-

CENTRES

Progammes & Centres

Location

क्या अफ्रीका में इस बात की संभावनाएं हैं कि वो यूरोप की रूस पर ऊर्जा संबंधी निर्भरता को कम कर सके?

अकारण ही रूस द्वारा यूक्रेन पर हमला करने से दुनिया के ऊर्जा समीकरणों में बहुत बड़े बदलाव देखने को मिल रहे हैं. दुनिया के तीसरे सबसे बड़े तेल उत्पादक (11.3 अरब डॉलर बैरल प्रति दिन) और तरल प्राकृतिक गैस (LNG) के दूसरे सबसे बड़े उत्पादक और निर्यातक के तौर पर रूस, दुनिया की कुल तेल और गैस के छठे हिस्से की आपूर्ति करता है. तेल और गैस के बाज़ार में मास्को का प्रभुत्व ख़ास तौर से यूरोप में दिखता है, जो अपनी तेल और गैस की ज़रूरतों के लिए रूस पर बहुत ज़्यादा निर्भर है. अंतरराष्ट्रीय ऊर्जा एजेंसी (IEA) के मुताबिक़, 2021 में यूरोपीय संघ (EU) ने रूस से 155 अरब घन मीटर (bcm) गैस ख़रीदी थी, जो यूरोपीय संघ के कुल गैस आयात का 45 प्रतिशत और उसकी कुल गैस खपत का 40 फ़ीसद है. अकेले जर्मनी ही रूस से हर दिन 555,000 बैरल तेल ख़रीदता है. अंतरराष्ट्रीय ऊर्जा एजेंसी का आकलन है कि पश्चिम द्वारा लगाये गए प्रतिबंधो के बावजूद वर्ष 2022 में रूस, कच्चा तेल और अन्य उत्पाद बेचकर हर महीने 20 अरब डॉलर कमा रहा है.

दुनिया के तीसरे सबसे बड़े तेल उत्पादक (11.3 अरब डॉलर बैरल प्रति दिन) और तरल प्राकृतिक गैस (LNG) के दूसरे सबसे बड़े उत्पादक और निर्यातक के तौर पर रूस, दुनिया की कुल तेल और गैस के छठे हिस्से की आपूर्ति करता है.

तेल और गैस के दाम में तेज़ी से हो रही बढ़ोत्तरी ने अफ्रीका के बड़े ऊर्जा उत्पादकों की तस्वीर बदल दी है. हालांकि, अफ्रीका के सामने जो अवसर है, वो असल में यूरोप की रूस के हाइड्रोकार्बन पर निर्भरता समाप्त करने की इच्छाशक्ति पर टिका हुआ है, जो राजनीतिक स्तर पर है.

अफ्रीकी देश, ख़ास तौर से पश्चिमी अफ्रीका में स्थित नाइजीरिया, अंगोला और सेनेगल के पास तरल प्राकृतिक गैस (LNG) के ऐसे भंडार हैं, जिनका अब तक ठीक से उपयोग नहीं किया जा सका है. इससे बड़ा सवाल ये है कि क्या अफ़्रीकी देशों में इतनी क्षमता है कि वो यूरोप की ऊर्जा संबंधी मांगों को पूरी कर सकें.

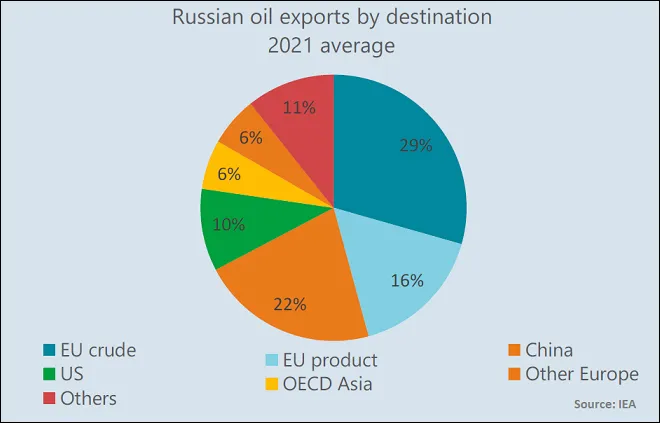

2021 में देशों के हिसाब से रूस के तेल निर्यात का औसत

अप्रैल 2022 में ही दुनिया की आठवीं सबसे बड़ी अर्थव्यवस्था इटली ने अंगोला और कॉन्गो गणराज्य के साथ प्राकृतिक गैस की आपूर्ति के नए समझौते किए थे.

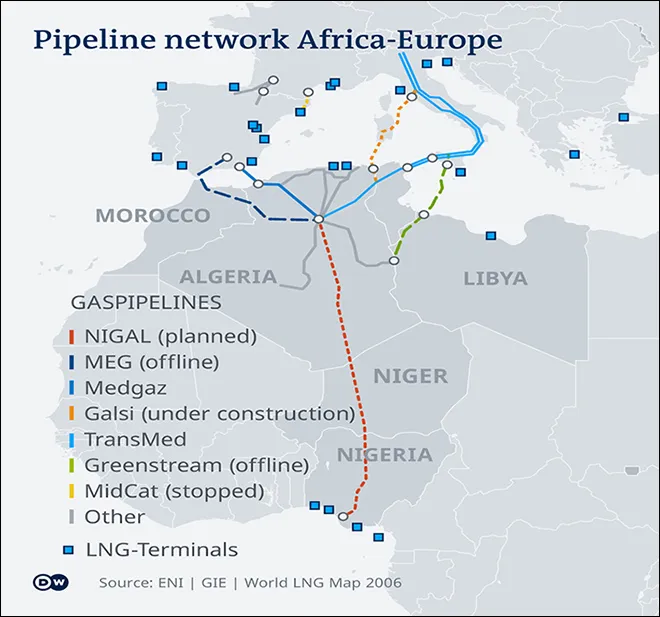

ऊपरी तौर पर देखें तो अफ्रीका के हाइड्रोकार्बन संसाधनों में यूरोप की रूस संबंधी समस्या का समाधान देने की क्षमता दिखती है. अफ्रीका महाद्वीप के जीवाश्म ईंधन के विशाल भंडार, यूरोप से उसकी नज़दीकी और उसका LNG का बढ़ता हुआ बाज़ार, यूरोपीय नेताओं को दक्षिण की ओर आकर्षित कर सकता है. अफ्रीकी देश पारंपरिक रूप से यूरोप को गैस की आपूर्ति करते रहे हैं और वो अपना निर्यात बढ़ाने के लिहाज़ से बहुत अच्छी स्थिति में हैं. ऐसा इसलिए है क्योंकि कई अफ्रीकी देशों में पहले से ही ऐसी पाइपलाइनें हैं, जो भूमध्य सागर में यूरोप में पाइपलाइनों के बड़े नेटवर्क से जुड़ी हुई हैं. इस वक़्त अफ्रीका से यूरोप को गैस आपूर्ति अल्जीरिया से स्पेन और लीबिया से इटली को होती है. हालांकि, नई पाइपलाइनों से गैस आपूर्ति शुरू होने में अभी कुछ वक़्त लगेगा.

अफ्रीका-यूरोप का पाइपलाइन नेटवर्क

अभी अप्रैल 2022 में ही दुनिया की आठवीं सबसे बड़ी अर्थव्यवस्था इटली ने अंगोला और कॉन्गो गणराज्य के साथ प्राकृतिक गैस की आपूर्ति के नए समझौते किए थे. इससे इटली को रूस से आयात में कटौती करने में बहुत मदद मिलेगी.

यूरोपीय देशों के साथ क़रीबी संबंध रखने वाले अफ्रीकी देशों के लिए ये एक बड़ा मौक़ा है. ख़ास तौर से इतालवी सुपरमेजर्स, एनी के पास अंगोला जैसे उन देशों के लिए जहां पर इटली की बहुराष्ट्रीय कंपनी एनी (Eni) की मज़बूत उपस्थिति है और वो एनी बाज़ार में सबसे ताक़तवर है. लुआंडा में इटली के विदेश मंत्री लुइगी डि माओ और अंगोला के पारिस्थितिक संक्रमण मंत्री मंत्री रॉबर्टो सिंगोलानी के बीच जिस समझौते पर दस्तख़त हुए, उससे आने वाले वर्षों में दोनों देशों के बीच प्राकृतिक गैस के व्यापार की शर्तें तय हुई हैं.

यूरोप में गैस के दाम में ज़बरदस्त उछाल आ गया है. रूस ने भुगतान से जुड़े विवादों के चलते पोलैंड, बुल्गारिया और फिनलैंड को पहले ही गैस की आपूर्ति रोक दी है.

अफ्रीका में बन रहे प्राकृतिक गैस के अहम स्टार्ट-अप प्रोजेक्ट

| प्रोजेक्ट | देश | संचालक | निवेश का अंतिम फ़ैसला | स्टार्ट-अप (तैयार होने का संभावित समय) |

| एटम (क्षेत्र 1एलएनजी-टी1 और टी2) | मोज़ाम्बिक | कुल ऊर्जा | 2019 | 2026 |

| गोल्फिन्हो (क्षेत्र 1 एलएनजी-टी1 और टी2) | मोज़ाम्बिक | कुल ऊर्जा | 2019 | 2026 |

| ग्रेटर टॉर्चर अहमेइम एफएलएनजी फेज I | मॉरिटानिया | ब्रिटिश पेट्रोलियम | 2018 | 2023 |

| ग्रेटर टॉर्चर अहमेइम एफएलएनजी फेज II | मॉरिटानिया | ब्रिटिश पेट्रोलियम | 2012 | 2027 |

| कोरल एफएलएनजी | मोज़ाम्बिक | एनी | 2017 | 2022 |

| मरीन XII फ़ास्ट एलएनजी | कॉन्गो गणराज्य | एनी | 2022 | 2023 |

| संहा लीन गैस | अंगोला | शेवरॉन | 2021 | 2023 |

| मरीन XII एफएलएनजी | कॉन्गो गणराज्य | एनी | 2022 | 2023 |

स्रोत: Rystad Energy, 12 May 2022

आज जब यूक्रेन में ज़बरदस्त संघर्ष छिड़ा हुआ है, तो यूरोप में गैस के दाम में ज़बरदस्त उछाल आ गया है. रूस ने भुगतान से जुड़े विवादों के चलते पोलैंड, बुल्गारिया और फिनलैंड को पहले ही गैस की आपूर्ति रोक दी है. इससे यूरोप को आपातकाल में ऊर्जा संसाधनों की आपूर्ति के विकल्प तलाशने पड़ रहे हैं और यूरोप से नज़दीक होने के चलते, अफ्रीका क़ुदरती तौर पर रूस के तेल और गैस का विकल्प बनकर उभरा है. ये कोई राज़ नहीं है कि अफ्रीका में गैस के दुनिया के कई सबसे बड़े भंडार हैं.

अफ्रीका के तेल और गैस के प्रचुर प्राकृतिक संसाधन उसके आर्थिक और सामाजिक विकास के लिए बेहद अहम हैं और आने वाले समय में वो पूरे महाद्वीप में विकास को रफ़्तार देने की क्षमता रखते हैं. आज जब यूरोप, ‘2030 से पहले’ रूस पर अपनी निर्भरता कम करना चाहता है, तो मध्यम अवधि में अफ्रीकी देश, यूरोप को प्राकृतिक गैस की आपूर्ति का अस्थायी विकल्प बन सकते हैं. हालांकि, रूस की ख़ाली की हुई जगह को भरने- यानी हर साल रूस के बराबर 50 से 190 अरब घन मीटर गैस की आपूर्ति करने की अफ्रीकी देशों की क्षमता कई बातों, जैसे कि ऊर्जा के मूलभूत ढांचे और इसके निर्माण में लगने वाली पूंजी की उपलब्धता पर निर्भर करती है.

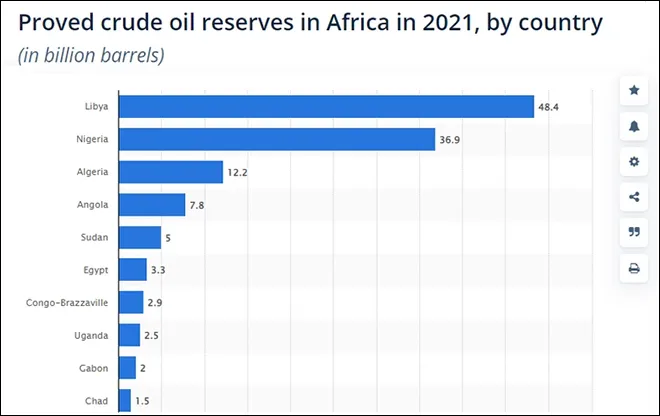

2021 में अफ्रीका में कच्चे तेल के भंडार क़रीब 125.3 अरब बैरल कच्चे तेल के भंडार होने का अनुमान था. जबकि प्राकृतिक गैस के भंडार 625 खरब घनफुट होने का अंदाज़ा लगाया गया था.

2021 में अफ्रीकी देशों में तेल के साबित हो चुके भंडार

इस वक़्त अफ्रीका में तेल और गैस की कई परियोजनाओं पर काम चल रहा है और कई को मंज़ूरी मिल चुकी है. इनमें से कुछ प्रमुख परियोजनाएं इस तरह से हैं;

-ट्रांस सहारा गैस पाइपलाइन (NIGAL): ये प्राकृतिक गैस की एक योजनाबद्ध पाइपलाइन है, जो नाइजीरिया से अल्जीरिया तक लगभग 4401 किलोमीटर लंबी है. इस परियोजना का प्रस्ताव पहले पहल 1970 के दशक में रखा गया था. लेकिन, साल 2002 तक इस मामले में तब तक कोई प्रगति नहीं हुई, जब तक नाइजीरिया के नेशनल पेट्रोलियम कॉरपोरेशन (NNPC) और अल्जीरिया की राष्ट्रीय तेल और गैस कंपनी सोनाट्रैच के बीच सहमति पत्र पर दस्तख़त नहीं हो गए. इस प्रोजेक्ट की अनुमानित लागत 13 अरब डॉलर है और इसके ज़रिए एक साल में 30 अरब घन मीटर तक गैस की आपूर्ति की जा सकती है.

-नाइजीरिया- मोरक्को गैस पाइपलाइन (NMGP): 2016 में नाइजीरिया और मोरक्को ने 5560 किलोमीटर लंबी पाइपलाइन विकसित करने का समझौता किया था, जो पश्चिमी अफ्रीका के बहुत से देशों को यूरोप से जोड़ेगी. इस पाइपलाइन का मक़सद, नाइजीरिया के प्राकृतिक गैस संसाधनों को पश्चिमी और उत्तरी अफ्रीका के 13 देशों तक पहुंचाया जाना है. ये पाइपलाइन, नाइजीरिया, बेनिन, घाना और टोगो के बीच फैली वेस्ट अफ्रीका गैस पाइपलाइन (WAGP) का ही एक विस्तार है. NMGP के इंजीनियरिंग की स्टडी के लिए ओपेक (OPEC) के अंतरराष्ट्रीय विकास फंड से 1.43 करोड़ डॉलर की रक़म दी जानी है.

-मेडगाज़ पाइपलाइन परियोजना: ये समुद्र के भीतर 210 किलोमीटर लंबी पाइपलाइन बिछाने की परियोजना है, जो अल्जीरिया के बेनी सफ़ से स्पेन के अल्मेरिया को जोड़ेगी. इस पाइपलाइन से हर साल 8 अरब घन मीटर गैस की आपूर्ति की जा सकेगी. चूंकि मेडगाज़ पाइपलाइन किसी तीसरे देश से होकर नहीं गुज़रती है, तो इससे दक्षिणी यूरोप को गैस की आपूर्ति की सुरक्षा और सुनिश्चित होगी.

-ट्रांस मेडिटेरेनियन पाइपलाइन (TRANSMED): 2475 किलोमीटर लंबी पाइपलाइन की इस परियोजना को ट्यूनिशिया और सिसिली से होते हुए अल्जीरिया से इटली तक गैस की आपूर्ति के लिए बनाया जा रहा है. इस परियोजना की कुल लागत लगभग 6.25 अरब डॉलर है और इसके ज़रिए हर साल 33.5 अरब घन मीटर गैस की आपूर्ति की जा सकेगी.

-तंज़ानिया तरल गैस प्रोजेक्ट (TLNGP): इस परियोजना को लिकोंग-ओ मचिंगा तरल प्राकृतिक गैस परियोजना के नाम से भी जाना जाता है. इस पाइपलाइन की परिकल्पना 2010 में तब से की गई थी, जब वहां प्राकृतिक गैस के पहले भंडार मिले थे. तंज़ानिया में प्राकृतिक गैस के 57 ख़रब घन फुट भंडार पक्के तौर पर मिल चुके हैं. इसके अलावा उसके समुद्र तट से दूर भी 29.5 खरब घन फुट प्राकृतिक गैस के भंडार मिल चुके हैं. इस परियोजना की लागत 30 अरब डॉलर होने का अनुमान लगाया गया है, और इसकी क्षमता हर साल एक करोड़ टन तरल प्राकृतिक गैस उत्पादन करने की होगी. नियामक संस्थाओं से मंज़ूरी में देरी के चलते इस परियोजना का निर्माण रुक गया था, जिसके इसी साल शुरू होकर 2028 तक पूरा होने की उम्मीद है.

-रोवुमा LNG तरलीकरण प्लांट: 30 अरब डॉलर लागत वाला रोवुमा LNG टर्मिनल, उत्तरी मोज़ाम्बिक के काबो डेलगाडो तट के क़रीब स्थित है. ये रोवुमा बेसिन के क्षेत्र 4 ब्लॉक के तीन गैस भंडारों पर आधारित है, जिनमें 85 ख़रब घनफुट प्राकृतिक गैस होने का अंदाज़ा लगाया गया है. इसके निर्माण की अगुवाई एक्सॉनमोबिल कर रही है. इस परियोजना से हर साल 1.52 करोड़ टन LNG का उत्पादन होने का अंदाज़ा लगाया गया है.

-नामिबे रिफाइनरी कॉम्प्लेक्स (NAMREF): इस रिफ़ाइनरी को अंगोला के नामिबे में बनाने का प्रस्ताव है और इसके 2025 में शुरू हो जाने की उम्मीद है. इस परियोजना की लागत लगभग 12 अरब डॉलर बताई जा रही है, जिसके तहत अंगोला के नामिबे में चार लाख बैरल तेल प्रतिदिन उत्पादन करने वाली रिफाइनरी बनाई जानी है.

तेल और गैस की कई प्रस्तावित और निर्माणाधीन परियोजनाएं उस अहम अवसर की तरफ़ इशारा करती हैं, जिसका फ़ायदा उठाकर अफ्रीकी देश ऊर्जा के वैश्विक बाज़ार में और अधिक केंद्रीय भूमिका निभा सकते हैं, क्योंकि आज यूरोपीय देश तेल और गैस की आपूर्ति के विकल्प तलाश रहे हैं. हालांकि अगर अफ्रीकी देश अपने सामने खड़े इस मौक़े को भुनाना चाहते हैं, तो उन्हें इस राह में आने वाली कुछ चुनौतियों से पार पाना ही होगा.

सबसे बड़ा मुद्दा तो है गैस आपूर्ति के मूलभूत ढांचे में निवेश की कमी. इस वजह से ख़ास तौर से उप-सहारा अफ्रीका क्षेत्र में गैस उद्योग का विकास नहीं हो सका है. तमाम देशों के आर-पार मूलभूत ढांचे के अभाव के चलते, अफ्रीका की प्राकृतिक गैस का निर्यात कर पाना मुश्किल हो जाता है. अगर अफ्रीकी देश, यूरोप की गैस की ज़रूरतें पूरी करना चाहते हैं, तो फिर उनके पास इसके लिए गैस के प्रसंस्करण के साथ-साथ पर्याप्त पाइपलाइनें और भंडारण की सुविधाएं होनी चाहिए. इसके लिए उन्हें अफ्रीकी गैस और मूलभूत ढांचों में वित्तीय संस्थानों, ऊर्जा कंपनियों और यूरोपीय देशों से निवेश को काफ़ी मात्रा में बढ़ाना होगा.

ऊर्जा संसाधनों की आपूर्ति की सुरक्षा एक और बड़ी चुनौती है. अफ्रीका के सहारा क्षेत्र के देशों से होने वाला ऊर्जा के ज़्यादातर निर्यात को सहेलियन क्षेत्र से गुज़रने की ज़रूरत पड़ेगी. सहेलियन क्षेत्र में कई राजनीतिक, सामाजिक, आर्थिक और सुरक्षा संबंधी चुनौतियां हैं. आतंकवाद, हिंसक उग्रवाद और सांप्रदायिक हिंसा के चलते ये चुनौतियां और भी बढ़ जाती हैं. अफ्रीका के पूर्वी तट के हालात भी कुछ ख़ास अलग नहीं हैं, जहां मोज़ाम्बिक के काबो डेलगाडो इलाक़े में इस्लामिक उग्रवाद के चलते टोटल एनर्जीस को काम रोकना पड़ा था और बढ़ती असुरक्षा के चलते कंपनी को अपने कर्मचारी भी वापस बुलाने पड़े थे.

यूरोपीय संघ के लिए रूस की गैस पर निर्भरता कम कर पाना आसान काम नहीं होगा. हालांकि, अगर वो अफ्रीका के गैस संबंधी मूलभूत ढांचे के निर्माण के लिए ज़रूरी पूंजी का बोझ उठाने को तैयार हो जाए और अफ्रीकी महाद्वीप से ऊर्जा की आपूर्ति की सुरक्षा सुनिश्चित की जा सके, तो अफ्रीका में इस बात की काफ़ी संभावनाएं हैं कि वो यूरोप की रूस पर ऊर्जा निर्भरता को काफ़ी हद तक कम कर सकता है.

The views expressed above belong to the author(s). ORF research and analyses now available on Telegram! Click here to access our curated content — blogs, longforms and interviews.

Abhishek Mishra is an Associate Fellow with the Manohar Parrikar Institute for Defence Studies and Analysis (MP-IDSA). His research focuses on India and China’s engagement ...

Read More +