Introduction

Harsh V Pant

There is a sense of déjà vu as a new variant of the novel coronavirus has once again pushed nations, big and small, to impose lockdowns and socio-economic restrictions on their populations. It comes at a time when a palpable sense of hope was emerging—that perhaps the global economy could revive, and the health threat of the pandemic has waned. The COVID-19 pandemic, however, continues to cast its long shadow on the world two years since the first reports of a “strange” respiratory disease came out of China. The global health crisis has led to a global wealth crisis, with far-reaching consequences for geopolitics and international affairs.

As 2021 comes to an end, we look back at a year whose devastating impacts continue to be felt in large parts of the world. We now know that we cannot simply wish COVID-19 away, and we will have to live with it for longer; it is the contours of such co-existence that are far from clear.

Global politics continue to be volatile; indeed, the geopolitical trends are solidifying with an alacrity that was only in the realm of speculation when the COVID-19 crisis began. The rise of China has forced countries across the world to re-assess their stakes, in turn ushering in a phase of tumultuous adjustments. Great-power contestations are rising and the US-China faultline is widening by the day. It did not take long for the world to see that Donald Trump was not really an exception; Joe Biden’s presidency has so far largely taken off from where Trump left, albeit with minor changes. This struggle for supremacy between the extant pre-eminent power and its foremost challenger is putting pressures on the global order in unprecedented ways. International institutions are withering under the weight of the rivalry; the normative shift underway is a distinct break from the post-1945 liberal consensus; and new kinds of balancing and bandwagoning among the states are visible.

Amid the churning, the Indo-Pacific region has become the centre of gravity of global geo-strategy. It is a pattern that is reflected in the global powers trying to reclaim their own space in this vast maritime geography. It is also underlined by the emergence of a multitude of variable geometries in the region that fill the void left by an absent institutional architecture. Coalitions of the willing are taking the place of formal alliances, with names like QUAD and AUKUS reverberating across the region this past year.

Across the world, democracies are facing challenges and states are leaning in on autocracy as a more efficient model of political governance. To be sure, the democratic world has been facing difficulties even prior to 2021. Economic stasis, ineffectual leadership, and political fragmentation have all contributed to the heightening sense of discontent with the state of world’s democracies. Technological shifts have ushered in a new era of social dislocation and disinformation campaigns where the open landscape of democracies has been exploited by the authoritarian world in their battle of narratives.

This ‘state of the world’ report outlines the key trends that have shaped the global landscape in the year 2021. We asked our researchers to delineate three meta trends in their respective domains; the analyses are showing interesting convergences.

The first section on major powers underscores how the rise of China is driving the foreign policy postures of these big states, even as the role of the Indo-Pacific region is becoming more salient. The state of flux among these large players is also quite evident as Europe’s ties with Russia, and Russia’s own attempts to balance multiple partners, become the defining features of the emerging global order.

The second section on key geographies highlights the impacts of structural changes in the international system. The US-China contestation is putting pressure on all parts of the world even as the American withdrawal from Afghanistan in 2021 and the country’s fall to the Taliban has unleashed new forces which regions such as South Asia and Central Asia are only beginning to come to terms with. The weakening of regional institutions is also making this framework of governance less effective.

The final section examines the challenges faced by the multilateral order in the past year. While global trade is still struggling to recover from the shock of the pandemic, the UNSC is fast becoming the major-power theatre once again. Climate change was a big part of global conversations throughout the year but for all the verbiage, the results on climate finance on mitigation and adaptation were underwhelming. Global technology governance saw some nascent steps towards norms-building, but the struggle of democratic nations against “digital authoritarianism” gained greater traction. Global health challenges show no sign of abating but national health systems across the world seem to be more cognisant of the linkages between a resilient health system and economic growth. Perhaps this will usher in a more hopeful global trend.

As 2022 commences, the overarching trends outlined in this report will continue to shape our external environment. It is our aim that the analyses presented here will generate more debate and lead to a more productive policy conversation – not only to understand the world around us but also to navigate it effectively by being more forward-looking.

I. Major Powers

The U.S.: Biden’s Goals and Strategic Compulsions

Vivek Mishra

The political metamorphosis implicit in the American presidential transition from Donald Trump to Joe Biden carried the promise of a changed US landscape in 2021. The presidential elections, and Biden’s oath-taking in January, seemed at the time to have set the tone for a markedly different presidential approach to foreign and domestic policies of the US. In many ways, numerous executive orders issued by Biden on his first day in office were intended to do that: rejoining global climate commitments through the Paris Agreement; keeping the US’s relations with the World Health Organization (WHO) intact; and revoking a ban on travellers from Muslim-majority countries. Despite such conscious attempts to underscore a policy rebalancing, the Biden administration has since been constrained by its own political and strategic compulsions that require a mix of continuity and change. The three trends that reflect some of these policy continuities and changes are the following: US policies vis-à-vis the Indo-Pacific; withdrawal from Afghanistan; and an assortment of steps by the US to defend its position as the global leader of the world, especially in the backdrop of a fast expanding China.

Indo-Pacific Policy

In geostrategic estimations, the Biden administration’s operational focus has continued to remain in the Indo-Pacific. This is because the region has become the fastest growing in the world, accounting for two-thirds of all economic growth; in parallel, China’s strides in the region seek to upset the existing balance of power. For Biden, the best way to manage the China challenge is through a resilient partnership-based approach in the region. A speech on 13 December by Secretary of State Antony Blinken straddles both these concerns by laying out priorities of the US in the region. These include: free, open, and rules-based domains across land, open seas, and cyberspace; strengthening partnerships to seek a favourable balance of power; investments to create alternative infrastructure in the region; reassuring allies and partners through aligning visions; and combining capacities and securing the Indo-Pacific through an “integrated deterrence” strategy in the region.

Fundamentally, the US’s Indo-Pacific strategy has structurally sought a dispersion of strategic concentration in power, earlier concentrated in the Pacific theatre. This shift is likely to strengthen in the future.

Afghanistan Crisis

Despite the continuity from his predecessors, the US withdrawal from Afghanistan in August this year made Biden the president who proverbially belled the cat. The decision to withdraw underscored two important long-term changes for the US: It married the erstwhile ‘pivot to Asia’ to the US’s Indo-Pacific strategy, reassuring allies and ushering America’s full focus to the current era of renewed competitiveness with China; and it has allowed Washington to re-engage some regional countries around Afghanistan, including in West and Central Asia, from a different prism. The Biden administration’s effort to resuscitate the Joint Comprehensive Plan of Action (JCPOA or Iran nuclear deal), its extended support to improving regional relations under the Abraham Accords, and its recalibrations vis-à-vis Central Asian states are attempts to keep a necessary toehold in the region.

Defending the ‘Global Leader’ position

The year 2021 has been marked by readjustments for American foreign policy, especially in accommodating changes in both internal and external balancing, primarily driven by China which is closing gaps with the US across sectors such as technology, infrastructure, and international aid. The new great-power game between China and the US has acquired a technology-intensive character with increasingly decisive roles for artificial intelligence (AI), Big Data, and other critical technologies, impacting how the two compete in sectors such as cyber, outer space, and even conventional defence. Advancements in these areas can act as force multipliers, catapulting one player significantly ahead of the other in relatively less time. The hypersonic test by China in November has forced the US to acknowledge China’s superior abilities in this domain.

If 2021 has shown anything, it is that in the forthcoming decade the US will likely exert efforts to defend its global leader position. This will require resource diversification in desired areas as well as the ability to quickly readjust. This strategy is likely to cut across the use of technologies, building alliances and partnerships, and creating alternative models of growth, development and governance to those of its competitors.

Finally, an important component of this defensive strategy will be to target its biggest competitor, China, on areas that will help political consolidation of support from the rest of the world. These domains include democracy, climate change, pandemic response, and rule of law.

China: Party, Power, and Pursuit of Prosperity

Kalpit A Mankikar and Antara Ghosal Singh

Despite the continued disruption from the COVID-19 pandemic, the year 2021 has been an eventful year for China: the economy experienced ebbs and flows, the country engaged in an impressive vaccine outreach programme, and also undertook wolf-warrior diplomacy. The following paragraphs look back to the past year, and outline the key highlights of Chinese diplomacy.

Asserting the China model’s superiority

The COVID-19 pandemic has exposed America’s Achilles heel. A presumed robust healthcare system notwithstanding, the country fared poorly, recording massive numbers of cases and deaths in 2020. And as 2021 began, a violent insurrection in Capitol Hill aimed at thwarting the transition to the new president, was seen in China as the ‘Huning thesis’ fructifying. The CCP’s political theorist Wang Huning had long predicted the superpower’s decline due to domestic strife. China seized the opportunity to popularise the narrative that while the US touted itself as the champion of democracy as a universal value, its own foundations were on unstable ground. China saw opportunity in the turmoil in the world’s greatest democracy to counter the ideological threat it poses to the CCP, and raised the slogan of “West declining and East rising” (read as China’s ascendance) due to the CCP’s superior system of governance.

Extending the CCP’s reach beyond the mainland thus became Xi Jinping’s pet project. At a time when President Joe Biden had taken the onus upon himself to host the Summit for Democracy in early December, the CCP also appears to be geared up to propagate the norms of its Party-state governance prototype across various parts of the world. In Zimbabwe, for example, the ruling party, ZANU-PF, has openly professed that it sought to learn from the CCP’s political system and imbibe its ideological orientation for the nation’s civil service.

The CCP’s confidence in its own political model is creating repercussions, particularly in the form of more high-handed policies. For instance, China modified Hong Kong’s electoral system to control the kind of public representatives who can gain office in the special administrative region (SAR). At the same time, the CCP seems to have given up on the prospect of peaceful reconciliation with Taiwan, in favour of a more muscular approach. In its November Plenum, the CCP announced, in the context of Taiwan, that its military is prepared to protect national sovereignty. This follows the record number of intrusions into Taiwanese airspace by Chinese warplanes around China’s National Day on 1 October 2021, as a warning that the CCP could deploy force to integrate Taiwan in the future.

Xi as Mao 2.0

In 2021, Xi’s tenacity brought him rich dividends. The Sixth Plenary Session or Plenum of the 19th Central Committee of the CCP, which concluded on 11 November 2021, saw Xi featuring in a “historical resolution”, and getting elevated to the league of Communist stalwarts Mao Zedong and Deng Xiaoping. There have been three historical resolutions since the CCP’s founding in 1921, and each served the purpose of showcasing unity in the ranks and unrivalled stature of its leader. While the CCP leadership met to deliberate over the Party’s achievements over the last 100 years, a big portion of the meeting’s resolution lionised Xi’s “successes” since his ascent to power barely a decade ago. According to the CCP, Xi’s achievements include pushing for balanced economic growth, upgrading the nation’s economic model to achieve high-quality growth, reducing disparity, attaining self-reliance in the face of US sanctions, modernising China’s defences, and reducing graft and pollution. Externally, it believes that the nation’s soft power and diplomatic heft have improved under him. China’s National Congress, which endorses leadership changes within the CCP, meets in 2022. China’s leaders usually enjoy two five-year terms in office, but indications are that the glorification of Xi will mean he may get an unprecedented third shot at power.

Pursuit of Common Prosperity

After Xi highlighted the concept of common prosperity as “an important feature of Chinese-style modernisation” at the Central Finance and Economic Affairs Work Conference on 17 August 2021, the term “common prosperity” has become fashionable in Chinese policy circles. The idea, which is believed to have its roots in the Mao era, prioritises issues like reasonably adjusting excessive income; promoting philanthropy; achieving an “olive shaped distribution structure”, and reducing regional disparities and the rural-urban divide. Xi’s push for common prosperity, which is being used alternately for both domestic and international contexts, has not only garnered global attention but has also fuelled intense domestic debates.

The campaign, characterised by an unprecedented crackdown on China’s top corporate firms in various sectors including technology, real estate, and online education, has alarmed foreign investors and stoked concern among sections within Chinese society. There have been reports of Chinese business leaders like Alibaba’s Jack Ma, Evergrande Group’s Xu Jiayin, and Tencent CEO Pony Ma vying to pledge multi-billion-dollar charitable funds to court favour with the government. Leading Chinese economists have warned that the campaign could become yet another “Great Leap Forward”—this time, to common poverty.

Meanwhile, China’s state media has been presenting a counter-narrative, arguing that Xi’s common prosperity is neither prosperity of a few people; nor is it uniform egalitarianism. It emphasises that this is neither some kind of leftist revisionism, nor is Chinese economy changing course altogether. That this is merely an effort towards course correction. The objective of the policy is not just reducing China’s growing wealth gap between rich and poor but also correcting the various manifestations of socio-economic malaise. The policies, which they say are all good for the people, include: tightening regulations on tech platforms; regulating fintech companies; controlling real estate space; and enacting pioneering regulations assuring data privacy, protecting gig workers, clamping down after-school tutoring, restricting gaming time for children, and restricting “celebrity” and “fan club” culture.

To conclude, the broad trends that marked the course of Chinese diplomacy this year can be summarised as – China’s intensified assertions of the superiority of its governance model over democracy, further centralisation of power within the CCP, that is President Xi further tightening his grip over China and Xi’s renewed thrust on pursuit of common prosperity, both domestically and internationally. All these trends are expected to be “long-term”, and therefore will define the contours of Chinese diplomacy in the years to come.

(The authors would like to acknowledge the research assistance provided by Aditya Pandey, Research Intern at ORF Mumbai.)

Russia: Rising Authoritarianism, Declining Ties with the West

Saaransh Mishra and Nivedita Kapoor

The year 2021 was a crucial one for Russia, both at the domestic and international level. The trends that had been visible in the past years intensified, giving a glimpse of Russia's trajectory in the coming years. These include a strengthening of the authoritarian political system at the domestic level, continued decline in relations with the West, and an increased focus towards the East.

Authoritarian domestic political system

The year began with the arrest of opposition leader Alexey Navalny, in what is seen as a politically motivated case, eventually leading to his organisation Anti-Corruption Foundation being classified as an “extremist group”. Several cases have since been filed against its members, who cannot contest elections for at least three to five years.

Allegations of election-rigging in the September Duma elections were also rampant. Indeed, the United Russia’s victory ahead of the 2024 presidential elections was particularly important for Kremlin as it sought to maintain a majority for the party of power to ensure a favourable legislature.

The list of organisations under the ‘foreign agent law’ continues to expand, and it now includes individual journalists, media organisations, NGOs, and lawyers who are critical of the government. Such designation hampers these organisations’ ability to carry out their activities, including raising funds. The law purportedly mandates organisations to be designated as such if they receive financial assistance from abroad and use those resources to engage in political activity.

For the first time, too, the revised 2021 National Security Strategy mentions “unfriendly countries”, accusing them of “instigating and radicalising” protest movements and using “indirect methods” to provoke instability. This label refers to the US and some of its allies, revealing a continued stalemate for future Russia-West ties.

Deteriorating Ties with the West

The fraught nature of relations is visible in the continuing stand-off on the Ukrainian border, and it remains unclear how Russia's proposal of security guarantees would be met by the US and NATO. This reveals fundamental divergences over the building of a European security architecture, Moscow’s reiteration of its red-lines in the post-Soviet space, and the long-standing issue of NATO expansion continues to be a crucial stumbling block. Since 2014, these issues have been exacerbated by allegations of Russian meddling in US presidential elections, imposition of unilateral sanctions, and accusations of cyber-attacks.

Notwithstanding the diplomatic engagement at various levels following the US-Russia Geneva Summit in June, and the latest virtual summit in December, the relations remain tense. It is unclear how the situation on the Ukraine border will de-escalate. Yet again, the NSS document reveals the Russian position, where the points of cooperation with the EU and the US mentioned in previous years are missing—this shows continued dissatisfaction within these relationships.

Instead, the focus is on CIS, Greater Eurasian Partnership, China, India, and related multilateral institutions of SCO, BRICS, and RIC. Along with its own policy goals, events in Eurasia also led Moscow to increase its focus towards the East in 2021.

Looking towards the East

The Taliban’s takeover of Afghanistan triggered apprehensions over the ripple effects of drug-trafficking, refugees, and terrorism on the regional countries. Russia is intensifying efforts to deal with the volatile situation.

The current situation provides Russia the opportunity to utilise its diplomatic influence, which could further help it consolidate its standing as a global power, especially in Eurasia. This would also advance Russia's stated ambition of improving its engagement with the East, as stated in President Vladimir Putin’s first ever address to the foreign ministry board as well as the NSS 2021.

This focus on the east, and in particular the Asia-Pacific, was also reflected in the bilateral Indo-Russia summit which put to rest speculations of a drift in India-Russia ties. New Delhi is a key player in its pivot to the East, prompting Russia to advise de-escalation of tensions to India and China. Meanwhile, the S-400 deal, the establishment of a 2+2 mechanism, inclusion of Russia as member of the Indian Ocean Rim Association (IORA), all point to a strengthening of the bilateral equation that has spanned many decades, and which in recent years was perceived to have been a casualty of changing global dynamics.

Current developments have reinforced the ideals of pragmatism that India and Russia share, as well as their commitment to building a multipolar world.

If relations with the West continue to deteriorate, the East will further gain significance for Russian foreign policy, with China as its key external partner. However, Russia’s need to balance China will keep Moscow interested in improving ties with Europe. Driven by the same compulsions, Russia will seek to strengthen its ties with India. It remains to be seen whether India can leverage this to its advantage.

The EU: Through the Looking Glass

Rahul Kamath

As 2021 began, the European Union (EU) was busy demonstrating its resilience while confronting geopolitical issues on various fronts. The EU witnessed multiple events that altered governance in the region, including Chancellor Angela Merkel’s resignation from German and European politics; the EU’s launch of its Indo-Pacific Strategy; the EU-UK trade and cooperation agreement; the Polish court ruling primacy of national laws over supranational laws; and the Ukraine-Russia conflict. Of these, however, three key events weighed more than the rest: the Afghanistan crisis; the fourth wave of the COVID-19 pandemic; and the energy crisis across the continent.

European Strategic Autonomy

The question of the EU trying to follow an independent strategy was always a subject of debate especially after former US President Donald Trump threatened to weaken the influence of NATO from the European borders. However, the Taliban’s takeover of Afghanistan in August, which prompted unilateral action from the US of withdrawing its troops without consulting its transatlantic neighbours, posed a question on European decision-making. Europe for long periods had depended on the US and NATO for safeguarding its territory. However, the Afghanistan crisis served as a watershed that created the possibility of establishing a European Strategic Autonomy.

The Afghan situation serves as another wakeup call for Brussels to invest in its strategic and security capabilities to act independently of Washington’s decisions. Indeed, Europe’s reliance on the US is likely to wane as leaders aim to invest in, and build their own security. The EU is working on a European Strategic Compass, a document that lists the union’s defining ambitions for security and defence for the next decade. The document, which aims to operationalise the EU’s strategic autonomy and allow Brussels to tackle Europe’s security responsibilities directly, is likely to be adopted in the first half of 2022.

COVID-19 and Anti-Lockdown Protests

Europe is once again at the epicentre of the COVID-19 pandemic and scientists are warning that the new strain, Omicron, could be the dominant variant in Europe by early 2022. The EU has witnessed an increase in cases with both the delta and omicron variants accounting for a record number of infections. Germany had recorded 52,970 daily cases in November, which was met with stricter curbs such as allowing access to public places only to those who are vaccinated or those recovered from the virus.

Other European countries such as Austria and the Netherlands have recorded high infection rates leading to lockdowns and debates regarding vaccine mandates, in turn triggering widespread protests across Europe. Over 40,000 unvaccinated Austrians marched through the streets of Vienna to protest the vaccine mandate and lockdowns after Austria became the first country in Western Europe to make the COVID-19 vaccine mandatory. Similarly, thousands marched in Belgium, the Netherlands, Croatia, and Italy as anger grew over new curbs such as requiring “Covid passes” to visit public places. Italians opposed the “Green Pass” certificates required at workplaces and public venues.

The European leaders remain divided over Omicron and a cohesive plan of action is needed to avoid further economic and social consequences. The EU in 2021 began its economic and social recovery from earlier COVID-19 waves but the spike in infection levels towards the end of the year poses a grave challenge for Brussels as they look to avoid the horrors of 2020 in 2022.

Energy Crisis

Europe saw an unexpected surge in natural gas prices which caused grave concerns over possible blackouts and frigid home temperatures during the winter season. As Europe and other countries bounced back from COVID-19’s economic fallout, the demand for natural gas and electricity grew with greater vigour than expected. The energy crisis is worsened in the winters as the demand for natural gas and electricity grows, leading to record-high prices. Due to shortages in natural gas, the crisis is expected to cause power outages. Europe’s heavy dependence on natural gas and its imports has led to a severe energy crisis as natural gas is often perceived as an alternative to other hydrocarbons. The EU has blamed Russia for causing natural gas shortages, but Russia has diverted such accusations by claiming that Moscow has decreased its supply to meet its domestic demands during the winter.

Moreover, the ongoing standoff between Russia and Ukraine is set to cause a further rift between Brussels and Moscow which could only intensify Europe’s energy crisis. Additionally, in the wake of the migration crisis caused by Belarus, President Alexander Lukashenko has threatened the EU by deliberating on shutting down the Yamal-Europe Pipeline carrying Russian gas to the EU. Any unilateral action by Lukashenko could worsen the energy crisis across Europe especially at the onset of the winter season and the fourth wave of the pandemic.

Indeed, public faith in renewable energy has declined as fuel and electricity prices have risen significantly. However, nuclear energy is once again at the forefront in European energy affairs despite opposition from other EU members. Nonetheless, the ongoing energy crisis of 2021 will spill over into 2022, thereby requiring the EU leaders to enlist a more robust and pragmatic energy security policy to power its economy amid other geopolitical challenges.

II. Key Geographies

The Indo-Pacific: A New Geopolitical Fulcrum

Premesha Saha and Pratnashree Basu

Many observers agree that the Indo-Pacific region will shape the trajectory of global politics for most of the 21st century. The region accounted for 60 percent of the world economy and two-thirds of all economic growth over the past five years. It is home to more than half the world’s people and many of the largest economies. In the past few years, the Indo-Pacific has gained more salience primarily due to the expansion of China’s footprint in the region, and with it, heightened uncertainty and ambiguity regarding Beijing’s ambitions. At the same time, others argue that China’s rise has occurred precisely owing to the changing geopolitical landscape of the Indo-Pacific: regional economies are growing and harbouring greater ambitions, natural and human capital is improving, and the shipping routes are becoming more productive.

The following trends emerged in the Indo-Pacific in 2021.

Expansion of issue-based cooperation

Bypassing the complexities and often unwieldy nature of multilateral forums of cooperation, minilateral platforms have mushroomed in the Indo-Pacific signaling an inclination towards smaller groups of partnerships among countries with a shared outlook. These partnerships are characterised by targeted and tangible areas of cooperation.

The Indo-Pacific has seen a rise in the number of these partnerships, among them: the Quadrilateral dialogue (or the Quad of India, the US, Australia, and Japan); the India-Australia-Japan trilateral; India-Indonesia-Australia trilateral; and AUKUS (of Australia, the UK, and the US, formed in September). The aim of these groupings is primarily to ensure the maintenance of a free, open, and rules-based order in the Indo-Pacific. So far, they are proving to be effective in bringing together countries with shared interests to work on issues and crises impacting the Indo-Pacific region. The Quad, for instance, has led the way in intra-regional vaccine diplomacy.

Greater involvement of extra-regional powers

The fate of the Indo-Pacific is linked almost inextricably with countries which are also geographically distant from the immediate region. Thus it is natural for individual countries within Europe—such as the UK and the European Union (EU), as an institution—to seek a more active role in the region. In September 2021, the EU published its first Strategy for Cooperation in the Indo-Pacific outlining the nature and scope of its envisioned involvement with countries in the region. The document was issued in the wake of the Indo-Pacific strategies published earlier by France, Germany, and the Netherlands. The rise in participation of extra-regional powers in the Indo-Pacific underscores the primacy that is being accorded to the region in global affairs. In turn, such engagements heighten intra-regional complexities.

Enduring US-China rivalry

For decades, the United States military hegemony, economic supremacy, and leadership in alliances governed the international order. This blueprint has come under strain in recent years, with China’s economic rise and its so-called “strategic revisionism”. Although the challenge to the US’s supremacy was already visible in the aftermath of the 2008 global financial crisis, the COVID-19 pandemic has underlined the patterns. Most countries of the Indo-Pacific started realigning their policies to effectively respond to the US-China competition. Some, like Australia, have chosen to bandwagon with the US, as seen in its recent policy measures that include calling for an investigation into the origins of the COVID-19 virus, and entering the AUKUS agreement.

Meanwhile, countries like India, Japan, Vietnam, the Philippines have also called out China for its aggressive actions in the South China Sea, East China Sea, and the 2020 Galwan clash, among others, while attempting a balance in its relations with both the US and China. It cannot be denied, however, that these countries are taking stronger positions vis-à-vis China in recent years. For their part, other Southeast Asian and East Asian countries such as Indonesia, Malaysia, Thailand, Singapore, and South Korea, continue to adopt a “hedging” strategy and avoiding any express declaration of which side they are taking.

These three patterns will also shape much of the course of policymaking and developments in the Indo-Pacific region in the coming years. The Indo-Pacific is where the interests of most of the regional and extra-regional players will map out, as it becomes the geo-political fulcrum around which countries will orient their foreign, defence, security, and economic policies.

West Asia: Shifts in the Status Quo

Kabir Taneja

Developments in the Middle East (West Asia) are difficult to anticipate. This is true whether in its fragile geopolitics led by its even more tenuous intra-regional ideological discrepancies, or in how its oil-rich kingdoms shape local and global economics, and how an already volatile geography will deal with a US-China rivalry that threatens to cause tectonic realignments comparable to those that followed the Second World War.

The Middle East has been a traditional sphere of influence for the West. However, changes in global power structures, specifically in new areas of great-power competition such as geoeconomics and geotechnology, have pushed middle powers at the forefront of hedging their interests. These countries are being courted by the likes of Washington D.C., the presumed hegemon, and Beijing, the threat—both looking to build their own spheres of influence using said middle powers as hedging tools.

Indeed, it might not be an overstatement to venture that Middle East powers were more active in the 2020-2021 period than they ever were. This was seen in the UAE’s interventions in conflict zones such as Libya and Yemen, and Turkey’s support for Qatar during the Gulf crisis between 2017 and 2021, and for Azerbaijan during the Nagorno-Karabakh war in 2020. Much of the trends for the region in 2021, including those related to US-China rivalry, revolved around certain critical outcomes that took place over the past 24 months. Three developments stood out: the signing of the Abraham Accords; fundamental shifts in economic policy by the likes of Saudi Arabia; and lingering, unanswered questions around Iran.

The Abraham Accords

The Abraham Accords, signed between a consortium of Arab states led by the UAE and Israel, was perhaps the watershed moment of 2020 around which crucial political outcomes in the region were ideated in 2021. The Accords pushed other states to also address the threats they are facing in the region, working on dialogue and diplomacy on the sidelines of conflict. The deal brought certain gains, as seen in the creation in October of what some observers are calling the ‘West Asian Quad’, of the UAE, Israel, the US, and India. This minilateral was made possible by the normalisation of Israel-UAE ties.

The arrangement was cemented during former US President Donald Trump’s tenure, and is thus seen as a key delivery on the foreign policy front in an otherwise chaotic Trump era. At the same time, another argument to be made is that Trump’s peculiar decision-making, his challenge to the US’s traditional allies, and exits from the Afghanistan war and the Iran nuclear deal, pushed countries such as the UAE and Israel to institutionalise years of back-door diplomacy. To be sure, some issues remain unresolved, such as the question of Palestine. Yet, there is a desire by regional powers to take onus for the region’s own security, matched only by a new global geoeconomics order.

Rethinking the economy

Saudi Arabia—the economic and ideological powerhouse of the Arab world—is attempting a historic move: to integrate itself into the global economic and business order instead of relying exclusively on the power it derives from its oil. The UAE has shown that it can be done, as Dubai became the financial engine of the region where global businesses found a palatable home in what was once a highly conservative Arab world. Riyadh, under heir-apparent Crown Prince Mohammed bin Salman, is attempting to walk the same path and change the economic trajectory of the kingdom. While such efforts are being welcomed by the global community, the path for the House of Saud looks precarious as it is met with the need to temper its vast constituency of conservative Islam, Salafist, and Wahhabi communities. This is critical to attracting foreign investment. A consistent shift in the Arab world towards “controlled liberalism” is a crucial experiment, the success of which can change the fortunes of Saudi Arabia; its failure could also have grave regional consequences.

The Iran Question

The multiple layers of crises around Iran continue to cause friction in the region. Attempts are underway to bring Tehran back into mainstream global economics and politics—from the return of talks around the nuclear deal, to foes like Saudi Arabia holding dialogue with Tehran to mitigate regional risks. However, an increasing Iran-Israel rivalry over the former’s nuclear program, and Tehran’s scaling up of militias in theatres such as Yemen and Syria as a negotiation tool, could yet spiral out of control. The Iran question needs an urgent, diplomacy-led solution to stave off the next potential conflict in a historically incendiary Middle East.

Africa: Fighting Global Inequities and Promoting Climate Action

Abhishek Mishra

Across the African continent, the year 2021 started on a positive note. On the first day of January, the African Continental Free Trade Area (AfCFTA) came into force. It would prove to be a false start, however, as trade under the agreement has not commenced owing to the lack of basic infrastructure and the inherent tensions between the free-market visions of the AfCFTA and the national economic development priorities of participating countries.

In the past year, the African landscape was shaped by three broad trends.

Democratic Recession and Spread of Authoritarianism

The downturn experienced by democratic systems across sub-Saharan Africa was accelerated in the past year, owing to several factors. Authoritarianism has gradually spread, and many states are today being run by ‘strongman’ rulers who seek to extend their terms in office either by changing constitutional term limits or manipulating election results. There were coup attempts in countries such as Sudan, Chad, Mali, and Guinea; and police and military repression of peaceful demonstrations. Opposition figures and government critics were arrested and put behind bars. Corruption is also worsening, especially in conflict-stricken countries such as Somalia and South Sudan, which in turn is hindering economic, political, and social development. Lastly, many leaders, most notably in Ethiopia, are using the COVID-19 crisis as a pretext for postponing elections and imposing new restrictions. The fall from grace this year of Ethiopian President Abiy Ahmed, a Nobel Peace Prize laureate, has been remarkable. Ethiopia’s military campaign in northern Tigray region, which started in November 2020, has set off a cascade of ethnic violence and humanitarian crisis that has engulfed the nation.

Climate Justice Activism

One positive trend that was notable in 2021 was the surge in a youth-driven wave of public discontent around current political and economic systems. African youths are becoming more aware of the role they could play in society in demanding just and more tolerant and democratic practices. In Sudan, youth-driven demonstrations and protests led to the fall of former President Omar al-Bashir; and in Nigeria, they forced the government to disband the controversial SARS unit.

This year, too, demand for climate justice was a regular feature among African leaders. At the COP26 in November, African leaders called on the international community to honour their commitments to the Paris climate agreement to provide US$100 billion annually to finance energy transitions in developing countries including those in Africa. The year also witnessed the rise of young African climate activists demanding action to combat climate change: Chido Nyaruwata of Zimbabwe, Adenike Oladosu (Nigeria), Kaluki Paul Mutuku (Kenya), and Ugandan activist Vanessa Nakate.

Debt Sustainability, Debt Servicing, and Debt-Trap Diplomacy

The COVID-19 pandemic exacerbated Africa’s debt problem, reduced fiscal space, and made debt servicing more difficult. This is worrying since the failure to meet debt servicing requirements may lead to downgrading by credit-rating agencies, domestic currency depreciation, and heighten pressure on foreign exchange reserves. A sense of anxiety over Chinese debt in several African countries has continued throughout the year, and reached fever pitch with the publication of an AidData report that revealed that African countries accumulated some US$40 billion in ‘hidden debt’ from 2000 to 2017, and that they owed China an estimated USD207 billion.

Sensationalist media reportage over the Chinese seizure of Uganda’s Entebbe International airport also caused an uproar on social media and lent its weight behind allegations of Chinese practice of debt-trap diplomacy in Africa. As suggested by the outcome of the eighth edition of FOCAC held in Senegal in November, the days of direct cash flows from Beijing and easy access to credit for African countries are numbered. China is now likely to explore more innovative models of financing and focus on ‘targeted’ investments in certain sectors.

In 2021, the politics around the pandemic laid bare the imbalances in the relationships between the African countries and the global North. The biggest trend has been the continuing frustration among African countries over the inequities in the global vaccine distribution efforts, as well as the recent round of travel bans against those coming from the continent—a policy which has been correctly dubbed as “travel apartheid”. The irony of such discriminatory mechanism, which stigmatises southern African countries despite contrary evidence of the variant first being identified in Europe—discourages sharing of information and global solidarity.

Central Asia: Deeper Faultlines Threaten Regional Integration

Ayjaz Wani

Central Asia is often called a “global chessboard” given the region’s importance as a pivot for geopolitical transformations. In 2021, the region was once again witness to a heightening of faultlines: violent clashes erupted on disputed borders, parliamentary and presidential elections were held in certain countries, and developments pointed to the need for regional integration and cooperation. In August, the fall of Kabul to the Taliban also reignited concerns of regional security and stability.

Border disputes, Regional integration, and Security cooperation

In April 2021, deadly clashes erupted on the Kyrgyzstan-Tajikistan border, one-third of which is disputed by the two. The encounter—the most violent in recent years—claimed the lives of 30 people, injured hundreds, and triggered the exodus of nearly 10,000; it also raised fears of a wider conflict. A timely negotiation between Kazakhstan and Uzbekistan agreed to aim for alliances and refocused the debate on regional integration. Subsequently, in August, leaders of Kyrgyzstan and Tajikistan met and participated in the Third Summit of Heads of State of Central Asia in Turkmenistan. Although issues of conflict prevention and resolution within the region were not mentioned, the summit succeeded in getting all the countries to discuss regional integration and security cooperation amidst the growing security crisis in Afghanistan. The Taliban have not only resurrected the spectre of rising extremism but also triggered concerns that intra-regional connectivity efforts will fail. The Taliban factor revealed the dependence of Central Asia on Russia and also showed divergence in dealing with the insurgent group. Tajikistan, Turkmenistan, and Uzbekistan felt the heat on the 2,387-kilometre-long porous border they shared with Afghanistan. Thousands of Afghan troops and civilians crossed the border, triggering increased vigil along those locations with the help of troops that Russia sent under the Collective Security Treaty Organisation (CSTO). Russia also sent equipment, and held military exercises with Uzbek and Tajik forces. Tajikistan criticised Taliban’s use of force to recapture Kabul and stressed the need for an inclusive Afghanistan government that will have representations from all ethnic groups especially the Tajiks. For their part, Uzbekistan and Turkmenistan hosted Taliban delegations to strengthen ties with the group and protect their geostrategic and geoeconomic interests. These two countries need cooperation from Taliban for South-Central Asian economic connectivity, trade, transit and export of natural resources.

Elections without opposition

Known for the authoritarian regimes in some of its countries, the region saw parliamentary elections in Kazakhstan and Turkmenistan this year, as well as presidential elections in Kyrgyzstan and Uzbekistan. The parliamentary elections held in Kyrgyzstan after the sweeping constitutional changes that weakened the parliament made people wary of elections. The election was marred by a record-low turnout of 34 percent, and was hobbled by technical glitches. In Uzbekistan, President Shavkat Mirziyoyev won his second term with 80.1 percent of votes. The independent candidates were not permitted to contest and the observers mission sent by the European Union alleged “significant procedural irregularities” on election day. Meanwhile, in Kazakhstan, the ruling party Nur Otan secured 71 percent of the votes. Even as Russia described the elections as “open and competitive”, it saw protests from opposition parties and Western countries criticised it.

Limits of Multilateralism

At the multilateral level, the Shanghai Cooperation Organisation (SCO) heads of state summit was held in Dushanbe in September 2021, in a hybrid format. The delegates discussed, among others, the confirmation of Iran as a full member and the ramifications of the return of the Taliban on member states and other countries. In the summit, Tajikistan called on the Taliban to declare a more inclusive government. Fearing a spillover of radicalism and extremism in the SCO region in the era of Taliban 2.0, the SCO members also stressed for an independent, neutral, united, democratic and peaceful Afghanistan that is free of terrorism, war, and illicit drugs.

In July 2021, Uzbekistan held a two-day Central-South Asia conference which saw 250 participants and 40 delegates from different countries including the US, Russia, Pakistan, India, and Japan. On the sidelines of the conference, the US held a C5+1 engagement to advance cooperation for infrastructure modernisation, energy sector improvement, increased connectivity and for upholding human rights, and strengthening the rule of law. The C5+1 grouping comprises the US and five Central Asian Countries.

The year 2022 will be crucial for Central Asia. Externally, the re-emergence of the Taliban poses geosecurity and geostrategic threats, and internally, the divergent approaches of the countries towards the insurgent group can only make things worse. With the US withdrawal from Afghanistan creating a security vacuum and increasing the country’s fragility, China and Russia will also try to increase their influence in the region.

South Asia: Standing at a Crossroads

Aditya Gowdara Shivamurthy

The year 2021 has been a crucial one for South Asia. Increasing competition in the Indo-Pacific region, the threat of extremism, and diminishing regionalism have shaped and influenced the region throughout the year.

A New Balance

In 2021, the world continued to witness multipolarity and increasing competition in the Indo-Pacific region. China remains invested in asserting itself in the region, and the second wave of the COVID-19 pandemic has only exacerbated South Asia’s dependence on Beijing. India, for its part, has maintained its status-quo position in the region. Indeed, it has made intense efforts to countering China with its connectivity projects and emergency and development assistance to countries of the region.

Other players such as the US and the EU have also started showing more interest in South Asia, considering its vitality for their Indo-Pacific strategy. They have amplified their diplomatic and economic presence in the region.

With South Asia attracting competition and the presence of multiple powers, the region’s states have responded in varied ways. Throughout the year, Pakistan, for example, distanced itself from the West and continued aligning with China, considering the former’s role in helping it transit to a geoeconomic state.

Other South Asian countries have, however, begun pushing back on China on multiple instances. Both Nepal and Bhutan have started formulating new policies to limit or prevent Chinese border intrusions. Bangladesh has refused to join Chinese projects for considerations of either strategic issues or economic feasibility. Western and Indian investments continue to flow into the country.

For their part, Sri Lanka and Nepal have used this past year to retain a degree of balance between its relations with both India and China. This balance has also determined the inflow of investments and infrastructure from these two large economies. Even Bhutan has begun looking for partners in the West to tackle its non-traditional challenges such as health and climate change.

Worsening extremism

Extremism was a serious challenge in South Asia in 2021. The amalgamation of politics and religion continued to nurture the extremist ecosystem that has already challenged the states and the institutions within.

In Sri Lanka, majoritarian politics could trigger mass unrest and make people more vulnerable to extremist content and propaganda. This is exacerbated by widespread use of social media platforms, on one hand, and on the other, the government’s failure to effectively reach out to the public.

In Muslim-majority countries such as Bangladesh and Maldives, the governments have continued to attempt to appease Islamist parties for electoral gains. This will only likely cause the mainstreaming of extremists and their ecosystem, thereby posing severe challenges to both the states. This threat is made more real by the presence of foreign fighters in the Maldives, and pan-Islamic extremist and terror outfits in Bangladesh.

For Pakistan, meanwhile, the year was characterised by sustained terror attacks and rallies by extremists, which will have long-bearing effects on the country. The Taliban’s takeover of Afghanistan has also induced anxieties of terrorism and trafficking throughout the region. There is concern that this will supplement, re-energise and normalise extremism and terrorism in the region.

The Weakening of Regionalism

Regionalism continued to be in decline in 2021. The Taliban’s takeover of Afghanistan, for one, has posed new challenges and debates within the already decaying regional organisation that is SAARC, or the South Asian Association for Regional Cooperation. The South Asian states have thus continued searching for alternatives to promote social and economic development.

Thus, bilateral cooperation and regional and sub-regional organisations such as the Bay of Bengal Initiative for Multi-Sectoral Technical and Economic Cooperation and the Bangladesh Bhutan India Nepal initiative are being used to promote connectivity and economic integration. China has also attempted to institutionalise its presence in South Asia and counter the SAARC.

Furthermore, a variety of minilateral forums have been proposed or loosely initiated in 2021. For example, India, Pakistan, Afghanistan, and Nepal, have worked on forming the same either with the West, the US or China. However, none of these initiatives have fructified as an alternative to the prevalent regional organisation.

Increasing competition, extremism, and diminishing regionalism have shaped South Asia in 2021. The implications of these will loom large in the coming year.

III. Multilateral Order

UNSC: Institutional Stasis Amid Great-Power Politics

Aarshi Tirkey

The United Nations Security Council (UNSC) is the UN’s primary organ tasked with the maintenance of international peace and security. Between January to December 2021, the council presidency rotated between four permanent members (United Kingdom, United States, China, and France), and eight non-permanent members (Tunisia, Vietnam, Estonia, India, Ireland, Kenya, Mexico, and Niger). The year also marked the beginning of India’s two-year stint as a non-permanent member of the UNSC, bringing with it the unique opportunity to shape its programme for a month.

In the backdrop of the COVID-19 pandemic, this year was beset by two regional crises: the military coup in Myanmar in February, and the Taliban’s takeover of Afghanistan in August. A significant trend was observed when Council members displayed a rare show of solidarity while taking cognisance of the two crises.

Solidarity and consensus

The UNSC collectively expressed concern regarding the violence in Myanmar, and called for an immediate cessation of violence. All 15 members of the UNSC did so unanimously through two press statements (February 2021 and November 2021), as well as a presidential statement in March during Washington’s council presidency. On Afghanistan, the UNSC adopted two resolutions: the first condemned the August 26 attacks at the Hamid Karzai airport and called on the Taliban to adhere to its commitment to allow Afghans to travel safely. The second resolution extended the mandate of the UN Assistance Mission in Afghanistan (UNAMA) which was established in 2002 to assist the state and the people of Afghanistan in laying down the foundations for sustainable peace and development. A press statement was also issued which called for “an immediate cessation of all hostilities” and the establishment of a new government that is “united, inclusive and representative”.

Absence of strong measures

Although members displayed solidarity, the UNSC was unable to adopt stronger measures that it is empowered to take under Chapter VII of the UN Charter. For instance, China opposed sanctions and other coercive measures to tackle the violent situation in Myanmar; it succeeded in blocking any resolution on Myanmar despite the egregious political violence taking place in the country. Moreover, while the resolution on Afghanistan was adopted, Russia and China had abstained from voting on the same. This demonstrates that it has become much more difficult to adopt ‘hard’ measures of sanctions and/or military action, as opposed to ‘soft’ measures of censure and condemnation. This continued weakening of the UNSC to fulfil its stated purpose, along with the intensification of the great-power contestation has contributed to the emergence of ‘minilaterals’ as alternative platforms to achieve security cooperation between like-minded countries.

Defining ‘security’

On the thematic aspect of “security” and what it entails, the UNSC members displayed consensus towards some, while remained divided over others. The high-level open debate in August 2021—chaired by PM Modi—was the first time that maritime security was discussed as a standalone theme before the UNSC. The outcome of the debate was a presidential statement which noted the “problem of transnational organized crimes” and emphasised “the importance of safeguarding the legitimate uses of the oceans”. However, India and Russia in December 2021 voted against a UNSC proposal that would authorise the Council to deliberate over issues related to climate change. Opponents argued that the UN Framework Convention for Climate Change (UNFCCC) would be the appropriate forum for addressing all such issues, whereas supporters asserted that climate change-induced events should be treated as a security threat as they can exacerbate existing conflicts.

While Council members were able to coalesce around some of the burning security challenges, the trendlines indicate that it has become significantly difficult for the UNSC to adopt stronger measures for the maintenance of international peace and security. Moreover, the contours of what defines “security” continue to evolve—countries have differing interpretations of what constitutes a security threat and which ones the UNSC can be empowered to deliberate upon. As the premier body with oversight on peace and security, the Council, through its proceedings, provides a look at trendlines that characterise global and country-level approaches to security threats.

Global Trade: A Revival, But Wider Regional Divergence

Abhijit Mukhopadhyay

Following many months of a pandemic-induced standstill, global economic activity underwent the beginnings of a revival in the first half of 2021, increasing volumes of merchandise trade above even pre-pandemic levels. This prompted the World Trade Organization (WTO) to revise its forecast for global merchandise trade volume growth rate to 10.8 percent in 2021 – up from 8.0 percent in March.

The following paragraphs outline the most palpable trends in global trade in 2021.

Global trade rebounds beyond expectations but recovery is marred by wide regional divergences.

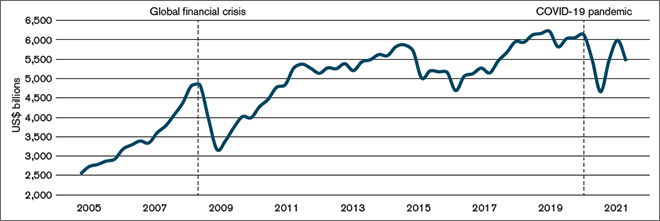

Total trade volume – in both merchandise and services trades – shows more resilient recovery in 2021, compared to the period after the 2008-09 global financial crisis (see Figure 1). The recovery is driven primarily by merchandise trade, as trade in services remains depressed.

FIGURE 1: Global trade (COVID-19 pandemic and 2008-09 global financial crisis)

* The line diagram represents the evolution of non-seasonally adjusted quarterly world trade volume for countries that reported both merchandise and commercial services trade flows.

Source: World Trade Report 2021, WTO

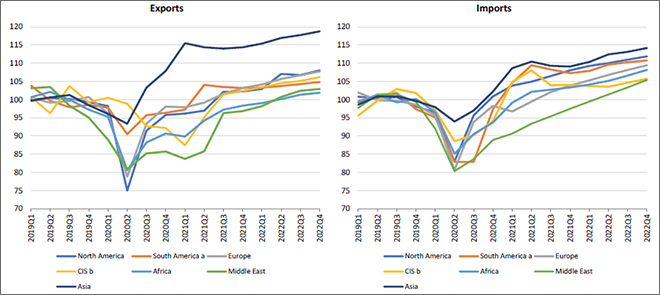

At the same time, however, the overall trade recovery continues to show divergence across regions. While Asia leads the rebound growth in both exports and imports, the Middle East, South America, and Africa have recorded the weakest recoveries in exports. On the imports side, the Middle East, the Commonwealth of Independent States (CIS) countries, and Africa are likely to have the slowest recoveries (see Figure 2).

Regions with more oil-reliant export bases went through drastic declines in both merchandise exports and imports during the 2020 pandemic-induced recession. These regions are yet to come out of those shortfalls in exports. South America’s comparatively better import recovery is partly the result of a low base effect, as some key economies were already in recession during 2019.

The rise of Asia in both exports and import growth and the decline of the oil export-reliant Middle East are the highlights of shifting trade horizons in 2021. As global vaccine inequality widens and the slowdown in infections is threatened by new variants of COVID-19, the risk of further divergence in regional trade recovery across the globe looks imminent.

FIGURE 2: Merchandise exports and imports by region, 2019Q1 – 2022Q4 (Volume index, 2019 = 100)

a Refers to South and Central America and the Caribbean.

b Refers to Commonwealth of Independent States, including certain associate and former member states

Source: WTO and UNCTAD

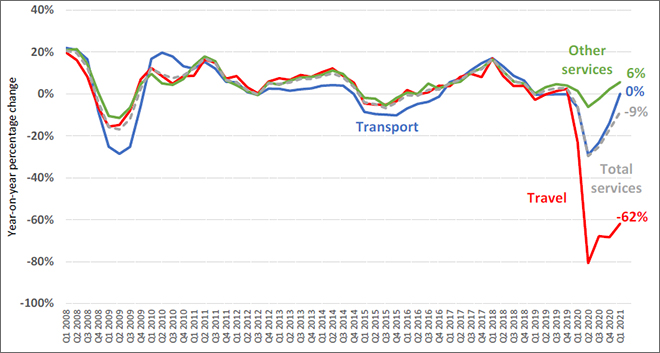

Trade in services is likely to stabilise around a lower trend line than the one before the pandemic.

Services trade was down by 9.0 percent year-on-year in the first quarter of 2021 – principally pulled down by a continued slump in the travel sector. Financial and other business services went up by 6 percent. Low base values in 2020 will likely take final annual services trade growth rate to the positive zone, although it is too early to predict a turnaround (see Figure 3).

FIGURE 3: World commercial services trade by sector, 2008Q1 – 2021Q1 (year-on-year % change)

Source: WTO-UNCTAD-ITC estimates

Source: WTO-UNCTAD-ITC estimates

WTO’s September projections suggest that trade in services may start stabilising by year-end, but the overall average growth trend will remain below the pre-pandemic levels.

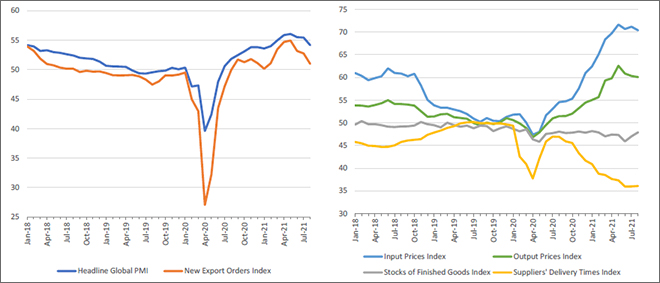

There will be upward pressure on both input and output prices in global trade due to pandemic-induced disruptions and supply chain bottlenecks.

Global Manufacturing Purchasing Managers’ Indices (PMIs) highlights the latest problem of port congestions. A plunging Suppliers’ Delivery Time Index indicates longer delivery times, and this has resulted in high prices for shipping services (see Figure 4).

The spike in shipping rates, along with strong rebound in export orders, signifies a resurgent global import demand. As the demand rises, prices of manufacturing inputs and final goods also sufficiently increased, as can be observed in the trends in the indices.

FIGURE 4: Global Manufacturing Purchasing Managers’ Indices (PMIs), January 2018 – August 2021 (Index base = 50)

* Values greater than 50 indicate expansion and values less than 50 denote contraction.

Source: IHS-Markit

Furthermore, a global shortage in semiconductors has hit the automobile industry significantly. Integrated circuits may have been diverted to other sectors like consumer electronics. Though this demand-supply mismatch seems to be temporary in nature, it can put additional pressure on input prices in the short run.

If sporadic economic disruptions continue due to the emergence of new variants of COVID-19 (such as the latest one named ‘Omicron’) – these existing economic conditions will only sharpen. This can lead to the risk of global inflation, particularly in tradeable commodities and services. Global equal access to vaccines will be key in averting such an eventuality.

Climate Action: Stronger Commitments But Less Finance

Aparna Roy

The year 2021 was an eventful one for global climate action, and of particular importance was the 26th Conference of Parties to the United Nations Framework Convention on Climate Change or COP26, held towards the end of the year. The year also coincided with the end of first five-year cycle of the Paris Climate Agreement of 2015. Countries across the world reported on their progress so far towards combating climate change and also on the renewed trajectory of progressive climate ambitions.

Much of these developments, as well as the climate change-related announcements by governments, businesses and other entities, are driven by certain all-embracing trends that shaped the discourse around climate change in the past year. These patterns are crucial as they give a sense of what to expect in the coming years; they also provide insights into the critical gaps that are emerging in the ongoing discourse around climate change.

The ‘Code Red’ warning

The first trend is the unequivocal warning from both, the scientific community and climate activists, around the need for immediate and urgent action. This stems from various reports which universally warn that, at the pace that climate change is happening, it has become nothing less than an existential threat to the Earth and all life on it; that stringent efforts to mitigate and adapt to changing climate is no longer an option, but an imperative. This was reiterated in the 6th Assessment Report by the Intergovernmental Platform on Climate Change which essentially issued a “Code Red” for humanity. It reaffirmed the stance of the scientific community of reducing carbon emissions by half till 2030 in order to restrict global temperature rise to below 1.5 degree Celsius. It also commented on the inadequacy of the progress made so far on this front and called on all countries to strengthen their climate ambitions and move towards a carbon-free world by 2050. Other than the scientific community, the momentum of climate action by activists was also a factor that gave shape to this trend. The role of youth activists in particular has been extraordinary. Demanding concrete action and denouncing the focus on rhetoric, youth activists spilled into the streets to express their displeasure with the way governments have been dealing with the issue of climate change across the world. This strengthened the trend of stakeholders outside the government machinery calling for stringent and urgent climate action.

Stronger Climate Commitments

The second overarching trend that shaped the landscape of climate change was the plethora of commitments from industry and government actors. More than 120 countries have pledged to transform themselves to a net-zero economy some time during this century, with most countries declaring their aim to do so by 2050. The most recent additions to this list include China (net-zero by 2060) and India (net-zero by 2070). This is a landmark development, given how their economic growth, like in other developing countries, continues to rely on coal. A complementary development for this trend has been the proactiveness shown by corporations and industry players in supporting the efforts of various governments. Examples include Adani and Reliance’s green plans in India, or the Royal Dutch Shell Plc announcing green commitments in the US.

The Challenge of Climate Finance

The third key trend this year was the issue of climate finance. It has been a matter of much discussion, and at the Glasgow summit, parties further postponed to 2023 the target of mobilising USD 100 billion in climate fund assistance from the developed countries to the global South. The need for climate finance for mitigation as well as adaptation has been recognised as a crucial obstacle to effective climate action. The same was true for 2021.

The future course of climate action must be informed by these trends. The challenges must be addressed in order for the global community to nurture a more sustainable future for our planet.

Tech, Society, and Geopolitics: Stranger than Fiction

Trisha Ray

2021 was a turbulent year, marked by growing pervasiveness of new and emerging technologies in our lives, even as social, geopolitical, and geoeconomic fissures continue to deepen. This piece highlights three trends: the virtualisation of everyday life, the ideological battles over the future of the internet, and the challenge of finding common ground on global governance of technology.

Digital Democracy: The Battle for the “Soul” of the Internet

“Digital democracy” has undergone a curious evolution. At first, it expressed how digital technologies could usher in a new era of civic engagement. This idea flourished during the Arab Spring, where social media platforms helped trigger a wave of pro-democracy movements.

Not too long after, this utopian vision got warped as these same digital tools began to be used in ways that laid bare the vulnerabilities of democratic systems. The year 2021 breathed new life into digital democracy, one that has pitted democratic nations in an existential battle against “digital authoritarianism”— a model of the internet that enables arbitrary censorship and widespread surveillance of citizens.

To be sure, democratic cooperation is not just about common beliefs and democratic values; it is a strategic tool. The December 2021 Summit of Democracies guest list was, for example, carefully curated based on the US’s own panoply of national security, economic and strategic interests. There are also players in this space that are arguably at par with governments in terms of agenda-setting, influence, and power: big tech. Justified concerns remain about how they collect, use and share data; and how they moderate content, often using standards that do not align with the laws of the country the user is located in.

In the years ahead, will we witness the emergence of a consensus on common democratic principles for the governance of digital spaces? And will these principles be reflective of views that are neither US-centric nor Eurocentric?

The Cake is a Lie: Escaping into the Metaverse

The virtualisation of our daily lives is not a new idea. Inklings of the metaverse can be found in the rapidly growing virtual reality (VR) market, in the explosive entry of NFTs into public consciousness, and most recently in the re-christening of the Facebook Group as Meta. The bandwagon keeps growing: the Seoul Metropolitan Government announced “Metaverse Seoul”, a plan to bring the city’s major cultural, civic and economic centres and services into the metaverse. Virtual “land” in the metaverse is being sold for millions; entire concerts are being held in the metaverse.

That said, the corporate imagining of the metaverse is decidedly banal: endless boardrooms; Zoom meetings but worse; transforming employees into efficient, always-plugged-in productivity bots.

The irony of being encouraged to plunge into the metaverse in the midst of a seemingly unending pandemic is also not lost. The term finds its origin in the 1992 sci-fi novel Snow Crash, set in a United States that has undergone economic collapse that plunged it into near-anarchy. The utopian vision of the metaverse being sold by tech companies is rooted in a dystopian reality. Or, as Marie Antoinette (may have) said, “Let them eat cake.”

The Goldilocks Problem in Emerging Tech Governance

2021 saw, despite all geopolitical odds stacked against them, consensus and agreements on global technology governance. The UN GGE on Advancing Responsible State Behaviour in Cyberspace adopted a consensus report, its first since 2015. The disagreement on the applicability of IHL, one of the main reasons why the 2016-17 GGE failed to achieve consensus, appeared to be settled as well. In AI, UNESCO adopted the Recommendation on the Ethics of Artificial Intelligence, which included principles of proportionality, equitability and fairness, environmental sustainability, data protection, as well as 11 specific policy action areas. The depth and breadth of the recommendations are dampened of course by the fact that the US, a leader in AI development, is not a UNESCO member, courtesy former President Donald Trump circa 2017.

A persistent issue, however, is inconsistent application of principles, which adulterate them in ways that are antithetical to their original intent. For any set of principles to become norms, they must be consistent and clear, not just in their application but in terms of consequences for violating them. In the coming years, observers should keep a keen eye on how these nascent norms-making processes play out on a national and sub-national level, in the form of concrete commitments and legislation.

Healthcare Reform: The Transformative Potential of the Pandemic

Oommen C Kurian

The last two years have shown that the direct impact of COVID-19 in the form of deaths and suffering has been only one part of the tragedy that is still unfolding. The disruption that the pandemic caused in the health sector effectively denied healthcare services to a large number of critically ill patients, causing avoidable deaths. Doctors share stories of meeting their cancer patients again, for example, after the severe pandemic waves, only to realise that lack of treatment resulted in the cancer worsening to advanced stages. Moreover, the economic disruption from the pandemic as well as the strict public health containment measures have triggered severe social and economic distress, perhaps at an unquantifiable scale.

It is often said that the skies are darkest just before dawn breaks; that things ought to get worse before they get better. However, with the experience of 2020 and 2021 before us and with the Omicron variant wreaking havoc, any forecast for 2022 remains highly uncertain. At the same time, as a definitive marker in world history, the pandemic may have triggered possible fast-paced changes in national health systems across the world, as it re-emphasised the strong link between a resilient health system and economic growth.

Healthcare as a Strategic Priority

First, it is expected that political barriers to universal healthcare will be weakened significantly due to the devastating impact of the pandemic. The ruling elites in many developing countries have faced the frightening prospect that they can no longer isolate themselves from health risks by selectively accessing the health system of a developed country according to their need. This will have long-lasting impacts in national health systems across the world, particularly the weaker ones.

Indeed, the status quo has changed for good; and policymakers will be forced to shed conventional wisdom around issues such as prioritising healthcare services, private sector participation in service delivery, and unbridled flow of healthcare personnel from the global South to the global North.

Democratisation of Health Systems and Business Models

The second major impact of the pandemic will be on global health governance structures, including institutions like the World Health Organization. Two years of the pandemic have strengthened demands for institutional reform like never before. Many countries, including India, have suggested that reforms within WHO are long overdue. As the global demand for operationalising the “health for all” agenda increases significantly amid the pandemic, only far-reaching reforms in the key institutions can ensure equitable and efficient changes in health systems.

The pandemic proved that the global pharmaceutical manufacturing ecosystem answers mostly to dollar power, and empty rhetoric on global solidarity may not amount to much in the real world. The stark vaccine inequality, which the world surprisingly tolerated in 2021, is likely to become politically untenable in 2022, and the case for local pharmaceutical production will be stronger than ever in most countries of the global South. This will have several strategic imperatives as well.

India’s experience in the sector makes it uniquely placed to mentor developing countries in achieving some level of self-sufficiency in their health systems, at least across Asia, Africa, and Latin America. The demand for health system reform and enhanced domestic investments will likely ensure that such shifts may now even make business sense. Many pharmaceutical multinational corporations can make strategic moves readjusting their current business models to secure a portion of the pie, if such tectonic changes do happen. Any movement towards a more broad-based, high-volume, low-margin model in pharmaceuticals will mean a key global leadership role for India, in general, and Indian pharmaceutical companies in particular.

Healthy Lifestyles as Vaccine

Lastly, continuous waves of novel-coronavirus variants have made a convincing case that a healthy lifestyle may be the only true vaccine available yet. In the immediate future, it is expected that there will be renewed focus on prevention, with greater attention being paid to the benefits of physical activity and healthy food habits, and to reducing self-harming behaviour such as smoking and excessive consumption of alcohol.

The pandemic may yet manage to shake the world from its stupor, and finally acknowledge that green spaces and playgrounds are as important parts of a national healthcare infrastructure as hospital buildings. Then SARS-CoV-2 could be said to have played its part in changing history and influencing modern society.

The views expressed above belong to the author(s). ORF research and analyses now available on Telegram! Click here to access our curated content — blogs, longforms and interviews.