-

CENTRES

Progammes & Centres

Location

Creating a new system to stimulate investment in enough future capacity without interfering with the ancillary market's valuation and procurement of reserve capacity would be complicated in India

This article is part of the series Comprehensive Energy Monitor: India and the World

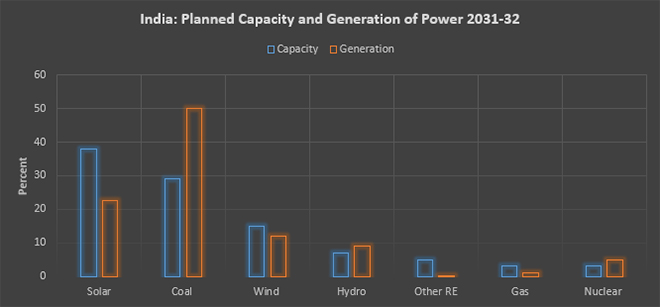

As of May 2023, India’s non-fossil fuel power generating capacity of over 173,619 megawatts (MW) was about 41.5 percent of the total installed power generating capacity of about 417,668.2 MW. New renewable energy (RE) capacity (excluding nuclear and hydropower) accounted for over 30 percent of total power generation capacity, the second largest share after coal. Solar, wind, small hydropower, biomass and others accounted for over 73 percent of non-fossil fuel-based capacity while large hydropower accounted for 27 percent and nuclear just 3 percent.

Though RE has the second largest capacity share, it accounted for less than 14 percent of power generation in 2022-23. Hydropower generation which has only about a third of renewable energy (RE) capacity accounted for over 10 percent of the power generation. Coal which accounted for about 50 percent of capacity contributed over 74 percent of generation in 2022-23. In terms of specific generation or power generated per unit of capacity that represents economic efficiency, nuclear power was the most efficient with a score of over 7 while RE power was the least efficient with a score less than 2 in 2022-23. This is because of low-capacity factors for RE which are in the range of 15-20 percent at best. Without stand-by capacity, a high RE power system can lead to compromise on the security of supply in the form of frequent power outages. As RE cannot be relied upon to provide needed electricity at any moment, other tools such as making payments for maintaining stand-by capacity (either in the form of batteries or in terms of gas or coal-based generation) or compensating consumers to reduce demand, when necessary, must be employed. India often uses the latter option of reducing demand through forced outages for rural consumers (or industrial consumers during elections when people are temporarily more valuable) who receive neither electricity nor payments for outages.

Consumers who are forced to accommodate outages are India’s back-up system or more accurately, its demand management system which is perverse and should be eliminated. The other credible options for supply security include creating vibrant markets for electricity, capacity, and ancillary services. India is technically an energy-only market but using the term market to describe India’s power sector is a stretch as the electricity tariff at one end and fuel supply at the other end do not respond to the market signals.

Capacity markets aim to ensure grid reliability by paying participants to commit generation for delivery years into the future. Energy-only markets, by contrast, pay generators only when they provide power on a day-to-day basis. Capacity markets prevent generating capacity that only supplies excess energy at high prices from being squeezed out of the wholesale electricity market in such quantities and at such speed that it may affect system reliability. Capacity markets that provide the opportunity to secure revenue years in advance give generators added incentives to build new plants. But the model could be wasteful, since financially challenged distribution companies (Discoms) in India will pay out the capacity costs for load events that may not materialise years down the line. Capacity markets also remain vulnerable to price depression as a result of out-of-market subsidies. If these resources also enter as price takers without any checks and balances into the capacity market, the regulator can end up compromising the ability of the capacity market to balance revenue flows. Capacity payments may also blur price signals on traded markets, preventing scarcity markets from functioning. Capacity remuneration also risks double payments to the generator-for energy and capacity.

In mature energy-only markets, regulators ensure reliability through a mechanism called scarcity pricing, which allows real-time electricity prices to increase on days of peak demand. Instead of guaranteeing generation revenue through a capacity market, the promise of high prices is supposed to incentivize generators to build new plants and keep them ready to operate. In an energy-only market, the grid’s reserve margin is maintained at sufficiently high levels allowing for enough instances of scarcity that increase prices to such an extent that generators can recover their capital costs. This can be seen in Indian electricity exchanges that demonstrate steep increases in electricity tariffs during summer months when the demand is high. The worry is that energy-only markets could become increasingly unstable due to the low electricity prices (on account of subsidies for certain energy forms or on account of depressed demand) which could discourage generators from building new power plants without guaranteed revenue of a capacity market. Essentially, securing sufficient flexibility in the system is a separate issue to stimulating investment in future capacity.

The critical difference is that in an energy-only market, generators must wait and hope for the day when real-time prices increase substantially. With a capacity market, some of that revenue is guaranteed. The capacity market is designed to provide a solution by balancing lower energy market prices with higher revenues for generators in the capacity market. Capacity remuneration mechanisms can remove investment incentives for demand-side response activity in the wholesale market and energy storage. They also impede cross-border electricity trade by reducing the peak-prices that make trade profitable. Over the long term, the energy-only and capacity market constructs could end up delivering similar cost results to consumers.

The third alternative, often confused with capacity markets, is to use ancillary service markets, which procure short-term reserve generation and grid support products for everyday system stability. As the proportion of RE continues to increase the demand for ancillary services to ensure daily operational stability is likely to increase. Ancillary services are traded in months, weeks, days and hours, not years like capacity. Ancillary service markets are for securing the right combination of resources for generation quality and not for generation adequacy. Competitive trading of these services is part of some, but not all, wholesale electricity markets. If generators can generate revenue from selling ancillary services, the need for capacity payments to keep plants online can be reduced. A properly functioning energy and services market can deliver all the capacity that the Indian grid requires.

The third alternative, often confused with capacity markets, is to use ancillary service markets, which procure short-term reserve generation and grid support products for everyday system stability. As the proportion of RE continues to increase the demand for ancillary services to ensure daily operational stability is likely to increase

India is slowly moving towards this system but there are significant challenges not only because it is an imperfect energy only market but also because India’s energy supply serves non-energy goals such as delivering development subsidies. However, keeping the future in mind, India’s central electricity authority (CEA), central electricity regulatory commission (CERC) and Grid India have studied the prospect of developing an ancillary services market But it is too early to say whether a well-designed market that makes it profitable for generators to provide ancillary services (short term reserves and grid support products) would also stimulate investment in future capacity in India. The worry is that continued policy-supported RE additions may keep electricity prices low, thereby reducing the incentive for generators to build new plants. Most of the RE is “aspirational capacity,” capacity directly contracted to meet commitments to multilateral climate treaties, not necessarily capacity needs. Reconciling environmental goals that demand more RE additions with the need to preserve market incentives for new generations is a critical challenge.

If India’s electricity sector matures into a vibrant open market, it can, at least in theory, value, reliability, and compensate investors for supplying fixed resources. A well-functioning wholesale electricity market in India should dynamically value the energy, support services, and capacity in response to the changing forces of supply and demand. An ancillary services market that responds to scarcity of flexible reserves by pushing up their price will make it profitable to operate peaking plants that can rapidly ramp up and down, giving generators a reason to keep plants online and invest in future capacity.

Another alternative is keeping strategic reserves of power generating capacity where the capacity mechanism is procured completely outside the wholesale market so that it does not compromise the move towards developing an energy market in India. As in the case of strategic oil reserves, it should be owned and operated by the government to provide national security (energy security), a public good. Strategic reserve for power generation is a pragmatic and relatively simple solution to meet the demand for short periods of extreme system stress. But the risk with a peak strategic reserve is that over time it can become just as expensive as a capacity market.

Creating a new system of benefits, or an entirely new market, to stimulate investment in enough future capacity without interfering with the ancillary market's valuation and procurement of reserve capacity is complicated even in the most mature market and much more so in India.

Source: Draft National Electricity Plan 2022

Lydia Powell is a Distinguished Fellow at the Observer Research Foundation.

Akhilesh Sati is a Program Manager at the Observer Research Foundation.

Vinod Kumar Tomar is a Assistant Manager at the Observer Research Foundation.

The views expressed above belong to the author(s). ORF research and analyses now available on Telegram! Click here to access our curated content — blogs, longforms and interviews.

Akhilesh Sati is a Programme Manager working under ORFs Energy Initiative for more than fifteen years. With Statistics as academic background his core area of ...

Read More +

Ms Powell has been with the ORF Centre for Resources Management for over eight years working on policy issues in Energy and Climate Change. Her ...

Read More +

Vinod Kumar, Assistant Manager, Energy and Climate Change Content Development of the Energy News Monitor Energy and Climate Change. Member of the Energy News Monitor production ...

Read More +