Modelling Decarbonisation Pathways for the Indian Economy

This brief explores four scenarios of climate action for India using a systems dynamics model called the Energy Policy Simulator for India. It investigates policy trade-offs and co-benefits and estimates the costs of climate action. It finds that deep decarbonisation in the Indian economy is possible while also boosting jobs and GDP and avoiding millions of premature deaths due to harmful air pollution. The low-carbon transition will require massive investments in power, industry, transport, and hydrogen. Early policy signals could accelerate technology adoption by industry, benefiting from decreasing technology costs.

Attribution:

Varun Agarwal, et al., “Modelling Decarbonisation Pathways for the Indian Economy,” ORF Issue Brief No. 503, November 2021, Observer Research Foundation.

Introduction

For developing countries like India, strong climate action can appear to be a trade-off—one that may come at the expense of robust economic growth. The question that India faces today is this: Will it compromise economic development and job creation if it chooses a low-carbon pathway, or can actions to reduce emissions in different sectors be the foundation of a stronger economy and improved human well-being?

India’s long-term development pathway cannot directly borrow the approaches of other countries. For countries that are already industrialised, tackling the challenge of climate change requires decarbonising the existing infrastructure and moderating high consumption. For India, on the other hand, it means creating new green energy infrastructure that meets the needs of its population without locking into fossil-fuel path dependence. For instance, the International Energy Agency’sIndia Energy Outlook 2021notes that 60 percent of India’s carbon dioxide emissions in 2040 are projected to come from infrastructure, buildings, factories, vehicles and appliances that do not yet exist, pointing to the opportunity to build cleaner. India will also need to plan for transition in the global economy away from fossil fuels, which will cause shifts in technologies, cost and availability of capital, competitiveness, prices, and employment. As India explores a net-zero emissions future, recent studies have shown the daunting scale of this challenge. Such studies, however, do not always model the macroeconomic implications of climate policies. For example, what could be the impact of climate policies on GDP and jobs? Will the savings in fuel costs, energy imports, improved health, and reduced climate damages outweigh the upfront capital costs? How will a carbon tax affect the government’s finances and consumers’ cash flow?

The Energy Policy Simulator for India (EPS-India), a free and open-source systems dynamics model for the period 2020–50,[i]explores such trade-offs and economy-wide effects. Created by Energy Innovation LLC and adapted for India in partnership with World Resources Institute India, the EPS-India uses publicly available data and offers hundreds of environmental, economic, and social outputs. Its interactive web interface allows users to create their own policy scenarios with various combinations of policy implementation levers across sectors.

Climate Action Scenarios for India

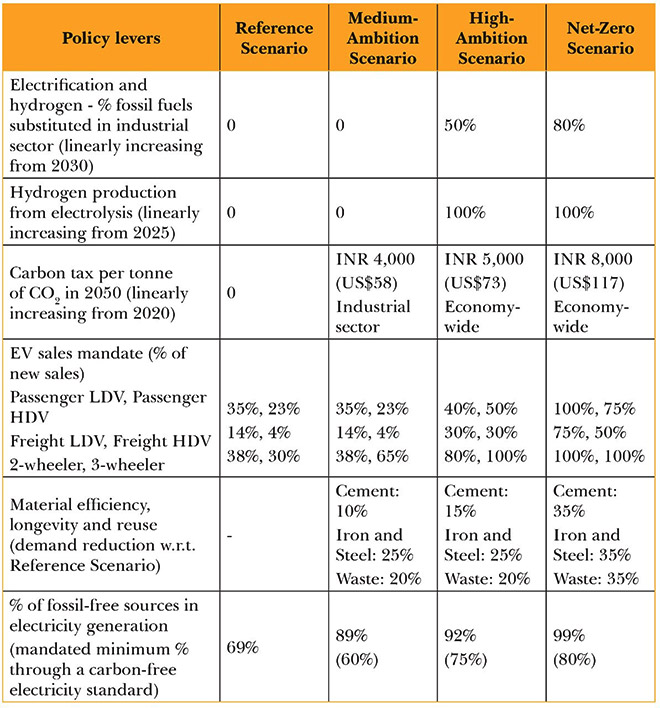

Through literature review and expert consultations held during 2019–21, the authors of this brief created four scenarios of climate action for India (See Table 1).

Reference Scenario,which includes India’s ongoing efforts in renewable energy (RE), energy efficiency, and electric mobility, and cost-optimisation of technologies in the electricity and transport sectors.

Medium-Ambition Scenario,which includes sectoral policies that align with India’s first Nationally Determined Contribution (NDC) and Sustainable Development Goals (SDGs) targets for 2030, but does not aim for more ambitious decarbonisation in the long term.

High-Ambition Scenario,which includes sectoral policies with high potential for GHG mitigation over the long term, including currently nascent technologies such as hydrogen and battery storage. Policies with proven technologies are phased in linearly from 2020 to 2050, while those relying on nascent technologies are phased in starting from 2025 or 2030.

Net-Zero Scenario, which further raises the policy settings in the High Ambition Scenario to achieve deep decarbonisation over the long term. For example, as given in Table 1, switching to electrification and hydrogen in industry is increased from 50 percent of fossil fuel use in the High Ambition Scenario to 80 percent in the Net-Zero Scenario; carbon tax is raised from INR 5000 (US$78) per tonne of CO2to INR 8,000 (US$117) per tonne of CO2by 2050; EV sales mandate for cars is raised from 40 percent to 100 percent by 2050. Carbon capture and storage is not used in the Net-Zero Scenario.

The model assumes falling technology costs based on a combination of projected global prices and endogenous learning. It finds the least cost options in the electricity and transport sectors, subject to specified policy mandates. All monetary estimates are in 2018 constant prices (1 US$ = 68.42 INR).

Table 1: Key Policy Levers Assumed in 2050 in Four Climate-Action Scenarios for India

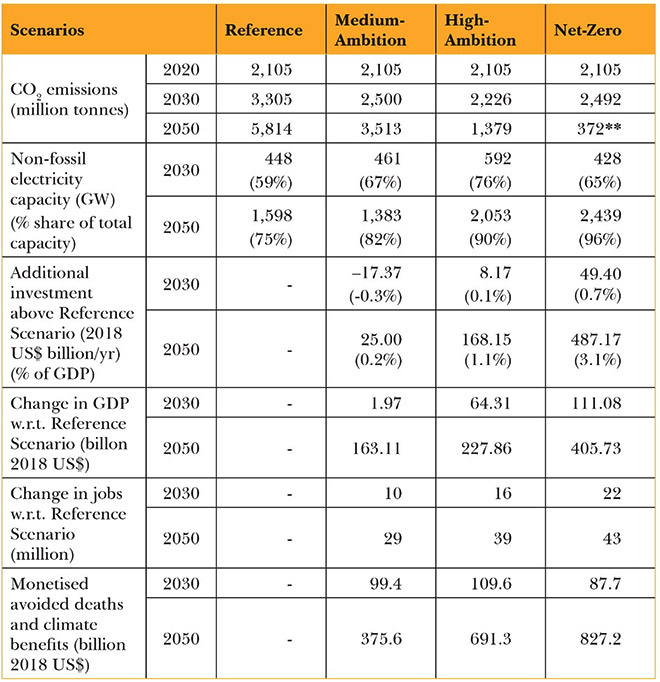

The Medium-Ambition, High-Ambition, and Net-Zero Scenarios yield better outcomes than the Reference Scenario in terms of CO2emission reduction, health co-benefits, and macroeconomic impacts (See Table 2).

Table 2: Key Outcomes in Four Climate Action Scenarios for India

**No Carbon Capture & Storage (CCS) assumed in Net Zero Scenario

Climate and Health Benefits

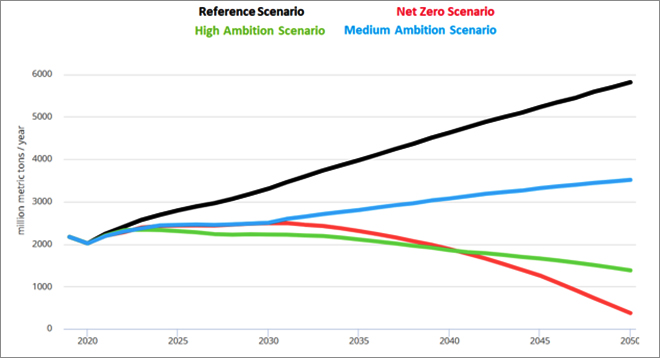

Sectoral decarbonisation policies, implemented together, can significantly reduce emissions, both in the medium term and in the long term (See Figures 1 and 2).

In the Medium-Ambition Scenario, the key policy drivers for emissions reductions are the implementation of a carbon tax and industrial energy efficiency standards and the reduction of demand for cement and iron and steel through material efficiency, longevity and re-use.

In the High-Ambition Scenario, the key policy drivers for emissions reductions are switching from fossil fuel in industrial facilities to a mixture of electricity and hydrogen; production of hydrogen through electrolysis supported by carbon-free electricity generation, and early retirement of otherwise non-retiring coal plants. The early coal-retirement policy can be particularly impactful in the earlier years if implemented from 2021, retiring all pre-existing coal capacity by 2032. In this scenario, CO2emissions fall to 1,379 million tonnes in 2050.

In the Net-Zero Scenario, the key policy drivers for emissions reductions are switching from fossil fuel in industrial facilities to a mixture of electricity and hydrogen; production of hydrogen through electrolysis supported by carbon-free electricity generation; an economy-wide carbon tax; and electric vehicle (EV) sales mandates. In this scenario, CO2emissions fall to 372 million tonnes in 2050, without using CCS.

No new coal capacity is added after 2024 in the Medium-Ambition, High-Ambition, and Net-Zero Scenarios due to the increasing cost-competitiveness of RE technologies as well as a carbon-free electricity standard policy, which mandates a minimum percentage of electricity generation from fossil-free sources—60 percent in the Medium-Ambition Scenario, 75 percent in the High Ambition Scenario, and 80 percent in the Net-Zero Scenario.

Figure 1: CO2Emissions in Different Scenarios (Million Tonnes)

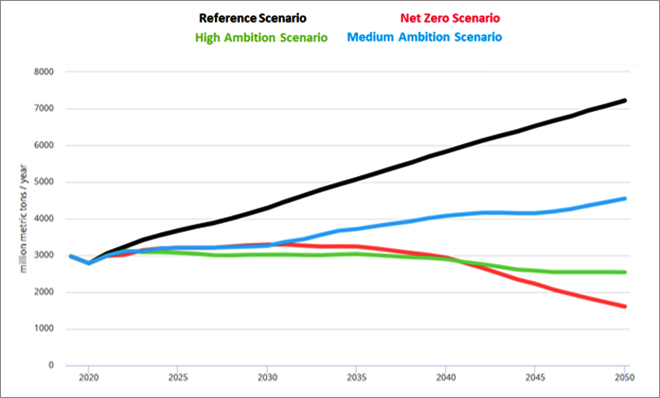

Figure 2: GHG Emissions in Different Scenarios (Million Tonnes)

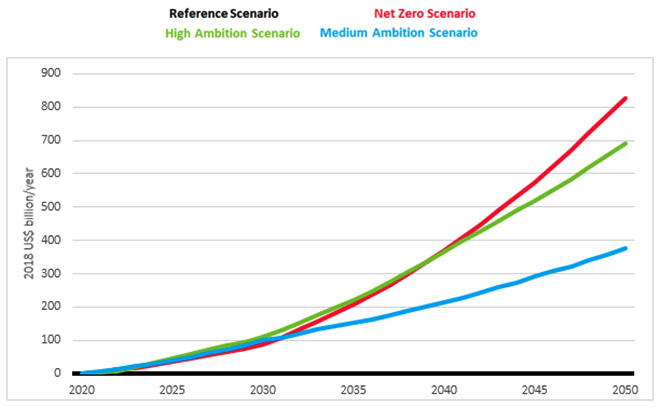

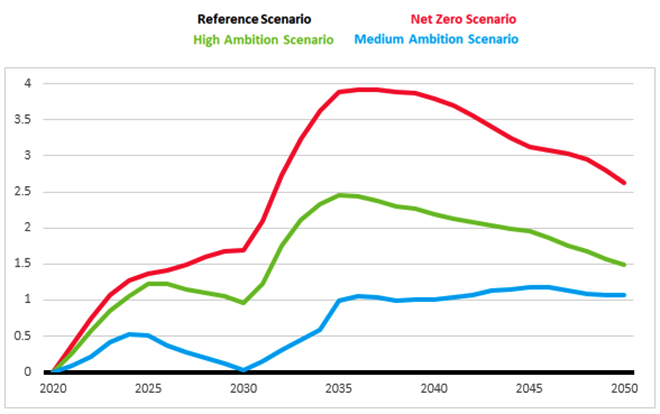

Figure 3: Monetised Avoided Deaths and Climate Damages Relative to Reference Scenario (2018 US$ Billion/Year)

Moreover, these climate policies will yield significant health co-benefits, preventing premature deaths due to air pollution over 2020–50—9.9 million in the Net-Zero Scenario, 9.4 million in the High-Ambition Scenario, and 5.7 million in the Medium-Ambition Scenario. The estimated monetary value of avoided premature deaths and avoided climate damages amount to US$827 billion in 2050 in the Net-Zero Scenario, US$691 billion in the High-Ambition Scenario, and US$376 billion in the Medium-Ambition Scenario (all in 2018 prices). Cumulatively, over the 30-year period from 2020 to 2050, this adds up to US$8,789 billion in the Net-Zero Scenario, US$8,329 billion in the High-Ambition Scenario, and US$5,073 billion in the Medium-Ambition Scenario (all in 2018 prices)[ii].

Strategic Sectoral Interventions

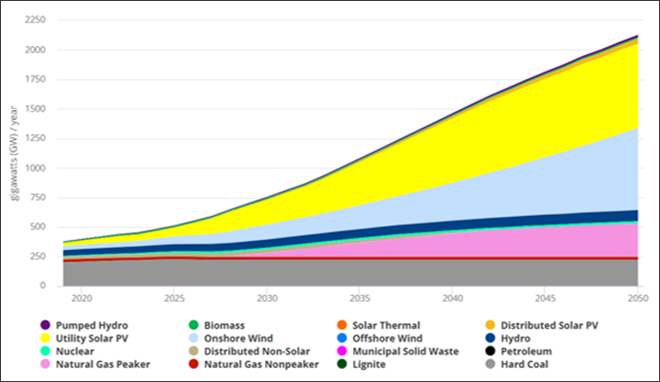

Due to the falling costs of variable RE generation technologies (i.e. utility-scale onshore wind and solar PV), the Reference Scenario already includes a significant amount of RE capacity. In 2030, the installed capacity of variable RE and large hydro together amount to about 410 GW, suggesting that market-driven progress alone might not be sufficient to achieve India’s ambitious target of installing 450 GW RE capacity by 2030. The share of non-fossil sources (i.e. utility-scale solar PV, wind, hydro and nuclear) in the capacity mix reaches 57 percent in 2030 and 72 percent in 2050 in the Reference Scenario. In terms of electricity generation, nearly 70 percent of the electricity generated in 2050 is from non-fossil sources in the Reference Scenario. In the Net-Zero Scenario, this goes up to 99 percent in 2050. This is important to achieve the mitigation potential of policies that rely on the availability of green electricity, such as electrification in industry, production of hydrogen via electrolysis, and EV sales mandates. Focus on energy storage and grid flexibility will be required to successfully integrate the growing share of variable renewable energy.

Figure 4:Installed Electricity Capacity in Reference Scenario

In India, the industry sector is crucial for decarbonisation and requires three key policies for the medium to long term.First, an industrial energy-efficiency roadmap, to strengthen and widen the coverage of the Perform–Achieve–Trade (PAT) energy trading scheme and to create incentives for investment in new energy-efficient technologies, particularly for energy-intensive products such as fertilisers.Second, guidelines for material efficiency for the construction sector, the certification and creation of formal markets for sustainable building materials, and financial incentives for the use of such materials (e.g. a lower goods and services tax), to realise the targeted reduction in the demand for emissions-intensive industrial products such as cement and steel.Third, the use of hydrogen as a fuel, which emerges as key to emissions reduction in the long term and is particularly important for decarbonising hard-to-abate parts of the industry and freight transport sectors. While this is currently at a nascent stage in India, the National Green Hydrogen Mission should create incentives for technology investments for fuel-switching in the private sector, develop hydrogen distribution infrastructure, and work on grid improvements to increase transmission and storage capacity for industrial-scale production of green hydrogen.

Financing the Low-Carbon Transition

The low-carbon scenarios have high capital expenditures on the deployment of clean technologies, but in the medium to long term, they yield increasing cost savings, primarily from reduced expenditure on fuels. The estimated savings in 2050 amount to US$911 billion in the Net-Zero Scenario, US$965 billion in the High-Ambition Scenario, and US$273 billion in the Medium-Ambition Scenario (all in 2018 prices) relative to the Reference Scenario. For instance, the reduction in energy import expenditure is depicted in Figure 5.

Figure 5: Energy Import Expenditure (2018 US$ Billion/Year)

The power sector undergoes a fundamental shift in the High Ambition and Net Zero Scenarios. For example, annual additions of solar- and grid-battery storage capacities increase eight-fold, and of onshore wind capacity increase six-fold by 2050. Annual costs incurred for these technologies could rise from 2.6 percent of the GDP in 2020 to 4.8 percent peak in 2035, thereafter moderating to around 2.5 percent of the 2050 GDP in the Net-Zero Scenario. Annual cost of hydrogen electrolysers for heavy industry decarbonisation quintuples in 15 years to around 0.1 percent of the 2035 GDP and around 0.35 percent of the 2050 GDP. Within heavy industry, significant investments will be required in steel and cement.The additional capital expenditure for new technology deployment in the Net-Zero Scenario can amount to US$828 billion over the next 15 years and US$5.6 trillion over the next 30 years (above the Reference Scenario).[iii]These magnitudes may seem astonishing, but the annual incremental CapEx amounts are no more than 1.8 percent of the 2035 GDP (US$160 billion) and three percent of the 2050 GDP (US$490 billion). Moreover, a steep and steady decline in expenditures on operation, maintenance and fuels fully outweighs the annual incremental CapEx costs as early as 2035 (–US$120 billion) in the Net-Zero Scenario. In 30 years, such fossil-fuel-linked expenditure reductions could amount to as much as US$1.4 trillion, illustrating that India’s gains from earlier decarbonisation can be very large.

Operating and maintenance expenditures, coupled with the lowering of fossil-fuel costs, increasingly defray the costs of capital investments almost halfway to 2035, accelerating the pace to 2050 and releasing internal financing resources. Further, technology costs will fall with adoption through economies of scale and diffusion over time.

In the global climate-action and macroeconomic context, the capital for clean project financing is abundant and at reasonable pricing. Domestic macroeconomic conditions are favourably poised for both private- and public-sector borrowings.The decarbonisation pathways are mainly private-sector-led, responding to policy incentives including the carbon tax. There are no fiscal implications from subsidies. A 30 percent capital subsidy for rooftop solar is largely offset by reduction in fuel subsidies due to the diminishing use of LPG and natural gas.

Boost to GDP and Employment

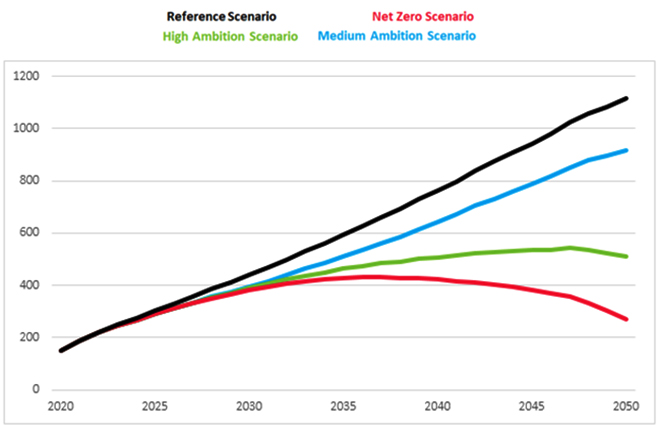

The overall effect of the low-carbon transition on India’s economic growth is positive. The GDP in 2050 is projected to be higher than the Reference Scenario by US$406 billion in the Net-Zero Scenario, US$228 billion in the High-Ambition Scenario, and US$163 billion in the Medium-Ambition Scenario (all in 2018 prices). The net positive impact is mainly due to three factors: fresh, additional investments in new technologies and capacities; cheaper RE, transport and maintenance and operation expenses; and a net increase in demand induced by consumption and employment.

The reduction in high-carbon sectors is led by mining and quarrying (particularly coal mining) and manufacturing of coke and refined products. This loss of output is largely recouped by the gain in value-added share of electricity generation and utilities, driven by greater electrification and a clean energy shift. Heavy emitter industries such as Iron and Steel, as well as Cement, which bear major costs of carbon abatement, could together lose marginal value-added share in 30 years.

The motor vehicle manufacturing segment is not adversely impacted by the transition; however, significant within-sector changes due to a shift from internal combustion engine vehicles to EVs will entail costs, changes in business processes, supply chains and skill requirements. Transport and storage, and trade, retail, and repair sectors—which have extensive ancillary linkages to the automobile sector—may shrink marginally by 2050.

Figure 7: Percent Change in GDP Relative to Reference Scenario

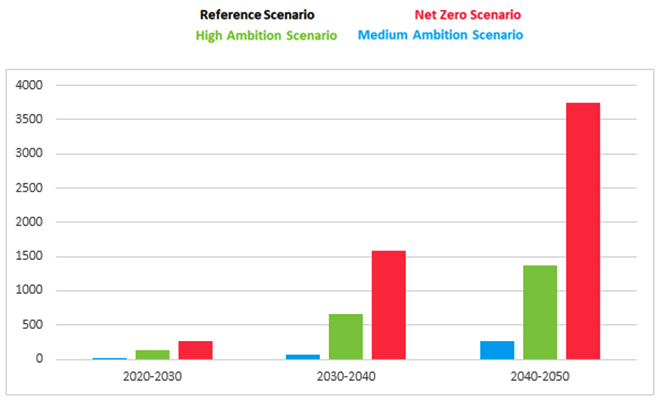

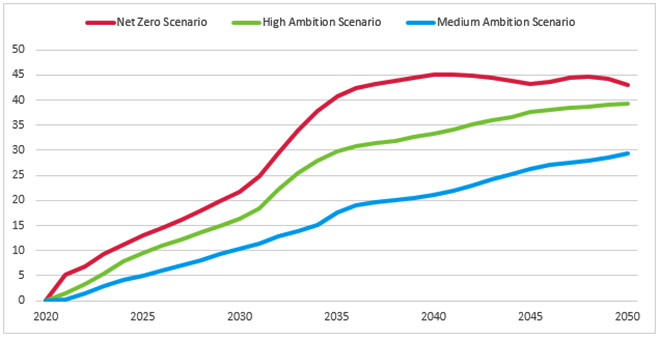

Coal mining, and coke and refined products, are likely to see a reduction in numbers employed (direct and indirect) throughout the 30-year period. Net jobs lost in coal mining relative to the Reference Scenario could be an additional 0.34 million in 2030 and 1.49 million in 2050. The net job reduction in coke and refined petroleum products, which is capital-intensive, could be 0.03 million in 2030 and 0.19 million in 2050. The fossil fuel and utility sector, too, could witness job losses, but these losses will be balanced by job gains in the expansion of clean electricity utilities due to increased electrification in industry, transport, and buildings. Maintenance and repair of motor vehicles, transportation and storage sectors could witness reductions in direct jobs in the transition but these will be offset by an increase in induced jobs.In all three low-carbon scenarios, there is a significant net increase in jobs relative to the Reference Scenario. The Net-Zero Scenario has 22 million more jobs by 2030 and 43 million more jobs by 2050 than the Reference Scenario. These include direct jobs (created in an industry due to climate policies), indirect jobs (created within industries that supply the directly affected industry), and induced jobs (created by re-spending of money paid to workers or government because of the growth of the affected industry). The net increase in jobs is predominantly driven by induced economic activity. However, while the employment impact is net positive at the macro level, there could be losses within specific sectors and cross-sector shifts that may not be spatially matched or evenly balanced.[iv]

Most of the new jobs are likely to be created outside the “losing” sectors, due to concomitant shifts in supply and demand, the expansionary effect of induced demand originating from new activities, and larger boosts from cost-savings in the later years.

Figure 8: Change in Direct, Indirect and Induced Jobs (Millions) Relative to Reference Scenario

Role of Carbon Tax

It is possible for India to achieve deep decarbonisation in the economy while also boosting jobs and the GDP. However, carbon taxes will play a key role in this. A carbon tax increased in a phased manner over time will be pivotal to offsetting shortfalls in government tax revenue from petroleum products (engendered by the reduction in overall fossil fuel use with time). This can be applied on fuels based on their CO2emissions and process emissions. The assumed carbon tax rate for the industry in the short term closely reflects the trend of the rising cess on coal.

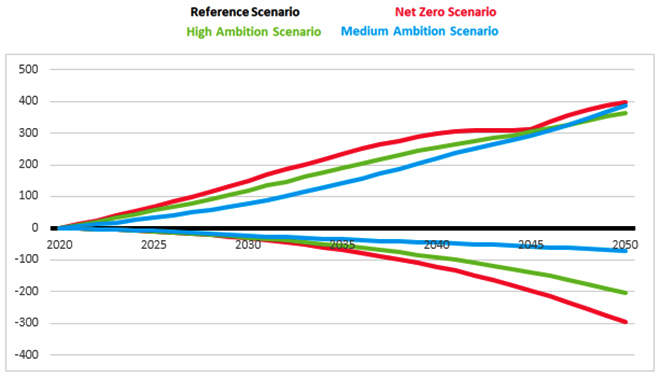

Most decarbonisation policies tend to displace fossil-fuel use with carbon-free alternatives. Thus, given the associated shortfalls in tax revenues from petroleum products, it is crucial to explore alternate mechanisms for revenue generation for the government. An effectively designed carbon tax in the industry and electricity sectors, implemented while the transition from fossil fuels to clean energy is still underway, can be particularly useful in augmenting government revenues and mitigating potential trade-offs in the economy. Under the various low-carbon scenarios, by 2050, as fossil fuel tax revenue falls by 0.5–1.9 percent of GDP, as compared to the Reference Scenario, carbon tax revenue grows by 2.4–2.6 percent. Redirecting carbon tax revenues towards government spending can, therefore, mitigate the negative impact on induced economic activity, resulting from a significant reduction in government expenditure.

However, carbon pricing must be carefully designed for the equitable balancing of contributions from households, businesses and taxpayers. In the Reference Scenario, a carbon tax is applied on top of already existing petroleum product taxes. The government can first explore alternate mechanisms such as the optimal utilisation of various cesses collected across sectors to reduce the high reliance on fossil-fuel tax revenues. Some components of the current fossil-fuel taxes can be subsumed or redesignated as a carbon tax, but a judicious balance must be struck by keeping in mind the overall cost burden of decarbonisation upon heavy industry, so as to not disincentivise clean-energy adoption. Subsequently, government income can be further augmented through an additional carbon tax to induce economic activity and create additional jobs.

Figure 9. Change in Carbon Tax Revenue and Fossil Fuel Tax Revenue (2018 US$ Billion) Relative to Reference Scenario

Ensuring a Just Transition

In India, climate change is one of multiple stressors and policy priorities, and the focus of climate action has rightly been on the co-benefits for the local environment and human well-being. There is a need, however, to give serious consideration to the challenges and potentially adverse social impacts that climate action might have.

India’s RE and EV targets are quite ambitious and will require significant investments in nascent technologies, developing a manufacturing base, ensuring mineral security, and judicious use of land.

It will be necessary to manage job losses in fossil fuel-based industries and provide social protection and safety nets in occupations that are directly at risk from low carbon policies. Further, India will need to ameliorate regional and gendered disparities in access to skills and finance for new green livelihood opportunities emerging in sectors such as RE, EVs, green buildings, recycling, and land restoration. Special attention will have to be given to the quality of jobs in terms of formal contracts, social benefits, job security, unionisation, etc., especially considering the large share of the informal micro, small, and medium enterprises sector in India. Since job gains will occur in different states and sectors than job losses, coordinated policies by the central and state governments will be imperative.

While the economic ramifications of low-carbon policies will benet positive, they will need to be carefully managed for their effects on vulnerable communities. For example, a carbon tax on the truck and rail transport of goods could have a ripple effect on prices. The withdrawal of free electricity for farmers to rationalise the use of electricity for irrigation could further increase the cost of cultivation. Without revenue recycling, carbon taxes on power generation could make modern energy services unaffordable for poorer households.

Conclusion

Currently, all potential low-carbon scenarios yield better economic outcomes than the Reference Scenario. Deep decarbonisation in the Indian economy is possible while also boosting jobs and GDP and avoiding 9.9 million premature deaths due to harmful air pollution over the next three decades. The low carbon transition will require massive investments in power, industry, transport, and hydrogen. However, it can be ensured that government revenues are neutral, with carbon taxes playing a key role in realising the positive economic impacts on India’s GDP and jobs. To be sure, subsidies play a small role, and the transition is primarily driven by industry response to policies such as the carbon tax. Early policy signals (e.g. mandates for renewable energy, electric mobility, and industrial fuels) could accelerate technology adoption by industry, benefiting from decreasing technology costs.

As India moves towards a low-carbon model, the workforce transition will need to be managed carefully over time. With thoughtful policies that build human capital, make prudent investments, and provide social safety nets, the low-carbon transition can also be ajust transition.

Varun Agarwalis Senior Program Associate – Climate, World Resources Institute India.

Anshu Bharadwajis Chief Executive Officer at Shakti Sustainable Energy Foundation (SSEF), provides leadership guidance and advisory policy support towards energy and environmental sectors programmes.

Shubhashis Deyis Director (Climate Policy) and leads SSEF’s Climate Policy, Clean Energy Finance and Energy Efficiency Programmes.

Ulka Kelkaris Program Director – Climate, World Resources Institute India.

Renu Kohliis an independent economist, previously with the Indian Council for Research on International Economic Relations, International Monetary Fund, and Reserve Bank of India.

Nidhi Madanis Senior Programme Manager (Climate Policy) at SSEF and works on low carbon development and land-use aspects.

Koyel Kumar Mandalis Chief of Programmes at SSEF and responsible for managing all programme verticals such as power, transport, energy efficiency and climate policy.

Apurba Mitrais Program Head – Climate policy, World Resources Institute India.

Deepthi Swamyis Consultant, Climate program, World Resources Institute India.

This brief was first published in ORF’s monograph, Shaping Our Green Future: Pathways and Policies for a Net-Zero Transformation, November 2021.

[ii]This uses estimates of the Social Cost of Carbon and the Value of a Statistical Life for India.

[iii]This assumes no discounting of investments made in the future.

[iv]The macroeconomic impacts in the model are calculated based on the transaction relationships between the industries in the economy in India’s input-output (I/O) tables, as of 2015. The future impacts are based on the static industrial classifications considered in the 2015 I/O table and are assumed to not change over time.

The views expressed above belong to the author(s). ORF research and analyses now available on Telegram! Click here to access our curated content — blogs, longforms and interviews.

Anshu Bharadwaj is Chief Executive Officer at Shakti Sustainable Energy Foundation (SSEF) provides leadership guidance and advisory policy support towards energy and environmental sectors programmes.

Renu Kohli is an independent economist previously with the Indian Council for Research on International Economic Relations International Monetary Fund and Reserve Bank of India.

Koyel Kumar Mandal is Chief of Programmes at SSEF and responsible for managing all programme verticals such as power transport energy efficiency and climate policy.

PDF Download

PDF Download