The global macroeconomy has undergone unprecedented change in recent years, particularly because of the COVID-19 pandemic. While the G20 had an effective coordinating role in steering the global economy through the 2008 global financial crisis, its role in engineering an inclusive and sustainable recovery from the pandemic has been more mixed. Incomes in the advanced G20 economies are on track to return to pre-pandemic levels by end-2022 but have recovered more slowly in the low- and middle-income countries. At the same time, debt has increased, and inflationary pressures are building due to supply chain disruptions, posing challenges to maintaining fiscal and monetary stability. The Russia-Ukraine conflict has further weakened the global economy, and the negative effects of climate change have also left countries vulnerable. Under the current G20 presidency (Indonesia), efforts are focused on encouraging countries to work together to achieve a stronger and more sustainable global recovery. A range of monetary, fiscal and trade policy issues are developing, and these, in addition to emerging issues, will inform India’s G20 presidency in 2023.

Introduction

The G20 has discussed issues related to the global macroeconomy since its inception in 1999, when it began as a grouping of finance ministers in the wake of the Asian financial crisis. The G20 Leaders Summit began in 2008. Early discussions were centred around financial coordination across the member-states to address the impact of the 2008 global financial crisis. In 2009, countries coordinated efforts through the Financial Stability Board to increase the resilience of the global financial system, while preserving its openness and integrated network structure. As a result, the G20 was able to stabilise financial markets through a series of coordinated financial and monetary stimuli that averted a major economic depression.[1]

Since 2009, the G20 has supported strong, sustainable, and balanced growth, but its actions appear to have had a limited effect in recent years.[2]For instance, actions to contain and counter the fallout from the COVID-19 pandemic have been less successful than those to tackle the 2008 global financial crisis,[3]although national-level responses in the form of monetary and fiscal policies have been substantial. Still, the global recovery from the pandemic is uneven and not inclusive or sustainable.[4]In addition, macroeconomic challenges in the form of increased debt, inflationary pressures, and new risks to global growth due to the Russia-Ukraine conflict have emerged.

Three emerging markets—Indonesia, India, and Brazil—will chair the G20 between 2022 and 2024, with Indonesia as the current chair. Under the banner of ‘Recover Together, Recover Stronger,’ Indonesia has encouraged all countries to work together to achieve a stronger and more sustainable recovery as the global economy continues to be affected by the impacts of the pandemic.[5]This paper discusses the global macroeconomic framework and priority options for India’s presidency in 2023. It provides an overview of the global macroeconomy in terms of growth and recovery and discusses macroeconomic measures to ensure global growth and recovery are inclusive, sustainable, and increasingly digital. It also examines the options and priorities for India’s presidency, including areas in which the UK and India can collaborate.

Global Macroeconomic Developments: An Overview

The most notable recent changes in the global macroeconomy include: (i) an uneven economic recovery from the pandemic across the world, with advanced countries recovering more quickly than emerging and low-income countries; (ii) marked increases in inflation and inflationary pressures; (iii) continued increases in global debt; (iv) the disastrous impact of climate change; and (v) the fallout from the Russia-Ukraine conflict. These issues will likely continue to evolve and dominate as India’s G20 presidency approaches.

Although the pandemic affected all parts of the world, low- and middle-income countries are recovering much more slowly than richer countries. With a high incidence of cases, low vaccination rates, and lack of government resources, such economies and their health systems faced the brunt of the fallout. Hospitals and their staff were burdened by the excessive pressure exerted by many cases and the high mortality rate associated with middle-income countries.[6]This was coupled with a much lower rate of access to vaccines and an uneven recovery path favouring those with access to essential food and medical goods. As the world recovers from the pandemic, an increase in demand for goods and services has exerted tremendous pressure on supply chains worldwide, exacerbating the supply-side disruptions caused by government-mandated closures and social distancing measures. As demand outgrew supply, prices of commodities (metals, energy, fuels, and food products) increased markedly in 2021, causing challenges for low-income households.

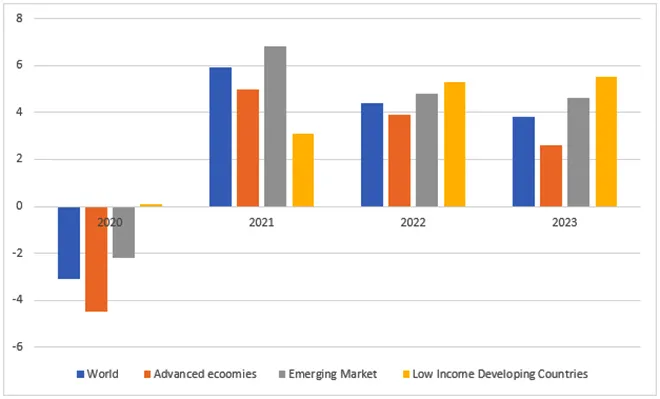

Figure 1: GDP growth in 2020-2023

Source:IMF January 2022 Update. Actual (2020) and estimates / forecasts (2021-2023)[7]

The pandemic had an unprecedented impact on the global economy in 2020. Richer countries were quick to respond with fiscal and monetary measures, and their GDPs are now approaching pre-pandemic levels. The US Federal Reserve (Fed), for example, injected large amounts of liquidity into the system, including the credit market, by purchasing commercial paper and exchange-traded funds, reducing the interest rate to zero and guaranteeing some loans.[8]At the same time, the European Union (EU) aimed to keep inflation below 2 percent.[9]Unfortunately, alongside the uneven impacts on the global economy,[10],[11]the pandemic has also had disproportionate and persistent effects on the poor, young, informal, and women workers in richer and poorer countries.[12],[13]

In addition to the lack of inclusion, the recovery has also seen a lack of attention to environmental sustainability. Recent analysis suggests that only 6 percent (US$860 billion) of the US$14 trillion G20 economic stimulus over 2020-2021 was “green”, and about 3 percent has been spent on activities that will increase carbon emissions, such as subsidies to coal.[14]This compares poorly (or three times less so) to the US$520 billion of green stimulus in a total of US$3.25 trillion support, equivalent to 16 percent, after the global financial crisis. This showcases that the world is not seeing a green recovery.

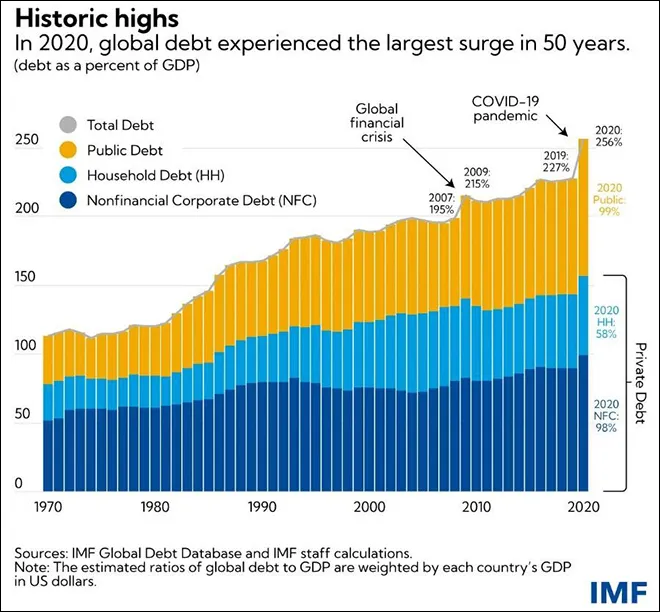

A long-term impact from the pandemic is the increase in global debt. In 2020, global debt increased to 256 percent of GDP (US$226 trillion). Public debt in advanced economies grew from 70 percent of GDP in 2007 to 124 percent of GDP in 2020. Private and public debt increased by twice as much during the pandemic compared to the 2008 financial crisis. Public debt in emerging markets reached record highs in 2020, while in low-income countries, it grew to levels not seen since the early 2000s, when many were benefiting from debt relief initiatives, such as heavily indebted developing countries and the Multilateral Debt Relief Initiative.

Figure 2: Global Debt, Public and Private (1970-2020)

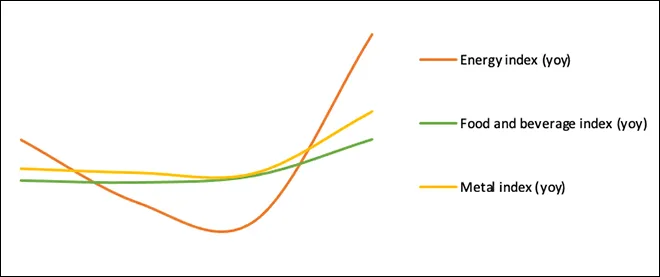

Inflationary pressures have built up in 2021, due in part to supply shortages. In addition, demand-side factors have also played a role as countries come out of the pandemic-induced recession through measures that stimulate the global economy. As a result of supply- and demand-side factors, energy, food and beverage, and metal prices increased quickly in 2021 (see Figure 3).

Source:IMF Primary commodity price system database, 2021

A looming concern is climate change and its observable impact on most countries in the form of natural disasters, erratic weather patterns, warmer temperatures, melting glaciers, and rising sea levels.[16]These affect food production, migration patterns, livelihoods, and consumer preferences. On a broader level, this will affect economic outcomes like output, investment, and productivity through shocks in the short-run and other long-term impacts.[17]The challenges presented by climate change arise from the global nature of pollutants. The G20 members, some of the world’s largest countries, are also responsible for over 80 percent of global emissions.[18]

New concerns have also emerged regarding the Russia-Ukraine conflict and associated sanctions on Russia by several countries, including the EU, the UK, and the US. This will have a major impact on the world economy and G20 countries. The precise impact depends on various factors, but global commodity prices such as oil and wheat have already increased markedly.

Estimates suggest that the combined impact of the pandemic and the ongoing conflict with Ukraine on Russian GDP over 2022-2023 is 5 percent, and the world economy is between 0.4 percent and 0.9 percent (and between 0.3 percent and 0.7 percent for the UK, and between 0.4 percent and 1.2 percent for India).[19]The effects stem from increases in oil, metals, and food prices, recessions in Russia and Ukraine, and general supply chain disruptions. All these effects are highly uncertain and will depend on the evolution of the conflict and associated sanctions. Further impacts can be expected from trade and financial sanctions. For example, a change in the G7 and EU trade policy stance away from the most favoured nation status may reduce Russian GDP by 1.1 percent.[20]

Other estimates suggest that the ongoing Ukraine war will reduce global output by 0.4 to 1 percentage point in 2022.[21]This will amount to global costs between US$380 billion and US$950 billion in 2022. A vulnerability index developed by researchers Sherillyn Raga and Laetitia Pettinotti quantifies the vulnerabilities of 118 low- and middle-income countries to the war’s impact based on each country’s direct economic links to Russia and Ukraine, indirect exposure to global effects of the war, and resilience of macroeconomic fundamentals.[22]The top seven most-vulnerable countries are Belarus, Armenia, the Kyrgyz Republic, Lebanon, Maldives, Montenegro, and Uzbekistan.

Amidst this macroeconomic crisis targeting monetary, fiscal, and trade policy, countries have adopted various stances to tackle it. For instance, the Fed aims to increase the interest rate to tackle rising inflation in the US market after quantitative easing during the pandemic led to a massive rise in prices for consumer products.[23]The European Central Bank (ECB) has been forced to announce a government bond-buying programme to tackle the ongoing sovereign debt crisis[24]This has helped keep countries afloat despite the drain on their finances during the pandemic, but led to a ballooning of inflation in the EU, even before the Ukraine crisis, which is likely to push the prices for oil and metals higher.[25]In this scenario, the ECB has terminated the bond-buying programme as of July 2022.

The surge in commodity prices has hurt emerging economies too. India, for example, has begun feeling inflationary pressures that could hurt its current account deficit, and the Reserve Bank of India might need to step in if inflation surpasses the target band of 4 percent to 6 percent for a long time.[26]Argentina, another emerging economy in the G20, has dipped into IMF’s Special Drawing Rights (SDR) reserve to obtain a 30-month extended arrangement to provide a balance of payment and budgetary support to the government amidst rising inflation and public debt.[27]Previously, the IMF had also injected US$650 billion of SDR into the global system to finance urgent liquidity requirements during the pandemic. However, only 3 percent of this went to low-income countries, 30 percent to middle-income countries, and the rest to advanced economies.[28]In response to this skewed access to IMF funds, it began supporting the Resilience and Sustainability Trust that would allow advanced countries to lend their IMF reserves to vulnerable countries cheaply to target climate and pandemic preparedness.[29]

Managing the Global Macroeconomic Recovery

G20 countries have responded to the pandemic with large monetary policy measures (unprecedented low-interest rates, more liquidity), fiscal actions (worth some US$16 trillion), and liberalising trade policies.[30]They now face a balancing act in the context of large increases in debt, higher inflation, and the need for a green and inclusive transformation. Fiscal and monetary policies were complementary; lower interest rates allowed governments to borrow historically large amounts at historic low costs. However, as central banks raise interest rates to dampen inflationary pressures, borrowing costs will rise, which is already affecting emerging markets.[31]This section reviews the recent evolution in macroeconomic policies.

• Monetary policy and tackling inflation

The rise in commodity prices, especially energy, has caused inflationary pressures in many countries. Central banks have responded with monetary policy measures to maintain price stability in their domestic markets. This comes at a time when major economies are looking to raise interest rates to tackle inflationary pressures and prevent price volatility. Expected tightening by advanced economies has contributed to currency depreciation in several emerging market economies.

The IMF’s G20 surveillance note,[32]tabled at the G20 finance ministers and central bank governors’ meeting in February 2022, details that monetary policy has pivoted towards tightening in most economies due to inflation expectations drifting above target in some economies and tightening labour markets. Central banks in Brazil, Mexico, and Russia started tightening, while those in Australia, Japan, and the US started to taper asset purchases. China loosened its monetary policy stance amid the backdrop of low inflation and softening growth.

At a more structural level, the G20 has called for central banks to communicate their intentions transparently and coherently to avoid large price swings.[33]It has also reaffirmed its goal to support central bank independence to reinforce the credibility and effectiveness of monetary policies. The members made a strong commitment to maintaining exchange rate flexibility by refraining from competitive devaluation that could be harmful to some economies.[34]

• Fiscal policy and confronting public debt

Falling government revenues, coupled with major public spending to reduce the immediate impact of the pandemic, increased global debt by US$20 trillion between Q3 2019 and Q3 2020.[35]Global debt-to-GDP ratios have climbed to an all-time high (see Figure 2). To put it into perspective, global debt-to-GDP ratio was a little over 100 percent in 1970, increased to 215 percent in 2009 and further still to the present value of 256 percent in 2020, with recent changes affected due to increasing private debt. According to World Bank standards, the threshold of public debt to GDP is 77 percent, and any increase above that negatively affects overall growth. In 2020, the total public debt-to-GDP was 99 percent.

The G20 members recognise that countries have accumulated debt in the course of tackling the pandemic through excessive external borrowings to finance health interventions, increasing unemployment benefits, and providing vaccination cover to the public. While fiscal consolidation efforts may increasingly become important in the advanced countries, growing debt has already led to (partial) defaults in the poorest countries. In April 2020, the G20 members announced the Debt Service Suspension Initiative (DSSI) to assist the most impoverished countries that have accumulated the most debt during the pandemic. The scheme mainly targeted the suspension of bilateral debt for 73 International Development Association-eligible and least developed countries until 31 December 2020. However, following the onset of new virus variants in 2021, the scheme was extended up to December 2021. As a result, debt repayment of over US$12.9 billion was deferred towards G20 members and Kuwait and the United Arab Emirates. Of this, about a third were deferred in terms of interest payments. Under the scheme, a refinancing operation was preferred over a deferral for countries where the creditor was a G20 country. One notable example is the refinancing of a loan owed by Papua New Guinea to Australia.[36]This scheme mainly benefitted Sub-Saharan Africa and South Asia, with Pakistan being the largest beneficiary of the scheme through deferred payments of up to US$1.3 billion in 2020. Within Sub-Saharan Africa, 28 counties were able to defer payments during the peak of the pandemic.

Recently, the G20 has also created the Common Framework for Debt Treatment beyond the DSSI. Providing countries with debt treatments will facilitate financial support from the IMF and multilateral development banks (MDBs).[37]The Common Framework looks to bring official creditors across the G20 and private creditors together to provide debt treatments on comparable terms. Although debt treatments will be offered on a case-by-case basis, it is expected to follow the Paris Club on solidarity, consensus, and information sharing.[38]Moreover, it would include the participation of private creditors. In particular, the IMF would have a pivotal and more active role to play, evolving from an emergency financier to providing standard IMF funding to countries in need.

The current Debt Sustainability Framework provides rules under which a country may receive lending. But in response to worries that the shock from a Greek restructuring might spill over to other European countries, the IMF introduced a “systemic exemption”[39]permitting the institution to provide Greece with financing despite doubts that the country’s debts were sustainable with high probability, i.e. when there was a high risk of international systemic spillovers. Emerging markets argued that large IMF shareholders received preferential treatment.[40]The systematic exemption was subsequently removed. So, there are still concerns about lending to a country whose debt is not deemed “sustainable”. There are other challenges to the framework and a new framework could be designed to be more country-specific, taking into account specific needs around investment needs.

• Trade policy, resilient supply chains, and avoiding protectionism

From the pandemic’s start, the G20 announced measures to ease supply chains, especially for food and medical products and avoid protectionism, with varying success. Indonesia’s presidency in 2022 is also dedicated to enhancing global economic recovery through trade, investment, and industry.[41]A joint report by the Organisation for Economic Co-operation and Development (OECD), World Trade Organization, and United Nations Conference on Trade and Development[42]argues that trade has been central to combatting the pandemic and provides strong foundations for a global economic recovery. Since the outbreak of the pandemic, 144 COVID-19 trade and trade-related measures in goods have been implemented by G2O economies. Of these, 105 (73 percent) were trade-facilitating and 39 (27 percent) could be considered trade restrictive. Export restrictions account for 95 percent of all restrictive measures recorded, and of these 54 percent had been phased out by mid-October 2021. The estimated trade coverage of COVID-19 trade restrictions was almost double (US$88.4 billion) that of trade facilitating measures US$48.2 billion. The monitoring of non-COVID-19 trade measures reveals that fewer restrictions were put in place in the half year to October 2021, but the stockpile of previous trade restrictions remains large. Therefore, much more needs to be done by the G20 to facilitate trade after the pandemic. The new challenges emerging from the Russia-Ukraine conflict will lead to further supply chain challenges. Importantly, dealing with supply chain issues will also contain inflationary pressure and reduce the need for monetary tightening, which will further weaken the global economy. Thus, easing supply chains and avoiding protectionism will remain a major issue in the coming year.

Measures to Ensure Inclusive and Sustainable Recovery

The G20 is currently focusing on three global issues that are likely to continue to be at the forefront of the grouping’s efforts to steer the global economy: (i) green growth; (ii) inclusive health; and (iii) digital transformation. How can the global macroeconomy be leveraged to support these issues?

• Green growth

The disastrous effects of climate change are undeniable, and it would take an international collaborative solution to confront it on multiple fronts. The macroeconomic risks of climate change are far-reaching and can leave a long-term footprint on the planet. As a result, climate change was a key part of the Framework Working Group (FWG) agenda for 2021 under the Italian presidency and is likely to remain an important part of the agenda in the coming years. The G20 finance ministers and central bank governors have agreed to tackle climate change and support environmental protection to aid sustainable growth through investment in innovative solutions and by incorporating the agenda in future economic policymaking The FWG is also working on systemically integrating climate risks into risk monitoring activities to manage short- and long-term economic damage.[43]

The G20 is also an important forum to promote private investment in green infrastructure projects that could help transition from fossil fuels to renewable and sustainable energy sources and achieve net zero in 2050, albeit at different times in different countries. The G20 could accelerate collaboration between advanced and emerging economies to create greener jobs, support green growth, and assist low-income countries to escape the brown growth trap.[44]In 2017, the OECD published a report on investment in climate and growth under the German G20 presidency that already set the tone for the effort made by the members in the years that followed. This report also recommended that any climate action taken at the time could result in a net growth benefit of 2.8 percent per year by 2050.[45]

The recent communique from the G20 stressed the importance of developing national pathways to meet short- and long-term climate goals by harnessing the power of finance, technology, sustainable consumption, and responsible production.[46]The communique also included the commitment to mobilise US$100 billion by advanced countries to finance the climate transition in emerging and low-income countries and secure additional funding from MDBs.[47]The renewed interest at COP26 to (i) secure global net zero by 2050; (ii) keep global temperature rise to 1.5 degrees; (iii) protect communities and natural habitats affected by climate change; and (iv) mobilise climate finance, both public and private that could be re-directed from brown projects[48]were in line with the communique and has accelerated the transition to a green and circular economy through redirection of public policy, public finance, and private investment across countries. This will require decoupling growth from the appetite for fossil fuels and related emissions.[49]However, China, India, and Saudi Arabia expressed concerns over phasing out the usage of fossil fuels, especially coal, which also attracted resistance from one of the world’s biggest coal producers, Australia, and major exporter-cum-importer, Russia. Any future effective action on tackling climate change will require consensus and dialogue between these countries and those in the favour of accelerated decarbonisation, including Japan, the UK, and the US.[50]

• Inclusive health

The pandemic has highlighted the uneven distribution of vaccines across high-, middle-, and low-income economies. Estimates show that up till mid-2022, G20 countries had used 82 percent of the world’s COVID-19 vaccines, while the low-income countries received close to 3 percent of all doses.[51]To tackle this population-vaccination mismatch, G20 health ministers met in Rome, Italy, first in May 2021 to launch the Access to COVID-19 Tools (ACT) Accelerator, along with the World Health Organization (WHO) to provide equitable access to testing kits, treatment, and vaccines.[52]They also met in September 2021 to unanimously sign the ‘Rome Pact’ to increase the supply of vaccines and medical assistance to poor and fragile nations to meet the global vaccination target of 40 percent by the end of 2021. Canada donated nearly two million doses of vaccines to Uganda in November 2021 under the WHO’s COVAX vaccine sharing facility (under the ACT Accelerator).[53]Health ministers reaffirmed the need to unlock the universalism of access to health services to tackle post-pandemic recovery. However, this pact has been considered “weak” due to the absence of strong and well-defined actionable goals by the G20, as well as the controversy around waiving patents on vaccines to ensure swift reproduction and delivery.[54]Notably, the G20 members are divided on temporarily suspending intellectual property rights (under the TRIPS Agreement) on vaccines technology to allow for wider production—India, Indonesia, and South Africa are pushing the agenda, while Germany, the UK, and the EU have blocked it thus far.[55]Inequality in access to global vaccines is a serious issue that could unravel the months of vaccination drive undertaken by rich countries, especially if the developing countries in Africa are left at the mercy of the virus.[56]The People’s Vaccine Alliance, a coalition of 75 health organisations, has called for the creation of global vaccine production hubs in developing countries to reduce the monopoly of the rich countries and establish direct control on its access and usage; as well as decentralise the technology and know-how around its manufacturing.[57]

• Digital transformation

Previous G20 statements already recognised the goal of promoting universal and affordable access to the Internet by all people by 2025.[58]The grouping previously welcomed G20 principles on the digital economy and trade, including artificial intelligence.[59]However, this is an unfinished agenda. A briefing by the B20-T20[a]argues that the pandemic has contributed to accelerating the digital transition.[60] The use of digital technology has increased during the pandemic and digitalisation impacts on growth and productivity. However, the benefits of these changes are hampered by inequalities, such as a growing digital divide—3.7 billion people lack access to the Internet and at least one-third of the world’s schoolchildren could not access remote learning in 2020-2021. The briefing suggests the G20 needs to do more to bridge the digital divide, build trust and coordination in the digital economy and guarantee security and privacy in the digital sphere.[61]Digital financial inclusion is one of the priority agendas of Indonesia’s G20 presidency, focusing in part on digital financial inclusion and small and medium enterprise finance, linked to the G20’s 2020 Financial Inclusion Action Plan.[62]This will help address the barriers to financial inclusion faced by individuals and firms. The digitalisation of services offers ways to be used to improve identity verification, access digital payment systems, and facilitate financial protection and literacy among populations.[63]

The G20 can address another issue dealing with the informality of the services sector. This issue is highly prevalent in the emerging economies of the group, particularly India and Brazil, both of which will chair the G20 in the next two years. Hence, it seems like the perfect opportunity to formalise large parts of the services economy to reflect its true size that can be used to design targeted and effective policies. Raising the legitimacy of these services can also be achieved if they are absorbed into the digital space for greater access to a larger proportion of their population. If India takes up this issue during its presidency, Brazil will likely continue the effort in 2024.

• Leveraging macroeconomic measures for inclusive, sustainable, and digital transformation

Macroeconomic policies are typically used to address short-term shocks, but they can also be used to steer the global macroeconomy in a way that fosters desirable structural changes along the lines in previous sections. For example, there are major finance-related issues to supporting a vaccination drive, access to green finance, or driving a digital transformation. Such finance-related issues could be supported through targeted fiscal, monetary, and trade issues. Central banks could more actively support a green transformation (for instance, through liquidity support and stress testing banks), advanced economies could use their SDRs and aid budgets to finance vaccines in the poorest economies, and private sector capital is essential in large infrastructure projects related to digital and green transformation. Trade policies can support a green transformation, provide more equitable access to vaccines, and support digital trade. The G20 could play a lead role in reconciling macro-economic responses with desirable long-term development trajectories.

Conclusion

The global macroeconomic environment is undergoing rapid changes, and the G20 will need to respond. Some macroeconomic policies need to respond to short-term shocks (for example, addressing inflationary pressures) and, in other cases, must accommodate structural shifts, such as green and digital transformation or drive towards complete global vaccination.

Table 1 sets out key macroeconomic issues facing the G20, the core balancing interests, and India’s possible role in advancing these issues. Specifically, India will need to:

Tackling the continued rise in public (and private) debt in the face of increasing borrowing costs;

Keeping rising inflation in check, but in the context of a weaker than expected global economy;

Opening global supply chains while balancing national pressures and domestic needs;

Raising vaccination rates, especially in the poorest parts of the world, to promote a more even recovery;

Financing a green transition in the context of high oil prices and energy crises;

Addressing the digital divide so that everyone benefits from increased use of digital technology, keeping widening inequalities in check; and

Other systematic issues include the voice of emerging market economies in global macroeconomic coordination, wealth and income inequalities, poverty reduction, climate change adaptation, small island states, and food and nutritional security.

Table 1: Global macroeconomic issues and possible roles for India’s G20 Presidency in 2023

Global macroeconomic challenge

Balancing macroeconomic issues

Macro policy instruments under consideration

Possible G20 actions under the Indian presidency in 2023

Increased (public) debt

Supporting households and firms to recover versus higher borrowing costs (and debt sustainability)

Moving towards better targeted fiscal measures

Continue fiscal consolidation and examine debt pressures in the poorest economies

Inflation

High (transitionary) inflation versus a less strong than expected recovery

Balanced / cautious approach towards raising interest rates

Providing limited but targeted liquidity

Continue to highlight a flexible and diversified approach, bearing in mind spillover effects

Inclusive health (vaccination)

Increasing vaccination rates in the poorer countries

Development co-operation to finance and deliver vaccines

India to take lead in push for global vaccination, leveraging global public finance

Green transformation

Access to (cheap) energy and increasing use of renewable energy

Central bank to ease monetary policy to accommodate green finance (e.g. directed liquidity)

Use DFIs and targeted climate finance

Focus on leverage private capital for green transformation

Supply chains

Self-reliance vs production efficiency with higher risks

Trade openness

Pushing for easing of trade restrictions, consolidating supply chain resilience measures, co-operation within the G20, and WTO reform

Digital divide

Improving digital infrastructure in poorest countries

Targeted DFI finance

Further promoting private capital flows to emerging markets and low-income countries; highlighting India’s digital achievements

New shocks (eg impact of Russia–Ukraine)

Disruptions to supply chains, increased inflation, economic impact of sanctions

As democracies, India and UK can work together to address conflict and economic fallout

Voice for emerging market economies in macroeconomic issues

Domestic importance of macro-policies versus negative spillovers

Forward guidance and better collaboration

Keep pushing for emerging market economy voice

The FWG, which India has chaired since its inception, will have a steering role to play during India’s presidency. It has already renewed its commitments to monitor potential risks for the global economy in the aftermath of the pandemic, while discussing the need to harness the digital transformation the world is seeing today.[64]Amidst this, there is a need to address the digital divide that was created due to the pandemic and the digital transformation that followed, both across and within countries. This will require public and private investment in digital technologies, including intangible assets (databases, digital skills, improved cybersecurity) that could spur innovation, employment, and growth. The FWG could mobilise these finances not just for the G20 members but also among low-income countries to speed up economic recovery. Furthermore, the FWG could also play an important role in continuing support for SMEs, women, and youth to enable a more ‘equal’ recovery for all.

India and the UK could work together around the following areas:

Monetary policy:Linking more clearly the need to ensure (i) sufficient liquidity for dealing with the green and digital transformation and supply chain issues (which will contain inflationary pressures), whilst (ii) taking a cautious approach to across-the-board monetary tightening, given the downside risks of the world economy (which would also slow down the green transformation). This would allow for more country-specific and targeted approaches to monetary policy.

Macroeconomic (trade and finance) policy and inclusive health:India and the UK could push for global vaccination, with India producing vaccines and the UK leading on distributional and value chain challenges. Together they need to leverage global public finance more clearly for global public goods. The initiative could be anchored in the broader value chain initiative.

Debt sustainability and fiscal space:A range of countries have defaulted (for instance, Sri Lanka) or are at high risk of default. The coming year is likely to see more defaults, given recent macroeconomic crises. A range of issues will need to be addressed, and the UK and India can take the lead on this. This includes improving the Common Framework and encouraging the IMF to use its entire balance sheet to address debt and crises.

Climate change:Both countries are equipped to lead a collective action to tackle the impact of climate change. The FWG already includes this theme and recognises its importance in ensuring a sustainable future. India is one of the largest emerging markets in the group and can use its unique position to incentivise domestic and international investment, both public and private, to develop new technologies to reduce reliance on fossil fuels and increase the uptake of green projects.

Economic fallout from the Russia-Ukraine conflict:As open democracies, the UK and India value the importance of democracy and avoidance of war. They can also work together to coordinate the G20 around macroeconomic measures to contain the fallout that is expected to play a role throughout 2022 and into the Indian presidency in 2023.

[a]B20 (Business 20) and T20 (Think Tank 20) are G20 engagement groups.

The views expressed above belong to the author(s). ORF research and analyses now available on Telegram! Click here to access our curated content — blogs, longforms and interviews.

Dirk Willem te Velde is Director for International Economic Development at ODI London. He has written extensively on trade investment and economic transformation including in ...

Prachi Agarwal is a Senior Research Officer at International Economic Development at ODI London. She has worked extensively on empirical analysis of trade policy digital ...

PDF Download

PDF Download