-

CENTRES

Progammes & Centres

Location

Some of the parameters used in the estimation of the SCC depend on ethical values, which could be subjective. This raises questions about the use of the SCC for policymaking in India.

A new paper (pre-print) from the National Bureau of Economic Research (NBER), United States (US), argues that the economic costs associated with climate change could be six times worse than the previous largest estimates, and 21 times worse than recent values used by the US government. Their estimation of the social cost of carbon (SCC) at US$1,056/tCO2 (per tonne of carbon dioxide) or US$3,872/tC (per tonne of carbon) is way outside the range of existing estimates of the SCC. High estimates of SCC justify increases in spending on mitigating climate change. While the conclusions of the paper are promoted by activist organisations and media outlets, uncertainties over the assumptions and methodology used in the paper to arrive at the high estimates for SCC are yet to be adequately scrutinised. Some of the parameters used in the estimation of the SCC depend on ethical values such as the rate of time preference (discount rate) and the rate of risk aversion both of which can be subjective and lead to an extraordinary range of values for SCC. This raises questions about the use of the SCC for policymaking in India.

SCC compares monetised benefits of policies that result in carbon reductions to their economic costs. Effectively SCC is the present value of future damages associated with an incremental increase (1 metric tonne) in CO2 emissions in a particular year expressed in consumption equivalent terms. In theory, damages from changes in agricultural productivity, human health risks, property damages from increased flood frequencies, and the loss of ecosystem services are included in most SCC models.

An earlier paper based on a sophisticated computational model identified parameters that contribute to uncertainty in SCC. The outcome of the model showed that for lower pure rates of time preference (discount rate plus product of the individual coefficient of risk aversion times the growth rate), the SCC increases and for higher rates, the SCC falls for lower rates because the effect on the discount rate dominates. For assumptions of average time preference and risk aversion, the global SCC was found to be US$12/tCO2 with complete global risk sharing and US$14/tCO2 without risk sharing. When specific equity weights are applied, the SCC ranges from US$2.4/tCO2 in the poorest region (South Asia) to US$1575/tCO2 in the richest.

Another paper estimated SSC by taking into account the future evolution of the economy without the impact of climate change, the Earth system response to emissions of CO2, the economy’s response to climate change, and the net present value of the time series of climate change related future damages arrived at a value of US$ 86/tCO2 for India, the highest, followed by US$48/tCO2 for United States (US) and US$47/tCO2. Brazil, the United Arab Emirates (UAE), and China were next with an SCC of US$24/tCO2. Northern Europe, Canada, and the erstwhile Soviet Union had negative SCC in this model because their current temperatures were below the economic optimum. In this model too the SCC varied considerably depending on the scenario and discount rate. According to the model, damage function uncertainty is a larger contributor to the overall uncertainty. The authors of the paper identified the divergence between country-level shares in CO2 emissions and country-level shares in the SCC as an important reason behind inadequate global carbon mitigation agreements. They concluded that if countries were to price their own carbon emissions at their own SCC, only about 5 percent of the global climate externality would be internalised. However, if the three highest-emitting countries (China, the US, and India) that also have the highest SCC, internalise the negative externalities of emissions by pricing carbon emissions at global SCC levels, it could result in emissions pathways for those countries that are consistent with the 1.5–2°C temperature target.

A paper that analysed the influence of inequality on the SCC concluded that climate and distributional policy cannot be separated. If only one country does not compensate low-income households for disproportionate damages, the social cost of carbon tends to increase globally. The model used in the study puts the SCC for India between US$80-130/tCO2 in 2035 under different assumptions. Higher values of SCC correspond to assumptions of higher inequality within households in the country.

India’s own assessment of country-level SCC is ambiguous. In the last decade, the only publicly available official document that dwells on SCC is the Economic Survey 2016-17. However, the concept of SCC is interpreted differently to justify the use of coal. The document begins by citing Nobel Laurette William Nordhaus who estimated India’s SCC at about US$2.9/tCO2 in 2015 and then proceeds to compare the social cost of coal with the social cost of renewables (RE). The social cost of coal-based power generation is calculated in terms of the number of annual deaths caused by coal-based pollution. Over 110,000 annual deaths attributed to pollution from coal-based power generation are estimated to impose a social cost of US$ 4.6 billion. For RE, the social cost is calculated by adding the cost of managing intermittency in power generation by RE, the opportunity cost of land required for RE-based power generation, the cost of stranded assets that RE displaces and the cost of government incentives for RE. The conclusion is that India is justified in its dependence on coal-based power as the social cost of using RE is three times that of coal. The Economic Survey 2016-17 also points out that India’s primary goals are to increase access to energy and close the development deficit gap.

The Economic Survey 2014-15 argued that India had moved from carbon subsidies to carbon taxation as part of its “green action”. Increasing taxes and levies and decreasing subsidies on petrol, diesel and coal justified this statement. Effectively taxes on coal and petroleum products were treated as implicit carbon taxes. In 2014, the implicit carbon tax on petrol was over US$ 140/tCO2 and that on diesel was US$64/tCO2 which was way above the prevailing global norm of US$25-35/tCO2. According to the OECD (Organisation of Economic Cooperation and Development) the effective carbon price in India in 2021 was US$16/tCO2 compared to the US$64/tCO2 a midpoint estimate for carbon costs in 2020, and a low-end estimate for 2030. A country is on a good track to reach the goal of the Paris Agreement to decarbonise by mid-century economically as per OECD classification when it prices carbon at US$64/tCO2 or more in 2020. In May 2024, the total tax levied on a litre of petrol in India was over INR35 and that on diesel was INR28.6. This is roughly equivalent to a carbon tax of US$175/tCO2 for petrol and about US$145/tCO2 for diesel. The average tax per tonne of coal is about INR797/tonne, corresponding to a carbon tax of US$6/tCO2. This implies that the effective carbon tax on petroleum products is higher than what is called for by carbon pricing policies or those set on the basis of SCC.

Global-, regional-, and country-level SCC is computed by models using a number of assumptions of which many are uncertain. Ethical values that set intergenerational time discounting and equity weights for rich and poor regions contribute to wide variation in SCC values that could be as large as three orders of magnitude. The damage function or the monetary value of climate damage that underpins SCC models is known to be unknowable. However, the models use assumptions to replace uncertainties and unknowables and the result is expressed in a simple number that suggests a level of knowledge and precision that is non-existent. The seductive power of quantitative analysis and outcomes often precludes comprehensive analysis that includes social and political choices in addressing climate change.

The concept of SCC which is subject to interpretation has received more interest from academics than from policy makers. Studies on academic studies of SCC have shown that authors of primary studies tend to report preferentially which creates an upward bias in the literature. The results also indicated that selective reporting tended to be stronger in studies published in peer-reviewed journals than in unpublished manuscripts.

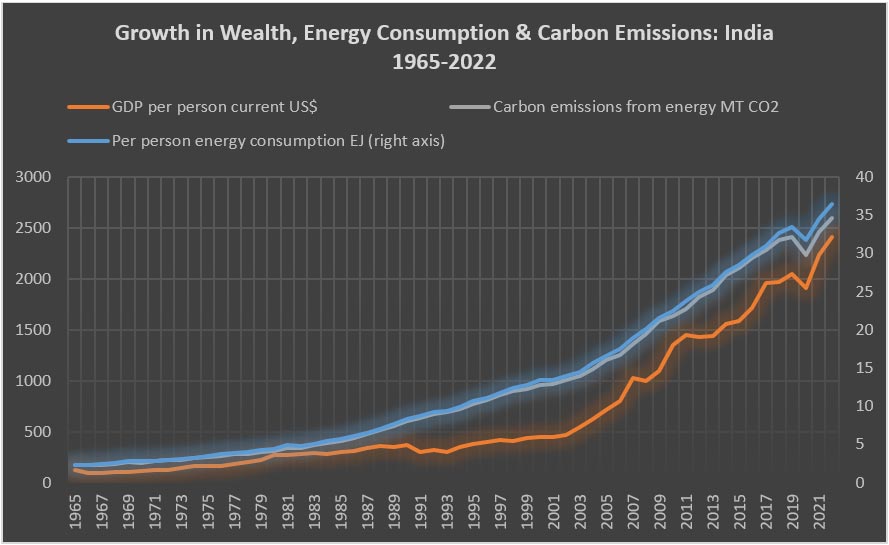

While the fact that the SCC is positive cannot be denied, developing countries such as India have also benefited from the use of fossil fuels (carbon). Since 1960, the global average temperature has increased by 0.75C. In this period India’s per person energy consumption has increased more than 16-fold resulting in a 20-fold increase in per person gross domestic product (GDP). This has translated into a dramatic increase in life expectancy at birth from about 45 years in 1965 to about 70 in 2022 as well as substantial improvement in quality of life. In light of the social benefits of carbon, it may be wise to weigh disaster narratives quantified with complex computational tools against evident qualitative development outcomes in climate policymaking.

Source: Per person GDP-World Bank; Energy consumption per person & CO2 emission-Statistical Review of World Energy

Lydia Powell is a Distinguished Fellow at the Observer Research Foundation.

Akhilesh Sati is a Program Manager at the Observer Research Foundation.

Vinod Kumar Tomar is a Assistant Manager at the Observer Research Foundation.

The views expressed above belong to the author(s). ORF research and analyses now available on Telegram! Click here to access our curated content — blogs, longforms and interviews.

Ms Powell has been with the ORF Centre for Resources Management for over eight years working on policy issues in Energy and Climate Change. Her ...

Read More +

Akhilesh Sati is a Programme Manager working under ORFs Energy Initiative for more than fifteen years. With Statistics as academic background his core area of ...

Read More +

Vinod Kumar, Assistant Manager, Energy and Climate Change Content Development of the Energy News Monitor Energy and Climate Change. Member of the Energy News Monitor production ...

Read More +