Sri Lanka, which in the 1970s was being hailed as a development success story for a low-income nation, is now mired in a financial and economic disaster, its worst yet since independence in 1948. Despite notable investments in infrastructure projects, and a largely stable growth rate from 2013 to 2019, the Sri Lankan story was marred by a series of untimely and mismanaged economic measures that led to the current meltdown. External factors have compounded the catastrophe, including the COVID-19 pandemic and the Ukraine-Russia conflict. This paper analyses six crucial economic issues that have led to the Sri Lankan crisis: the impact of the 2019 tax cuts on the domestic economy; successive BOP crises; a series of IMF bailouts that went wrong; the sudden disastrous switch to organic farming; the downfall of the tourism sector following the 2019 Easter Sunday bombings; and soaring external debt.

Attribution:

Soumya Bhowmick, “Understanding the Economic Issues in Sri Lanka’s Current Debacle,” ORF Occasional Paper No. 357, June 2022, Observer Research Foundation.

Source Image: Understanding the Economic Issues in Sri Lanka’s Current Debacle

Introduction

The South Asian neighbourhood has been fraught with crises in recent years. Myanmar, for one, is battling a massive humanitarian crisis involving the exodus of minority Rohingyas, severe food insecurity, and soaring unemployment following the military coup in 2021. Meanwhile, Pakistan’s new government is seeking an International Monetary Fund (IMF) bailout of debts to the tune of US$ 6.4 billion[1]over the next three years, amidst an economic disaster in the country. The COVID-19 pandemic caused supply chain disruptions, compounding the economic challenges across the region. The Ukraine-Russia conflict have further worsened the situation, as Western sanctions on Russia have caused devastating economic fallouts.

This paper examines the crisis in Sri Lanka—one of the worst economic disasters in South Asia’s contemporary history. To be sure, the interconnectedness in the global economy does not allow for an isolated view of the national economic emergency in Sri Lanka, home to a population of some 22 million. Indeed, the supply chain disruptions following the pandemic and the Russia-Ukraine conflict have exacerbated the Sri Lankan crisis. In turn, Sri Lanka’s woes are bound to have repercussion across regions, trade regimes, and Global Value Chains (GVCs).

This paper discusses six key economic challenges that have created a proverbial perfect storm for Sri Lanka: the state of the domestic economy; Balance of Payments (BOP) crises; successive IMF loans; the unwarranted agricultural reforms contributing to FOREX scarcity and soaring inflation; the downfall of the tourism sector; and the country’s historical fetishism for sovereign debts.

Domestic Economy and Tax Cuts

Sri Lanka is facing its worst economic crisis yet since the country’s independence from British colonial rule in 1948, and new dynamics continue to unfold in the island nation every day. In May 2022, Prime Minister Mahinda Rajapaksa resigned his post, paving the way for the appointment of the new PM, Ranil Wickremesinghe—this is only the most recent[2]of key developments in Sri Lanka’s politics and economy in recent years.

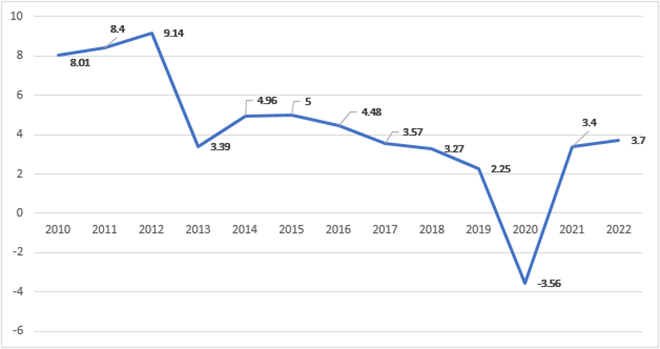

The 26-year-long civil war that ended in 2009 had a massive impact on the fundamentals of Sri Lanka’s domestic economy. The global financial crisis of 2008 drained the country’s forex reserves, and economic mismanagement by a succession of governments caused the twin challenges of budget shortfall and Balance of Payments (BOP) deficits. The country’s soaring external debts, coupled with the increase in government spending to enact COVID-19 relief measures, have further weakened the domestic economy structurally. The country’s GDP growth rate had plummeted from 8.01 percent in 2010 to (–) 3.56 percent in 2020 when the pandemic hit. (See Figure 1)

Figure 1: Sri Lanka’s Real GDP Growth Rate (2010-2020)

Source:World Bank, 2022 Projection by Central Bank of Sri Lanka[3]

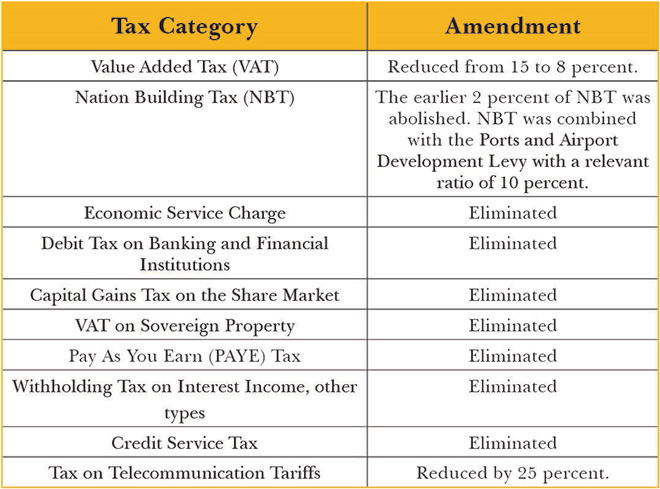

Towards the end of 2019, and in early 2020 before the pandemic, the government enacted deep tax cuts in fulfilment of an election promise. This led to the loss of approximately one million taxpayers between 2020 and 2022—[4] a massive challenge for an economy that was already suffering from widespread tax evasion. Table 1 lists the direct and indirect taxes that were amended by the Sri Lankan government.

Table 1: Taxes Abolished in Sri Lanka in 2019-2020

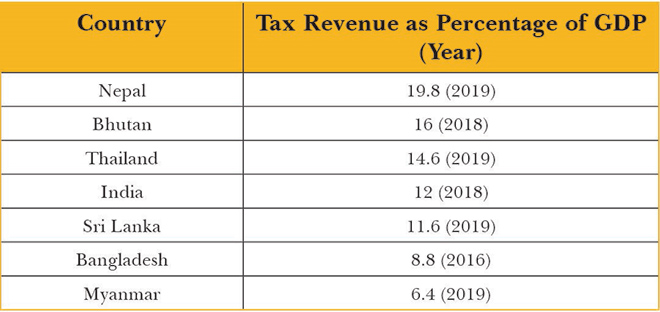

Prior to these tax cuts, Sri Lanka already had one of the lowest tax revenue-to-GDP ratios in the region; these cuts created further burden on the exchequer. The ratio dropped to a disastrous 7.7 percent[6] in 2021 after the unplanned tax cuts in 2019 and 2020. (See Table 2)

Mainstream economic theory suggests that such tax cuts could enhance disposable incomes and money circulation in the economy, in turn spurring economic growth in the medium to long term. For Sri Lanka, however, the consequences have been dire. Given the weak base of the island nation’s economy, coupled with a steep rise in pandemic-induced expenses on various welfare measures, further frictions on resource mobilisation had widened the budgetary deficit and increased the external debts for the Lankan economy. The budget deficits rose significantly from 9.6 percent of GDP in 2019, to 11.1 percent and 12.2 percent of GDP in 2020 and 2021, respectively. The government’s total debt-to-GDP ratio had also escalated from 86.9 percent in 2019 to 100.6 percent in 2020, and 105.6 percent in 2021.[8]

In 2020 and 2021, the economy had net repayments to foreign creditors and therefore the entire budget deficit was financed by domestic sources such as the Central Bank of Sri Lanka.[9]The significant amount of monetary financing by the Central Bank worsened the inflation and exchange rate. As the situation has critically aggravated, there is need for fiscal consolidation through revenue enhancement as well as expenditure rationalisation. Recognising the unsustainability of the tax cuts, the government is looking at hiking the tax rates again to attract revenue. To this effect, a few key announcements made by the Government on 31 May 2022—including increasing VAT from 8 percent to 12 percent effective immediately (expected to add approximately US$ 180 million in revenues); and raising corporate income tax from 24 percent to 30 percent from October 2022 (expected to add approximately US$ 145 million in revenues).[10]Moreover, the withholding tax on employment income has been made mandatory and exemptions on individual tax payments have also been reduced.

Yet, what is essential is for the government to complement its revenue enhancement policies with adequate expenditure rationalisation measures required for boosting economic growth and creating employment opportunities. In parallel, it is crucial to expand the immediate social protection measures for the poor sections of the society who are most impacted by the pandemic. Any macroeconomic restructuring, however, must be guided by the basic tenets of inclusive progress given that the economic impact of the pandemic has been skewed against women and the poor.[11]Finally, given the public distrust that has led to civil unrest, as well as the historical patterns in huge tax evasion in the country,[12]the government must make the tax collection systems more robust to increase revenues in the medium to longer term.

Balance of Payment Deficit

Sri Lanka is experiencing a classic case of the ‘twin deficits’ hypothesis: that an economy’s current account moves in the same direction as its fiscal account. Establishing the link between the two, we have:[13]CA = (𝑆p−𝐼 ) + (𝑇 − 𝐺 );[a]where CA is the current account balance, Sp is the total private savings, I is the private investment expenditure, T is the Government tax revenue and G is the Government spending (including transfers), and hence the total Government savings Sg = (𝑇 − 𝐺 ) denotes the fiscal account balance. The twin deficits are characterised by consumption-driven economies that are associated with high levels of domestic and international debt, which is true in the case of Sri Lanka. In this case, the excess demand in the domestic economy increases imports and drives inflation, in turn making domestic commodities less competitive in global export markets.

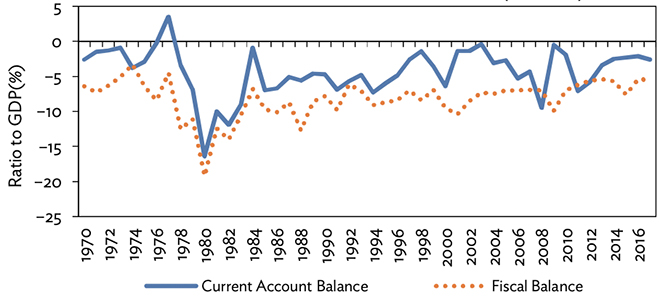

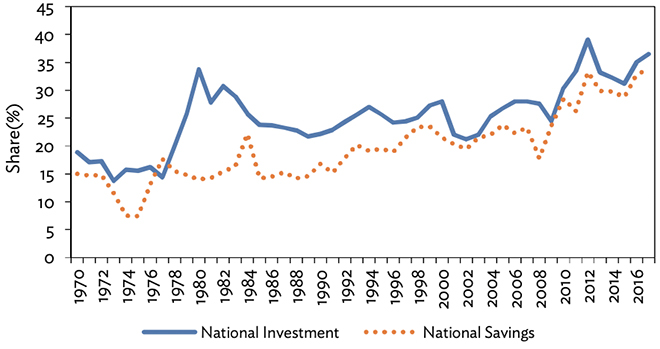

For Sri Lanka, the twin deficits on the current and fiscal accounts have moved together consistently since 1970 (with an exception in 1977 when current account surplus had occurred), while the correlation between the two had weakened after 2000 (see Figure 2). The economy’s national savings have been consistently lower than its national investment, but the gap has reduced over the years after a peak difference of 19.8 percent of GDP in 1980, when the country had undertaken large-scale public investment schemes (see Figure 3).[14]

Figure 2: Trends in Sri Lanka’s Current Account Balance and Fiscal Balance (1970-2016)

Source:Asian Development Bank, Data from Central Bank of Sri Lanka[15]

Figure 3: Trends in Sri Lanka’s National Investment and National Savings (1970-2016)

Source:Asian Development Bank, Data from Central Bank of Sri Lanka[16]

The twin deficits phenomenon increased Sri Lanka’s reliance on foreign debt, leaving the economy more susceptible to exogenous shocks like the COVID-19 pandemic. During the pandemic period, Sri Lanka’s Government spending (G) had increased in tandem with the expenditures that were being undertaken in economies across the world, while the tax cuts right before the pandemic had driven down the tax revenues (T) by large proportions – enhancing the fiscal deficits, and the corresponding current account deficits substantially.

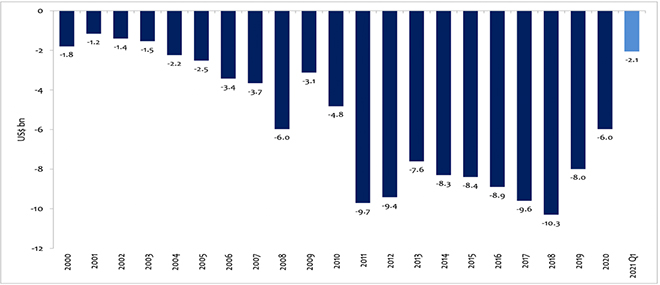

Indeed, Sri Lanka’s Balance of Trade (BOT)[b]has been registering a consistent deficit, with an approximately increasing trend in deficits over the years (see Figure 4). Between December 2021 and March 2022, Sri Lanka’s trade deficit decreased from US$ (-)1085 to US$ (-)762, denoting a drastic reduction in imports due to FOREX exhaustion and indicating the onset of the crisis situation in the economy.[17]

Figure 4: Sri Lanka’s Balance of Trade (2000-2021)

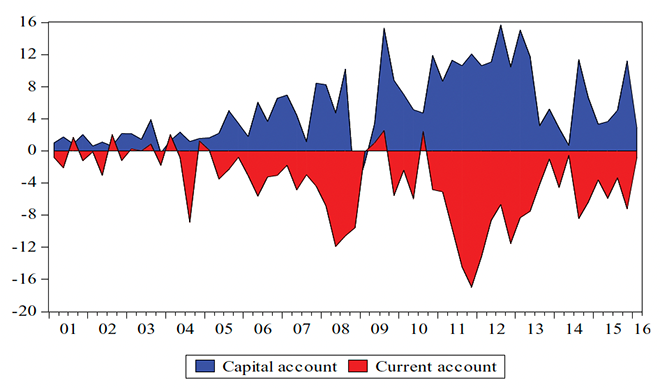

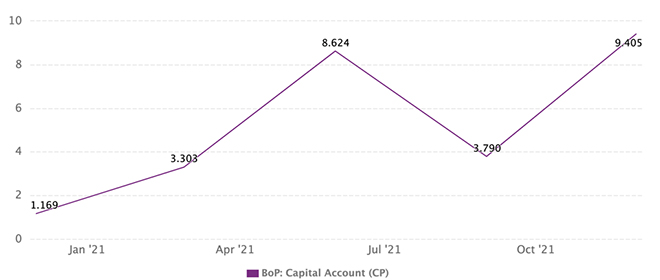

On the other hand, Sri Lanka’s capital account is not impacted by its current account or exchange rates; but the reverse may not be true. Econometric analysis shows that the interest rates have a positive impact on the capital account.[19]Theoretically, capital account can have a negative impact on the current account in two ways: First, a boost in capital surpluses increases investment and releases liquidity which tends to raise consumption demand, thus leading to current account deficits via increased imports.[20]Second, capital inflows lead to the appreciation of the domestic currency, making imports cheaper and exports more expensive, relatively. Therefore, the surge in imports and fall in exports cause the current account deficits to widen.[21]

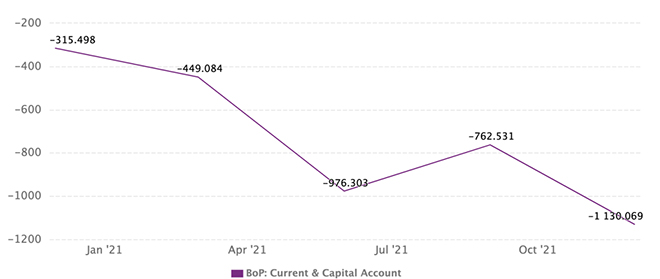

Historically, Sri Lanka’s capital account and current account balances have moved in opposite directions: the former has been in surplus while the latter is characterised by prolonged deficits. To be sure, there have been a few exceptions, such as during the 2008-09 financial crisis, when Sri Lanka’s capital account balance had plummeted disastrously (see Figure 5). This divergence is typical of consumption-driven developing economies that are hotspots for incoming capital investments, which provide the FOREX to finance the imports in order to satiate domestic demand.

Figure 5: Historical Trends in Sri Lanka’s Current and Capital Account Balances (in US$ million)

Figure 6: Sri Lanka’s Recent Current Account Balance Trends (in US$ million)

Source: CEIC, Data from Central Bank of Sri Lanka[23]

Figure 7: Sri Lanka’s Recent Capital Account Balance Trends (in US$ million)

Source:CEIC, Data from Central Bank of Sri Lanka[24]

Figure 8: Sri Lanka’s Recent Balance of Payments (BOP) Trends (in US$ million)

Source:CEIC, Data from Central Bank of Sri Lanka[25]

The relatively slower capital account, combined with the strongly deteriorating current account, have led to a massive BOP crisis in Sri Lanka in recent times, and the country is finding it extremely difficult to pay for its essential commodities.

The Overseas Development Institute (ODI) charts out a few important lessons in this context:[26]reducing the delay in seeking IMF assistance and bailouts; strengthening crisis management capabilities; creating safety nets for political instability and poverty mitigation; investing in a macroeconomic regulatory structure to reduce the economic costs of the crisis; and avoiding the spread of misinformation by conducting better public communication.[c]

IMF Bailouts

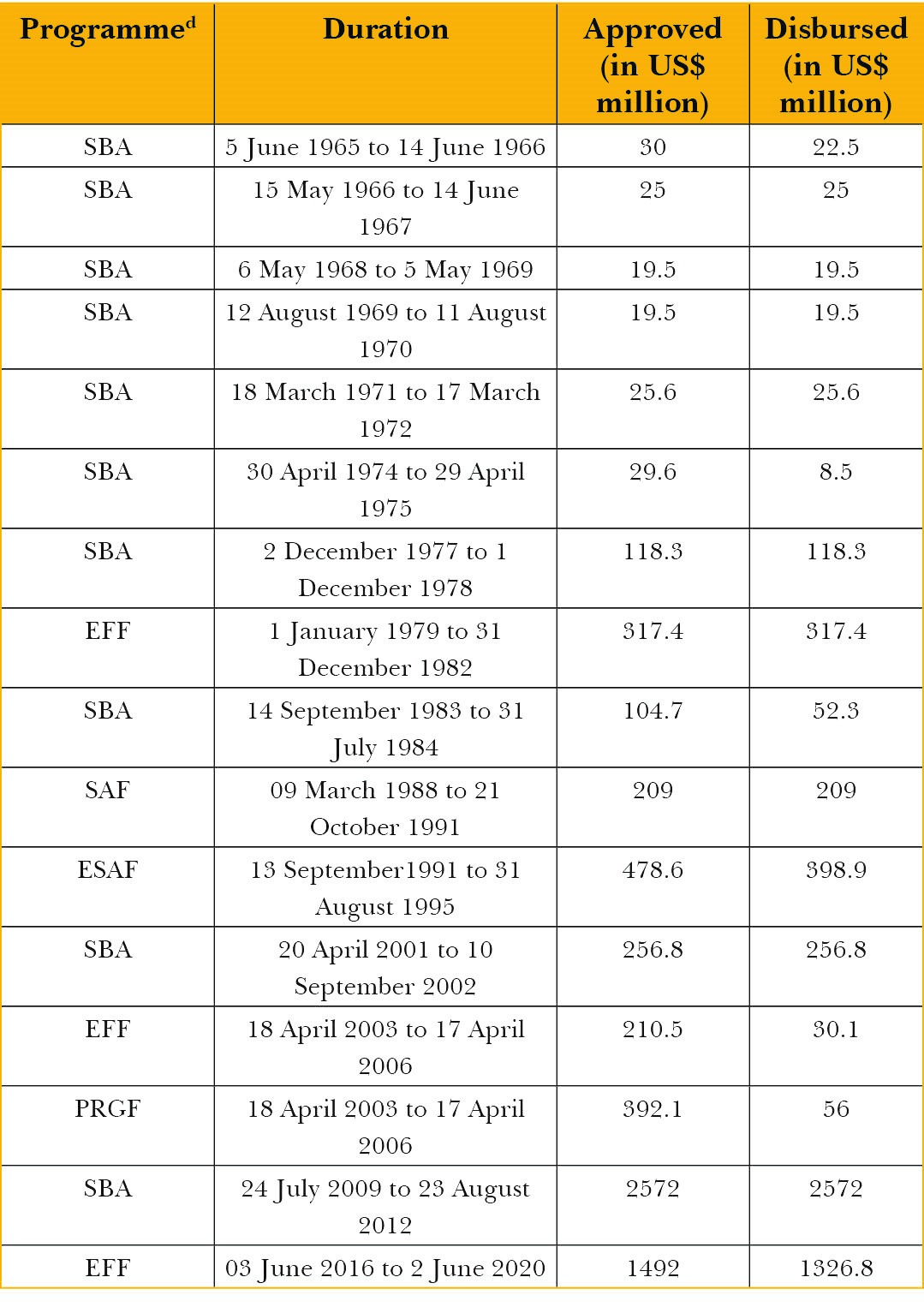

The last two decades have seen a series of BOP crises in Sri Lanka, and the country has sought a number of bailouts from the International Monetary Fund (IMF). In 2009, IMF extended a loan with the condition that budget deficits will be reduced to 5 percent of GDP by 2011. With no improvement in growth or export, the country requested the IMF in 2016 for another round of debt amounting to US $1.5 billion with some new clauses. The IMF package caused repercussions to the economy’s health,[27] and growth rate fell from 5 percent in 2015 to 2.9 percent in 2019. During the same period, government revenue also contracted from 14.1 percent to 12.6 percent of GDP.

IMF loans come with a set of conditions that are often restrictive for the debtor nations. Sri Lanka, despite its severe BOP crisis, did not immediately seek assistance from the IMF given its previous track record of faltering economic recovery. Eventually, however, sheer desperation drove Sri Lanka to IMF once again.[28](See Table 3)

Table 3: Sri Lanka’s IMF Structural Adjustment Programmes (1965-2020)

Source:Compiled from Jayalath (1990), CBSL (1998, 2001, 2002, 2009), and IMF[29]

Sri Lanka could find little option but to seek IMF support, which entails conditionalities related to budgetary cuts and trade openness, amongst others. As anti-government protests grew across the Sri Lanka in 2022, the IMF had requested cash-strapped Sri Lanka to “restructure” its massive foreign debt before a rescue deal could be finalised.[30] Today, as Sri Lanka considers its options between IMF conditionalities and a deepening debt pool to China, it is time to negotiate how the government’s engagement in the short-run can be conducive to inclusive and sustainable growth in the longer term.

Agricultural Reforms, FOREX Crunch, and Inflation

After the 2019 presidential election, the new president, Gotabaya Rajapaksa, outlined a 10-year vision for transition into complete organic farming in Sri Lanka. However, in April 2021, the Sri Lankan government decided to completely ban the import of agrochemicals to mitigate the health impacts of chemical fertilisers and pesticides in farming, and also to promote eco-friendly sustainable agricultural systems. This was also a measure to keep a check on Sri Lanka’s rapidly depleting foreign exchange reserves from various imports at that point.[31]

The ill-advised and sudden switch to organic farming could be considered the final nail in the coffin for Sri Lanka’s economy. It provides lessons in agricultural policy, especially for countries of the Global South.

Although the transition towards organic farming seemed like an environmentally sustainable step, the sudden shift was like a time bomb waiting to explode. As the new methods of production were more costly with lower yields, this agricultural policy—unprecedented in Sri Lankan history—led to serious impacts on the country’s economy.[32]Rice production quickly fell by 20 percent, leaving nearly 33 percent of agricultural land unused and increasing rice prices by 50 percent in only seven months. This disrupted the economy’s self-sufficiency in rice production, and the country has since had to import rice from countries such as Myanmar and China[33] to derail an impending food crisis.

The country has now resorted to importing not only rice, but also sugar and various other commodities, using the country’s FOREX reserves and thus worsening the foreign exchange situation in the economy. The tea industry—which was once a major commodity of exchange—incurred losses of some US$ 425 million.[34] Between June 2021 and April 2022, Sri Lanka’s FOREX reserves were drastically reduced from US$ 4.06 billion to US$ 1.92 billion. (See Figure 9)

Figure 9: Trends in Sri Lanka’s Dwindling FOREX Reserves (in US$ million)

Source:CEIC, Data from Central Bank of Sri Lanka[35]

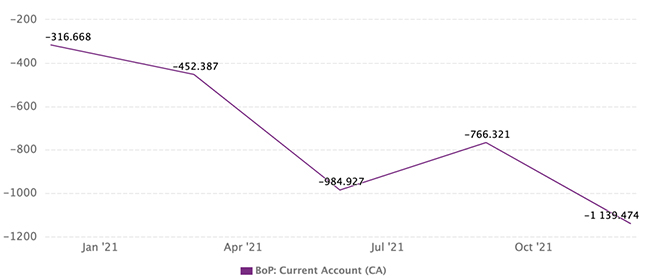

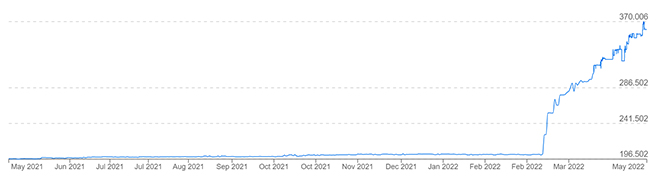

The country’s export profits (agricultural) fell by 2.1 percent in February 2022 compared to February 2021, mainly owing to a drop in export earnings from tea, spices, and unmanufactured tobacco.[36]The surging imports of wheat, sugar, and milk powder and other essential items from foreign countries increased the demand for FOREX. The various factors contributing to the demand pressure on FOREX reserves led to massive currency depreciation in the Lankan economy. With the Sri Lankan currency falling by 7.3 percent in 2021, import costs skyrocketed, increasing inflation and raising concerns about panic purchasing and hoarding. To prevent market irregularities, the government declared frequent curfews and sent armed troops to distribute food at reduced costs. As a result, the nation’s external economic performance deteriorated, and its current account deficit increased to US$ 1.14 billion in January 2022 from US$ 0.136 billion in January 2021.[37]The purchasing power of the Lankan currency plummeted, and it became one of the worst-performing currencies (see Figure 10). The Sri Lankan Rupee (LKR) – US$ exchange rate reached an all-time high of US$ 1 = LKR 371.26 on May 13, 2022.

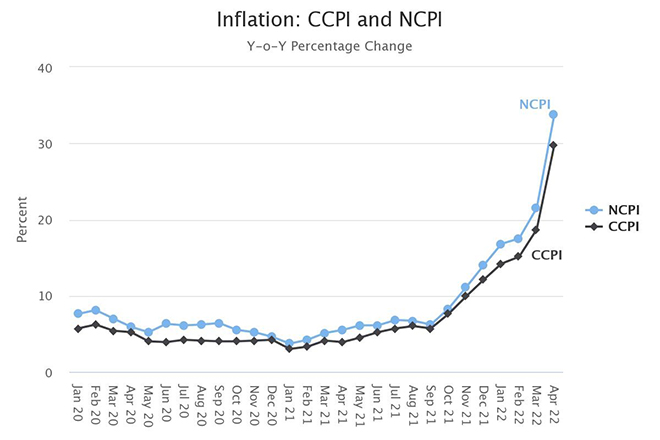

The crisis in the island nation hit the headlines more prominently when the prices of necessities such as food grains started rising sharply, petrol and other fuel became scarce, causing long power cuts across the country. The soaring inflation in Sri Lanka can be explained by the interplay of supply and demand factors. With wrecked agricultural processes on the domestic front and increasing costs of production, the country started depending on imports for basic necessities—therefore, the supply of these commodities became constrained, in turn leading to a cost-push inflation. Meanwhile, the earlier tax cuts in 2019 and 2020 had increased disposable incomes, leading to demand-pull inflationary pressures as well. The year-on-year headline inflation on the Colombo Consumer Price Index (CCPI) and National Consumer Price Index (NCPI) reached a disastrous 29.8 percent and 33.8 percent, respectively, in April 2022.

Additionally, Sri Lanka has printed its domestic currency to the tune of LKR 588 billion only in the first quarter of 2022 (includes reserve sales to repay loans), after LKR 1225.20 billion and LKR 505.90 billion printed in 2021 and 2020, respectively.[40]The country had started to actively print money since the end of the devastating civil war in 2009, to mitigate the BOP crises it would often run into in the last decade. It was mainly after 2015 that money was printed particularly to provide a stimulus targeting an output gap, and boost growth in the economy. However, the steady currency printing over the years made it extremely difficult to control inflation or bring stability to the exchange rates.

Indeed, the Sri Lankan agricultural crisis provides two important lessons in the domain of developmental policies that countries across the world are attempting to undertake. First, the contemporary sustainable development agenda has its flaws in implementation, where one aspect of development often induces a negative externality to another. The framework may not be the problem, but the implementations often leads to unfavourable spill overs. It presents some inherent challenges that not only make it difficult to operationalise directed policy action, but also the comprehension of their outcomes. For instance, in terms of the UN Sustainable Development Goal (SDG) framework, there is no doubt that knee-jerk policies on organic farming will help advance the targets of SDG 13 (Climate Action), but will put a huge burden on achieving SDG 8 (Decent Work and Economic Growth)—as evident from the Sri Lankan case. The adoption of organic farming in Sri Lanka was not inherently flawed. Rather, the lack of a nuanced understanding of the interplay between several factors that would go against a complete ban of traditional farming was problematic.

Second, Sri Lanka is a classic case of how a one-size-fits-all approach toward sustainable development is detrimental to inclusive progress. Not all policies can be absorbed at the same pace for developing nations in comparison to the Global North. This is mainly because of the resource gap in the foundations of the economy. For example, when organic farming was introduced to Sri Lanka, the sudden transition was extremely problematic due to the lack of farming infrastructure, dependence on imported agrochemicals, lack of access to modern techniques, and agricultural illiteracy. The transition would undoubtedly be easier (if not seamless) in an advanced economy in comparison to Sri Lanka.

In November 2021, the ban was lifted following the backlash from the industry due to reduced productivity, soaring inflation, and therefore continuous protests to abandon the policy. Despite this step, the country experienced a sharp increase in prices for all commodities, as farmers were unable to access imported fertiliser due to dwindling forex reserves. Against this background, Sri Lanka’s closest neighbour, India, delivered 100 tons of nano nitrogen liquid fertiliser to Sri Lanka immediately after.[41]However, as is now evident, lifting this ban did not help save the island nation from the mess it had already run into.

Downfall of Tourism

Sri Lanka’s tourism sector accounts for 12 percent of the country’s GDP and is the fifth largest source of foreign currency in the economy.[42]The industry has been severely damaged by the island nation’s deepening economic crisis, out-of-control gasoline costs, and power outages. In 2018, tourism brought in US$ 4.4 billion and contributed 5.6 percent of GDP, but this was reduced to just 0.8 percent in 2020, amidst the pandemic.[43]The severe impact of the tourism sector on the GDP is the cumulative effect of a number of crises faced by the economy in a consecutive manner.

The Easter Sunday bombings in April 2019 was a series of coordinated terrorist suicide bombings in Colombo, leading to a casualty count of 250 people. It had an initial dire impact on tourism: many establishments stayed closed for days following the incident, and tourists fled as the number of visitors fell by more than 70 percent in May and over 60 percent in June compared to the same months a year earlier.[44]The COVID-19 pandemic also resulted in a 50 -percent revenue loss in 2020, and a consequent drop in tourist numbers.[45]

Figure 12: Sri Lanka’s Tourist Numbers in 2019 and 2020

These events were further compounded by the impact of the Sri Lankan economic crisis coupled with a severe shortage of FOREX. Tourists would undoubtedly assist the disaster-hit country with its foreign exchange problems, but the repercussions of the crisis, along with the violence and imposition of emergency rule, are jeopardising a sector that is a critical component of a viable economic solution. Long queues of motorcycle taxis congested at service stations, waiting for scarce gasoline, are making it difficult to get across the country due to the fuel shortages. Moreover, the Sri Lankan government’s ban on social media sites such as Twitter and Facebook on 3 April 2020[47]has made tourists anxious about the country’s future.

The government of President Gotabaya Rajapaksa has maintained that a boost in tourism and exports will assist Sri Lanka in refilling its foreign currency reserves and potentially navigate the crisis. Adding to the woes of the country is the Russia-Ukraine war which crippled the country’s tourism sector further. Russia and Ukraine, the top and third-largest tourist markets this year, respectively, have played a critical role in this plan. Russia is also Sri Lanka’s second-largest market for tea, the country’s principal export.

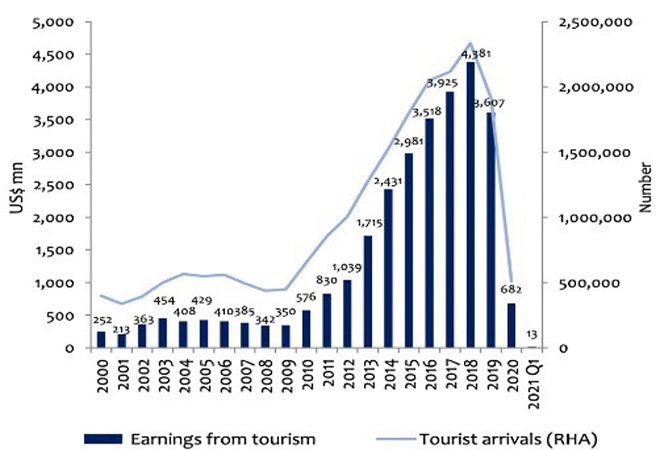

Almost 20,000 Russians and Ukrainians visited Sri Lanka in January 2022, accounting for more than a quarter of all visitors; while they accounted for fewer than 10 percent of the tourist population in January 2018.[48]Russia, Ukraine, Poland, and Belarus accounted for almost 30 percent of tourists in 2022,[49]and the conflict also threatens to cut off that flow. Official records reveal that Sri Lanka generated US$ 3.6 billion in tourism in 2019 before the crisis dropped it to less than one-fifth, a short two years later. The cumulative impact of these crises is reflected in the earnings from tourism, as illustrated in Figure 13.

The tourism sector is also responsible for the direct and indirect employment of Sri Lankans—estimated to the tune of 403,000 people in 2019.[51] The decline of the tourism sector due to a number of interrelated and combined factors will have a dire impact on the status of the Sri Lankan economy as it stands today. After all, the sector holds a key position in the economic revival of the country, by attracting FOREX and boosting growth in the longer horizon.

External Debt and the China Factor

Sri Lanka’s past decade was characterised by seemingly robust economic moves in terms of multiple infrastructure projects as well as a booming tourism industry, among others. This led to a large inflow of funds in the capital market from creditor nations and organisations in the form of International Sovereign Bonds (ISB)—[52]instruments of capital market borrowings with high interest rates and shorter durations of repayment and no grace period. Indeed, considering principal payments at the bond maturity date, as ISBs mature the debt repayment requirements increase resulting in the outflow of foreign currency, thereby increasing the BOP precarities. Currently, these ISBs account for close to 50 percent of the country’s external debt.[53]

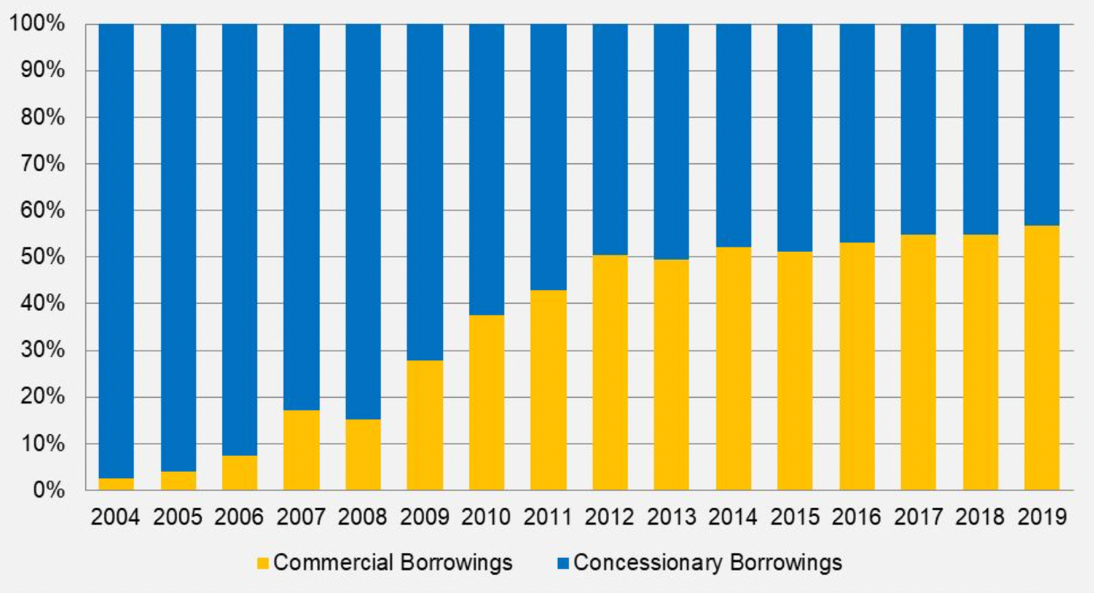

Before Sri Lanka’s graduation to a middle-income country in early 2000s, most of its foreign debt came in the form of concessionary funding from multilateral organisations such as the World Bank, Asian Development Bank, and Japan International Cooperation Agency. It got favourable loan conditions as a low-income nation—i.e., low interest rates (1 percent or less) and longer repayment periods aided FOREX management to not lead into a BOP crisis.[54] However, as access to concessionary loans declined, the economy shifted to a new structure of foreign debt composition (see Figure 14), with an increasing proportion of commercial loans, mostly in the form of ISBs. Although Sri Lanka’s foreign debt-to-GDP ratio has reduced dramatically over the last two decades, the change in the total structure of the external debts has made the economy more vulnerable to currency crises in the last few years.

Figure 14: Sri Lanka’s Foreign Debt Composition (2004 – 2019)

Source:The Diplomat, data from the Central Bank of Sri Lanka and the Department of External Resources, Sri Lanka[55]

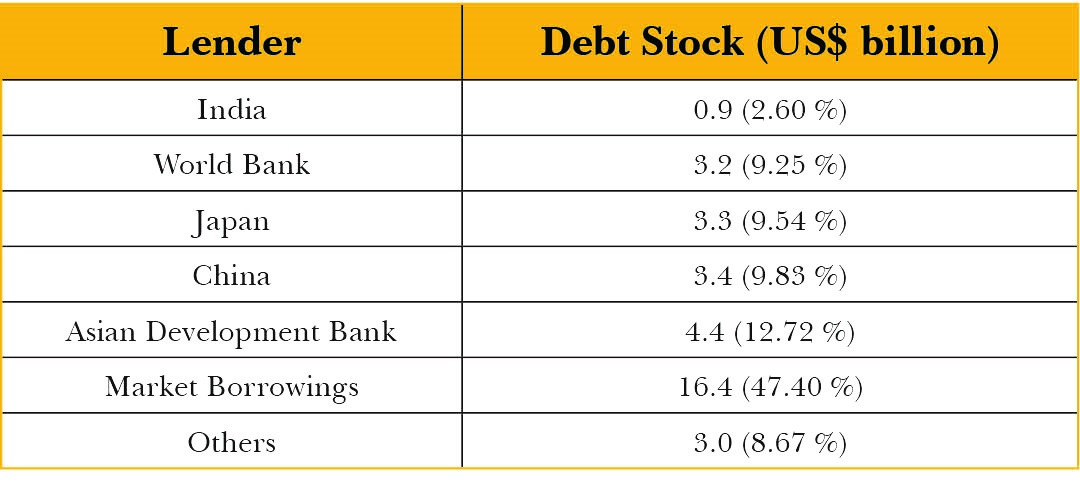

While the domestic public debt levels have remained mostly stable—primarily driving growth in the Lankan economy—the foreign debt-to-GDP ratio (comprising mostly commercial borrowings) has surged from 30 percent in 2014 to 42.6 percent in 2019.[56]The country’s excessive foreign borrowing for low-return infrastructure projects, as well as rising external debt service, hammered an already weak economy that was reeling from the economic costs of a 30-year civil war that ended in 2009, followed by the repercussions of global financial crisis in 2007-08, and persistent fiscal and current account deficits. Table 4 summarises the foreign debt stock in Sri Lanka till the year 2019, which has only worsened since the 2022 economic collapse.

Table 4: Sri Lanka Foreign Debt Stock (2019)

Source:Foreign Debt Summary,Department of External Resources, Sri Lanka[57]

Sri Lanka has external debt service payments of US$ 7 billion for the rest of 2022 against foreign reserves of US$1.9 billion at the end of March 2022.[58]On 12 April, the country declared that it was defaulting on its external debts to the tune of US$ 51 billion, pending an IMF bailout; the announcement immediately led to a crash in the market prices for these ISBs issued by the country. According to the Finance Ministry, about US$ 3 million worth of external assistance will be required over the next six months to restore supplies of essential goods and catalyse the recovery path for the economy.[59]

Against this background, it becomes particularly important for the regional economies to maintain a fine balance between their overall external debt and their debt to China (the developing world’s largest creditor nation), especially for the Belt and Road Initiative (BRI) countries such as Sri Lanka. For Sri Lanka, the Hambantota port reflects unrealistic projects built on foreign loans that created highways, airports and convention halls. Despite an expert panel’s rejection of the concept, it was erected near the hometown of then-President Mahinda Rajapaksa and paid for with US$1.1 billion in Chinese financing.[60]Due to the port’s failure to produce cash, Beijing bailed it out in 2017 by purchasing a 99-year lease for US$1.1 billion from a state-owned corporation, China Merchants Group.

Many global analysts concur that Sri Lanka has fallen victim to China’s ‘debt-trap diplomacy’. Although China does not account for the highest percentage of Sri Lanka’s outstanding external debt, China’s liquidation techniques and hidden debts in various projects also reflect the problematic outcomes of Beijing’s economic imperialism. According to the Advocata Institute, a Colombo-based think tank, the amounts owing to Chinese creditors were US$ 119 million to the China Development Bank Corporation, US$ 232 million to the China Development Bank, and US$ 232 million to the Export-Import Bank of China, as of 2022.[61]The ongoing economic crisis in Sri Lanka had caused Colombo to request for a moratorium on debt repayments to the visiting Chinese Foreign Minister in February 2022—stirring up the issue of “problematic Chinese debts” once again in the global economic arena. The island nation also sought a new loan of approximately US$ 2.5 billion in March 2022.[62]

Meanwhile, in the last couple of years, Sri Lanka and India have been able to substantially strengthen their economic ties and remain amongst the largest trade partners for each other within the ambit of the South Asian Association for Regional Cooperation (SAARC). Some highlights of India’s financial package to Sri Lanka include: US$ 400 million worth of SAARC currency swap; deferral of Asian Clearing Union Settlement of US$ 515.2 million by two months; and US$ 500 million for fuel procurement in Sri Lanka.[63]In a ground-breaking move, New Delhi also extended a Line of Credit worth US$ 1 billion to Colombo to aid the procurement of food, medicines, and other essential commodities in March 2022.[64]This was followed by another humanitarian aid consignment from India worth approximately US$ 2 billion in May 2022 – comprising mainly of rice, milk powder, and pharmaceutical supplies.[65]

Unfortunately, but quite expectedly, there is no lack of competitive undertones to the aid provided by India versus China, all at the cost of the Sri Lankan crisis. There are actual concerns regarding Beijing’s pressure on Colombo for a Free Trade Agreement (FTA) during such trying times.[66]Former PM of Sri Lanka Ranil Wickremesinghe agreed that India has extended “maximum” support to Sri Lanka and added, “we will have to see the outcome of the support of India while New Delhi is still helping in non-financial ways.”[67]

There is no doubt that Sri Lanka’s foreign debt concerns have contributed to the country’s present economic woes. First, the nation’s reliance on commercial borrowings without addressing the structural weaknesses in the economy such as decrease trade as a percent of GDP (from 33 percent in 2000 to 13 percent in 2019), low FDI levels (successive governments were unable to meet the FDI targets) and plummeting tax revenues, among others—have impacted the economy, due to the complicated interactions of domestic and external macroeconomic factors.[68]Second, the Chinese fund flow into Sri Lanka needs a closer look before the country makes any more payback promises that will be difficult to keep in the coming years. In fact, credit diversification and foreign debt restructuring will be of utmost importance for Sri Lanka.

Going ahead, one question needs careful attention: Given the current debacle in the Sri Lankan economy, the impact of the pandemic on the global economy, and most importantly the country’s low sovereign credit ratings, it will be extremely difficult for the country to seek commercial borrowings from foreign sources in the near future, which has often been the rescue path for Sri Lanka in its previous BOP crises.

Conclusion

On 10 June 2022, the United Nations (UN) had warned that the extreme economic situation in Sri Lanka could develop into a “full-blown humanitarian emergency”. The UN and its partners are seeking a funding of US$ 47 million to urgently cater to the needs of 1.7 million of the most vulnerable population in the country.[69]Sri Lanka’s success stories on a few fronts in the last decade, including its triumph in the COVID-19 vaccine rollout in 2021, have been overshadowed by several policy missteps aggravated by external factors leading to an unprecedented economic catastrophe.

It is important to analyse the complex interplay of these domestic and international economic factors not only to help chart a steady recovery process for Sri Lanka, but also to establish relevant red flags for developing countries as they plan for their post-pandemic economic readjustments. This paper outlines some unambiguous arguments from the Sri Lankan case that needs careful examination to provide macroeconomic lessons for the South Asian neighbourhood.

Economics over politics.Sri Lanka’s comprehensive tax cuts in 2019 were part of the election announcements, with little consideration for the massive fiscal deficits that the nation could run into. In fact, the budgetary deficits had led to unnecessary pressure on the Central Bank, causing a deterioration of the exchange rate situation as well as inflationary tendencies. It devastated the domestic resources that were required to create a buffer for impactful macroeconomic shocks such as the COVID-19 pandemic and the Ukraine-Russia conflict.

Minding the (BOP) gap.Consumption-driven emerging economies like Sri Lanka have an inherent tendency to attract foreign capital with the promise of higher profits. These tendencies increase disposable incomes and enhance the affinity towards imported goods. However, when the trade structure starts featuring necessary commodities in the import basket, it is a clear signal that the country is going beyond its means—this has devastated the current account balance in Sri Lanka, leading to the BOP crisis.

Employing pragmatism with the IMF.IMF bailouts have historically been the most unfavourable option for any economy. The conditionalities are often difficult to keep up with and could have a host of negative impacts on the domestic economy. This was true for Sri Lanka in the last decade. However, it is equally important to consider the pace and severity of an economic crisis and the potential consequences. Therefore, Sri Lanka’s early reluctance to seek any IMF package had arguably made things worse and reduced its options to avert the current meltdown.

One size does not fit all.Recent developmental policies in Sri Lanka such as the shift to organic farming needed a more calibrated approach. The choices have tended to be myopic, and have not only disrupted the country’s resilience in some agricultural commodities such as rice and tea, but have also had ripple effects on other macroeconomic parameters. The low productivity and excess demand in the agricultural sector had had to be satiated with imports of necessary food items, in the absence of sustainable FOREX reserves. This has led to a host of interlinked economic issues ranging from soaring inflation to currency depreciation.

Protecting the Most Valuable Players. The 2019 Easter Sunday bombings that killed almost 250 people had immediately devastated the consistently good performance of Sri Lanka’s tourism sector. However, the Sri Lankan government has not been able to undertake any concerted efforts towards reviving the industry that has historically contributed substantially to GDP growth and attracted foreign currency into the economy. The double-whammy of the COVID-19 pandemic and the Ukraine-Russia conflict amidst the economic crisis makes it extremely challenging to revive this sector.

Do not borrow to the hilt.Sri Lanka’s habitual borrowing from creditor nations and multilateral organisations took a precarious turn when the composition of its foreign debt structure started shifting towards commercial borrowings in the form of ISBs, rather than the concessionary borrowing patterns it had prior to its graduation to a middle-income country. This was compounded by the Chinese pressures of ‘debt-trap diplomacy’ that completely engulfed Sri Lanka under the garb of the once-glorious BRI.

The impact of exogenous shocks on regional economies, such as the South Asian nations, has been brutal. To be sure, the pandemic has provided a strong stimulus for economic resilience. However, the lack of resources, coupled with skewed policies driven by domestic and global politics, have often led to economic crises, especially in the Global South.

The current wave of economic and political crises in the South Asian neighbourhood has three crucial implications. First, there must be a minimum level of insulation among countries in times of crises that will prevent an economic collapse of the entire region. Second, structural changes on the domestic front must enable economies to sustain short-run emergencies and supply chain disruptions without falling apart. And third and most important, resilient and timely policies should absolve countries of extreme external dependence by increasing the efficacy of their domestic production and consumption processes.

Endnotes

[a]To decipher the relationship between the fiscal and current account deficits, we start with the standard national income accounting identity. For an open economy, gross national product (Y) is written as:

(1) Y = C+I+G+(X−M) +R

Where C is the private consumption expenditure, I is the private investment expenditure, G is the government expenditure (including transfers), X is the total exports, M is the total imports, and R is the net factor income from abroad and net transfers. The current account balance (CA) is:

(2) C A = 𝑋 −𝑀 +R

National savings (𝑆) in an open economy is:

(3) 𝑆 = Y−C−G

Combining equations (1) and (3), we get the national savings as:

(4) 𝑆 = I+C A

Again, total national savings (S) are a sum of private savings (𝑆p) and Government savings (𝑆g):

(5) 𝑆 = 𝑆p + 𝑆 g

𝑆p is the part of individuals’ disposable income (Y adjusted for taxes, T) that is not consumed, that is:

(6) 𝑆p = 𝑌 −𝑇 −𝐶

𝑆g, is the difference between the government’s receipts (taxes) and the government’s expenditures on goods and services, written as:

(7) 𝑆g = 𝑇 − G

Substituting, (6) and (7) in equation (4), we get:

(8) 𝑆 = 𝑆p + 𝑆 g = 𝑌 −𝑇 −𝐶 +(𝑇 −𝐺) = 𝐼 +𝐶 A

Or:

(9) 𝑆p+(𝑇 −𝐺) = 𝐼 +𝐶 A

Finally, equation (9) can be further simplified as:

(10) C A = (𝑆p−𝐼) +(𝑇 −𝐺)

Where CA is the current account balance that is denoted by the sum of the private sector savings balance (difference between private savings, 𝑆p and investment, I), and the fiscal balance (difference between government revenue from taxes, T and government expenditure on goods and services and transfers, G).

[b]This comprises of visible trade in the current account (difference between visible exports and imports)

[c]A large number of proxy accounts and Facebook pages with political messaging is rampant in Sri Lanka amidst the current crisis.

[19]Biswajit Maitra, “Dynamics of capital account and current account in Sri Lanka,”Journal of International Trade and Economic Development27, no. 1 (June 2017): 54-73.

The views expressed above belong to the author(s). ORF research and analyses now available on Telegram! Click here to access our curated content — blogs, longforms and interviews.

Soumya Bhowmick is an Associate Fellow at the Centre for New Economic Diplomacy at the Observer Research Foundation. His research focuses on sustainable development and ...

PDF Download

PDF Download