrial Revolution”, World Economic Forum, 2016

[ii]The EU’s Growth Potential vis-à-vis a Shrinking Workforce by Dr Jorg Peschner, EU Dialogue on International Migration and Mobility: Matching Economic Migration with Labour Market Needs, Brussels, 24 February 2014, European Commission paper,http://www.oecd.org/els/mig/Peschner.pdf

[iv]Human Resources and Skill Requirement in the IT and ITeS Sector (2013-17, 2017-22) KPMG, for Government of India, Ministry of Skill Development and Entrepreneurship and National Skill Development Councilhttp://www.ugc.ac.in/skill/SectorReport/IT%20and%20ITeS.pdf

[viii]Defining Broadband: Minimum Threshold Speeds and Broadband Policy by Lenard g. Kruger, 04 December 2017, Congressional Research Service,https://fas.org/sgp/crs/misc/R45039.pdf

[xxii]In a Chapter on “The Future of Work”, in “Beyond Shifting Wealth: Perspectives on Development Risks and Opportunities from the Global South”, OECD, 2017

The views expressed above belong to the author(s). ORF research and analyses now available on Telegram! Click here to access our curated content — blogs, longforms and interviews.

Samir Saran is the President of the Observer Research Foundation (ORF), India’s premier think tank, headquartered in New Delhi with affiliates in North America and ...

Vivan was a visiting fellow at ORF, where he supports programmes on the ‘new economy’. Previously, as the CEO of ORF’s Global Governance Initiative, he ...

PDF Download

PDF Download