The African continental free trade area and its implications for India-Africa trade

Abhishek Mishra

The African countries are set to launch the African Continental Free Trade Area or AfCFTA, the biggest free trade agreement in the world since the World Trade Organization was created in the 1990s. When implemented, the AfCFTA is projected to increase intra-African trade by 52.3 percent by 2022, from 2010 levels. In turn, higher trade levels can facilitate economic growth, transform domestic economies, and help the countries achieve the Sustainable Development Goals (SDGs). This paper analyses the AfCFTA in the context of the continent’s long history of efforts at regional integration. It also examines the potential impact of the AfCFTA on India-Africa trade and bilateral investments, and argues that India must actively support the African efforts for AfCFTA.

Introduction

The vision of “pan-Africanism” and “collective self-reliance” has long been an integral component of attempts by African leaders and policymakers to find Africa-driven solutions to African problems. However, due to weak political, economic and governance structures, these attempts have largely failed to facilitate a structural transformation of the continent and today, the African nations continue to be fragmented economies working in isolation. Therefore, in order to achieve an African resurgence, virtually all the African countries have embraced the notion of “regionalism” and “regional integration” as part of their broader aspirations towards continental integration.[i] Over the years, various pan-African organisations have been working towards deepening economic, social and political integration in Africa.[ii]

One such attempt was made at the 18th ordinary session of the African Union (AU), held in Addis Ababa in January 2012, with a decision to launch a Continental Free Trade Area (CFTA) by 2017. This was followed by eight rounds of negotiations between 2015 and 2017. A major breakthrough was achieved on 21 March 2018 when leaders from 44 African countries met in Kigali, Rwanda, and signed a framework agreement to establish what is being called one of the world’s largest trade blocs.[iii] The agreement declared that the African Continental Free Trade Area (AfCFTA) would “come into effect 30 days after ratification by the parliaments of at least 22 countries. Each country has 120 days after signing the framework to ratify the agreement”.[iv]

The first section of this paper discusses the objectives of the CFTA agreement and its expected benefits for the African countries. The second section describes the history of African regional integration efforts and the establishment of Regional Economic Communities (RECs) over the past decades. The third section highlights the status of intra-African trade within the eight officially recognised RECs by the African Union using the 2016 African Regional Integration Index report as reference. The fourth section charts out the earlier African initiatives aimed at enhancing regional integration, such as the New Partnership for African Development 2002, Minimum Integration Programme 2009, Boosting Intra-African Trade 2012, and Tripartite Free Trade Area 2015. The fifth section explains the opportunities for and challenges facing the AfCFTA agreement. The sixth section examines current trends in India-Africa trade and the potential impact of the AfCFTA agreement.

1. Aims and objectives of AfCFTA

The CFTA is an attempt by the African governments to “unlock Africa’s tremendous potential” to deliver prosperity to all Africans.[v] It seeks to create a single continental market for goods and services with free movement of business people and investments.[vi] By 2030, the African market size is expected to reach 1.7 billion people, with a combined and cumulative consumer and business spending of US$6.7 trillion.[vii]

The CFTA aims to expand intra-African trade through better harmonisation and coordination of trade liberalisation and facilitation regimes and instruments across subregions (RECs) and at the continental level.[viii] As part of the agreement, “countries have committed to remove tariffs on 90 percent of goods with the remaining 10 percent of items to be phased in at a later stage”.[ix]

A study by the UN Economic Commission for Africa (UNECA) estimates that successful completion and implementation of the CFTA agreement – complemented with efforts to improve trade-related infrastructure, reduced import duties and transit costs – could lead to a 52.3 percent increase in intra-African trade by 2022, from the 2010 levels. The figures are expected to double upon further removal of non-tariff barriers.[x] An increase in intra-African trade will “drive the structural transformation of economies from low productivity and labour intensive activities to higher productivity and skills intensive industrial and service activities”.[xi] This will subsequently help in generating better paid jobs, leading to poverty alleviation.

The AfCFTA also seeks to “foster a competitive manufacturing sector and promote economic diversification”.[xii] At present, manufacturing represents only about 10 percent of the total GDP in Africa, on average, lagging behind other developing nations.[xiii] Given the CFTA’s enormous “market size of 1.2 billion people and over $3.4 trillion of cumulative GDP”, if implemented properly, the CFTA could reduce this gap by increasing growth in the manufacturing sector and its value added products.[xiv]

Prof. Landry Signé of the Stanford University’s Centre for African Studies says that “the continental free trade area is expected to offer substantial opportunities for industrialisation, diversification and high skilled employment”.[xv] He further says that such a market would also “offer the opportunity to accelerate the manufacture and intra-African trade of value-added products, moving from commodity based economies and exports to economic diversification and high-valued exports”.[xvi]

2. Africa’s regional integration efforts: A brief history

At the time of independence, individual African countries were divided, fragmented and were unable to capitalise on their vast wealth of natural resources. They lagged behind the rest of the world in growth and development. In an attempt to address these challenges, the African nations and their leaders affirmed their resolve to work towards sub-regional and regional integration of the continent. Consequently, the concept of “regionalism” gained traction and the African countries embraced regional integration as an important component in their development strategies.

Although such aspirations gave rise to ideals such as “pan-Africanism” and “collective self-reliance”, there were varying notions amongst the African countries. Two schools of thought emerged: the “Casablanca school” that wanted to create a federation of all African countries, with a few powers being transferred from the national governments to a pan-African authority; and the “Monrovia school” that supported gradual unity through economic cooperation, and wherein each nation would have full control over its decisions.

According to Winters (1996), regional integration or ‘regionalism” is “any policy designed to reduce trade barriers between a subset of countries regardless of whether those countries are actually contiguous or even close to each other”.[xvii] Tanyanyiwa and Hakuna (2014) define regional integration as “the formation of closer economic linkages among countries that are geographically near each other especially by forming Preferential Trade Agreements (PTAs)”.[xviii]

Regional economic integration means the following:

Free movement of goods, services, people and capital between national markets.

More robust, equitable economic growth.

Elimination of poverty and reduction in unemployment.

Increase in competition in global trade and improvement in access to foreign technology, investment and ideas.[xix]

Integration of small landlocked African countries, connecting them to a much larger, deeper regional and global market. Tuluy (2017) argues that “the need for scale and market consolidation is particularly relevant for African countries, many of which are small, landlocked economies with small populations”.[xx] Mello and Tsikata (2015) state that “African Regional Economic Communities (RECs) have pursued the ‘linear model’ of integration with a stepwise integration of goods, labour and capital markets, as well as eventual monetary and fiscal integration”.[xxi]

Early integration efforts: the Economic Commission for Africa

The first step towards continental integration was the establishment of the Economic Commission for Africa (ECA) by the United Nations Economic and Social Council (ECOSOC) in 1958. The ECA worked with partners and member states to achieve sustainable development, poverty alleviation, good governance and promote international cooperation for Africa’s development.

It was believed that the years of colonialism had weakened the continent socially, politically and economically.[xxii] This belief led to the establishment of the Organisation of African Unity (OAU) in 1963 to promote unity and solidarity amongst the African states and to act as a collective and cohesive mechanism for the continent. The OAU continued to work as an inter-governmental organisation, rather than as a supra-national body. Parallel to the creation of OAU, the African Development Bank Group (AfDB) was established in 1963 after an agreement was signed by 23 founding member states in Khartoum, Sudan.[xxiii] The group includes two other entities with AfDB as the parent institution: African Development Fund and Nigeria Trust Fund. The main work of the AfDB is to “mobilise and allocate resources for investments in member states and provide policy advice and technical assistance that supports development efforts in the continent”.[xxiv]

One of the earliest proponents of Africa’s political and regional unity is the Nigerian economist Prof Adebayo Adedeji who served as executive secretary of the ECA for 16 years (1975-1991). He worked to identify solutions to Africa’s developmental challenges from within the continent, particularly to reverse the damaging effects of the Structural Adjustment Programmes (SAPs) imposed on the continent in the 1980s, by conceiving the African Alternative Framework for Structural Adjustment Programmes (AAF-SAP). Prof Adedeji championed the cause of pan-African integration and his efforts led to the establishment or re-establishment of a host of regional integration agreements. This took place in two waves: the first between mid-1970s to early 1980s and the second during the first half of the 1990s.

The Lagos Plan of Action and the first wave of RECs

The EAC and OAU adopted the Lagos Plan of Action (LPA) in 1980 at the OAU Extraordinary Summit in Lagos, Nigeria. According to Trudi Hatzernburg (2011), the aspirations of the African leaders to integrate Africa provided the rationale for the LPA.[xxv] The LPA, together with the Final Act of Lagos (FAL), aimed to establish an African social order by utilising the continent’s resources to build a self-reliant economy. The plan also charted a roadmap towards establishing an African Economic Community (AEC) by the year 2000.

The LPA envisioned four agreements at the subregional levels, which would ultimately move towards developing a regionally integrated Africa. These were: Economic Community of West African States (ECOWAS), Preferential Trade Area (PTA) for the Common Market for Eastern and Southern Africa (COMESA), Economic Community of Central African States (ECCAS), and Arab Maghreb Union (UMA). (See Annexure for more information on these RECs).

The Abuja Treaty and the second wave of RECs

The second wave of the RECs began in 1991, when the African heads of state and government signed the Abuja Treaty. At the continental level, the treaty aimed to establish an AEC gradually by the end of six successive phases. The rationale behind the six-phased approach was to ensure consolidation of the integration vision, first at the regional level, through creating and strengthening the RECs, which would then eventually merge into the African Economic Community.[xxvi]

During this period, various other RECs were established, namely, South African Development Communit

Six phases towards an African Economic Community (AEC)

Phases

Years

Aims

First

1994-1999

Strengthen existing RECs and establish new RECs in regions where they did not exist previously, stabilise tariff barriers, non-tariff barriers, customs duty and internal taxes in each REC.

Second

1999-2007

Harmonise custom duties and strengthen sector integration.

Third

2007-2017

Establish a Free Trade Area (FTA) and customs union in each REC.

Fourth

2017-2019

Coordinate and harmonise tariff and non-tariff systems leading to a continental customs union, common sector policies and harmonise monetary, financial and fiscal policies.

Fifth

2019-2023

Free movement of persons and right of residence and establishment of African common market and pan-African economic and monetary union.

Sixth

2023-2028

Establish an African central bank, Pan-African parliament and develop African multinational enterprises.

(SADC), Intergovernmental Authority on Development (IGAD), Community of Sahel-Saharan States (CEN-SAD) and East African Community (EAC) (see annexure for more information on these RECs).

Sirte Declaration and the African Union (AU)

During this period, the leaders of the African nations saw it fit to re-examine the OAU charter in order to align it with the Abuja Treaty. Therefore, at the fourth extraordinary summit of the OAU held in Sirte, Libya, on 9 September 1999, the heads of state and government called for the establishment of an African Union (AU) in conformity with the ultimate objectives of the OAU charter and the Abuja Treaty provisions.

This led to the Constitutive Act of the African Union in Lome, Togo, in July 2000. At the thirty-seventh session of the assembly of the heads of state and government in 2001, in Lusaka, Zambia, a transition period of one year was agreed during which various consultations took place before the inaugural launch of the African Union in Durban, South Africa, on 9 July 9 2002.

Status of Intra-African trade under various RECs

The eight AU-recognised RECs are at different stages of and progress in the integration process. The Africa Regional Integration Index (ARII) developed by the UNECA, AfDB and AU recognises five indicators of regional integration through which progress among the African RECs is measured. These indicators are: trade integration, regional infrastructure, productive integration, free movement of people and financial and macroeconomic integration.[xxvii] Individual country scores on each dimension are ranked on a scale of 0 to 1.

Table 1: African Regional Integration Index, 2016

Regional Economic Community

Trade Integration

Regional Infrastructure

Productive Integration

Free Movement of People

Financial and Macroeconomic Integration

CEN-SAD

0.353

0.251

0.247

0.479

0.524

COMESA

0.572

0.439

0.452

0.268

0.343

EAC

0.780

0.496

0.553

0.715

0.156

ECCAS

0.526

0.451

0.293

0.400

0.599

ECOWAS

0.442

0.426

0.265

0.800

0.611

IGAD

0.505

0.630

0.434

0.454

0.221

SADC

0.508

0.502

0.350

0.530

0.397

UMA

0.631

0.491

0.481

0.493

0.199

Average of Eight RECs

0.540

0.461

0.384

0.517

0.381

Source: Africa Regional Integration Index Report, 2016

Based on Table 1, it is clear that the overall regional integration score for the ‘trade integration’ dimension (0.540) is the highest among the RECs. On the other hand, it is lowest for ‘financial and macroeconomic’.

In ‘trade integration’, the East African Community (EAC) scores the most (0.780) while the Community of Sahel-Saharan States (CEN-SAD) scores the least (0.353). In ‘productive integration’, the EAC again tops (0.553) the list while the CEN-SAD is at the bottom (0.247). In ‘free movement of people’, the Economic Community of West African States (ECOWAS) is the most integrated one with a score of 0.800 and the Common Market for Eastern and Southern Africa (COMESA) is the least with a score of 0.268.

It can be concluded that the African RECs are making noticeable progress towards integration. While some are ahead of others, they are all headed towards greater regional integration.[xxviii]

3. Intra-African Trade Initiatives

Based on available data, it is clear that Africa has immense potential for increasing the level of intra-African trade, both within the RECs and throughout the continent. A number of African initiatives aimed at accelerating the process towards regional and continental integration have been adopted in recent years.

New Partnership for Africa’s Development (NEPAD)

The New Partnership for Africa Development (NEPAD) is an example of an African initiative with a continent-wide focus. It was ratified by the AU in 2002 and provides a comprehensive integrated development strategy to bring about a holistic socio-economic development of Africa. The NEPAD aims to transform Africa’s relationship with its development partners to replace the ineffective, patronage and tied-aid transfers from Africa’s northern partners.

The African Free trade Zone (AFTZ)

The African Free Trade Zone (AFTZ), also known as the African Free Trade Area, was announced at the EAC-SADC-COMESA Summit in October 2008. In May 2012, the agreement was extended to include ECOWAS, ECCAS and AMU to operationalise an African Free Trade Zone by 2018. The agreement marked a milestone in Africa’s journey towards regional and continental integration as, for the first time a truly transcontinental union from north to south was established.

Minimum Integration Programme (MIP)

In 2009, the AUC along with the RECs signed the Minimum Integration Programme (MIP) as a mechanism for convergence among the RECs to focus on key areas of concern, both at the regional and continental levels. The MIP “embodies the activities of the project and the programmes which require quick implementation in order to speed up and ensure the successful completion of regional and continental integration process”.[xxix] It works on “variable geometry” approach in integration, according to which the RECs are expected to integrate at varying pace. Therefore, the RECs are required to identify and implement their own priority programmes while working on other activities under the MIP.

Boosting Intra-African Trade (BITA)

The African Union (AU) Heads of State and Government Summit, held in January 2011, decided to hold the next summit in 2012 under the theme of “boosting intra-African trade” to deepen Africa’s market integration and significantly increase the volume of intra-African trade. An action plan was drafted to “enhance the levels of intra-African trade from current levels of 10-13 percent to 25 percent or above within the next decade”.[xxx] In order to tackle the obstacles to the intra-African trade, the action plan outlines seven priority clusters: trade policy, trade facilitation, productive capacity, trade-related infrastructure, trade finance, trade information and factor market integration.

Tripartite Free Trade Area (TFTA)

A breakthrough in Africa’s journey towards regional and continental integration was achieved when the Heads of State and Government of COMESA-EAC-SADC met on 10 June 2015 in Sharm El Sheikh, Egypt, to launch the Tripartite Free Trade Area (TFTA). Its launch demonstrated the possibility of a collective action among several heterogeneous nations and showcased the feasibility of harmonising three different preferential trade regimes into one unified scheme. When fully implemented, the TFTA is expected to create a large market with 626 million customers (about eight percent of the world’s population), along with an emerging middle class.[xxxi]

South African Customs Union (SACU) 1910, 1969 and 2002

The SACU is one of world’s oldest customs unions.[xxxii] The 1910 SACU agreement, which lasted till 1969, agreed on a “Common External Tariff (CET) on all goods imported into the union from the rest of the world and a common pool of customs duties”.[xxxiii] It also included provisions for free movement of SACU manufactured products within SACU and revenue-sharing formula (RSF) for the distribution of customs and excise revenues.[xxxiv] The 1969 agreement extended the provisions to included excise duties in the revenue pool and a multiplier in the RSF. The final SACU 2002 agreement aimed to implement a joint decision-making process by establishing an independent administrative secretariat, a customs union commission, technical liaison committee, an ad-hoc SACU tribunal and SACU tariff board. The RSF was revised to include customs excise and a development component.

Single African Air Transport Market (SAATM)

A number of other initiatives aimed at regional and continental integration in Africa have also been taken. The Single African Air Transport Market (SAATM), a ‘flagship project of AU under Agenda 2063’ aims at “creating a single unified air transport market in Africa and liberalise civil aviation in Africa”.[xxxv] Signed in 2015, the agreement is based on the implementation of the Yamoussoukro Decision of 1999 and is aimed at establishing a single air transport market by 2017. In January 2018, 23 African countries launched SAATM initiative to “enhance connectivity between African nations and reduce flight ticket prices”.[xxxvi]

Relaxing Visa rules

A number of African countries have worked towards relaxing visa rules and issuing visa on arrival.[xxxvii] Countries such as Seychelles, Niger, Namibia, Kenya and Ghana have been leading the way in this regard. Although the AU has launched an electronic pan-African passport, it is only available for a few government officials at present. The African countries need to ensure easy procurement of visas, reduction in costs of flights, reduction in high airport taxes and fees and facilitate open air routes to boost travel across the continent.

4. Opportunities and Challenges for AfCFTA

The AfCFTA provides an important opportunity for the African countries in an increasingly globalised world. The elimination of tariffs in goods and services will help in boosting economic growth of the African countries, transform their economies and achieve sustainable development goals (SDGs). Furthermore, if the non-tariff barriers to trade in goods and services are addressed and if the informal trade is integrated into the formal channels, the benefits accruing from the CFTA will be even greater. The following are some of the potential benefits of AfCFTA:

A bigger and integrated regional market for African products.

Improved conditions for forming regional value chains (RVCs) and integration to global value chains (GVCs).

Consumer access to cheaper imported products from other African countries.

Benefits to producers from economies of scale and access to cheap raw materials.

Better allocation of resources leading to faster economic growth.

Higher intra-African and external direct capital flows to African countries.

Elimination of challenges associated with multiple and overlapping trade agreements.

The structural transformation of the African countries from resource and low technology-based economies to more diversified, knowledge-based economies.

Stronger cooperation in other areas, such as technology transfer, investment, innovation and continent wide infrastructure development.[xxxviii]

Although, the CFTA offers numerous opportunities for attaining sustainable development, there are formidable challenges facing the participating member states.

Firstly, the share of intra-African trade in the total African trade is small, around 11.3 percent in 2011 which increased to 14 percent in 2013.[xxxix] These numbers show that “intra-African aggregate trade and share in total African trade is low as compared to other parts of the world, such as Asia, Latin America etc.” [xl] Therefore, the African countries need to ensure that a cohesive policy framework is in place which includes the Rules of Origin (RoO) compatible with the African productive capacity needs. In the build-up to the negotiations, there appeared to be a divide between the francophone western Africa and the southern and eastern Africa on the question of RoO. The western and central African countries preferred more general rules of origin, whereas countries like Kenya, South Africa and Egypt were pushing for more restrictive rules of origin (i.e. product specific list of rules). South Africa was in favour of using the SADC RoO model as the basis for the AfCFTA rules. In the end, the negotiators reached a compromise which includes general rules with the exceptions for 843 specific tariff lines.[xli]

Secondly, analysts hypothesise that the trade growth and welfare benefits from the CFTA are likely to “accrue unevenly among African countries”.[xlii] Countries with stronger supply capacity and competitiveness will be able to capture larger portions of the benefits and trade growth. This is reinforced by the fact that at present seven African countries account for more than “60 percent of total intra-merchandised exports while the majority African countries account for the remaining 40 percent”.[xliii] Small landlocked countries and small economies fear tariff cuts in the form of fiscal revenue loss and destruction of local economies.

Therefore, the CFTA agreement should factor in inclusiveness and reflect a mutually inclusive agreement beneficial for all African countries. This calls for a ‘bottom-up’ approach to identify, at the disaggregate level, what is currently effective, what was effective in the past or somewhere else, and could be effective in Africa without any inordinate effort.[xliv] The governments can help to address the impediments that they themselves identify as crucial to the success of the CFTA. The governments, private sector, international organisations and civil society can engage in an exchange of ideas, information and resources that can build a market-friendly and development-oriented collaboration. A ‘rules-based’ governance system and an ‘institutional architecture’ are necessary to foster harmonisation, consistency and predictability.[xlv]

The solutions to these challenges are, however, more political and less economic; the leaders should exhibit political will.

Thirdly, Nigeria – Africa’s largest economy and most populous country – has refused to sign the CFTA agreement. It was one of the earliest champions of this move but has deferred signing it on the plea that it needs more time for domestic consultations. The Nigerian Labour Congress (NLC), an umbrella organisation of trade unions, has termed the agreement as a “renewed, extremely dangerous and radioactive neo-liberal policy initiative”.[xlvi] The general view among the labour unions and industry bodies is that Nigeria’s export capacity in the non-oil sectors is not robust enough to be exposed to external competition.

Finally, the CFTA agreement needs to work out complementary policies in a number of diverse areas, such as market access to goods and services, competition policy, dispute settlement mechanisms, intellectual property and unfair trade practices.[xlvii] The negotiating process should also be given due consideration. Regional organisations such as UNCTAD must work with the AU Commission and individual countries to ensure successful completion of the negotiating process.

So far, 49 African countries have signed the AfCFTA framework but only seven – Kenya, Ghana, Rwanda, Niger, Chad, eSwatini and Guinea – have ratified it. The AfCFTA will officially come into force once it is ratified by at least 22 countries.[xlviii]

5. India-Africa trade and investment cooperation

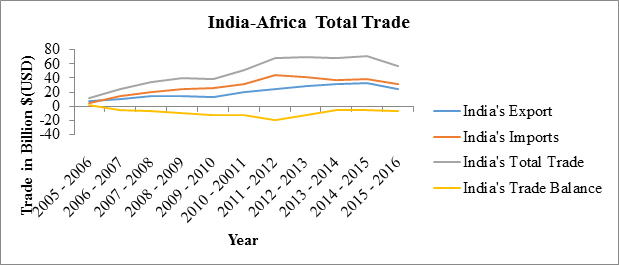

Since 2000, the economic cooperation between India and Africa has increased, helped by the India-Africa Forum Summit (IAFS) process. Both the regions have worked closely and engaged constructively with each other. The synergy that exists between India and Africa can be gauged from the robust trends in trade relations, wherein bilateral trade has increased five-fold in a decade – from $11.9 billion in 2005-06 to $56.7 billion in 2015-16.

India’s overall trade including exports, imports and trade balance with Africa from 2005 to 2016 has been given in Graph – 1 (for details see table 2 in annexure).

Graph – 1

Source: Data collected from Ministry of Commerce and Industry (MOCI), Government of India; and EXIM Bank Analysis and graph designed by the author

Graph-1 shows that India’s exports to Africa increased almost four-fold – from $7 billion in 2005-06 to $25 billion in 2015-16 – accounting for 9.5 percent share in India’s total exports. India’s imports from Africa during the same period increased seven-fold from – from $4.9 billion to $31.7 billion – accounting for 8.3 percent share in India’s total imports. India’s imports from Africa grew at an annual average of 29.8 percent while its exports to Africa grew at an annual average of 15.9 percent.

However, the recent trends show a steady decline in the India-Africa trade in both actual and comparative terms from 2013 to 2017. In 2014-2015, the total India-Africa trade stood at US$71.5 billion, which went down to US$56.7 billion in 2016-2016 (see Table 2 in annexure) and has further dropped to US$51.96 billion in 2016-2017.[xlix]

The balance of trade has also shifted in favour of Africa. India had a surplus of US$2.1 billion in 2005-06, which turned into a deficit of US$6.6 billion in 2015-16. India’s negative trade balance is mainly because of its high demand for oil and energy resources. Interestingly, India’s exports to the African countries have also been dominated by petroleum products. Therefore, in order to correct the trade imbalance, India needs to expand and diversify its export basket to include both primary and manufactured goods.

As for India’s investments in Africa, there has been an upsurge in recent years, mainly due to high-growth in some of the African markets and their mineral rich reserves. The Indian Multi National Enterprises (MNEs) have ventured into various sectors of investments spanning telecommunications, energy, computer sciences, power and automobile, among others. According to data from the Ministry of Finance, the Government of India and Reserve Bank of India approved a cumulative investment of US$54 million in Africa between 1996 and 2016 – nearly one-fifth of India’s overseas direct investments. The major destinations of such investments were Mauritius, Mozambique, Sudan, Egypt and South Africa (for more on India’s approved overseas direct investments in Africa and FDI Equity inflows from Africa to India, see Tables 3 and 4 in Annexure).

However, just as in the trade, India’s investments in Africa have witnessed a slump since 2013. According to the World Investment Report 2018 of the UNCTAD, Indian FDI in Africa stood at $14 billion in 2016-2017, which is lower than $16 billion in 2011-12. One of the reasons for this is that apart from India’s traditional investors, few companies are looking at the continent with any degree of seriousness. An increase in the Government of India’s Lines of Credits (LOCs) to the African continent is not matched by a similar increase in investments by the private and public sectors.

In spite of such realities, there exists an enormous potential for improving the India-Africa trade and investment partnerships if the AfCFTA comes into force.

AfCFTA and its impact on India-Africa trade

The AfCFTA will provide a number of opportunities for the Indian firms and investors to tap into a larger, unified, simplified and more robust African market. It is critical for India to view Africa not just as a destination for short-term returns but as a partner for medium and long-term economic growth.

An important component affecting the volumes of trade with Africa is the “third-country fabric” provision. Various Asian countries’ traders and investors, including those from India, are reaching out to the African markets as a market of “choice”. This is often perceived as a way to indirectly take advantage of the preferential trade programmes offered to the African countries by the third parties. A case in point is the African growth and Opportunities Act (AGOA) of the US, under which some African countries are eligible to source raw materials from third countries like India and China, to make clothes and then export to US duty-free. Such provisions help to shield African industries such as textiles and apparel, which have benefitted from huge amounts of Indian and Chinese investments in African export processing zones.

Therefore, to establish a long-term partnership with Africa, India should not target African markets only for its unilateral preferences granted by the third parties.

In terms of the possible trade diversion effects of the AfCFTA, a recent study of the Economic Commission for Africa (ECA) by Mevel and Mathieu (2016) projected that the African countries would be adversely affected by the signing of the Mega Regional Trade Agreements (MRTAs) due to erosion of preferences and increased competition in the MRTA markets.

MRTA’s are a recent phenomenon where countries or regions with a major share of world trade and foreign direct investment (FDI) join together and form deep-integration partnerships, with the aims of increasing trade links, improving regulatory compatibility, and providing a rules-based framework for working out differences. The best examples of MRTAs are the Trans-Pacific Partnership (TPP), the Transatlantic Trade and Investment Partnership (TTIP), and the Regional Comprehensive Economic Partnership (RCEP) which bring together Australia, Japan, China, India, Korea, New Zealand and ten countries of the Association of Southeast Asian Nations (ASEAN).

If the RCEP is established, there will be an increase in intra-RCEP trade, as its member countries will be more inclined to trade amongst themselves. This will act as a detriment to third countries, i.e. India and African countries, whose export shares towards RCEP member countries will decrease. The total exports from Africa would decrease by about US$3 billion by 2022 as compared to a situation without MRTAs.[l]The following are the main findings of the study:

Exports from Africa towards the Regional Comprehensive Economic Partnership (RCEP) countries will decrease sharply by nearly US$11 billion.

Exports from Africa towards other areas outside RCEP countries will increase by US$8 billion.

Exports from Africa to the European Union will increase by US$1.5 billion.

Exports from Africa to the US will increase by US$2.5 billion.

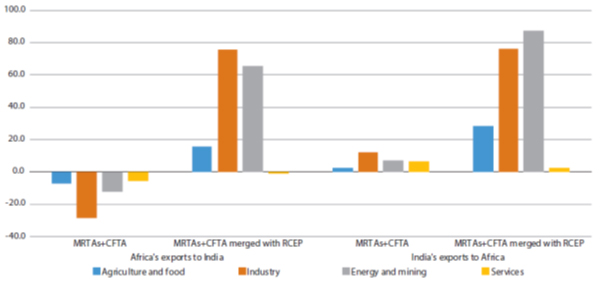

Figure 1: African exports to India and Indian exports to Africa following mega-regional trade agreements 2022 (%)

Source: Mevel and Mathieu (2016)

A 2018 joint report by the UNECA and Confederation of Indian Industries (CII)[li] also provides some key findings:

Total African exports will decrease by US$3 billion if the MRTAs are established outside Africa, especially the RCEP.

African exports will increase by US$27.5 billion by 2022 if the AfCFTA is established in parallel with other MRTAs.

This surge in exports will be driven primarily by the increased intra-African trade which is expected to progress by US$40.6 billion (39.9 percent) while the African exports will decline everywhere else.

Indian exports to Africa will increase by US$5.7 billion (13.2 percent) if the MRTAs are established.

Indian exports to Africa will increase by US$4.3 billion (10 percent) following the establishment of the AfCFTA.

The above findings project that following the establishment of the AfCFTA, the India-Africa trade relations will be marginally affected, as opposed to being negatively affected after the creation of the MRTAs, especially the RCEP. This is demonstrated in Figure 1.

However, it is important to note that a bulk of the African exports to India consist of energy and mining products. Since there is less domestic demand for these products, the African countries are redirecting exports of these products from India, and to some extent from China, to the European Union and the US where they are able to maintain their preference margins.

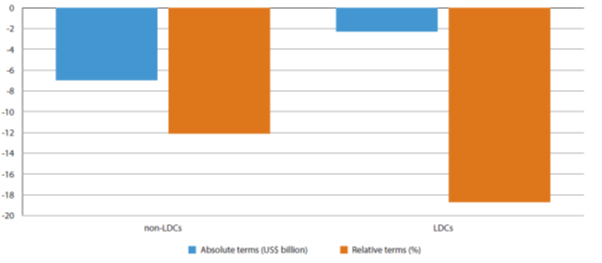

As Africa’s exports to India will decrease following the establishment of the RCEP, Africa can look to its internal markets to offset a part of its trade losses. In absolute terms, this drop in the total amount of African exports to India will be the largest among the non-least developing countries (non-LDCs), amounting to three quarters of the total amount or US$7 billion (see Figure 2).[lii] In relative terms, the exports from the African least developing countries (LDCs) to India will experience a bigger setback with a decrease by 18.7 percent as compared to a 12.1 percent decrease in export from the non-LDCs.[liii] Therefore, if the RCEP is established it will undermine the trade benefits extended to the African LDCs under India’s Duty Free Tariff Preference (DFTP) scheme for the LDCs.

Figure 2: Exports to India from African non-LDCs vs. African LDCs following the establishment of MRTAs, relative to the baseline, 2022

Source: Mevel and Mathieu’s (2016) calculations based on MIRAGE CGE model

To mitigate the expected trade losses for the African countries resulting from the establishment of MRTAs, especially the RCEP, India and Africa must build a solid partnership to boost their bilateral trade and investment flows. To this end, India’s active support towards Africa’s ongoing continental integration efforts can serve as basis for negotiations aimed at reciprocal market access and investment opportunities.

It is important to note that positive outcomes for the India-Africa trade and investment partnership are hinged on Africa having sufficiently integrated markets, enhanced regional and continental connectivity, and improved infrastructure facilities. These will, in turn, help the African countries to address the supply-side constraints, remove bottlenecks, and move up the regional value chains. The African Trade Policy Centre of the ECA and CII must continue to work closely to identify the sectors that offer opportunities for development in Africa in the context of AfCFTA reform.

The Mevel and Mathieu (2016) study clearly projects the negative impact of MRTAs, especially the RECP, on India-Africa trade. Africa’s exports to India will decrease because there will be an increase in the intra-African trade. On the other hand, if the AfCFTA is established, India’s exports to Africa could increase by US$4.3 billion (or 10 percent) by 2022 because it will provide the Indian industries and companies a larger, more unified market with less restrictive regulations. Since the trade balance between India and Africa is in favour of the African countries largely due to India’s high demand for energy resources, crude oil and petroleum, the establishment of AfCFTA augurs well for India-Africa trade and investment partnership.

India agrees to the AfCFTA in principle and supports its successful implementation. This has been reiterated in the 2015 Delhi Declaration.[liv] However, India and Africa need to move in tandem to ensure that the full gains are realised. After the AfCFTA comes into force, it is expected not only to support industrialisation and structural transformation efforts in Africa but also offer a more visible and robust market for Indian firms and investors to access, thereby making Africa a top business partner for India.

Conclusion

The AfCFTA agreement represents a historic development in Africa’s journey towards creating a single, common and integrated market for the continent. To achieve this goal, it is imperative that the African countries develop the ability to produce and manufacture goods on their own, which will subsequently increase intra-African trade. There are many constraints that have impeded Africa’s progress. Some of the key ones are: lack of implementation of cohesive policies, underperformance in trade liberalisation, poor infrastructure facilities, lack of skilling, restrictive movement of persons, and illiteracy.

The biggest challenge facing the African countries is the creation of higher-wage manufacturing jobs that require a range of critical industrial policies and measures. For the less industrialised countries, initiatives like the Accelerated Industrial Development for Africa (AIDA), supplemented with domestic investments in education and training, as well as the implementation of the Africa Mining Vision, can complement the AfCFTA by helping the resource-based economies to strategically diversify their exports to other African markets. The success of these initiatives, and the extent to which higher-wage manufacturing jobs can be created, will determine if Africa’s demographic advantage will yield dividend. In an era of knowledge and digital economy, Africa has to focus on human capacity development by enhancing the skills sets of its workforce and providing universal basic education.

There is also a need to ramp up investments in infrastructure to build linkages within and among the African countries. The challenges are immense in the landlocked countries. On the other hand, although Africa has made progress through port modernisations and trans-border road projects, these need to be completed in time to provide economic benefits. The trade policies need to be harmonised and the non-tariff barriers eliminated.

As for the AfCFTA, the African countries must fast-track the process of ratifying it to realise its promise. They must demonstrate commitment to unite and create a single, large market for the collective aspiration of seeing the ‘Africa Rising’ come true. As Kwame Nkrumah, the first prime minister of Ghana and a visionary, argued half a century ago, the clarion call, “Africa Must Unite”, continues to ring true today.

Annexure

RECs established under the Lagos Action Plan – the first wave (mid 1970s – early 1980s)

Economic Community of West African States (ECOWAS) – ECOWAS was established in 1975 to promote economic integration in the West Africa region. The integrated economic activities as envisaged in the area revolved around but not limited to industry, transport, telecommunication, energy, commerce, monetary and financial questions, natural resources, social and cultural matters. The group comprises of 15 member states: Benin, Burkina Faso, Gambia, Cape Verde, Cote d’Ivoire, Ghana, Guinea, Guinea Bissau, Liberia, Mali, Niger, Nigeria, Senegal, Sierra Leone and Togo.[lv]

A Preferential Trade Area (PTA) for the Common Market for Eastern and Southern Africa (COMESA) – A PTA agreement for COMESA was signed in 1982. The common market envisaged in the PTA was created in 1993 under the COMESA Treaty.[lvi] It has a total of 19 members: Burundi, Comoros, DR Congo, Djibouti, Egypt, Eritrea, Ethiopia, Kenya, Libya, Madagascar, Malawi, Mauritius, Rwanda, Seychelles, Sudan, eSwatini, Uganda, Zambia and Zimbabwe.

Economic Community of Central African States (ECCAS) – The ECCAS Treaty was signed in October 1983 in Libreville, Gabon, and came into force in December 1984. Following internal crises in many member states, ECCAS ceased activities between 1992 and 1998.[lvii] ECCAS was revitalised by a Heads of State and Government decision at the 1998 Summit in Libreville. It has a total of 10 members: Angola, Burundi, Cameroon, Central African Republic, Chad, Congo, DR Congo, Equatorial Guinea, Gabon and Sao Tome and Principe.

Arab Maghreb Union (UMA) – The UMA was established under the Marrakech Treaty of 1989 with the primary purpose of strengthening ties between member states, promoting prosperity, defending national rights and adopting common policies to promote the free movement of people, goods, services, and capital within the region. It has a total of 5 member states: Algeria, Libya, Mauritania, Morocco and Tunisia.

The Abuja treaty and the second wave of RECs – (early 1990 onwards)

South African Development Community (SADC) – It is the successor to the South African Development Co-ordination Conference (SADCC) established in 1982.[lviii] The transformation of SADCC into SADC took place in 1992 and was further amended in 2001. There are a total of 15 members: Angola, Botswana, DR Congo, Lesotho, Madagascar, Malawi, Mauritius, Mozambique, Namibia, Seychelles, South Africa, eSwatini (Swaziland), Tanzania, Zambia and Zimbabwe.[lix]

Intergovernmental Authority on Development (IGAD) – It was established in 1996 to address recurring droughts and other natural disasters in East African region. It has a total of eight members: Djibouti, Eritrea, Ethiopia, Kenya, Somalia, South Sudan, Sudan and Uganda.

Community of Sahel-Saharan States (CEN-SAD) – It was formed in 1998 with the primary objective of “promoting economic, cultural, social, and political integration of its member states”.[lx] It aims at establishing a comprehensive economic union particularly in agricultural, industrial, social and energy fields.

East African Community (EAC) – The EAC was Africa’s first REC established back in 1967, but collapsed in 1977 due to political differences. The treaty establishing the EAC was signed on November 1999 and came into force in July 2000. The EAC established a Customs Union in 2005 and a common market in 2010. It has a total of six members: Burundi, Kenya, Rwanda, Uganda, Tanzania and South Sudan.

Table 2: India’s Trade with Africa ($ bn)

2005-2006

2006-2007

2007-2008

2008-2009

2009-2010

2010-2011

2011-2012

2012-2013

2013-2014

2014-2015

2015-2016

India’s Export to Africa ($ bn)

7

10.03

14.2

14.8

13.4

19.7

24.7

29.1

31.2

32.8

25

Africa’s Share in India’s Exports (%)

6.8%

8.1%

8.7%

8.0%

7.5%

7.9%

8.1%

9.7%

9.9%

10.6%

9.5%

India’s Imports from Africa ($ bn)

4.9

14.7

20.5

24.7

25.6

32

44.1

41.1

36.6

38.6

31.7

Africa’s Share in India’s Imports (%)

3.3%

7.9%

8.1%

8.1%

8.9%

8.6%

9.0%

8.4%

8.1%

8.6%

8.3%

India’s Total Trade with Africa ($ bn)

11.9

25

34.7

39.5

39

51.7

68.8

70.3

67.9

71.5

56.7

India’s Trade Balance with Africa ($ bn)

2.1

-4.4

6.3

-9.9

-12.2

-12.2

-19.4

-12

-5.4

-5.8

-6.6

Source: Ministry of Commerce and Industry (MOCI), Government of India; and EXIM Bank Analysis

Table 3: India’s Approved Overseas Direct Investments in Africa ($ mn)

Country

Apr 1996-Mar 2010

2010-11

2011-12

2012-13

2013-14

2014-15

2015-16

Apr 1996 – Mar 2016

Mauritius

9081.4

13106.9

7421.1

4438.9

4581.9

4580.8

3670.4

46881.4

Mozambique

18.2

3.0

1.0

0.6

2643.1

7.7

1.7

2675.2

Sudan

1224.8

13.9

0.0

0.0

–

–

–

1238.8

Egypt

821.8

24.0

11.8

76.6

29.2

17.6

8.3

989.3

South Africa

197.5

41.8

12.2

137.5

19.1

29.5

60.6

498.2

Libya

163.2

56.0

–

0.8

27.2

7.4

0.1

254.7

Tunisia

5.2

–

–

4.7

103.5

–

82.2

195.6

Liberia

191.0

–

0.4

0.4

0.3

0.2

–

192.3

Kenya

150.4

0.7

1.8

8.7

1.8

6.1

3.8

173.2

Zambia

3.1

0.9

2.8

4.5

12.0

41.7

79.7

144.5

Morocco

35.9

38.0

0.0

4.9

5.8

14.9

21.7

121.2

Nigeria

66.4

8.9

16.3

7.7

6.6

12.7

0.6

119.2

Gabon

69.1

0.1

0.2

–

18.7

12.1

–

100.0

Ethiopia

12.2

3.7

3.6

3.1

6.0

42.2

17.0

87.7

Ghana

15.9

11.6

17.4

8.9

24.4

2.2

2.0

82.5

Tanzania

36.3

6.6

7.4

7.4

3.8

1.6

11.4

74.6

Botswana

19.6

2.9

5.6

3.9

0.9

5.0

–

38.0

Uganda

3.6

23.3

0.3

0.5

0.7

1.5

1.4

31.2

Rwanda

18.9

–

–

1.0

2.3

1.5

1.1

24.8

Senegal

23.3

–

–

1.1

–

–

–

24.3

Ivory Coast

15.6

–

–

–

0.1

–

–

15.7

Algeria

1.3

–

2.0

–

–

3.1

5.5

12.0

Mali

0.3

0.0

1.2

1.4

4.1

1.4

0.1

8.4

Mauritania

1.7

–

1.4

2.9

0.2

–

–

6.1

Congo

4.4

–

0.7

–

–

0.2

–

5.3

Madagascar

0.1

0.0

0.6

1.9

–

0.3

0.9

3.7

Seychelles

0.0

2.5

0.7

–

0.3

–

–

3.5

Zimbabwe

2.5

–

0.1

–

0.2

–

2.9

Namibia

0.2

0.6

1.3

–

0.2

–

–

2.3

Malawi

1.3

–

–

–

–

0.1

0.5

1.9

Guinea

–

–

0.1

0.2

0.2

0.3

0.6

1.4

Benin

0.1

–

–

–

–

–

1.0

1.1

Niger

0.5

0.2

0.2

–

–

–

–

0.9

Swaziland

0.4

–

–

–

–

–

–

0.4

Chad

–

0.1

–

–

–

0.1

–

0.2

Djibouti

–

–

–

0.1

–

–

0.1

0.2

Central African Rep

–

–

–

0.1

–

–

–

0.1

Burkina Faso

0.1

–

–

–

–

–

–

0.1

Sierra Leone

–

–

–

–

–

–

–

–

Cameroon

–

–

–

–

–

–

–

–

FDI Outflow to Africa

12215.8

13346.7

7510

4717.5

7492.5

4790.2

3970.5

54043.3

Share in India’s Total FDI Outflow

13.7%

30.4%

24.3%

17.6%

20.3%

15.5%

18.0%

19.2%

Note: ‘-‘ Negligible / Unavailable Source: Ministry of Commerce and Industry (MOCI), Government of India; RBI and EXIM Bank Analysis

Table 4: FDI Equity Inflows to India from Africa ($ mn)

Country

FDI Inflow, April 2000 to March 2016 ($ mn)

Share in India’s FDI inflow (%)

Africa

96,687.6

33.5%

Mauritius

95,909.7

33.2%

South Africa

372.2

0.1%

Seychelles

187.3

0.1%

Morocco

138.0

0.1%

Kenya

22.0

–

Liberia

14.6

–

Nigeria

13.2

–

Ghana

7.7

–

Egypt

4.7

–

Tunisia

4.3

–

Uganda

3.9

–

Tanzania

3.5

–

Others

6.5

–

Note: ‘-‘ not available / negligible Source: Department of Industrial Policy and Promotion, ministry of Commerce and Industry, Government of India; and EXIM Bank Analysis

Endnotes

[i] Tesfaye, Dinka, and Walter, Kennes. “Africa’s Regional Integration Arrangements: History and Challenges,” ECDPM Discussion Paper 74, (September 2007): 5. http://ecdpm.org/publications/africas-regional-integration-arrangements-history-challenges/

[ii] “History of Africa’s Regional Integration Efforts”, United Nations Economic Commission for Africa, https://www.uneca.org/oria/pages/history-africa%E2%80%99s-regional-integration-efforts

[iii] Indication of legal instruments to be signed at the 10th extraordinary session of the assembly on the launch of the AfCFTA, https://au.int/sites/default/files/pressreleases/34033-pr-indication20of20signing20authority20-20updated20final20final20docx.pdf

[iv] Signe, Landry. “Africa’s big new free trade agreement, explained,” The Washington Post, March 29, 2018. https://www.washingtonpost.com/news/monkey-cage/wp/2018/03/29/the-countdown-to-the-african-continental-free-trade-area-starts-now/?noredirect=on&utm_term=.9c1eaddad574

[v] The Continental Free Trade Area: Making it Work for Africa,” UNCTAD Policy Brief, No.44, (2015). http://unctad.org/en/PublicationsLibrary/presspb2015d18_en.pdf

[vi] “Why Africa’s free trade area offers so much promise,” news24, 27 March 2018, https://www.news24.com/Africa/News/why-africas-free-trade-area-offers-so-much-promise-20180326

[vii] Satchu, Aly-Khan. “Is free trade a silver bullet for African prosperity?” TRTWorld, 30 March (2018). https://www.trtworld.com/opinion/is-free-trade-a-silver-bullet-for-african-prosperity–16355

[x] Luke, David and Sodipo, Babajide. “Launch of the continental Free Trade Area: New prospects for African trade?” International Centre for Trade and Sustainable Development, June 2015. https://www.ictsd.org/bridges-news/bridges-africa/news/launch-of-the-continental-free-trade-area-new-prospects-for-african

[xi] “Why Africa’s free trade area offers so much promise,” news24, 27 March 2018, https://www.news24.com/Africa/News/why-africas-free-trade-area-offers-so-much-promise-20180326

[xiii] Signe, Landry. “3 things to know about Africa’s industrialization and the Continental Free Trade Area,” Brookings, November 2017, https://www.brookings.edu/blog/africa-in-focus/2017/11/22/3-things-to-know-about-africas-industrialization-and-the-continental-free-trade-area/

[xv] Landry Signe. “Why Africa’s Free Trade Area offers so much promise,” The Conversation, 26 March 2018, https://theconversation.com/why-africas-free-trade-area-offers-so-much-promise-93827

[xvii] Winters, L. Alan. “Regionalism Versus Multilateralism,” World Bank Policy Research Working Paper No. 1687, (1996). https://papers.ssrn.com/sol3/papers.cfm?abstract_id=615007

[xviii] Tanyanyiwa, Itai, Vincent and Hakuna, Constance. “Challenges and Opportunities for Regional Integration in Africa: The Case of Sadc,” IOSR Journal of Humanities and Social Sciences (IOSR-JHSS), 19, no.2, (2014). http://iosrjournals.org/iosr-jhss/papers/Vol19-issue12/Version-4/P019124103115.pdf

[xix] United Nations Economic Commission for Africa (UNECA), “Assessing Regional Integration in Africa IV: Enhancing Intra-African Trade,” Addis Ababa: Ethiopia, (2010).

[xx] Hasan Tuluy, “Regional Economic Integration in Africa,” Global Journal of Emerging Market Economies 8, no.3, (2017) 22 January

[xxi] Jamie de Mello & Yvonne Tsikata. Regional integration in Africa: Challenges and Prospects, The Oxford Handbook of Africa and Economics: Volume 2: Policies and Practices, (2015).

[xxii] Adebayo Adedeji. “History and prospects for regional integration in Africa,” Paper presented at the Third meeting of Africa Development Forum, Addis Ababa, Ethiopia. (March 2002).

[xxiii] “History of Africa’s Regional Integration Efforts,” United Nations Economic Commission for Africa, https://www.uneca.org/oria/pages/history-africa%E2%80%99s-regional-integration-efforts

[xxiv] Africa Development Bank Group (AfDB), “Mission and Strategy,” (2018). https://www.afdb.org/en/about-us/mission-strategy/

[xxv] Hatzernburg, Trudi. “Regional Integration in Africa,” World Trade Organization Paper, no. ERSD-2011-14, South Africa, (2011).

[xxvi] “Key pillars of regional integration in Africa,” United Nations Economic Commission for Africa, (2018). https://www.uneca.org/oria/pages/key-pillars-africa%E2%80%99s-regional-integration

[xxvii] Lopez, Carlos. “Inching towards integration,” International Monetary Fund, 53, no.2, (June 2016). http://www.imf.org/external/pubs/ft/fandd/2016/06/lopes.htm

[xxviii] Sow, Mariama. “Figures of the week: Regional integration in Africa,” Brookings, 18 January (2018). https://www.brookings.edu/blog/africa-in-focus/2018/01/18/figures-of-the-week-foresight-africa-regional-integration/

[xxxv] “The Single African Air Transport Market – An Agenda 23 Flagship Project,” (2018): 2. https://au.int/sites/default/files/newsevents/workingdocuments/33100-wd-6a-brochure_on_single_african_air_transport_market_english.pdf

[xxxvi] Kazeem, Yomi. “African countries have taken the first major step towards cheaper continental flights,” Quartz, 29 January, (2018). https://qz.com/1191558/africa-union-launches-single-african-air-transport-market/

[xxxvii] Kazeem, Yomi. “More African countries opened up to African travellers in 2017,” Quartz, 29 December (2017). https://qz.com/1167238/africa-travel-kenya-namibia-nigeria-to-issue-visa-on-arrival/

[xxxviii] Saygili, Mesut et al. “African Continental Free Trade Area: Challenges and Opportunities of Tariff Reductions,” UNCTAD Research Paper 15, (February 2018): 5. http://unctad.org/en/PublicationsLibrary/ser-rp-2017d15_en.pdf

[xxxix] “Building the African Continental Free Trade Area: Some Suggestions on the Way Forward,” UNCTAD, (2015): 3. http://unctad.org/en/PublicationsLibrary/ditc2015misc1_en.pdf

[xli] Parshotam, Asmita. “Can the African Continental Free Trade Area Offer a New Beginning for Trade in Africa?” South African Institute of International Affairs Occasional Paper 280, (June 2018): 23. http://www.saiia.org.za/research/can-the-african-continental-free-trade-area-offer-a-new-beginning-for-trade-in-africa/

[xlii] “Building the African Continental Free Trade Area: Some Suggestions on the Way Forward,” UNCTAD, (2015): 3. http://unctad.org/en/PublicationsLibrary/ditc2015misc1_en.pdf

[xlvi] Witschge, Loes. “African Continental Free Trade Area: What you need to know,” Al Jazeera, 20 March (2018). https://www.aljazeera.com/news/2018/03/african-continental-free-trade-area-afcfta-180317191954318.html

[xlvii] The Continental Free Trade Area: Making it Work for Africa, UNCTAD Policy Brief, No.44, 2015, http://unctad.org/en/PublicationsLibrary/presspb2015d18_en.pdf

[xlviii] “AfCFTA to spur Africa’s industrialisation and economic development,” African Review, 20 September (2018). http://www.africanreview.com/finance/economy/afcfta-to-spur-africa-s-industrialisation-and-economic-development

[xlix] Haidar, Suhasini. “PM in Africa amid trade slump,” The Hindu, 23 July (2018). https://www.thehindu.com/news/national/pm-in-africa-amid-a-trade-slump/article24497558.ece

[l] Mevel and Mathieu. Emergence of mega regional trade agreements and the imperative for African economies to strategically enhance trade-related South-South Cooperation, presented at the 19th Annual Conference on Global Economic Analysis, Washington DC, (March 2016).

[li] “Deepening Africa-India Trade and Investment Partnership,” African Trade Policy Center and Confederation of Indian Industries Joint Report, Addis Ababa, Ethiopia, (March, 2018). https://www.uneca.org/sites/default/files/PublicationFiles/africa-india_trade_and_investment_study_fin.pdf

[lii] United Nations Economic Commission for Africa and Confederation of Indian Industries Joint Report, (2018): 17. https://www.uneca.org/sites/default/files/PublicationFiles/africa-india_trade_and_investment_study_fin.pdf

[liv] “Third India Africa Forum Summit,” Delhi Declaration, 29 October, New Delhi, India, (March, 2015): 3. http://www.mea.gov.in/Uploads/PublicationDocs/25980_declaration.pdf

[lv] Economic Community of West African States (ECOWAS), “Member States,” http://www.ecowas.int/member-states/

[lvi] African Union webpage. “Regional Economic Communities (RECs),” https://au.int/en/organs/recs

The views expressed above belong to the author(s). ORF research and analyses now available on Telegram! Click here to access our curated content — blogs, longforms and interviews.

Abhishek Mishra is an Associate Fellow with the Manohar Parrikar Institute for Defence Studies and Analysis (MP-IDSA). His research focuses on India and China’s engagement ...

PDF Download

PDF Download