Health systems in the BIMSTEC and East Africa: Current and future engagements

Rajeev Ahuja

The BIMSTEC and East Africa, which together account for 25 percent of the world’s population, are low-resource regions.[1]While their share in the global disease burden is disproportionately high, their combined healthcare expenditure is a minuscule share of the global healthcare spend. Their health systems are underfunded, understaffed and ill-equipped to deal with the monumental challenge of disease burden. This paper aims to compare the healthcare systems of the BIMSTEC and East Africa blocs, to explore opportunities for learning and exchange, trade and investment, and partnerships between the two regions. While trade and investment mostly flow from the BIMSTEC to East Africa, there is scope for mutual learning between the two regions. The engagement must be guided by strategic, long-term goals as markets in both regions will mature over time. In the long run, the BIMSTEC’s engagement in East Africa can also create a gateway to the pan-African market.

Attribution:

Rajeev Ahuja, “Health Systems in the BIMSTEC and East Africa: Current and Future Engagements”, ORF Occasional Paper No. 197, June 2019, Observer Research Foundation.

Introduction

The five countries of East Africa (Ethiopia, Kenya, Mozambique, Rwanda and Tanzania) and the seven that comprise the Bay of Bengal Initiative for Multi-Sectoral Technical and Economic Cooperation (BIMSTEC—Bangladesh, Bhutan, India, Myanmar, Nepal, Sri Lanka and Thailand) share certain similarities. The two regions have comparably low per-capita incomes, large informal sectors, low urbanisation, high disease burdens, low health spending, mixed health systems, and lower ranking on the human development index (HDI). At the same time, the two regions are dissimilar in certain aspects: compared to the BIMSTEC countries, East Africa has a less diversified economy, lower levels of development, a significantly higher burden of communicable diseases (CDs), a lower average life expectancy, lower literacy levels, and higher poverty rates.

Africa’s population is expected to double by 2050, reaching a total of 2.4 billion people—that is more than half the world’s population growth between 2015 and 2050. East Africa is the fastest growing subregion in the African continent. While such demographic growth presents opportunities, it also poses challenges, particularly if basic healthcare is not met for this large population.[2]

There is thus significant scope for the BIMSTEC to engage with Africa, especially for India, which accounts for 80 percent of the BIMSTEC’s population and 75 percent of its economy.[3]The faster-growing regions in Africa are expected to invest more in the health sector. While it will be a slow process, the current engagement with the region must be guided by this longer-term vision. Pharmaceuticals, medical education and training, digital health, and knowledge-sharing and exchange are some of the areas where deeper engagement can be pursued. While opportunities for the delivery of healthcare services are currently limited due to the acute shortage of health professionals, which is a slow-moving constraint, some sporadic opportunities may still exist.

India has significant health-sector engagements across Africa in the area of pharmaceuticals and is a major supplier of these products in the region. India’s export of pharmaceutical products to Africa increased from US$247.64 million in 2000 to US$3.5 billion in 2014.[4]Its Foreign Direct Investment (FDI) in the African pharmaceutical industry was estimated at US$246 million cumulatively between 2008 and 2014.[5]Barring Rwanda, all countries in the East Africa region are amongst the major recipients of India’s investments in pharmaceuticals. India has also emerged as a popular destination for medical tourism for African citizens. Many African countries view India as a reliable partner and are seeking its aid in the health sector, in areas such as medical education and training, treatment of specific diseases, and development and management of hospitals and diagnostic centres.

While the current level of health-sector engagement between India and Africa is significant and growing, there is still much unexplored potential. East African nations, as well as other African countries, are important emerging markets. Engaging with East Africa now will provide an entry point for India to access other African countries in the future, which will likely constitute a lucrative market as the “African rising” story unfolds over the coming decades.

Section 1 of this paper compares the BIMSTEC and East Africa in terms of disease burden, healthcare financing, human resources for health, and digital health. Section 2 discusses the need to align the private sector with the public health agenda. Section 3 focuses on knowledge-sharing and exchange. Section 4 discusses the current partnerships and collaborations. The paper concludes with Section 5.

I. BIMSTEC and East Africa: A Brief Comparison

The BIMSTEC and the East African regions fall on the lower end of the per-capita income scale and rank low on the HDI. With the exception of Thailand and Sri Lanka, the countries in these regions rank higher than 100 on the HDI, with the BIMSTEC faring better than East Africa, both on the per-capita income scale and on the HDI. In East Africa, Kenya is the most advanced country and its socioeconomic indicators are the closest to those of the BIMSTEC members. This pattern is reflected in health-sector indicators too, as shown in Graphs 1 and 2.

1.1 Disease Burden

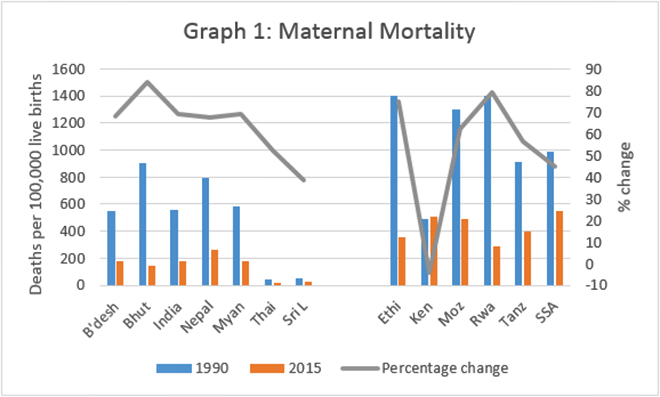

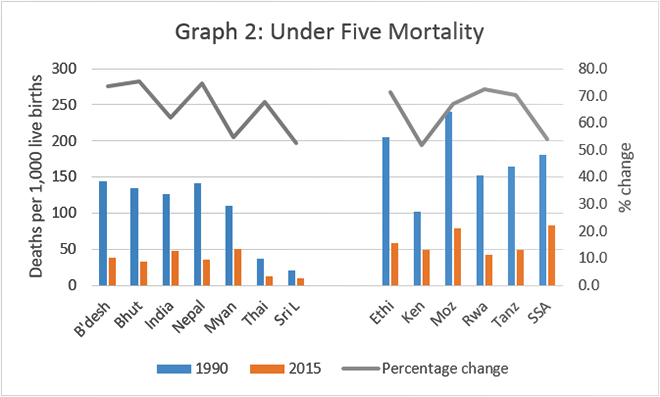

The burdens of communicable diseases, and maternal and perinatal conditions permeate East Africa, despite the region’s notable progress since 1990 in reducing maternal and child deaths (see Graphs 1 and 2).

Source: “Trends in Maternal Mortality 1990–2015,” WHO, 2015.Source: “Levels and Trends in Child Mortality,” UN Interagency Report, 2015.

A few important observations can be made from Graphs 1 and 2. One, even though both regions have made considerable progress in reducing maternal mortality rate (MMR) and under-five mortality (U5M) between 1990 and 2015, the BIMSTEC bloc continues to perform better. Two, East Africa performed better than Sub-Saharan Africa (SSA) averages in both the indicators. Three, significant variation exists within these regions, with some countries doing better than the others. Finally, in the East African region, Kenya is the only country where the MMR has increased, albeit marginally, which is unusual.

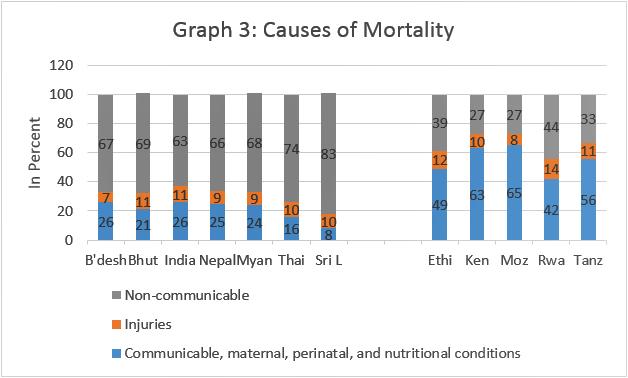

The nature of healthcare needs in the two regions will be determined by their current and emerging disease burdens. Amongst the countries in East Africa, the share of mortality due to communicable, maternal, perinatal and nutritional conditions is the lowest in Rwanda (42 percent) and highest in Kenya (63 percent). In the BIMSTEC, on the other hand, this share ranges between 21 percent to 26 percent in five out of the seven countries. This share is even lower in Sri Lanka (eight percent) and Thailand (16 percent) (See Graph 3).

Source: Non-communicable Diseases, Country Profiles, WHO 2018.

Given the disproportionate burden of CDs in East African nations, their health systems give less priority to NCDs. However, the burden of NCDs is likely to increase in the future, even as the countries try to tackle CDs and address maternal- and child-health conditions. The early detection and management of NCDs is far more cost-effective than treating them at an advanced stage. Thus, it is crucial for East Africa to invest in NCDs. It can learn some useful lessons from the BIMSTEC members that are successfully dealing with CDs and treating NCDs, particularly Thailand and Sri Lanka.

There is a lack of data on the correlation between change in age-specific mortality or morbidity and the change in the population pyramid. However, certain broad trends can be inferred from the changing population pyramid in both regions. For example, by 2040, the BIMSTEC region will have a much higher elderly population (60 and above) than the East African region (16.1 percent in BIMSTEC versus 6.9 percent in East Africa). This has implications for not only making provisions for elderly care but also pursuing a development path that is pro-elderly. On the other hand, the population in the 0–14 age bracket will be significantly lower in the BIMSTEC region than in the East African region (20.6 percent versus 33.7 percent) by 2040. This, too, has implications for tackling early childhood-related diseases.

The extent to which any country is able to meet the healthcare needs of its population is dependent on its healthcare system. Certain well-known building blocks of the system include healthcare financing, human resources for health (HRH), the organisation of healthcare delivery systems, and the extent of technology used. The following section looks at some of the building blocks of the health systems in BIMSTEC and East Africa.

1.2 Health-Sector Financing

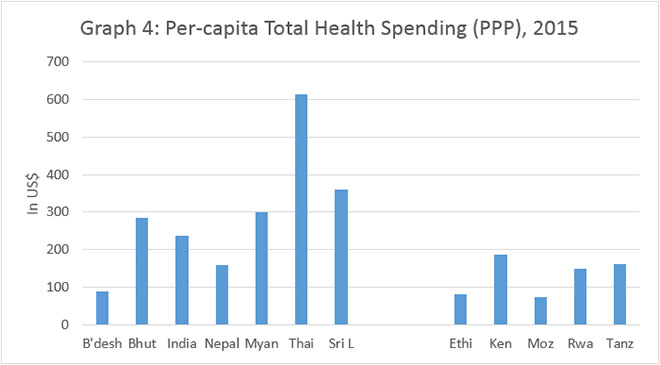

The per-capita total health spending in terms of purchasing power parity is generally low in both the regions, with the average per-capita spending in the BIMSTEC being almost twice as high as that in East Africa at US$240 and US$122, respectively. However, there is significant variation within these regions, with Bangladesh spending as low as US$90 per capita and Thailand spending US$614 per capita in 2015. Amongst the countries in East Africa, Mozambique spent US$73 while Kenya spent US$187 in 2015 (see Graph 4).

Source: “Financing Global Health Database 2017,” IHME, University of Washington.

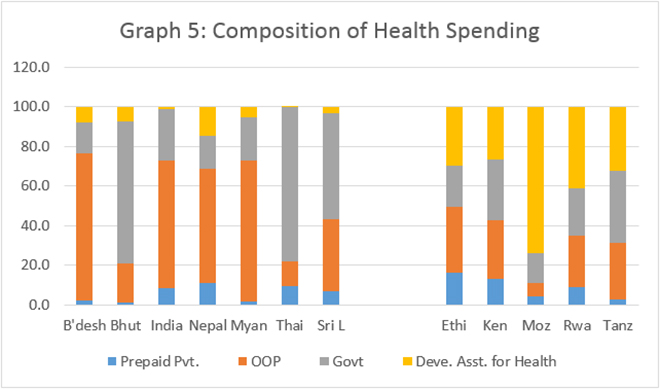

In terms of the composition of this spending, the average out-of-pocket (OOP) expenditure constitutes a bigger share in the total health spending in the BIMSTEC than in East Africa, while the share of development assistance for health is higher in the latter. This is consistent with the trends observed globally across countries of different income groups, i.e. OOP expenditure forms a higher share of healthcare spending in lower-middle-income countries than in low-income countries.

Source: “Financing Global Health Database 2017,” IHME, University of Washington.

In 2001, all African countries committed to the Abuja Declaration and pledged to spend at least 15 percent of their public budgets on health. A few countries have already succeeded in meeting this commitment. With higher economic growth expected in both regions, public health spending should also increase in a commensurate manner.[6]

Countries with substantial pooled spending progress faster on the universal health coverage (UHC) front. Thus, reducing the share of OOP health expenditure is crucial in both the regions. In SSA, the average OOP spending accounts for 36 percent of the current healthcare expenditure, compared to only 22 percent in the rest of the world. Similarly, external assistance contributes a large share (14 percent) of funding in SSA, compared to less than one percent in the rest of the world.[7]Domestic mandatory prepayment financing (tax and mandatory insurance) constitutes, on average, 35 percent of the healthcare financing in SSA. This share must be increased, along with the share of voluntary health insurance schemes, of which there are currently very few.

Reducing the share of OOP expenditure is an urgent need in at least in five of the seven BIMSTEC members as well. Insufficient public health spending, along with a high share of OOP spending, contributes to health-system inefficiencies and inequitable health outcomes. To address these issues, initiatives such as government-sponsored health-insurance schemes (e.g. in India) are worth emulating. Rwanda, too, holds some lessons for both regions, with its success in providing significant financial-risk protection through the sustained development of its national health-insurance system.

1.3 Drugs and Pharmaceuticals

Most African countries face the problems of inadequate supplies of pharmaceuticals, heavy reliance on the import of drugs, fragmented supply chain and distribution channels and, above all, the circulation of counterfeit drugs and substandard medicines. The size of Africa’s pharmaceutical industry is anywhere between one and two percent of the global share, and its local production cannot meet the continent’s health needs. Therefore, most African countries import roughly 70 percent of medicines and 95 percent of active pharmaceutical ingredients.[8]The market value of the African pharma industry is expected to be around US$40–65 billion by 2020[9]and is likely to grow at an unprecedented rate, riding on the wave of the increasing purchasing power of its citizens that will come with economic growth.

In the BIMSTEC region, India has emerged as a major global player in pharmaceutical production. The Indian pharma industry was valued at about US$30 billion in 2015. Of this, nearly 55 percent is exported while 45 percent is domestic. Indian pharma ranked third in the world in terms of volume and is amongst the top 14 countries in terms of value. This highly competitive industry is expected to reach US$55 billion by 2020, with over 3,400 companies registered in 2014–15. Around 170 large players in the organised sector account for 80 percent of the market. Between April 2000 and March 2016, India received approximately US$14 billion in FDI in the drugs and pharmaceuticals sector. India allows for 100 percent FDI in pharmaceuticals under the automatic route.[10]

Indian pharma manufactures generics or branded generics[11]and branded formulations. The Indian generics market was valued at US$21 billion in 2015. Generics account for 82 percent of the country’s market share in value and 90–95 percent in volume. Further, India contributes 20 percent of the world exports in generics and is known for producing cost-effective drugs of acceptable quality. India’s second-largest export to Africa, by value, was of pharmaceuticals (US$3 billion) in 2014–15, with products worth US$704 million exported to East Africa. In the same year, however, India’s pharma export to the other BIMSTEC members was valued higher, at US$807 million.

Demand for pharmaceutical products is expected to increase over the coming years in both regions. To encourage local production, Africa has come up with the Pharmaceutical Manufacturing Plan for Africa (PMPA) to help member countries establish efficient pharmaceutical production guidelines. Local production will help African nations diversify their economy,[12]develop more reliable sources of pharmaceutical supplies, generate jobs and meet their public health goals.[13]Moreover, setting up local manufacturing units in Africa will lower cost, as compared to importing pharmaceutical ingredients. Ethiopia was the first country to create a National Strategy and Plan of Action for Pharmaceutical Manufacturing (2015–25).

Indian generic drug companies stand to benefit significantly by investing in Africa. Pharmaceutical manufacturers can directly set up units in Africa instead of merely exporting finished products, which will benefit both sides. However, such a system will require investments to create a pool of human resource trained in technical and marketing skills, currently in short supply in Africa. The Indian pharmaceutical industry must act swiftly and work with the government to create a favourable policy environment in Africa, to prevent other countries from hogging the opportunity, for instance China, which has a strong pharmaceutical industry as well.

1.4 Health Workforce

SSA has an acute shortage of HRH.[14]For example, the physician-to-population ratio is the lowest in the world, at 18 physicians per 100,000 population. A 2014 WHO Report[15]estimated a deficit of 1.8 million health workers in SSA in 2013, and this deficit was projected to increase to 4.3 million workers by 2035.[16]According to the framework of action adopted by African countries to strengthen health systems for UHC and the Sustainable Development Goals (SDGs), the health workforce is one of the two areas where Africa spends significantly less (the other area being health infrastructure). For the five East African countries, the health workforce is a common area of underinvestment.[17]

Inadequate supply of health professionals coupled with their uneven geographical distribution limit the delivery of primary and specialised care services.[18]The HRH shortage cannot be resolved without overhauling the entire ecosystem around its production. For example, creating the capacity for educating and training health professionals and improving the quality of training by designing better training programmes is necessary for the supply of skilled healthcare professionals. Moreover, policies and programmes should be framed to ensure even distribution and long-term retention of such professionals. To prevent them from moving overseas, attractive remunerative packages and better working conditions must be provided. Strengthening the technical skills of health workers—especially doctors, nurses and managers of health services—will help improve the performance of health services. The adequate supply of well-trained health professionals is a pre-condition for any large-scale private engagement in the delivery of healthcare services.

Investment in medical education and training must precede any attempts at large-scale collaborations for the delivery of healthcare services. The current shortage of HRH in East Africa limits both large-scale investments and collaborations for the delivery of healthcare services. While technology can speed up the training process through e-learning modules combined with hands-on training, given the size of the workforce required, it will still take a substantial amount of time. The two regions must discuss whether this can be an area of mutual interest and, if so, formulate terms of engagement that will be attractive to both sides.

A few HRH challenges that SSA faces are also faced by some BIMSTEC members, to varying degrees. For example, the shortage of doctors is common to both regions but is more acute in East Africa (e.g. doctor–population ratio is 0.8 in India as compared to 0.2 in Kenya).[19]The two regions must meet their own challenges before attempting to support service delivery in SSA. However, there is definite scope for collaboration between the two in medical education and training and must be explored by the respective governments.

1.5 Digital Technology for Health

As with many other sectors, digital revolution is playing a transformative role in the health sector in a wide variety to ways: improving access to care, e.g. through tele-consultation/tele-radiology; improving effectiveness of care, e.g. by empowering the frontline health workers with handheld devices; improving health system performance, through IT-enabled procurement and supply-chain system; improving health governance through better programme management and monitoring; changing providers’ and patients’ behaviours; measuring patient satisfaction; bringing diagnostics closer to people through simplification; shifting of clinical tasks to non-clinicians, etc. India and Kenya—both hotspots for digital innovations—have much to offer by way of replicable, affordable and scalable solutions. Nairobi is fast emerging as a technological hub for Africa. The capital city, with the highest internet penetration rate in Africa and rapidly improving digital infrastructure, is now considered as Africa’s most “intelligent city.”[20]

Mobile health, or mHealth, is the fastest-growing area in the sector and promises to improve the quality, accessibility and affordability of healthcare, even in low-resource countries. In Africa, almost 80 percent of the countries claim to be using mHealth, although the majority of these projects are still in their infancy.[21]In India, the digital healthcare market was valued at US$381.3 million in 2014, estimated to reach US$1.45 billion in 2018.

Some of the key drivers of mHealth investments are higher economic growth, an increase in mobile access, the development of high-quality networks, healthcare apps and the demand for wearables, and the use of mobiles phones to improve and integrate business and services.

An example of the scale at which digital technology is being used is India’s establishment of more than 75 nodal centres for research and development of telemedicine. Additionally, regional nodal centres have been established to connect district-level hospitals to speciality hospitals. Healthcare in Africa currently does not incorporate technology at such a scale.

The pan-African e-network project on tele-education and tele-medicine is a good example of how the BIMSTEC could support Africa.[22]This initiative was a joint undertaking by the Government of India (GoI) and the African Union (AU) High Commission, conceived in 2004 and launched in 2009, with the aim of building the capacity of the AU members by providing quality education, medical tele-expertise and consultations with some of the best Indian academic and medical institutions. This initiative, funded entirely by the GoI, was largely successful.[23]Since July 2017, however, the Indian government has handed over the initiative to the AU.

Digital innovations such as blockchain, cloud-based computing, virtual health, artificial intelligence and robotics, digital reality, and internet of medical things are improving the accessibility, affordability and quality of healthcare delivery. They help low-income countries overcome several constraints such as the health workforce, procurement and supply-chain management and infrastructure. It is difficult to chart the exact pathway of the evolution and adoption of digital innovation in the healthcare space, but its scale and speed can be unprecedented and truly transformative. This opens up several unanticipated avenues of south–south partnerships and collaborations between and across the BIMSTEC and East Africa. It is important for countries in both regions to collaborate in adopting and implementing digital-health innovations.

II. Aligning the Private Sector

Aligning the private sector with public health goals is a necessity in the countries that have committed themselves to achieving the UN’s SDG of “healthy lives for all” by 2030 (SDG #3.8). There are at least three compelling reasons for aligning with the private sector.

First, the resource requirement for achieving the UHC goal is enormous, in terms of both health spending and the availability of a skilled health workforce. Most governments of low-and middle-income countries (LMICs) struggle to meet this requirement alone. An analysis showed an annual health spending gap of US$274–371 billion across 67 LMICs, needed to make significant progress towards their 2030 commitments for UHC.[24]Similarly, there are huge gaps in the health workforce. Thus, there is a need to leverage the private sector for its existing capacity, investments and innovations.

Second, the private sector is already playing an important role in the financing and delivery of healthcare and has a significant presence in both regions. In SSA, for-profit organisations account for as much as 50 percent of the total healthcare provision, and their role is growing. Nearly 60 percent of healthcare financing, predominantly OOP, comes from private sources.[25]In the BIMSTEC, too, the private sector is dominant, with the exception of Thailand and Sri Lanka, where public healthcare provision is much stronger.[26]Thus, the private provision of healthcare has become a force to reckon with.

Third, some governments in both regions are opting for strategies and delivery models that will only increase their reliance on the private-sector overtime. For example, government-sponsored national health-insurance programmes in India and Kenya are designed to purchase publicly funded care from both public and private providers. The public sector is also engaging with the private sector through other arrangements such as public-private partnerships and contracting. Despite this, healthcare provision in both regions is marked by a low level of leveraging of the private sector’s potential in expanding care coverage and quality. Not too long ago, the UN Deputy Secretary General stated that Africa’s health targets cannot be met without contributions from the private sector. This applies to the BIMSTEC as well.[27]

To ensure private-sector engagement in healthcare, at the desired scale, it is important to capture the interest of investors and entrepreneurs, particularly those keen on delivering significant healthcare impact while expecting reasonable financial returns in the long run. The government must find new ways of engaging such investors in mutual partnerships that leverage the core competencies of all parties involves. Investments must be channelled into creating innovative business models that support scale and standardisation instead of fragmentation and variation, promote ‘last mile’ access to the poorest and most vulnerable instead of urban islands of excellence, and increase affordability.

Both the BIMSTEC and East Africa have had a number of promising private investments with an eye on development impact; these are worth building on by replicating, scaling and expanding. Some of the core ideas of these successful business models include hospitals with cross-subsidisation, high-volume and low-cost hospitals, network models of primary- and secondary-care clinics, and hospitals that offer in-house insurance.[28]

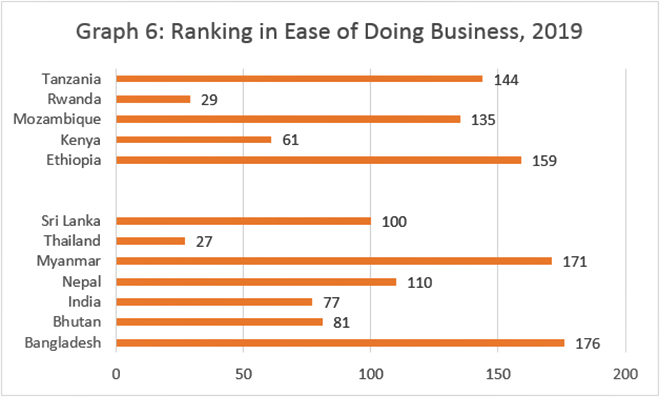

Investors and entrepreneurs interested in doing business in these regions, particularly in Africa, must take into account market variations in terms of size and economic conditions. For example, the “ease of doing business” ranking varies considerably across countries. Companies must first target established African cities to optimise their initial set-up costs before exploring mid-sized or rural markets.

Source: Doing Business 2019, 16th Edition, World Bank.

III. Knowledge-Sharing and Exchange

Knowledge-sharing and exchange must be a two-way street between the two regions. The countries in the two regions can learn and benefit from each other’s experiences in areas such as policymaking, design and implementation of interventions, health workforce and infrastructure, and health-sector governance. For example, the BIMSTEC can learn from Africa’s initiative in non-physician leadership. Given the shortage of physicians in both regions, Africa’s experience in transferring responsibilities to non-physician health workers (i.e., nurses and mid-level health professionals) can help improve healthcare access. Most African countries deploy non-physician clinicians (NPCs), after expanded training, for diagnostic and therapeutic tasks that are generally reserved for clinicians. A few states in India, notably Assam and Chhattisgarh, have tried creating mid-level service providers through expanded training. However, these initiatives have so far remained limited, while in Africa, NPCs are recognised in most countries.[29]

Another area of collaboration can be the checking for counterfeit drugs, which is a significant problem in both regions. More than 120,000 people die each year in Africa due to the consumption of fake anti-malaria drugs, while 25 percent of drugs in the Indian market is estimated to be counterfeit. Further, nearly 75 percent of the global supply of counterfeit drugs originates from India. While several African countries have strengthened their regulations with respect to the importation of drugs, active collaboration is required to tackle this problem in a sustainable manner. In the meantime, technology companies are working to institute stronger checks on drugs by texting the code printed on the scratch-panel stickers. However, this method puts the onus on the consumers to check for fake medicine, which is not a substitute for implementing regulations that discourage their production in the first place.[30]

There are various opportunities for learning and exchanging policy and business knowledge between the two blocs. Countries such as India, Kenya and Bangladesh have piloted market-based innovative business models that can have a social impact at scale and in a sustainable way. These models, with some modifications based on local conditions, can provide solutions for development challenges in the health sector.[31]

Other health-sector challenges shared by the two regions include the acute shortage of health professionals, particularly doctors; dual practice by government doctors; difficulty in posting doctors in rural areas; challenges of mixed health systems; weak regulations; low spending by the government; and weak incentives and accountability mechanisms. Health-sector regulation is a good example of an area where both regions need to improve and can jointly develop regulations to address their common concerns.

Other promising areas for trade and investment in the health sector are traditional knowledge and medicine, medical tourism, clinical trials, and R&D.

IV. Engagements, Partnerships and Collaborations

The sheer size of its economy and population makes India a dominant player in both East Africa and the BIMSTEC. India accounts for nearly 70 percent of the combined population of both regions and 70 percent of their total economy. Thus, the country is at the centre-stage in partnerships and collaborations, which exist at multiple levels. At the government level, India has a longstanding relationship with Africa, dating back to the 1960s, although the nature and intensity of this partnership have undergone significant change in response to evolving needs.

Extending lines of credit (LOCs) is one of the main instruments of India’s development assistance to less developed and developing countries, including African nations in recent years. LOCs, managed by the Export-Import (EXIM) Bank of India, are given to promote the export of eligible goods on deferred payments. Africa has been the beneficiary of India’s development assistance through LOCs, and there has been a sharp increase in the number of LOCs provided to Africa over the years. In 2012, of the 17 LOCs made operational by India, 12 were to African nations. Cumulatively, the Indian government has extended 152 LOCs worth US$8 billion to 44 African countries to date.[32]India has also been offering grants for capacity-building activities, e.g. to set up specialised institutions, provide scholarships and fund training programmes. The pharmaceutical industry has been one of the traditional areas of cooperation between India and Africa. However, there is a risk of traditional areas getting crowded out by a noticeable shift in focus towards investing in renewable energy and sustainable development projects. This does not bode well for the health industry of either India or East Africa.

Multiple international agencies and organisations, such as the African Development Bank, World Bank, World Health Organization, private foundations (e.g. Bill and Melinda Gates Foundation) and health alliances (e.g. the Global Fund and Gavi, the Vaccine Alliance) are engaged in health-sector development in both the regions. In addition to contributing resources (funding and/or technical know-how) and serving as implementing partners, they contribute to knowledge-building and sharing across countries. However, it is not yet clear to what extent these agencies and alliances can help realise the trade and exchange potential between the two regions.

There are also industry-to-industry links mediated through bodies such as the Confederation of Indian Industry, the Federation of Indian Chamber of Commerce, and industry-specific bodies (e.g. Healthcare Federation of India and Association of Healthcare Providers, India). Guided purely by commercial interests, these bodies connect to understand and invest in profitable segments of the health industry. To exploit profitable investment opportunities, a closer engagement between the industry and the government must be encouraged. Exploiting opportunities in the health industry often requires investments in semi-public goods such as gathering market intelligence, building ecosystems, and investing in complementary activities that can best be undertaken by engaging with governments.

A good example of this is India’s first Med-tech Zone. To encourage the domestic manufacturing of medical devices, the government of Andhra Pradesh has set up Andhra Pradesh Med-tech Zone, which provides excellent infrastructure that med-tech companies require. The Indian medical device market, currently valued at US$5.2 billion, is Asia’s fourth-largest market, growing at a compound annual growth rate of 15.8 percent. A number of variables are fuelling this growth: growing and ageing population, rising burden of chronic diseases, increasing health-insurance penetration, and growing medical tourism. The lack of domestic manufacturing despite increasing market demands is leading to import dependency. As a result, nearly 80 percent of the medical devices being sold in the country are from multinational companies, which distribute import products and provide support function instead of manufacturing the devices in India.[33]Once domestic manufacturing expands, for which the government has given incentives, India can start exporting those to the BIMSTEC and East Africa.

It is crucial for governments to involve the private sector in national development cooperation programmes, to generate benefits for their domestic industry. These benefits can be in terms of creating an ecosystem or public goods, which will eventually benefit the private sector. Further, development projects should be targeted to sectors and countries that are of interest to domestic businesses too.[34]

A 2018 study found a weak correlation between India’s development cooperative initiatives and its investments in Africa.[35]Development cooperation programmes can sustain only when they are beneficial to all the countries involved. Thus, nations must leverage existing forums, platforms and alliances, even as they attempt to create new ones to tap into the opportunities present in the two regions.

Conclusion

With a few exceptions, countries in the BIMSTEC and East Africa face similar health-sector challenges. Both regions are also expected to grow at a rate faster than the global pace. Given their demographics and epidemiology, their respective health industries are likely to expand with the growth of their economies.

Both regions have much to gain from each other by way of knowledge-sharing, trade and investments, and collaborations and partnerships. The BIMSTEC should, for example, explore the East African region for the opportunities its health sector presents in pharmaceuticals and medical education and training. Additionally, the latter will act as a potential gateway to SSA in the long run. Thus, it is important for the BIMSTEC to forge relations with East Africa with a long-term plan in mind. This will require investments in building the necessary ecosystems before entering the East African market to gain the most from healthcare delivery.

Digital technology is changing the way in which healthcare is delivered and received. There is potential to significantly transform healthcare systems, even in countries at lower-income levels. The emergence of a new class of investors and entrepreneurs, who are looking for long-term financial returns as well as social impact, is giving rise to inclusive business models that have the potential to make quality healthcare more accessible and affordable. In each nation, the private sector must work in tandem with their country governments to exploit opportunities in the health sector. In turn, governments should engage their private sector to ensure the sustainability of their development cooperation programmes.

Endnotes

[1]World Population Prospects: The 2017 Revision, Population Division, United Nations.

[4]T.C. James, et al., “India-Africa Partnership in Healthcare: Accomplishments and Prospects,” Research and Information System for Developing Countries, Delhi, 2015.

[6]That the 2020s is set to be the Asian decade is well-known. East Africa will be the fastest growing region in Africa as per AfDB Report: “Africa in 50 Years’ Time: The Road towards Inclusive Growth,” African Development Bank, September 2011.

[7]Although the reliance of the East African region on external development assistance for health will decline between now and 2040, this assistance will continue to play a significant role as per the IHME Global Health Financing Database 2017.

[8]“Health in Africa over the Next 50 Years,” African Development Bank, 2013.

[9]Tanoubi Ngangom, “India and Africa’s Partnership for Access to Medicines,” ORF Commentaries, 10 August 2016.

[10]Facts and figures for this paragraph have been taken from a single reference: “The Best of India in Pharma”, India Brand Equity Fund.

[11]Off-patent pharmaceutical products marketed under a brand name.

[12]East African countries have very low levels of economic diversification. For example, contribution of manufacturing to the GDP of Kenya, Mozambique, Tanzania, Rwanda and Ethiopia is 11.4 percent, 10 percent, 5.6 percent, 4.8 percent and 4.1 percent, respectively.

[16]There are country variations too. For example, against the WHO’s recommended staffing norms and standards, Kenya has a shortage of 83,000 doctors.

[17]“State of Health in WHO Africa Region,” WHO Regional Office for Africa, 2018.

[18]There are some country-specific HRH challenges, such as low-productivity of HRH, fuelled by poor management and weak enforcement of policies and regulations in Tanzania.

[20]Ronak Gopaldas, “The Race to become Africa’s Preferred Gateway is Heating up,” ORF Raisina Debate, June 2018.

[21]“Health in Africa over the Next 50 Years,” op. cit.

[22]Abhishek Mishra, “Pan Africa E-network: India’s Africa Outreach,” ORF Raisina Debate, May 2018.

[23]“First Progress Report of the Chairperson of the Commission on the Pan Africa E-Network on Tele-Education and Tele-Medicine,” Meeting of the Permanent Representatives’ Committee, 29 March 2018.

[29]Kabir Sheikh and Anns Issac, “Strengthening Health Systems in India and Africa,” inSecuring the 21stCentury: Mapping India–Africa engagement, eds. Ritika Passi and Ihssane Guennoun (Wiley-Blackwell, 2017).

[30]Franklin Cudjoe, “Chapter 8: Building a Robust Healthcare System,” inSecuring the 21stCentury: Mapping India–Africa engagement, eds. Ritika Passi and Ihssane Guennoun (Wiley-Blackwell, 2017).

[31]“Corridors of Shared Prosperity: Intra South Asia Replication of Inclusive Business Models,” International Financial Corporation, 2016.

[32]Abhishek Mishra, “The Changing Nature of India’s Lines of Credit to Africa,” ORF: India with Africa, May 2018.

[33]Facts and figures for this paragraph have been taken from “Med Tech: India’s Growth Story,” AMTZ, Bennett, Coleman & Co Ltd., December 2018.

The views expressed above belong to the author(s). ORF research and analyses now available on Telegram! Click here to access our curated content — blogs, longforms and interviews.

PDF Download

PDF Download