-

CENTRES

Progammes & Centres

Location

PRC has realised that the trade in weapons can serve several Chinese foreign policy and economic objectives

The Chinese defence industry has made rapid advances in the recent past. Data compiled by the Stockholm International Peace Research Institute (SIRPI) for the year 2021 indicates that Chinese defence companies were at the forefront of defence sales in the Asia-Oceania region. Although the United States’ defence industry sits at the apex of the world’s major weapons manufacturers, the Chinese have significantly expanded their footprint in the Asia-Oceania region accounting for over 80 percent of all weapons sales from the region. What accounts for the People’s Republic of China’ (PRC) defence industry gains in weapons sales and dynamism? The PRC’s rise as a significant defence industrial actor on the global stage owes to systematic and relentless investments since its inception as a communist state in 1949.

Virtually, the entirety of China’s major defence industries ranging from space technology to electronics to shipbuilding and synthetic chemicals have come from PLA contractual support to these industries.

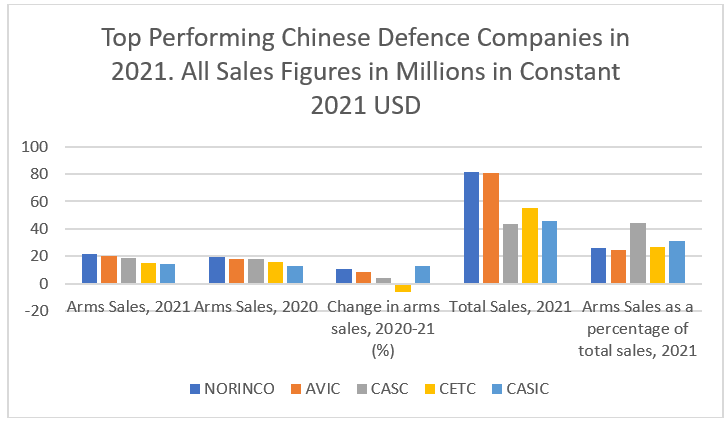

The most crucial variable that explains the robustness of today’s PRC’s defence-industrial base is the Peoples Liberation Army’ (PLA) and its senior leadership’s sustained commitment and patronage of the Chinese defence industry. Virtually, the entirety of China’s major defence industries ranging from space technology to electronics to shipbuilding and synthetic chemicals have come from PLA contractual support to these industries. The penetration of the Chinese military into the country’s economy at the institutional, organisational and ideological level occurred during the most perilous phase of China’s external threat environment between the years 1950 and 1969. The PLA’s influence at the level of policy, ideology, organisation and process continued into the Reform era starting in 1978. The distinctive features of the PRC’s innovative organisational strategy towards national security involved an absolute commitment to self-reliance, despite periodic purchases from abroad and co-production. The defence industry has successfully blended institutions that combined Stalinist top-down mobilisation of resources with an incentive structure that mimics the Silicon Valley’s entrepreneurship characterised by risk-taking, individual incentives, initiative and networks of cooperation among technical experts. Notwithstanding setbacks to broader reform under Xi Jinping, China’s defence industrial base has not suffered any tangible or visible damage. Consequently, the Chinese defence industry has thrived and the latest SIPRI report bears this out in the form of large arms sales for the year 2021. A cursory look at Chart 1 will illustrate why the Chinese defence industry has thrived despite the COVID-19 pandemic and all the supply chain issues that have adversely affected the defence industries of other countries. China North Industries Group Corporation Limited (NORINCO) saw a surge in sales by 11 percent in 2021 as opposed to 2020, whereas the second-ranked company Aviation Industry Corporation of China (AVIC) saw a rise by 9 percent in sales from 2020 to 2021. The third major company to make a gain of 4.2 percent in 2021 in contrast to 2020 was China Aerospace Science and Technology Corporation (CASC). China Aerospace Science and Industry Corporation (CASIC) saw a jump in sales by 13 percent from 2020 to 2021. Only China Electronics Technology Group Corporation (CETC), albeit by the measure of total sales exceeded CASC and CASIC and which builds Information Technologies and Electronics experienced a fall by 5.6 percent, but then supply-chain disruptions in these technological sectors were among the worst hit worldwide as a result of the pandemic.

Chart – 1

Source: Adapted from Stockholm International Peace Research Institute Report, 2022

Despite the rapid advances made by the PRC’s defence industry—there are three core areas where the Chinese still face challenges: very advanced electronics, submarine quieting technology and shipbuilding technology in the area of propulsion which involves precision engineering. Although China’s development of conventional submarines is moving from Air-independent propulsion systems to lithium-ion batteries. In due course, Russian assistance in submarine quieting technology will help Beijing reduce the gap with more advanced naval powers such as the US. The Chinese have also made considerable investments in space, cyber, electronic warfare, Artificial Intelligence (AI) and quantum technology. Indeed, the advances made by the Chinese in indigenous defence capabilities and several emerging technologies has precipitated to a large extent the US’ “Third-offset” strategy win a quest to maintain technological superiority over its rivals in specific technology fields such as AI, cyber capabilities, unmanned systems, and machine learning.

The PRC’s challenge on critical and emerging technologiesThe Creating Helpful Industries to Produce Semiconductors and Science Act (CHIPS Act) passed by the United States Congress recently is a US$ 53-billion law geared to subsidising and assisting the American semi-conductor industry from Chinese competition. It bars American companies that are beneficiaries’ of subsidies under the Act from investing in China’s semi-conductor industry in a quest to “catalyse” advance Research and Development (R&D) within the US. Most importantly, semi-conductors are a vital component in key weapons extending from missiles to Artificial Intelligence (AI) to automotive parts and China’s tension with world’s largest manufacturer of semi-conductor. To be sure, semi-conductors and submarine propulsion are high-end technologies. However, the success of the Chinese defence industry is instructive—by adopting a “good enough development model” that is absorption based keeping costs low and acquiring capabilities at a rapid clip, the Chinese have managed carry out a vast amount of indigenisation making them a fairly effective seller of defence products to the Chinese armed services and a competitive defence exporter, but Beijing faces a serious challenge in migrating from an absorption-based development model to an innovation-based development that involves more cutting edge weapons development. The latter will test the Chinese defence industry’s capacity to keep costs low even as innovation is advanced to meet the acquisition requirements of the Chinese armed services. At least between 2016-2020, the PRC’s primary defence export destinations were Pakistan, Bangladesh and Algeria, which respectively imported 38 percent, 17 percent and 8.2 percent of defence systems. Apart from the aforementioned countries, in 2011, the Chinese started exporting combat or armed Unmanned Aerial Vehicles (UAVs) to Saudi Arabia, Egypt, and Uzbekistan. Armed UAVs were until that point only being used by the US, Israel, and Britain and the only country the US exported UAVs were to France. It is also indicative of the distance the PRC has traversed transitioning from a major importer of weapons to now a major defence exporter.

On the pretext of training and upgradation programmes meant for the civil service through initiatives like the ‘China-Africa Action Plan’, China increased the intake of defence personnel.

It seems that the PRC has realised that the trade in weapons can serve several Chinese foreign policy and economic objectives. Take the case of Africa, which is rich in hydrocarbons and minerals that are a draw for China’s economy, the world’s second largest after the US. The continent is also important to China, given that Xi’s ‘Belt and Road’ initiative aims at connecting Beijing to Africa and Europe through a network of ports, railway lines, power stations and special economic zones. Here, China seeks to bind itself to other one-party states in Africa and makes common cause with them through antipathy with the West. Ahead of the Forum on China-Africa Cooperation in November 2021, Xi’s address harped on the need to “oppose intervention in domestic affairs, racial discrimination and unilateral sanctions … and translate our common aspirations and interests into joint actions”, alluding to the West that has on several occasions pulled up African governments for violations of human rights. On the pretext of training and upgradation programmes meant for the civil service through initiatives like the ‘China-Africa Action Plan’, China increased the intake of defence personnel. In 2018, China hosted senior military officials from 50 African nations at the China-Africa defence forum, with an aim of expanding its influence among the defence brass. While this is a more formal arrangement, ties with senior military figures in Africa have kept China ahead of the geopolitical curve and manage any fallout of leadership transitions in volatile African nations. For example, the chief of Zimbabwe’s armed forces, General Constantino Chiwenga, was in China and met senior leaders three days before Robert Mugabe, one of Africa’s longest serving leaders was deposed in 2017, sparking speculation as to whether or not Beijing was in the know about the coup. The PRC has been very effective at co-opting, especially senior defence personnel in the developing world. Militaries form the backbone of several developing countries and nominally civilian leaders do require their support. Consequently, the Chinese industry has readily available defence export markets.

Any industry needs a market to bring in revenues and a testing ground to improvise its product. As China’s arms industry thrives, its dynamics with Africa will be interesting. Both have a great deal to offer each other. A resource-starved China eyes Africa to power its economy, whereas African nations that thrive on the extractive-industry economy, but deprive its citizenry of public services will increasingly look to acquiring instruments of hard power to bolster their regime.

The views expressed above belong to the author(s). ORF research and analyses now available on Telegram! Click here to access our curated content — blogs, longforms and interviews.

Kartik is a Senior Fellow with the Strategic Studies Programme. He is currently working on issues related to land warfare and armies, especially the India ...

Read More +

Kalpit A Mankikar is a Fellow with Strategic Studies programme and is based out of ORFs Delhi centre. His research focusses on China specifically looking ...

Read More +