The early trends on electoral bonds suggest that the new channel would greatly undermine India’s electoral democracy by inviting unbridled corporate influence

On January 2, 2018, the National Democratic Alliance (NDA) government notified the enforcement of Electoral Bond Scheme (EBS). The Union Budget 2017 which for the first time devoted a full section on political funding reforms, introduced the novel bonds scheme to check rampant “under-the-table cash transactions”. The key motive behind EBS as stated by the Finance Minister Arun Jaitley was to infuse political system with “white money” to fight the scourge of black money. However, with controversial features like anonymity for donors and corresponding removal of 7.5% limits for corporate donations, EBS has attracted considerable attention from many corners particularly the regional parties, press, civil society actors and election watchdogs who have challenged the scheme before the Supreme Court. Even the Election Commission of India called it “a retrograde step”. The highest court, which had earlier asked for a response from the Central government, is set to hear the case on 2nd April 2019. While the petition is being heard, let us capture the key early trends emerging from the scheme.

What is an electoral bond?

Electoral bond is a bearer instrument in the manner of a promissory note and an interest free banking instrument whereby a citizen, or a corporate body, in India is eligible to purchase (through cheque or digital payments only) the bond from notified branches of the public sector bank (State Bank of India) for 10 days each in months of January, April, July and October. The electoral bonds can be purchased for specified denominations and the payee then can bestow it upon a registered political party as donation.

The key highlight of the scheme is that the bonds will stay valid for 15 days and shall not carry the donor's name, although the payee will have to fulfil KYC (Know Your Customer) norms at the bank. Further, no report is required to be submitted by receiving parties in case of donations received via electoral bonds. In short, neither the donors nor the political parties are obliged to reveal the sources of donations.

What Makes Electoral Bonds Controversial?

While EBS would act as a check against traditional under-the-table donations as it insists on cheque and digital paper trails of transactions, several key provisions of the scheme that make it highly controversial. First, anonymity clause or lack of disclosure requirements for the individuals or corporates buying electoral bonds defeats the fundamental principle of transparency in political finance. Opacity in donation would make it a convenient channel for black money. To extend this further, EBS could be convenient channel for business to round-trip their cash parked in tax havens to political parties for quid pro quo. What makes the scheme even more controversial is the removal of 7.5% cap on corporate donations (by amending the Companies Bill 2013). This allows for unlimited corporate donations even from the loss making companies. Finally, given the fact that a public sector bank (SBI) will be sole repository of donor details, in effect the government of the day (given the proximity with the bank) will have an upper hand on this new mode of donations.

Early Trends

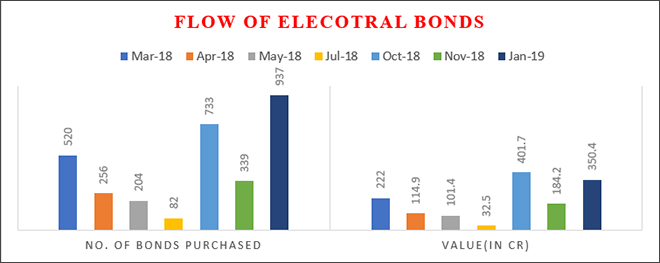

Starting March 2018, seven tranche of bonds have been rolled out (Table 1). From the below mentioned data (Table 1 & Figure 1), it is easily discernible that electoral bonds have emerged as the most popular channel of donations to parties. In less than a year, as much as INR 1407 crore (Figure 1) donations have flown in the form of bonds.

Table -1 No. of Electoral Bonds and their values

Issuance & value of bonds purchased

Month

No. of bonds purchased

Value(in Cr)

Mar-18

520

222

Apr-18

256

114.9

May-18

204

101.4

Jul-18

82

32.5

Oct-18

733

401.7

Nov-18

339

184.2

Jan-19

937

350.4

Total

3071

1407.1

Source:Computed from ADR data

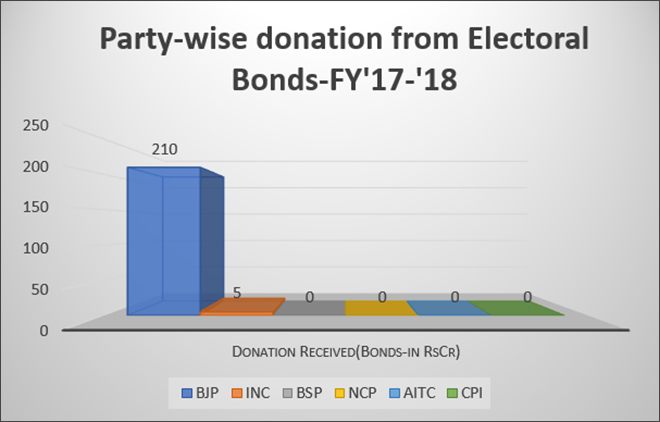

Second and the most alarming trend is complete lopsided flow of donations from bonds. As forewarned by many analysts, the ruling Bharatiya Janata Party has captured as much as 95 per cent of total EBS donations (Figure 2). This greatly undermines the principle of equality in political finance, a cornerstone for a healthy and equitable democracy.

Third, until 2016 donations coming through Electoral Trusts used to be the most dominant (known) source of funding for political parties. However, the entry of bonds scheme is beginning to change that. For instance, as per the available data the contribution from electoral trust for FY 2017-18 was INR 194 crore, whereas first tranche of bonds garnered INR 222 crore (March 2018). This easily establishes that individual corporate who earlier used to make their contribution through Electoral Trusts are now routing the same through the new channel. The clearest proof of this is that nearly all bonds (99.9%) purchased are of high value denominations between INR 10 lakh and INR 1 crore, implying corporates are preferring bonds channels for political donations.

Key trigger seems to be anonymity clause in EBS, which protects donor’s identity. Whereas, an electoral trust has a mandatory requirement to submit a report to Election Commission listing contributors and donations to different parties. While this is early trend based on 13 months data, it should serve as a wake-up call for the policy makers. This is surest way of inviting unbridled corporate influence into politics and governance of the country, and the negative implications of cosy business-politics relations are widely known.

Finally, as discussed above, given its anonymity provision, EBS is likely to push the trends of “unknown” source of political donations in India. This goes against the grain of clean campaign finance goal as the NDA government had loudly claimed in its 2017 Finance Bill.

To conclude, the early trends on electoral bonds attest to what political analysts have been fearing that the new channel would greatly undermine India’s electoral democracy by inviting unbridled corporate influence. Electoral bonds along with corresponding changes that the government introduced in 2017 Finance Bill particularly the removal of 7.5% cap in corporate donations undo the significant gains achieved in political finance reforms and transparency norms. To put it simply, electoral bond is an anathema for a healthy democracy and the government should read the early warnings as succinctly captured in the key trends.

Figure-1 Flow of Electoral Bonds

Source: Computed from ADR data (released by political parties)

Figure 2: EBS Donations to Political Parties

Source: Computed from ADR Data (based on March 2018 tranche)

Niranjan Sahoo is a Senior Fellow, ORF and Niraj Tiwari is a Research Intern, ORF.

The views expressed above belong to the author(s). ORF research and analyses now available on Telegram! Click here to access our curated content — blogs, longforms and interviews.

Niranjan Sahoo, PhD, is a Senior Fellow with ORF’s Governance and Politics Initiative. With years of expertise in governance and public policy, he now anchors ...

On January 2, 2018, the National Democratic Alliance (NDA) government notified the enforcement of Electoral Bond Scheme (EBS).

On January 2, 2018, the National Democratic Alliance (NDA) government notified the enforcement of Electoral Bond Scheme (EBS).  Source: Computed from ADR data (released by political parties)

Source: Computed from ADR data (released by political parties) Source: Computed from ADR Data (based on March 2018 tranche)

Source: Computed from ADR Data (based on March 2018 tranche)