The Geopolitical Imperative for Reorganising Global Supply Chains

Global supply chains are being restructured to achieve distinct geopolitical goals, given the strategic vulnerability of such networks due to being controlled by a few nations. Countries that are prominent sourcing hubs for some supply chains could potentially ‘weaponise’ their economic influence for larger geopolitical gains. This brief argues that although multiple global efforts have been initiated to address such threats, efforts to restructure supply chains must be accompanied by financial incentives to minimise the costs associated with such a reorientation.

Attribution:

Amitendu Palit, "The Geopolitical Imperative for Reorganising Global Supply Chains,"ORF Issue Brief No. 533, April 2022, Observer Research Foundation.

Introduction

Amidst the COVID-19 pandemic, the reconstruction of global supply chains is being premised on geopolitics rather than just economic efficiency facilitated by globalisation. This is an unprecedented endeavour. Global supply chains in various industries have evolved based on the specific economic advantages of different countries in contributing to the diverse stages of the supply network. These advantages range from being a supplier of raw materials, intermediates, parts and components, to having the ability to design and market. Producers from different countries with distinct advantages were brought together to maximise economic efficiencies, but this rational is now being contested by geopolitical developments. Economic efficiency alone is no longer the driver of supply chains, with geopolitical imperatives becoming significant factors in the organisation of such networks.

This brief attempts to assess the feasibility of geopolitically-driven efforts to reorient supply chains. It reflects on the character of supply chain disruptions before and after the outbreak of COVID-19 to understand how geopolitics has become a major driver of such networks. It reviews the prospects of the economic fundamentals of supply chains aligning with the geopolitical push. It argues that efforts to reorganise supply chains by multi-country coalitions such as the Quadrilateral Security Dialogue (Quad) will encounter challenges as they try to reconcile geopolitical imperatives with economic efficiency.

Understanding Supply Chain Disruptions

Global businesses were grappling with disruptions in supply chains long before the onset of the COVID-19 pandemic. In recent years, various supply chains have experienced disruptions due to diverse reasons, with natural calamities being the most prominent disruptor (see Table 1).

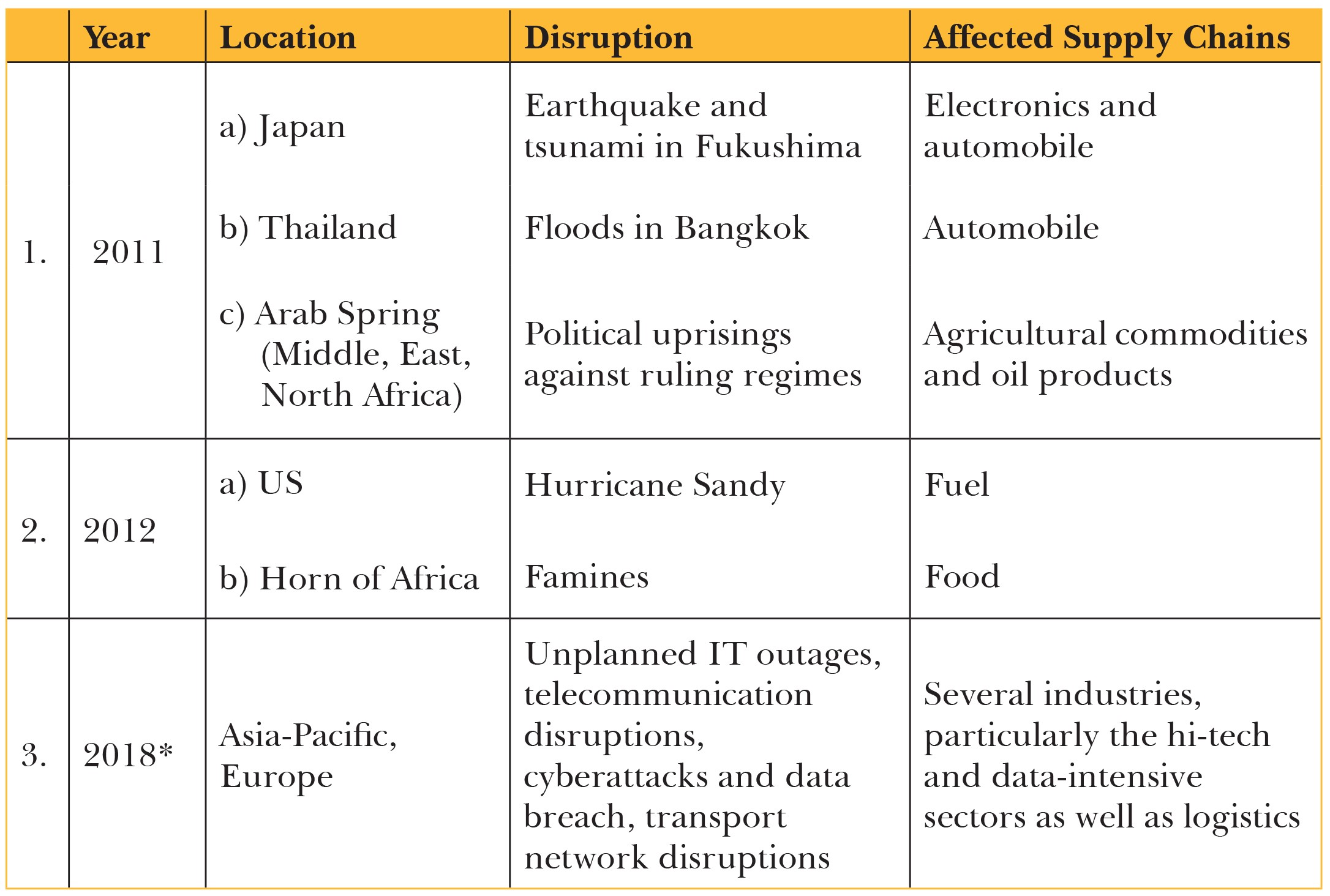

Table 1: Prominent Disruptions and Their Impacts

Note:*The disruptions are reported from a survey of regional business responding to supply chain breakdowns for 2018. The impressions are likely to have been not just for 2018, but even in the earlier years of the decade. Source:World Economic Forum[1]and Asian Development Bank[2]

The 2011 Fukushima earthquake was the first event of consequence to draw the attention of global businesses to the sourcing vulnerabilities of supply chains that used semiconductors.[a],[3]Widespread flooding in Thailand in the same year reinforced the wisdom obtained from the Fukushima disaster about the helplessness of downstream assemblers[4]in several supply chains with respect to critical dependencies for sourcing parts and components from a few select countries (Thailand and Japan, in these instances). Other natural calamities, such as Hurricane Sandy in the US in 2012 and the famines in several African countries in the early years of the last decade, produced widespread supply chain disruptions.[5]

Indeed, global businesses identified natural disasters and extreme weather events as the most prominent risks to the uninterrupted functioning of supply chains.[6]Political unrest and social conflict, such as the Arab Spring in West Asia, were other important factors that caused disruptions. Towards the end of the last decade, just before the onset of COVID-19 in January 2020, unscheduled IT disruptions were noted as major causes of supply chain breakages, along with adverse weather events, cyberattacks, data breaches and natural disasters.[7]

While the pre-pandemic disruptions were sporadic and often localised in their impacts, the upheavals caused by COVID-19 were extensive. Indeed, these disruptions, which begun from the strict lockdowns introduced in China from early 2020 to curb the pandemic (particularly in the Wuhan province), affected many supply chains that relied extensively on that country for sourcing. Wuhan is one of the most important sourcing hubs in China, with over 900 Fortune 500 companies having supply links with the province.[8]The impact of the shutdown in Wuhan was expectedly profound—supply shortages led to production cutbacks across various supply chains, acquiring wider proportions when the pandemic spread to Southeast Asia and the region introduced lockdowns that affected more sourcing.

China was able to recover from the pandemic faster than other parts of the world, enabling a resumption of activities across several supply chains. However, it has since experienced subsequent periodic disruptions—such as the closure of the Ningbo-Zhoushan port, one of the busiest cargo ports in Asia-Pacific, in August 2021 due a COVID-19 outbreak among workers—that have caused serious disruptions in container and cargo movements.[9]Further disruptions are expected from the renewed surge in cases in the mainland since March 2022.

Supply chains continue to remain prone to disruptions; business surveys point to a variety of factors, including human illnesses, loss of skills, transport disruptions, outsourcing failures, and insolvencies, as the key supply-chain disruptors post-COVID-19.[10]Notably, these factors are systemic outcomes of COVID-19. The urgency to adapt to digital operational modes during the pandemic has resulted in occasional efficiency loss and disruptions in supply chains since different firms at the various levels of the networks have digitalised at varying paces.[11]The prevalence of the pandemic in the Asia-Pacific region has also led to periodic industrial closures that have impacted vital supply chains, such as semiconductors[b],[12]and large batteries, with production continuing to remain below-capacity in Japan, Korea, Taiwan, China and Malaysia, all prominent sources of electronic chips and lithium batteries.

The outcome of the disruptions in supply chains in the post-pandemic period has been to boost their resilience amid unforeseen exigencies, such as those arising from the pandemic and its persistence. From a firm-level perspective, resilience is seen as the ability of supply chains to acquire adaptive capacities to withstand unforeseen disruptions and resume normal functions.[13]The World Economic Forum defines resilience as “the ability of a global supply chain to reorganize and deliver its core function continually, despite the impact of external and or internal shocks to the system.”[14]

A key aspect of the efforts to build resilience is to work towards diversifying sourcing by reducing the dependence on a few key sourcing locations. The need to diversify has been strengthened by the urge to decouple supply chains from countries that are major sourcing hubs and may be inclined to exploit the advantage for geopolitical benefits. This distinct geopolitical feature of the ongoing multi-country effort to reorganise supply chains through sourcing-diversification strategies is a notable outcome of COVID-19.

Geopolitical Factors

The deeply integrated modern world presents significant opportunities of economic coercion by certain countries. The close integration of the various stages of economic production—best symbolised by the well-knit and spatially dispersed global supply chains—makes all stakeholders involved in the supply chains vulnerable to the ‘power’ that each has in running these networks. Such powers can be used to obtain geopolitical benefits by countries that are conscious of the strategic influence yielded by their businesses in the supply chains. Indeed, several countries have shown an increased tendency towards such actions, reflected in the rising incidents of coercive economic measures, such as import and export bans or restrictions, the imposition of discriminatory tariffs on imports, and stringent localisation requirements (especially for valuable intellectual property in technical processes and know-how).[15]

The tendency of employing economically coercive measures has been particularly noticeable over the past decade, when ‘trade wars’ between countries became common. These wars are characterised by unilateral trade-restrictive actions by countries that are economically strong and able to use their geoeconomic strengths for geopolitical benefits. The US-China trade war is a case in point.

In March 2018, the Trump administration initiated unilateral trade actions by raising tariffs on imports considered strategic to the US’s national interests (steel and aluminium items) and escalating tariffs on several items imported specifically from China. Tariffs on all steel and aluminium imports into the US were increased by 25 percent and 10 percent, respectively.[16] Separately, tariffs were imposed on imports from China. These actions invited tariff retaliation from China, leading to several items traded by the two countries coming under new levies.[17]The EU, Canada, Russia and many others reacted to the US tariffs on steel and aluminium through retaliatory tariffs and formal complaints at the World Trade Organization (WTO),[18]and several countries, including China, India, Russia, Thailand, the EU, Mexico, Canada, Brazil and Singapore, filed disputes filed against the US at the WTO.

China too, has long tended to employ trade coercion in its dealings with other countries. Notable examples include China’s blocking of rare earth mineral exports to Japan during a dispute over Senkaku islands in the East China Sea (in 2010), and further trade coercive measures taken at various points in time against the Philippines (in 2012), Taiwan (in 2016), South Korea (in 2017), and most recently, Australia (in 2020).[19]

Importantly, none of China’s coercive actions were imposed to achieve specific domestic economic objectives, such as protecting local industries from foreign competition, which was the ostensible objective of the Trump administration’s trade restrictive measures.[c]The Trump administration used the US’s economic heft to rework several existing trade agreements (such as the North American Free Trade Agreement and the US-Korea Free Trade Agreement) by building in provisions that were more beneficial for American industries and workers to secure domestic political gains.[20]In China’s case, however, the impetus seems to have been to respond to the foreign policy positions taken by countries critical of Beijing on various international issues. This is visible in Europe, where a diplomatic dispute with Lithuania arising from the latter allowing Taiwan consular access in its territory led to China imposing trade sanctions on the country and pressurising European businesses from trading with Lithuania.[21]

The ‘punishing’ goal of trade coercion is perhaps best exemplified by China’s actions against Australia post-COVID-19. Australia’s economic dependence on China is striking—China is its largest export market and source of imports.[22]In the aftermath of COVID-19, China restricted major Australian exports, such as barley, grain, beef, coal, wine, and sugar by raising tariffs (barley), banning imports (grain, beef), initiating anti-dumping investigations (wine), and instructing local businesses to defer buying (coal). Chinese tourists were also discouraged from travelling to Australia, as were Chinese students, who were encouraged to explore other higher-study locations. The coercive actions were prompted by Australia’s leading role in urging the World Health Organization to conduct an independent enquiry into the origins of COVID-19, which irked China.[23]Indeed, these actions against Australia were the latest in a series of similar behaviour by China against trade partners with whom it runs into diplomatic disputes, leaving little doubt of its intention to use trade actions for political goals.

Global supply chain vulnerabilities arising from high sourcing dependencies have been driven by industrial advances in the recent decades. Exponential growth in the use of hi-tech items, such as smartphones, tablets and laptops, have increased the reliance of such supply chains on the country sources of these products. China now extensively dominates various stages of production in these specific chains and there is mounting anxiety over the country ‘weaponising’ its economic control over various supply networks to its geopolitical advantage.[24]COVID-19 has accentuated such fears, with China enjoying huge leverage in strategic industries such as pharmaceuticals and critical minerals due to its abundant domestic endowments. This, coupled with China’s tendency to resort to coercive tactics against diplomatically ‘errant’ trade partners, has spurred the drive to diversify sourcing and relocate supply chains substantively out of the mainland.

The weaponisation of supply chains must be understood in the context of the US-China conflict, which is premised on the race for technological supremacy.[25]The conflict is explained around the principle of techno-nationalism, which ties national technological capabilities to national security and economic progress. The race to dominate critical technologies and their global supply chains are inevitable in this regard. An inevitable outcome of the conflict has been the need to retain control over critical technology supply chains (for instance, semiconductors, rare earth minerals, telecommunications, and pharmaceuticals) that have a significant bearing upon both countries’ national security interests, including the efforts to expand strategic influence over the world order. COVID-19 has accentuated the competitive tendencies between the US and China in this regard. Its onset revealed the criticality of ‘owning’ vital supply chains by diversifying sourcing and building local capacities.

The geopolitical urge to move supply chains out of China after COVID-19 has seen a flurry of activity among countries, mostly the US and its allies (comprising global middle powers with large economies), to come together to safeguard supply chains. The most notable initiatives are the Quad (comprising Australia, India, Japan, and the US); the Supply Chain Resilience Initiative (SCRI) by India, Japan, and Australia; and the G7’s commitment to strengthen supply chains. All three initiatives share a common anxiety over supply chains being weaponised to serve the security and strategic goals of countries that possess the geoeconomic capacities to disrupt such networks. The initiatives are aimed at neutralising the influence that China can exert on supply chains, and the goal is clear from their composition—all countries are, if not US defence allies, at least important strategic partners of the US, threatened by the prospects of China exploiting its economic clout for geopolitical power projection.

Going forward, the US and China are likely to work with their allies to secure these objectives. The result of such efforts will be to posit supply chains as instruments of strategic influence; as both countries and their allies aim to control more and more of the critical supply chains, these will become geoeconomic tools for geopolitical rivalry.

Aligning Geopolitics with Business

Substantial diplomatic efforts have been invested in the Quad’s resurgence amid the pandemic. COVID-19 has infused new energy in the Quad, with the group’s members committing to work together to boost the resilience of global supply chains. The first iteration of the commitment came at the foreign ministers’ meeting in Tokyo in October 2020,[26]and was restated by the Quad heads of the states in their meetings in March and September 2021: “We are mapping the supply chain of critical technologies and materials, including semiconductors, and affirm our positive commitment to resilient, diverse, and secure supply chains of critical technologies, recognizing the importance of government support measures and policies that are transparent and market-oriented.”[27]

The emphasis on government support resonates with the sentiments expressed by the SCRI. The SCRI was proposed by Japan, India, and Australia—all Quad members—in September 2020[28]and was amplified further in April 2021.[29]Indeed, given the similarity of purpose and commonality of members, the initiative may well be subsumed into the Quad in the future.

It is also noteworthy that the overall emphasis on increasing the resilience of supply chains, particularly those involving critical technologies and materials (and, therefore, sensitive from geopolitical and security perspectives), has also been expressed by the G7 group of countries in their June 2021 summit.[30]The G7 includes the US, UK, Canada, Japan, Germany, France, and Italy, and comprise the world’s most prominent grouping of high-income industrialised nations. The June summit also included Australia, India, South Korea, and South Africa.[31]As such, the meeting had all members of the Quad and SCRI, underpinning the prospect of the two groups and the G7 working together to pursue the common objective of making strategic supply chains more resilient.

Seen through the prism of geopolitics, the G7, Quad and SCRI reflect an emerging pattern of global political coalescence taking shape around supply chains. The coalition comprises major democracies with open societies. Between them, the countries have significant technological capabilities—both existing and emerging—and are well-positioned to host new supply chains.

The key question is whether these coalitions, which represent one side of the US-China conflict on technological supremacy and weaponisation of supply chains, will be able to economically sustain the shifts in supply chains. This is crucial because geopolitics has never been the driver of supply chains.

Since the onset of the current round of economic globalisation around four decades ago, supply chains have been spatially dispersed to maximising on the economic efficiencies of various geographical locations. This explains why despite being the global frontrunner in technological innovation, the US mostly limits itself to the design of semiconductors, and imports chips, to be used by its domestic industries, from cheaper manufacturing locations in the Asia-Pacific region. It also explains why the US and most of Europe have vacated the upstream supply space for producing drug intermediates and raw materials and import them from China to produce finished dose formulations at their factories.

Economic globalisation resulted in the extensive slashing of cross-border tariffs across the world, enabling the unrestricted movement of vast volumes of goods and components among countries. Coupled with similarly liberal rules for the cross-border movement of capital, export-intensive investments by lead firms in various global supply chains have led to the growth of densely enmeshed layers of mutually supportive businesses in geographically dispersed supply chains.

The current geopolitical environment calls for a retreat from the principle of economic efficiency shaping supply chains. It further demands a reorganisation of supply chains, including the physical reshoring of several existing networks, among a group of ‘like-minded’ countries (a band of states that are geopolitical allies).

Challenges

The Quad has seized the context of the pandemic to address global public health challenges through a vaccine partnership; Australia, India, Japan, and the US will leverage their respective economic strengths to make a billion doses of the COVID-19 vaccines by the end of 2022 for countries in the Indo-Pacific region. The US International Development Finance Corporation will finance increased capacity in India’s Biological E for making vaccines; Japan will provide concessional loans to India to expand the manufacturing of COVID-19 vaccines for export; and Australia will financially contribute to providing vaccines and ensure logistics for their regional distribution.[32]However, extending a similar partnership template to strategically sensitive supply chains, such as semiconductors and large batteries, might be challenging due to China’s current influence over these networks as a major sourcing location and a significant final demand market.

The steady growth prospects of the Chinese economy, notwithstanding the pandemic, ensures that lead firms in most hi-tech supply chains will continue to look at China as a major market for consumption, particularly in products like lithium-ion rechargeable batteries and consumer electronics. At the same time, the lead firms in these chains will also seek to stay geographically close to the Chinese market to ensure that ‘just-in-time’ supplies are not choked and inventories not exhausted, as it happened during COVID-19.

Reshoring production from mainland China to ‘like-minded’ countries will also depend on the financial incentives that they are able to offer. Japan, Australia and India have announced various policies in this regard—Japan has announced subsidies to encourage its companies to relocate back to the country and several others from China;[33]India has announced production-linked-incentives to expand local capacities in several industries;[34]and Australia has announced an economic package for more resilient supply chains and greater domestic manufacturing capacities.[35]The challenge in the foreseeable future is to ensure that sourcing dependencies on China do not constrain the reshoring of supply chains. Locating alternative sourcing destinations and building enough local capacities are the ways forward. However, despite the financial incentives, the results will take time to be delivered.

In the meantime, exogenous geopolitical events might significantly complicate reshoring prospects. The Taliban’s capture of power in Afghanistan and its easy ties with China offers Beijing an unprecedented opportunity to access Afghanistan’s untapped mineral resources, including lithium and rare earths, increasing its control over the global critical materials market with significant implications for strategic supply chains.[36]Other such geopolitical developments with far-reaching geoeconomic implications will pose challenges for the prospects of reorganising global supply chains among the Quad, SCRI and G7 coalitions.

Conclusion

The COVID-19 pandemic caused large upheavals in global supply chains, made more pronounced by most countries’ inability to address the disruptions. With national resources focused on tackling the pandemic-induced public health exigencies, supply chain fractures have only deepened.

At the same time, COVID-19 also unleashed a notable geopolitical urge to reorganise global supply chains. Stemming from the trend of techno-nationalism that has characterised the US-China conflict, post-pandemic developments, primarily China’s deteriorating ties with several US allies, have led to the crafting of multi-country coalitions to boost the resilience of strategic supply chains.

Notwithstanding the overriding geopolitical drive, reorganising supply chains, driven by rationale of economic efficiency, will not be without challenges. Much will depend on how the participating countries are able to align their business and regulatory policies to facilitate the reorganisation, and how they manage unforeseen geopolitical developments.

Endnotes

[a]A decade later, the vulnerabilities have accentuated to result in a global shortage of semiconductor chips following production lockdowns in Taiwan and Southeast Asia to tackle the COVID-19 outbreak.

[b]A telling reflection of the chip shortage and its impact on supply chains are the lower sales for Apple, which CEO Tom Cook has attributed to supply disruptions from Southeast Asia.

[c]The US steel and aluminum tariffs were, however, imposed on national security grounds under Section 232 of the US Trade Expansion Act of 1962. The national security justification was to ensure sufficient domestic availabilities of steel and aluminum, as these are widely required by domestic industries, and their import-reliance could be detrimental for national security. Tariffs were, therefore, meant to encourage greater local capacities.

[13]Jamison M. Day, “Fostering emergent resilience: the complex adaptive supply network of disaster relief,”International Journal of Production Research52(7): Pages 1970–1988, 2014

The views expressed above belong to the author(s). ORF research and analyses now available on Telegram! Click here to access our curated content — blogs, longforms and interviews.

Dr Amitendu Palit is Senior Research Fellow and Research Lead (trade and economic policy) in the Institute of South Asian Studies (ISAS) in the National ...

PDF Download

PDF Download