Covid Corrections: How the Pandemic Reveals the Failures of India’s Growth Model

The COVID-19 pandemic can serve as an opportunity for India to redefine its approach to economic growth. The policy objective should be that once the threat of the current pandemic subsides, the country will not return to business-as-usual mode and rather build an economy for the future. The Indian government has declared that it is considering measures towards distress mitigation, relief disbursement, and a revival of growth. At the same time, however, the government must aim for qualitative changes in the country’s growth pattern. The relief policies should have built-in elements to repair the country’s broken economic model and aim for economic stimulation that considers objectives of pollution reduction and bridging inequities. Any future claims of success in tackling the COVID-19 crisis will only be unquestionable if the pandemic paves the way for a new economic framework.

Attribution:

Puja Mehra, “Covid Corrections: How the Pandemic Reveals the Failures of India’s Growth Model,” ORF Issue Brief No. 363, May 2020, Observer Research Foundation.

INTRODUCTION

The COVID-19 pandemic has put India’s economic growth path under scrutiny. For decades, analysts have argued that the growth-environment trade-off could be managed better. This, however, has had little influence on economic policy. The ongoing public health emergency has crystallised many debates around this theme. It is now recognised that material prosperity has come at the cost of the environment, leading to climate change and worsening working conditions for labour. This inherent conflict has been given little attention over the decades. To continue to do so would be inviting greater economic vulnerability in times of shocks such as the current crisis.

Over two months since India first imposed a national lockdown, there is evidence that sustainability policies—and not millions of rupees spent on projects like “river rejuvenation”— produce superior outcomes in environment conservation. The air in dense cities like Delhi is cleaner, the rivers are blue again, and the skies are becoming clearer.[1]

In many countries, the public health emergency also fast emerged as a humanitarian crisis. In Delhi, for example, this was illustrated in the state’s failure to provide migrant labourers safe passage home. Not receiving assistance nor any clear reassurance that they will be taken care of during the lockdown, these labourers—suddenly finding themselves out of jobs—were forced to walk their way home.[2] Indeed, the government displayed no administrative mechanisms nor policy instruments to deliver relief to this huge population of Indian citizens.

This, considering that nearly half of India’s annual gross domestic product (GDP) comes from the unorganised sector and 80 percent of the workforce consists of informal labour who are employed without contracts, nor any retirement or health benefits.[3] This huge informal workforce is outside the trade union system, with neither rights nor bargaining power. That such a large number of labourers are without recourse to savings or food stocks is a confirmation that they have been living in a subsistence manner.

These two realities—the palpable improvements in air quality and other ecological outcomes, and the impact of the lockdown on the lives of many of India’s poor—have shown the weaknesses in the country’s growth model. Indeed, the COVID-19 pandemic is serving as a call for India to rebalance its policy objectives. The crisis can serve as an opportunity to redefine the approach to economic growth, so that once the threat subsides, the country does not return to business-as-usual mode. The policy objective should be to build an economy for the future.

To be sure, the Indian government has declared that it is considering measures towards distress mitigation, relief disbursement, and a revival of growth.[4] At the same time, however, the government must aim for qualitative changes in the growth pattern. The relief policies should have built-in elements to repair the country’s broken economic model and aim for economic stimulation that considers objectives of pollution reduction and bridging inequities.

A POST-PANDEMIC ECONOMIC MODEL

The following paragraphs will outline two crucial elements of a blueprint for a post-pandemic Indian economy.

Clean Energy-Focused Stimulus

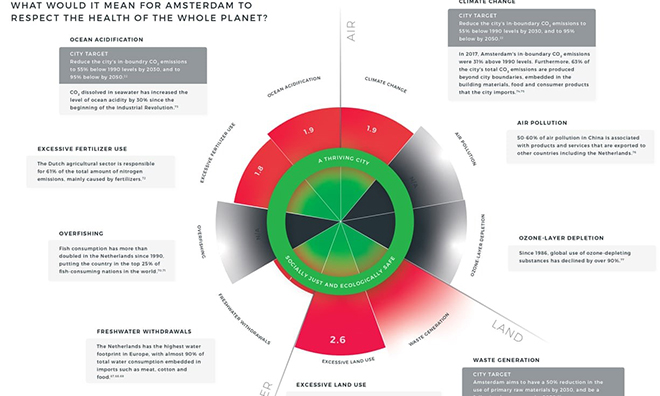

One of the things that the pandemic has taught the world is that the long-held view that many global megacities are sustainable is largely a myth.[5] Many cities around the world will likely emerge from the public health crisis and economic stagnation inflicted by the COVID-19 pandemic with a new approach to urbanisation. Milan in Italy, for instance, after its lockdown will introduce one of Europe’s most ambitious schemes yet—relocating street space from cars to cyclists and pedestrians.[6] The Dutch capital Amsterdam, too, has declared that it will revisit the fundamental economic structure on which it has evolved, and begin using the “doughnut model” devised by British economist Kate Raworth from Oxford University’s Environmental Change Institute.[7]

The premise of Amsterdam’s new commitment is that the goal of economic activity should be about meeting the core needs of all but within the means of the planet. The doughnut in the figure is like a venn diagram. In the Amsterdam plan, the inner ring of the doughnut sets out the minimum – derived from the United Nations Sustainable Development Goals (SDGs) – for human beings to have a healthy life. It includes food and clean water, shelter, sanitation, energy, education, healthcare, gender equality, income and political voice. A person who does not attain these minimum standards is living in the doughnut’s hole.

The outer ring of the doughnut represents the ecological ceiling, drawn up by earth-system scientists and universally accepted to be true for all nations. If these boundaries are crossed, there is risk of damage to the climate, to soil, oceans, the ozone layer, freshwater resources, and biodiversity. Human needs and those of the planet are justly met between the two rings. For instance, as part of Amsterdam’s new vision, its policymakers are looking at how to shift from an energy basket that is dependent on fossil fuels to one that will rely on more renewable sources.

In India too, good environmental and climate economics can be integrated into the economic relief and recovery packages. The stimulus packages are an opportunity to deepen the green agenda by linking them to the adoption of environment regulations. Conditions for switching to renewable power sources can be built into the relief measures, as well as commitments to use public transit and clean fuel that draws on waste streams from municipal garbage, introduction of walking paths and bike lanes, and other such goals. Ideally, a new environment policy framework should be drafted before the stimulus package is designed so that the two objectives can be incorporated.

This is important because recent economic history has shown that the response to a crisis can itself cause future crises. Crisis managers must not lose sight of the fact that the revival packages after the global financial crisis of 2008 made the mistake of ignoring this. Those interventions revived growth in the short term but sowed the seeds of new problems. Even 10 years later, the Indian economy has not recovered from the problem of bad bank loans created by the asset stimulus of those years. Banks went overboard extending evergreen loans for projects that were no longer viable. Many of those projects have since fallen through the cracks and banks are saddled with non-performing assets (NPAs). A jammed banking system is a huge price to pay for a short-lived economic recovery. One reason the economy is more vulnerable to the COVID-19 shock than it was in 2008 is the weaker health of banks.[8]

A green stimulus tends to be cheaper in the long run, as shown by the case of South Korea. It has demonstrated robust and consistent standard operating procedures, combining high volumes of testing and quarantine of infected individuals to contain the spread of COVID-19 without strict lockdowns.[9] The virus was suppressed – even as most factories, shopping malls and restaurants remained open—using data from surveillance cameras, cell phones and credit card transactions to map the social connections of suspected cases. Reopening the economy, though, has led to new infection cases. The Korea Centers for Disease Control and Prevention (KCDC) has reported at least 34 new infections, the highest since April 9, after a small outbreak emerged around a slew of nightclubs, prompting the authorities to temporary close all nightly entertainment facilities around the capital.[10]

The country’s response is not surprising given that it had invested heavily in infectious disease control following prior experiences with Severe Acute Respiratory Syndrome (SARS) and the Middle East Respiratory Syndrome (MERS).[11] Incidentally, South Korea’s 2008 stimulus package included big investments in the sectors where eco-friendly measures were required, with a focus on river restoration, building energy efficiency, and green transport.[12]

Why should a resource-constrained government such as India’s have any focus other than economic revival? The COVID-19 pandemic may well be followed by other public health crises. Returning to the pre-COVID-19 economic model will not reduce vulnerability to future shocks. Repeated crises can erode resilience and the capacity of crisis managers to respond to the shocks. Already, the scope for using fiscal levers is reduced considerably because they were overused to mitigate the impact of the 2008 financial crisis. Resources available for use in hard times are not unlimited; therefore, reducing vulnerability to shocks is the least expensive coping strategy over the medium term. For instance, improving air quality and reducing pollution reduces the vulnerability to threats related to respiratory health.[13]

The country’s real estate development has received multiple rounds of support from the Reserve Bank of India (RBI) and the government. Going forward, the support can discriminate positively in favour of energy efficient homes, buildings and factories.

The bailouts for companies, big or small, and relief for individuals ought to have green goals built into them. Polluting industries, especially those that release waste into rivers and groundwater, should be provided conditional bailouts if at all. The MSME (micro, small and medium enterprises) relief packages, for example, should differentiate between auto-ancillary units linked to the production of electric cars, including charging stations for them, and those linked to fossil fuel vehicles, favouring the former. If a stimulus is being provided to the big corporate houses, the green-non-green distinction should be maintained.

Eventually, large corporate houses will need bailouts and concessions and regulatory forbearance on stressed loans. Otherwise, the NPAs in the banking system will surge. India must make such relief conditional on guarantees of no job cuts and reduction in wage inequality, as measured by the ratio of promoter and senior management remuneration to that of lower-level employees.[14]

The US Congress has approved fiscal spending of just under $3 trillion – more than the stimulus given after the global financial crisis. Small companies can take bank loans to cover running costs, wages and rent for a couple of months. If they do not lay off workers, the US Treasury will repay the loans. These loan schemes are conditional on companies freezing share buy-backs[15] and capping management pay and bonuses.[16]

Airlines, airports, hotels and tourism industries—all of which generate employment—are among the worst hit and are likely to seek relief sooner than later. Any lifelines extended to them must be made conditional on measurable goals for emissions reduction, cleaner environment, more equitable pay structures, more jobs and greater commitment to a better deal for casual labour.

Low-cost labour cannot be allowed to mean disempowered labourers. If India’s growth model has come to depend on cutting corners and miserable wages for migrant labourers, it needs to be reformed. But that can be a medium-term goal. More immediately, steps must be taken to ensure that the support from banks and the government reaches workers. One way is for regulatory filings by companies to require disclosures about how they are ensuring that their contractors for casual labour are paying workers. Ideally, formalisation of casual jobs to ensure better bargaining power for casual labour should be one of the conditions of the stimulus and support packages.

Similarly, relief for agriculture can be designed to move farming away from depleting groundwater, and towards more sustainable practices and crop choices. Technical improvements for energy efficiency in irrigation include facilitating the upgrade to energy-efficient pump sets, and reduction of diesel consumption in irrigation can be incentivised.[17]

Incentives can be corrected over time for more sustainable farming practices. Flawed pricing and procurement policies responsible for this should be reviewed and corrected as part of the support plans.

Green growth interventions can also be made through bank finance. Banks are reluctant to lend in the current business scenario of heightened uncertainty. But policy signals can stimulate the market for green technologies and services and products, making it less risky for banks to finance growth in this sector, one that will also have export potential as the world re-orients its green business policies post-COVID-19.

Increase the Health GDP

Infrastructure stimulus is usually understood as providing finance for highways, high-speed trains and airports. Investing in schools and hospitals is rarely seen as being a crucial part of “infrastructure development”. Healthcare’s availability and affordability does not receive as much attention in policymaking as hard infrastructure does. This approach needs to change.

The COVID-19 crisis is a reminder of the importance of a well-functioning public health system. It opens up an opportunity for course correction in this sector. An effective public health system would have afforded policymakers greater leeway in deciding about the economic shutdown. However, the choice of preventive strategies against the spread of COVID-19 is limited to stringent lockdowns because of India’s public healthcare infrastructure deficit.

There are just 0.55 hospital beds per 1,000 people in India.[18] Even this national figure, modest as it is, does not convey the inequity in healthcare access. Some states are way below the national average. Bihar has an acute shortage of government hospital beds, with just 0.11 beds available per 1,000 people.[19]Some states do better on this metric such as West Bengal (2.25 government beds per 1,000) and Sikkim (2.34 government beds per 1,000). The capital city of Delhi has 1.05 beds per 1,000. The southern states of Kerala (1.05 beds per 1,000) and Tamil Nadu (1.1 beds per 1,000) also have better availability of beds than the average.[20]

India’s neighbours fare better, such as China (4.2 beds per 1,000), Sri Lanka (3.6 beds per 1,000), Pakistan (0.6 beds per 1,000), and Bangladesh (0.8 beds per 1,000).[21] India has 0.7 medical doctors per 1,000 people, and on this parameter too lags behind China (1.7 medical doctors per 1,000), Pakistan (0.9) and Sri Lanka (0.9) but is better off than Bangladesh (0.5).[22]

The meagre healthcare resources have consequences for both human well-being and development. One in four Indians runs the risk of dying from a non-communicable disease (NCD) – including cardiovascular disease, cancers, diabetes and obesity – before they reach 70.[23] NCDs are increasingly responsible for premature deaths and disabilities every year across the globe. Nearly 15 million people die before the age of 70 from chronic and non-communicable diseases.[24]

Shocks to incomes and unexpected medical expenditure because of health issues and emergencies push 55 million Indians below the poverty line every year.[25]

Healthcare spending is not increasing at the same pace as GDP. The 11th Five Year Plan (2007-12) brought some reforms as a result of which the private sector’s share in total number of hospital beds and insurance coverage has increased.[26] Between 2002 and 2010, the private sector created over 70 percent of the new beds.[27] The 12th Five Year Plan (2012-17) had envisioned universal health coverage as a long-term goal. It declared “assured access to a defined essential range of medicines and treatment at an affordable price, which should be entirely free for a large percentage of the population.”[28]

In September 2018, India introduced the Ayushman Bharat – Pradhan Mantri Jan Aarogya Yojana to provide free secondary and tertiary hospitalisation to poor and economically vulnerable families across the country. The aim is to achieve Universal Health Coverage by 2030. It is a health insurance scheme that covers hospitalisation and a public primary healthcare network of wellness centres. Yet in 2019-20, the Centre and the states together spent just INR 2.6 lakh crore, or 1.29 percent of GDP, on health.[29] (This included establishment expenditure comprising salaries, gross budgetary support to various institutions and hospitals, and transfers to the states under centrally sponsored schemes such as Ayushman Bharat.) The total per capita government spending on healthcare has doubled from INR 1,008 per person to INR 1,944 over the last five years but continues to remain low. Even total healthcare spending (private and government combined), at 3.6 percent of GDP, as per the Organisation for Economic Cooperation and Development’s (OECD) data, is very low compared with other countries. The average for OECD countries in 2018 was 8.8 per cent of GDP.

For years, the International Monetary Fund’s (IMF) annual Article IV reports have been reiterating that investing in education and healthcare can boost India’s human capital and ensure that the demographic dividend pays off.[30] In 2018, it identified poor public health as the 12th most important obstacle to India’s rise in the ease of doing business ranking, ahead of crime and theft, tax regulations and policy instability.[31] Health and working conditions formed a key recommendation amongst its suggestions for labour market reforms.

The COVID-19 crisis presents an opportunity to improve healthcare. Increasing the share of GDP on health will not only address the infrastructure deficit, improving the quality and productivity of the economy’s human capital, but can also reduce the economic cost of the lockdowns.

Substantial ramping up of manufacturing capacities for medical grade masks, gloves, gowns, ventilators, testing labs, and other supplies and equipment will enable India to put up a better fight against the virus and be better prepared for future outbreaks. It will also minimise economic costs the next time there is a public health crisis. And if the ramp-up is on a scale large enough to allow for exports once the domestic market is taken care of, costs can drop and be internationally competitive.

The strategy calls for fully operational hospitals to be constructed in every district, new hospitals that will outlast COVID-19 and will be a step towards addressing the overall health infrastructure deficit over the medium term. In the immediate term, a move to set up hospitals, laboratories, schools and training institutes for healthcare professionals can generate both high-skill and low-skill jobs such as for construction labour. If these are spread across the length and breadth of the country, they can create rural and semi-urban jobs, taking off some of the pressure on cities.

On the reforms side, the regulatory, intellectual property, import tariffs and pricing policy frameworks will have to be simultaneously overhauled to strike a balance between affordability and viability of the health and pharmaceutical industries.

Stimulating the health GDP is a difficult task, as is making healthcare the engine of growth and a driver of GDP. It requires problem-solving of an unprecedented order.

Mobilising finance will be a challenge but not the biggest one. Markets and sovereign rating agencies may disagree with government if it decides to borrow directly from the RBI or dip into its reserves to maintain its spending on pensions and pays. However, the reaction will not be the same if this is done to increase public investments in healthcare to, say, five percent of GDP, or to promote the greening of the economy.

Health is a state subject. Still, most states will welcome a central scheme for financing healthcare infrastructure expansion, particularly in Tier-II cities and rural areas. The states have limited tools to deal with the fiscal crisis and cannot borrow as freely as the Centre.[32] The Fiscal Responsibility and Budget Management (FRBM) Act bars them from exceeding a three-percent fiscal deficit threshold and even the escape clause allows for an additional spending of only 0.5 percent of gross state domestic product in times of crisis. The restrictions have been relaxed for 20-21 by the Centre from 3 to 5 percent so that states can have the finances they need to tide over the crisis.[33]

State goods and services tax (SGST) collections, which constitute almost 45 percent of own tax revenue of states, have collapsed because of the lockdown.[34] As have collections from taxes on alcohol, petroleum products and property, which account for 15 percent of revenues on average.[35] The Centre will have to find the resources to supplement states’ spending.

The Union Budget presented on February 1 had not foreseen the COVID-19 crisis. The Centre must immediately present a new budget with a three- to four-year medium-term fiscal strategy.[36] Redrawing the February 1 budget can release funds for immediate use. For instance, the centre spends INR 3.4 trillion annually on centrally sponsored schemes, according to the Fifteenth Finance Commission’s estimates.[37] There are likely to be savings on this head this year on account of the disruptions due to the lockdown. Again, Rathin Roy, Director, National Institute of Public Finance and Policy (NIPFP) has estimated that there could be another INR 1 trillion of unspent balances available, which can be marshalled immediately by leveraging the RBI’s ways and means advances channel.[38]

Dr Roy estimates that there is enough liquidity for the central government to borrow an incremental three percent of GDP through non-typical borrowing instruments carrying fixed interest in perpetuity to be paid back in a specified time frame after the government tides over the emergency.[39] Retained earnings of corporations, including public sector firms, can be sequestered and parked in these specialised bond issues, in green bonds/corona bonds/Green corona bonds. The RBI can also directly buy specialised bonds from the government.

There is a lesson here for the government. If it had not already raided RBI’s balance sheet for more than INR 1.7 trillion last year in ‘peace time’, that additional recourse would have been available to it during this emergency.[40]

If the funds can be made available, what should the central government spend on? The bulk of the spending should go into upgrading infrastructure in primary and secondary care centres, i.e., district hospitals and primary health centres. Executed well, these investments will improve the quality of human capital, and create jobs and markets for pharma products and medical devices. The government can be the primary financer or provider of healthcare. It need not necessarily be the producer.

For this, a specially-designed fiscal stimulus can be funnelled into public health, and policy bottlenecks removed so that the sector becomes the engine of GDP growth in the coming months.[41] Subsidised loans, earmarked land, prompt single-window clearances and approvals, tax holidays, and all such fiscal tools can be deployed to manufacture medical devices and medicines and set up hospitals.

If new business models need to be created, now is the time to design them. Affordability, quality and accessibility will be key. If all citizens across income groups are able to use the public health system equitably, the wealthy will not resent having to pay taxes to maintain quality standards. Those in the highest income quintiles do not resent paying taxes for defence because they need protection as much as those who are in the bottom of the ladder, and there is no private sector alternative.

Conclusion

The ongoing COVID-19 pandemic serves as a warning that persisting with a flawed economic model has eroded the capacity of people, business and the government to weather shocks. There is a need therefore to remodel the country’s approach to growth. Once urgent distress relief has been attended to, the focus must shift to correcting structural weaknesses. Wherever possible, distress relief measures must incorporate policy objectives of sustainability, repairing labour’s bargaining power, and reducing the healthcare infrastructure deficit. Increased fiscal spending on such a package will provide income opportunities for individuals and business, and at the same time alleviate long-term bottlenecks.

Resources are not a binding constraint in doing this. An economic support package striving for these goals is unlikely to invite adverse sovereign rating action even if it involves a sharp surge in the government’s fiscal deficit. The primary challenges are in changing attitudes and redesigning policy.

Amsterdam and Milan illustrate how in the wake of the COVID-19 crisis, Western cities are revisiting the fundamentals on which they were built. Before they even begin to repair and reconstruct, they first have accepted that their current model is flawed. It would serve India well to do the same.

About the Author

Puja Mehra is a Delhi-based journalist and author of The Lost Decade (2008-18): How India’s Growth Story Devolved into Growth Without a Story.

[8] The Gross Non Performing Assets (GNPA) Ratio of all scheduled commercial banks increased from 2.5 percent in 2011 to 11.2 percent in 2018. It reduced after that and was 9.3 percent in 2019. (RBI’s December 2019 Financial Stability Report)

Public Sector Banks (PSBs) posted aggregate operating profits during FY2017–18 and FY2018–19 of Rs. 1,55,603 crore and Rs. 1,53,871 crore respectively. However, primarily due to continuing ageing provision for NPAs, they made aggregate provision for NPAs and other contingencies of Rs. 2,40,973 crore and Rs. 2,35,623 crore respectively. As a result, PSBs made aggregate net losses of Rs. 85,370 crore in FY18 and aggregate net losses of Rs. 81,752 crore in FY19. PSBs returned to profitability in the current FY, reporting an aggregate profit of Rs. 3,221 crore in the first half of FY20. (Written Reply of MOS Finance to a Lok Sabha question on 9 December 2019.)

The views expressed above belong to the author(s). ORF research and analyses now available on Telegram! Click here to access our curated content — blogs, longforms and interviews.

PDF Download

PDF Download