-

CENTRES

Progammes & Centres

Location

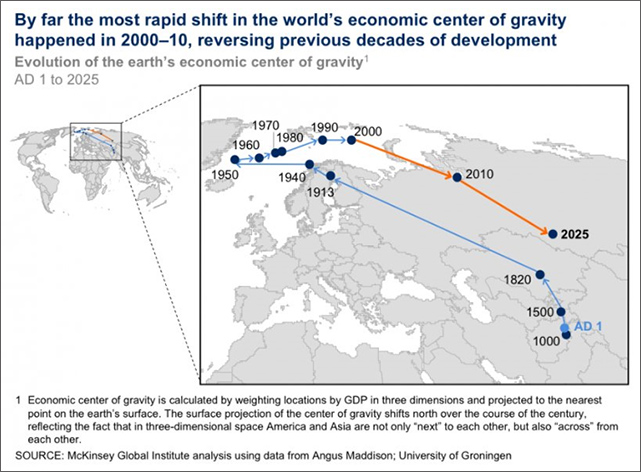

Predictions that the 21st century will be the Asian century appear to have been borne out already. From the 1990s there has been a decisive shift in global economic activity—current projections pit the centre of economic activity globally between India and China by the middle of the century.<1> This shift in economic activity—arguably a return to patterns before the industrial revolution—has occurred over an unprecedentedly short period of time. Over 2003-2013, the global median level of real income nearly doubled.<2> This was essentially an Asian effect, the only region to experience sustained productivity growth and catch-up this century; above all, this transformation has been driven by Chinese and Indian growths. China is likely to overtake the United States soon as the world’s largest economy and the World Economic Forum predicts that India will become the world’s third-largest economy by 2030.<3> Asian economies succeeded through embracing globalisation, but they did so on their terms. More subtly, emerging economies have come to play a much greater role in global economic governance, notably as the G7 was superseded by the G20 and through a more active role within the World Trade Organisation (WTO) in particular. Further, emerging economies have started to construct institutions of international economic cooperation and governance parallel to existing ones established and dominated by Western powers. Asian economies, particularly China, have forged new trade and investment relationships with emerging economies in Africa and Latin America. The period before the global financial crisis was characterised by a phase of hyper-globalisation based on a particular conception of global integration that came to be associated with a policy package of openness to trade and financial flows and general economic liberalisation. This came to be seen as driven by US economic hegemony, often dubbed the Washington Consensus, although the European Union was also an active player particularly in the field of financial liberalisation. The new economic relations promoted by emerging economies in Asia and elsewhere have reshaped the architecture of economic globalisation in the 21st century.

Yet the future of these trends now poses major challenges for Asian countries, both in terms of globalisation generally and the role of Asian development models specifically. Only a decade ago, globalisation trends were widely expected simply to continue—global flows of trade, investment and finance would continue to grow, global economic governance would continue to evolve to promote such flows and reduce barriers to them. Since the 2007/08 global financial crisis (GFC) global growth has been continued to be anaemic—emerging economies were central to dragging the world economy out of the post-crisis downturn, but latterly growth has slowed in China and elsewhere (although it remains strong in India). China responded to the GFC with a major stimulus package, but with the slowdown there may be emergent debt problems in its banking and shadow banking sectors.<4>

More fundamentally, developments since the GFC have challenged assumptions of ever-growing globalisation. Trade flows fell sharply at the start of the crisis and, although growth has resumed, it remains subdued and is no longer growing relative to GDP.<5> Foreign direct investment flows of multinational corporations have only recently resumed growth, having slumped after the financial crisis, and they too have ceased to grow relative to GDP.<6> The reversal of financial globalisation has been even more dramatic—international financial flows had grown exponentially from the 1970s but have fallen back since to a fraction of their pre-crisis levels; relative to GDP, international financial flows are now comparable to levels last seen in the mid-1980s.<7> Much of this is driven by retrenchment of cross-border banking flows—unsurprisingly in the aftermath of a financial crisis—but it also points to reduced appetite for the risks of international investment. The persistence of these trends indicates more than just a cyclical phenomenon. Not only have flows fallen, barriers may also be returning. Even before the GFC, the Doha round of the WTO had become deadlocked, not least because of a lack of agreement between emerging economies and Western powers. Whilst the financial crisis did not see a return to 1930s-style protectionism, trade barriers did rise and are partly responsible for the subdued level of global growth. The election of Donald Trump and the UK’s Brexit vote point to a turn against globalisation; already the Trans-Pacific Partnership (TPP) and Transatlantic Trade and Investment Partnership (TTIP) negotiations appear doomed. There is historical precedent from the inter-war years for a turn against globalisation. Emerging Asian economies are central to the globalisation processes that have brought the world economy to its current juncture.

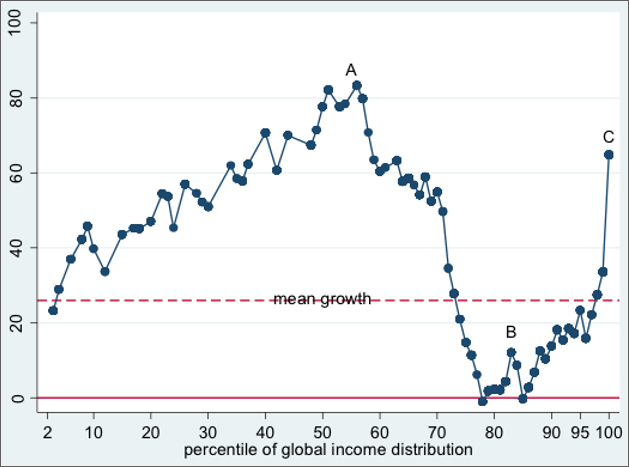

Whilst countries elsewhere have registered gains, the global transformation is essentially a story of the rise of emerging Asian economies—above all, China and India. Initially globalisation developed from the 1980s largely as an intensification of flows between developed countries, but a series of technological developments and policy shifts led to a wholesale shift of global manufacturing power. As Richard Baldwin has recently documented,<8> economic globalisation of the past quarter century has seen the development of global value chains leading to the rapid industrialisation of emerging economies and the further deindustrialisation of developed economies. What is unprecedented here is the combination of trade openness with the new information and communication technologies (ICTs), enabling the flow of ideas and technological know-how. Offshoring enabled the transfer of advanced technology and the rapid evolution of manufacturing in emerging economies; this drove the unprecedented growth and catch-up in Asia. Emerging economies were able to access leading-edge technologies and multinational companies were able to transfer production to lower-wage economies. These new ICTs effectively eliminated many of the barriers to diffusion of advanced technological know-how, enabling a shift in manufacturing to Asia.

This wholesale shift in industrial production has created a profound pattern of winners and losers. In what Milanovic has characterised as the “greatest reshuffle of individual incomes since the industrial revolution,” growth in the two decades before the GFC was concentrated around the global—the vast majority in Asia—and amongst the global top one percent.<9> On the other side, incomes stagnated for lower and middle income earners in developed countries; the timing and extent of this varied between countries, but the combined effects of globalisation, policy shifts, automation and anaemic growth have hit household income growth across the developed world.<10> In these circumstances the populist backlash in Europe and the United States—focused on trade, immigration, or both—is not surprising. Increasingly, parallels are drawn with the inter-war retreat from the pre-First World War phase of globalisation.

Cumulative real income growth between 1988 and 2008 at various percentiles of the global income distribution

Source: Milanovic (2016)

Source: Milanovic (2016)The Asian growth model has been predicated upon export-led growth through manufacturing and high levels of savings and investment; since the 1997 East Asian crisis this has entailed current account surpluses. There are major external and internal challenges to the future of this model. The shift in industrial power over recent decades is very unlikely to be reversed in the foreseeable future; whatever his election promises, Donald Trump won’t be able to engineer a renaissance in American manufacturing. Instead, the shift in manufacturing towards emerging economies is likely to continue. Nevertheless, the growth of world trade has slowed and Asian export growth has not picked up with the recovery of the global economy in contrast to earlier global downturns. The rapid expansion of trade before the GFC with the spread of global value chains now appears exceptional. Trade barriers have risen, and may rise significantly further under the Trump administration. Further, the model itself became increasingly reliant on the United States as the ‘consumer of last resort.’ The imbalances that developed between trade deficits in the United States and surpluses in Asian economies cannot be sustained indefinitely (ultimately, growth of consumer demand in the United States was based on rising house prices, falling savings and rising debt). In the face of sluggish world trade growth Markus Rodlauer, deputy director for Asia and the Pacific at the International Monetary Fund, has gone so far as to assert that “

Internally, too, there are a number of challenges to the continuation of this model. Latterly developing economies appear to be experiencing ‘premature deindustrialisation’—manufacturing output and, especially, employment peaking at lower levels of income than was the case historically. This is particularly significant given the evidence that manufacturing is central to productivity growth and development. In general Asia has been the major exception to these trends; indeed, its very success in industrialisation appears to have limited the opportunities for further industrialisation in Africa and Latin America. However, India does display signs of this phenomenon,<12> although a combination of factors has underpinned its advantage in services trade. In the past manufacturing generated mass employment and was central to absorbing labour from agriculture. As advanced technology spreads modern factories in emerging economies, like their counterparts in the already industrialised world, these are far less labour intensive. In 2016 Foxconn was reported to have replaced 60,000 factory workers in China with robots.<13> The demographics pose key challenges for China and India, particularly in both generating sufficient employment to continue to absorb workers with basic education and skills whilst also ensuring growth of a skilled workforce to enable up-grading of production.<14> This is closely related to the potential challenge of ‘middle income trap’; it has been claimed that although countries may find it relatively easy to achieve some development, they appear to hit a ceiling rather than accede to the still small club of rich nations. Low-wage industries are increasingly footloose, but transitioning from initial export-led manufacturing growth to more sophisticated production as incomes rise requires a set of policies, skill generation and institutions.

Related to these developments, Asian economies have also experienced significant rises in inequality since 1990. Historically labour-intensive export-led industrialisation in Asia produced relatively egalitarian outcomes through strong growth of formal employment; although Asia remains on average more equal than Africa or Latin America, the general forces that have raised inequality in developed countries―globalisation, technological change and policy shifts―have also acted to manifest themselves in the same adverse manner across emerging Asian economies.<15> In the face of mounting evidence that inequality is economically harmful and politically destabilising, these developments raise concerns over the sustainability of current development paths.

The rapid pace of industrialisation based on the spread of global value chains may render older policy packages redundant or inoperable, but neither upgrading nor ensuring inclusive growth is a simple task or an automatic process. Recent proposals for revitalising industry sketch out strategies that may enable governments to adapt policy tools to develop capabilities so that countries are able to upgrade within value chains.<16>

Trade and financial integration are often discussed separately, but for emerging economies these have become intertwined. In the aftermath of the 1997 East Asian currency crises emerging economies have attempted to manage their exchange rates to ensure continued export growth and strong external balances. This has been associated with an accumulation of reserves that has, in turn, brought forth accusations of currency manipulation, particularly in the United States. The financial turbulence following the GFC, combined with low interest rates and quantitative easing, led to potentially disruptive capital flows to emerging economies. (This also led to accusations of currency manipulation against the United States; the possibility of currency wars remains). In response to this China, India and a number of emerging economies in East Asia and elsewhere instituted capital controls or utilised existing such provisions to manage these inflows. There has been a striking shift in the intellectual climate since the start of the crisis that now claims that capital controls are a potentially useful tool for emerging economies to manage capital flows and mitigate associated risks. The IMF in particular appears to have adopted a more lenient view of some forms of capital controls. This has occurred in the context of a marked retrenchment in international financial flows. Emerging economies have retained considerable access to international finance—in particular, external corporate debt in emerging economies has boomed over the past decade under conditions of accommodative monetary policy and weak economic prospects in developed economies.

Financial liberalisation had become increasingly entwined with trade agreements in practice. The General Agreement on Trade in Services under the auspices of the WTO does have provisions for opening up capital markets. Further, regional and bilateral trade agreements with developed countries have increasingly aimed at opening up emerging economies’ financial markets. Bilateral investment treaties―the principal means of negotiating arrangements for foreign direct investment in the absence of an established global regime for this—also frequently include provisions for financial openness.

Here the emerging economies’ response has shaped the evolution of the global financial architecture. Acting in consort through international economic agencies they have cooperated to create provisions to regulate capital flows and create policy space. National finance often underpinned the export-led growth model, directed to national priority sectors and export promotion. Asian countries have actively cooperated with emerging economies in Africa and Latin America on this. The result has been a shift to reregulate global finance in the aftermath of the GFC, in contrast to earlier developments. This has been one of the influences in the shift in policy thinking in international agencies, but has also been reflected in the response of the G20 to emphasise measures to address international financial instability and effective macroprudential regulation.

This process of reregulation of international finance by emerging economies entails a partial return to national regulation of finance rather than the construction of a new global financial regime. The US dollar remains the dominant currency and although the IMF adding the Renminbi to its Special Drawing Rights is symbolic of China’s global importance, there is little prospect of it rivalling the dollar in the foreseeable future. Rather than envisaging developments in terms of emergence of a single international monetary hegemon, in the way the United States in the 20th century took over from Britain in the 19th, emerging market economies are not seeking to create a unified international monetary system. Rather, they have used their increasing power to reshape the operation of global finance. As well as their activity within international economic agencies, there have been a number of key initiatives between emerging economies, notably the establishment of the New Development Bank (headquartered in Shanghai) and the Asian Infrastructure Investment Bank, as well as plans to create a BRICS-based credit rating agency.

The global financial crisis bookended a phase of hyper-globalisation, based on a conception of a unified set of global rules and an expectation of continuously rising global flows. The financial crisis itself raised profound questions over the effectiveness of global arrangements in ensuring financial stability. While for earlier proponents of globalisation, the phenomenon could ensure general prosperity—or, at least, only a relatively small minority of national populations would be affected adversely—today, wider concerns over globalisation have emerged and strengthened

In practice a far more disruptive reconfiguration of economic power has been underway. The combination of global integration and ICTs has meant that advanced technological know-how is no longer essentially the preserve of richest countries. The establishment of global value chains has created industrialisation and productivity growth in emerging Asia at an unprecedented rate. This has also created major global patterns of winners and losers—the flip-side of income growth in middle income countries has meant stagnation of incomes for swathes of households in developed ones. The drive towards deeper trade agreements now appears to be over—the backlash from groups in developed countries appears to have effectively stopped TPP and TTIP. More widely the increased organisation of emerging economies within the WTO has changed the nature of global trade negotiations. For some analysts these developments raise the possibility of a reversal of globalisation, comparable to that seen during the Great Depression. The prospect of a return to US protectionism under a Trump administration and even the possibility of the European Union imploding do raise concerns. However, the analysis here points to a more nuanced outcome. The response to this from emerging Asian economies has been to cooperate with other emerging economies and effectively this is leading to a multi-polar system of globalisation.<17> A series of initiatives amongst the BRICS are leading to emerging financial relations amongst emerging economies. China’s New Silk Road strategy is an alternative mechanism for integration from traditional trade agreements, but could potentially integrate markets across Eurasia.

The emergence of a multipolar system of globalisation poses particular challenges for emerging Asian economies. The dangers of rising protectionism and an inward turn amongst developed economies have already been highlighted. Global trade negotiations through the WTO have stalled; regional trade negotiations continue, but these could lead to fragmentation of global trade. Further, critics have noted that recent regional trade agreements often contain provisions strengthening firms’ intellectual property rights. International technological diffusion has been central to the industrialisation of emerging Asia, and measures that entrench the advantages of developed country multinational enterprises may limit the ability of emerging economies to absorb best practice technology.

Although recent developments have focused attention on the potential for a rise in trade protection, the future development of the international financial system remains at least as important for emerging Asia. The global financial system remains US dollar-based. It has not functioned effectively to promote development—flows to emerging and developing countries have often been too low, too volatile and too short term. In response to the 1990s crises, emerging Asian economies have pursued strategies of reserve accumulation as an insurance policy, but this entails significant costs and creates global economic tensions. Since the 2007 global financial crisis emerging economies have effectively utilised countervailing power to enhance domestic policy space and promote new arrangements, but this falls some way short of reshaping the global financial system.<18> A shift to a multipolar system which reflects the shifts in economic activity would offer the potential for the emergence of an international financial architecture more conducive to development finance. However, developments since the global financial crisis point to only limited reform and a marked continuation of existing relations.

The industrialisation of emerging Asia still looks set to continue. The Asian growth model does face challenges in the face of sluggish global growth, and of ensuring sustained productivity growth and inclusivity within nations. Nevertheless, emerging Asian economies have reshaped global production and through their increased role in international integration, they have reshaped the nature of globalisation from the Western hyper-globalisation model of the 1980s and 1990s.

This article was originally published in Raisina Files: Debating the world in the Asian Century

<1> Danny Quah, “The Global Economy’s Shifting Centre of Gravity,” Global Policy 2, no. 1 (January 2011).

<2> Tomas Hellebrandt and Paolo Mauro, “The Future of Worldwide Income Distribution,” Peterson Institute for International Economics Working Paper 15–7, April 2015, https://piie.com/publications/working-papers/future-worldwide-income-distribution.

<3> Wolfgang Lehmacher, “Why China should lead the next phase of globalization,” World Economic Forum, November 22, 2016, https://www.weforum.org/agenda/2016/11/china-lead-globalization-after-united-states/.

<4> Richard Dobbs et al., “Debt and (not much) deleveraging,” McKinsey Global Institute report, February 2015, http://www.mckinsey.com/global-themes/employment-and-growth/debt-and-not-much-deleveraging.

<5> WTO, World Trade Report, 2016 and 2013, part II.

<6> UNCTAD, World Investment Report, 2016.

<7> Kristin Forbes, “Financial “deglobalization”?: Capital flows, banks, and the Beatles” (speech, November 18, 2014).

<8> Richard Baldwin, The Great Convergence: Information Technology and the New Globalization (Cambridge: Harvard University Press, 2016).

<9> Branko Milanovic, Global Inequality: A New Approach for the Age of Globalization (Cambridge: Harvard University Press, 2016).

<10> Richard Dobbs et al., “Poorer than their Parents? A new perspective on income inequality,” McKinsey Global Institute report, July 2016, http://www.mckinsey.com/global-themes/employment-and-growth/poorer-than-their-parents-a-new-perspective-on-income-inequality.

<11> Quoted in Wayne Arnold, “Asia’s Export Engine Splutters,” Wall Street Journal, April 28, 2014, http://www.wsj.com/articles/SB10001424052702304163604579527483006022494.

<12> Amrit Amirapu and Arvind Subramanian, “Manufacturing or Services? An Indian Illustration of a Development Dilemma,” Center for Global Development Working Paper 409, June 2015.

<13> Jane Wakefield, “Foxconn replaces ’60,000 factory workers with robots,’” BBC, May 25, 2016, http://www.bbc.co.uk/news/technology-36376966.

<14> Richard Dobbs et al., “The World at work: Jobs, pay, and skills for 3.5 billion people,” McKinsey Global Institute report, June 2012, http://www.mckinsey.com/global-themes/employment-and-growth/the-world-at-work.

<15> ADB, Asian Development Outlook 2012: Confronting Rising Inequality in Asia (Manila: ADB, 2012); R. Balakrishnan, C. Steinberg and M. Syed, “The Elusive Quest for Inclusive Growth: Growth, Poverty, and Inequality in Asia,” IMF Working Paper 13/152, 2013, https://www.imf.org/external/pubs/ft/wp/2013/wp13152.pdf.

<16> Transforming Economies: Making industrial policy work for growth, jobs and development, eds. Jose M. Salazar-Xirinachs et al. (Geneva: ILO, 2014).

<17> Some of these issues are explored in more detail in Marko Juutinen and Jyrki Käkönen, “Battle for

Globalisations? BRICS and US Mega-Regional Trade Agreements in a Changing World Order,” ORF Monograph, March 21, 2016, https://www.orfonline.org/research/battle-for-globalisations/.

<18> See: Kevin Gallagher, Ruling Capital: Emerging Markets and the Reregulation of Cross-Border Finance (Ithaca: Cornell University Press, 2015).

The views expressed above belong to the author(s). ORF research and analyses now available on Telegram! Click here to access our curated content — blogs, longforms and interviews.