The Digital Indo-Pacific: Regional Connectivity and Resilience

Introduction: The Digital Indo-Pacific

At its heart, the Indo-Pacific is a term with its roots in the maritime realm, a confluence of security, economic, and geopolitical interests linked to free and open movement between the Pacific and Indian Oceans. A relatively new entrant in geopolitical nomenclature, the ‘Indo-Pacific’ has since expanded to capture several ideas: the rule of law, balancing against China’s rise, strengthening regional institutions, and, most recently, securing technology and information flows.

However, the Indo-Pacific also reflects distinct aspirations amongst those who use it. The United States’ framing, being militarily driven, ends at the west coast of India with the US Indo-Pacific Command.[1]India’s conception, driven by its broader political-economic vision, stretches from the horn of Africa to the western Pacific.[2]

The emergentDigital Indo-Pacificconcept is linked to four factors. The first, the region is home to the largest, most rapidly growing internet user bases in the world. The region accounts for a little over half of the world’s internet users, and these users are primarily young and mobile: over 90 per cent access the internet using their phones.[3]The vibrant digital ecosystem is buoyed by booming e-commerce and fintech applications and an engaged and wired user base: Thailand, Philippines, Indonesia, Malaysia and India spend the most time online on their phones in the world.[4]

Second, there has been a search for regional and domestic alternatives due to the US–China trade war during the Trump administration. While some countries in the region are holding onto a semblance of balancing their ties with both countries, several are shifting decades-old stances to adapt to changing dynamics. For some, this has taken the form of enhanced investment into domestic technology capacity-building, investment in R&D and in skilling and education. The Quad has also gotten a new lease on life and, in October 2020, the foreign ministers of Japan, Australia, India, and the US met to discuss ‘secure digital connectivity’.[5]

Third, exposed by the trade war and heightened by the pandemic is the essentiality and fragility of global technology flows. With governments, businesses and individuals forced to rely on online means for continuity, there is both a greater appreciation of the importance of digital spaces, services, and goods as well as greater scrutiny of bottlenecks created by ‘efficient’ global supply and value chains.

It is within this milieu that this paper seeks to analyse regional connectivity and resilience. The four sections of this paper – Minerals and Technology Manufacturing; Digital Economy and Adoption; Inclusive Digital Transformation; and Regimes – represent a ‘four-layer’ framework for analysis.

Connectivity encapsulates technology trade, access to online services (where access is a spectrum, not a binary), as well as interoperable regimes, including data protection and cybersecurity.

Resilience, meanwhile, has been defined various ways, with varying levels of detail. K.A. Foster defined regional resilience simply as ‘The ability of a region to prevent, prepare, respond and “recover” after a disturbance so as not to stand this obstacle to its development’.[6]Oksana Palekiene added further nuance to this description, calling it the ‘[c]apacity of a region to withstand and recover from external pressure or shock in order to maintain region’s growth path close to potential or, if it is necessary, to reorganize its structure and transit to the new growth path’.[7]For the purpose of this paper, regional resilience is defined as the ability of the region to withstand and recover from shocks generated by political, regulatory, and economic action by one or more major partners. This is represented in the following ways: diversification, domestic capacity, and strength of regulation.

This paper analyses seven countries – India, Australia, Singapore, Vietnam, Cambodia, Indonesia, and Malaysia – all representing different systems of governance, demographic drivers, levels of maturity of digital ecosystems, and economic models.

Finally, the Conclusions and Recommendations section pulls out a few key observations based on the research and identifies pathways for collaboration condensed into 10 recommendations. The aim of this paper is to lay a foundation for inclusive collaboration toward a Digital Indo-Pacific, which accounts for the differing but complementary strengths present in the region.

Minerals and Technology Manufacturing

Global Supply and Value Chains

While the jury is out on the precise trade-off between the national security imperatives of import and export controls, and the competitiveness of a country’s technology industries, countries have been re-evaluating their trade interdependencies under the looming shadow of the US–China ‘decoupling’.[8]

Global value chains (GVCs) account for nearly 50 per cent of global trade.[9]However, while GVCs grew rapidly in the 1990s and early 2000s, riding a wave of liberalisation and globalisation policies, they plateaued after the 2008 global financial crisis and are now likely to crunch due to what the World Bank characterises as growing ‘disenchantment with free trade’.[10]

Chandrasekaran, co-chair of the US-India CEO Forum highlighted this shifting equation: ‘the global supply chain is getting redesigned, redefined because supply has always been created for efficiency. Now the recent incidents, the pandemic, the geopolitical situation, and trade issues have stressed the importance of having a supply chain that is rebalanced, resilient and not only efficient.’[11]

Different countries have adopted different strategies to position themselves in this arena. Singapore’s Lee Hsien Loong’s measured ‘Asia-Pacific countries do not wish to be forced to choose between the United States and China’ is emblematic of the region’s hesitation to label either country a threat outright, due to the economic, institutional, and security benefits of ties with both.[12]

The pandemic, while not a driving factor, has seen the intensification of scrutiny of the risks of global supply and value chains. The trend toward ‘regionalisation’ and indigenisation will continue in the coming decade. What then are the strengths and weaknesses of the region in the physical components that go into technologies?

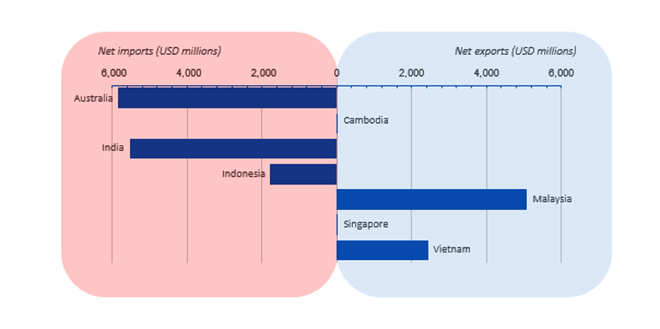

Fig 1: Hardware (HS8471) imports and export in USD millions (data extracted from Comtrade)

Of the seven countries under study in this paper, three are net importers (Australia, India, Indonesia) and four are net exporters (Cambodia, Malaysia, Singapore and Vietnam) of computer hardware.[13]

This section will use components for smartphones as a proxy for where the countries in this study are placed in technology GVCs and whether they are able to develop and exploit their resources. The components studied will include rare earths and semiconductors.

All smartphones consist of the following components: an integrated circuit or a ‘system-on-a-chip’; the sensors (for touch, light, motion etc); the screen (usually LCD); a battery; camera; and speaker.

The globalisation of supply chains and the ‘slicing of the value chain’ over the past decades means that ‘firms across advanced and developing countries add value along these global supply chains by completing a specific task associated with the production of a finished product and then exporting it’.[14]The supply chain of a smartphone typically spans several countries and hundreds of suppliers. Therefore, net ‘exporters’ of electronics like Vietnam and Malaysia are part of a regional value chain and are heavily dependent on components from China, and usually fulfil basic assembly roles. South Korean ICT giant Samsung, for instance, operates smartphone factories in Northern Vietnam but supplies its electronics components from China.[15]

This section of the paper focuses on rare earth elements (REEs) and semiconductors as basic indicators of dependency and potential to ‘move up’ the GVC for electronics. Subsequent sections will delve into the innovation ecosystems of these countries, including skills, R&D, and regulation.

Rare Earths

Rare earths elements (REEs) are a group of 17 elements that have become increasingly strategically relevant in the digital age. Rare earths are used in components for televisions, electric cars, smartphones, and medical imaging, among many others.[16]All REEs are not equal: their differing properties lend them to different end uses.[17]

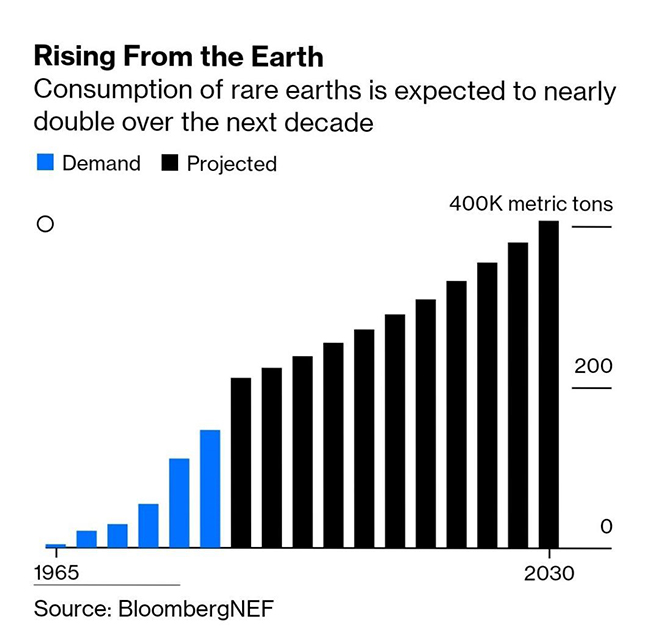

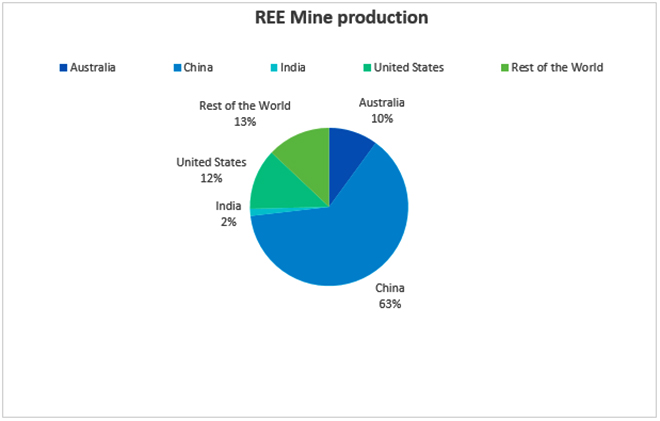

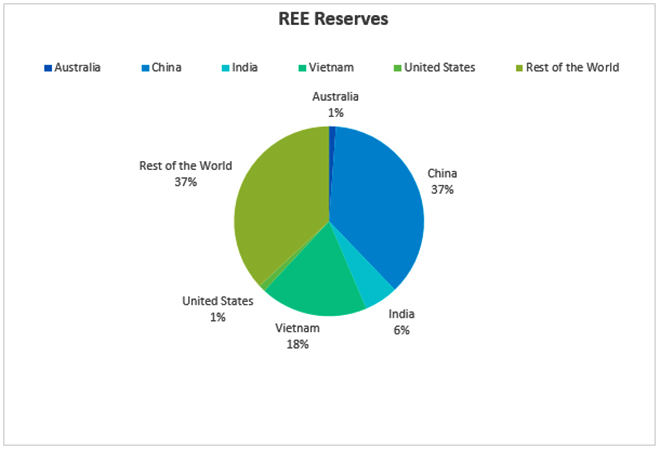

Global consumption of rare earths is expected to double over the next decade, driven primarily by growth in consumer electronics (especially mobile phones) as well as ‘green tech’ such as electric vehicles.[19] While China dominates the production of rare earths, there is no dearth of global reserves, so while it accounts for 63 per cent of mine production, it accounts for only 36 per cent of global reserves. Among the countries in this study, Australia, Vietnam, and India possess significant reserves of rare earths.[20]

The drive to diversify away from China has also taken the United States to Africa. The Pentagon’s Defense Logistics Agency is, for instance, conducting outreach to REE miners in Sub-Saharan Africa,[21]and South Africa has unearthed REE reserves with some of the highest concentrations in the world.[22]

The production of rare earths is, however, steeped in start-up and long-term hidden costs. Surveying, extraction, chemical processing, and management of rare earths incur significant expenses, especially since rare earths are not found in concentrated pockets, making their extraction a tedious and dangerous process.[23]The separation process typically uses concentrated acids, which – in the absence of proper waste management and environmental regulations – result in erosion and water contamination. Additionally, REEs are often found in conjunction with radioactive elements like thorium and (to a lesser extent) uranium, meaning that processing of REEs often generates slightly radioactive waste.[24]If the experience of the Democratic Republic of Congo, which supplies over 60 per cent of the world’s cobalt, is anything to go by, mining of lucrative minerals in the absence of strong institutional, legal safeguards will result in environmental degradation and human rights abuses.[25]It is critical, therefore, that as new geographies enter the REE supply chain, they do so in a way that is sustainable, low-impact and backed by the necessary legal regimes.

Fig 3: Global REE production and reserves in 2019 (data from US Geological Survey, 2019)

Australia

Australia began producing REEs in 2013, rapidly scaling up to become the world’s second-largest producer by 2019. A handful of companies are undertaking feasibility studies for further mining projects, which could add a further 1.6 kt/year of production capacity.[26]

India

India was a relatively early entrant in the REEs market. Indian Rare Earth Limited (IREL), a public sector enterprise, was established in 1950. However, rare earth mining was halted between 2004 and 2011 due it being economically unfeasible and was replaced by cheaper REE imports from China.[27]Following the tightening of REEs exports by China in early 2011, IREL resumed its mining operations, backed by a partnership with Japan’s Toyota Tsusho.[28]In India, monazite is the principal source of REEs, and while it has abundant reserves of REEs, its potential remains untapped.[29]While it accounts for around 2 per cent of global production, India is home to 6 per cent of global reserves. Additionally, the Geological Survey of India (GSI) is researching cost-effective extraction methods and exploring the feasibility of extracting REEs from Arabian Sea sediments.[30]

Vietnam

Vietnam is home to the world’s third-largest reserves of REEs. Vietnam, like India, was a beneficiary of China’s restrictions on REE exports, having received significant investments from Japan, South Korea, and Australia. Vietnam Rare Elements Chemical, a joint enterprise with Japan’s Keita Kodama, for instance, began a production project in 2014.[31]Decision 2427/QD-TTg, Vietnam’s Mineral Resources Strategy 2020, lays out further plans for exploration of rare earth mines and establishing international partnerships for exploration, mining, and processing of REEs.[32]

Semiconductors

Semiconductors are a class of crystalline solids – such as silicon and gallium arsenide – whose conductivity lies between that of conductors and insulators, hence the term.[33]The semiconducting material to look out for in the future is gallium nitride (GaN), which may see growing importance as a component of 5G cell sites.

Semiconductor devices are electronic circuit components that are important components in electronic systems, including memory, processors, and sensors. While ‘semiconductor’ as a term is used for both the materials themselves as well as the devices made from them, the remainder of this section will use the term to describe the latter, unless stated otherwise.

The global semiconductor market nearly quadrupled between 1998 and 2020, growing from USD 125.6 billion to a forecasted USD 426 billion.[34]AI-related semiconductors alone are expected to grow at a CAGR of 50 per cent between 2019 and 2022.[35]Mobile semiconductors, meanwhile, are expected to grow at a CAGR of 7.49 per cent between 2020 and 2025, although economic slowdown in the wake of the pandemic will likely mute this growth.[36]

Going through the life stages of semiconductor manufacturing provides key insights into a country’s place in GVCs. Quartz and silica sands, for instance, are one of the fundamental raw materials that eventually go into semiconductors. The United States is the world’s largest exporter of silica sands (36.1 per cent), followed by Australia (11.2 per cent). Silica sands are, like rare earths, fairly abundant but also environmentally hazardous to extract.

Silica sands are refined to obtain silicon dioxide. The major exporters (in terms of value in USD) are China (22.8 per cent), Germany (17.4 per cent), and Japan (9 per cent), while major importers are United States (8.41 per cent), Germany (7.14 per cent), and China (6.98 per cent).[37]

The world’s top 10 semiconductor foundries, also known as fabrication plants or fabs, are concentrated in Taiwan and China:

Taiwan Semiconductor Manufacturing Company Limited (TSMC): Taiwan, ROC

United Microelectronics Corporation (UMC): Taiwan, ROC

Globalfoundries: US

Samsung Electronics: South Korea

SMIC: China, PRC

Powerchip Technology: Taiwan, ROC

Towerjazz: Israel

Fujitsu Semiconductor: Japan

Vanguard International: Taiwan, ROC

Shanghai Huahong Grace Semiconductor: China, PRC

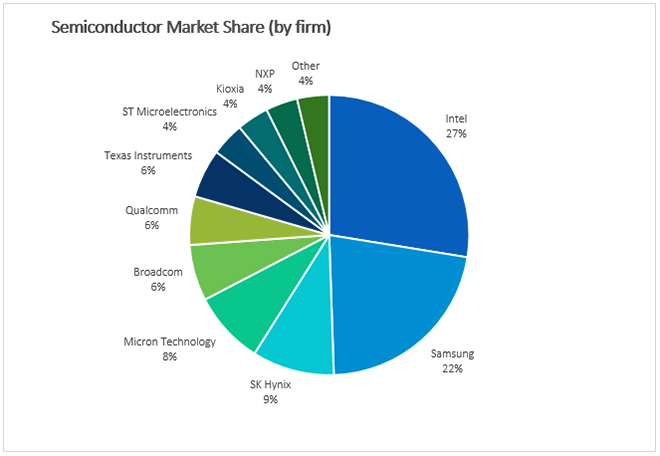

However, the biggest of these – TSMC, UMC, Globalfoundries and SMIC – are all ‘Pure Play foundries’, i.e. they do not design semiconductors, but only manufacture them under contract. Hence, the final share of the semiconductor market is dominated by firms based in the United States.

Fig 4: Global semiconductor market share (based on data from Gartner)[38]

As a result, the supply chain for semiconductors suffers from two major setbacks. First, two semiconductor vendors, Intel (US) and Samsung (South Korea), account for nearly half of global revenue. Second, the supply chains for semiconductors are heavily specialised – lean but brittle – characterised by ‘bottlenecks’ that, if disrupted, risk the collapse of the entire chain. A handful of countries – US, South Korea, Japan, Taiwan, and China – dominate different stages and components.[39]

The twin pressures of the US–China trade war and the COVID-19 pandemic have exposed many of these flaws in the supply chain, but also created opportunities for countries in the Indo-Pacific who are looking to reap the benefits of a semiconductor supply chain shift and are angling themselves as the next favoured destination for semiconductor foundries.

Cambodia

Cambodia’s electronics exports constitute around 3 per cent of its total export value, and its place in the GVCs for semiconductors is restricted to assembly of electronic components such as semiconductor wafers, integrated circuits, and bare circuit boards.[40]Cambodia has been a recipient of Japanese investment in electronics manufacturing: Khmer Semiconductor (founded 2012), Cambodia’s first semiconductor manufacturing enterprise, is a joint venture with semiconductor manufacturers in Japan.[41]

India

India is a massive consumer of electronics. In 2018, for instance, its electronics and machinery imports stood at USD 96.5 billion, or 19.6 per cent of its total imports. By 2025, the Indian semiconductor component market alone is expected to reach USD 32.35 billion.[42]

Today, India is home to a handful of semiconductor firms. For instance, the Bangalore-based SmartPlay Technologies specialises in semiconductor design, and Invecas provides assembly and testing services, in partnership with TSMC and Globalfoundries.[43]The Defence Research and Development Organisation established the Society for Integrated Circuit Technology and Applied Research with the aim of providing integrated circuit design for strategic and security systems.[44]

The Government of India identified the need to build a domestic fab facility a decade ago. The then Department of Electronics and Information Technology (DeitY) invited expressions of interest (EOIs) for the setting up of semiconductor fabs in 2011.[45]Consequently, Hindustan Semiconductor Manufacturing Corporation (HSMC), a consortium of companies including ST Microelectronics and Silterra, was established with the aim of building the country’s first wafer fab in the state of Gujarat.[46]The project has, however, faced several delays. India’s 2020 budget has given a fresh boost to this indigenisation effort with proposed schemes to incentivise electronic manufacturing in the country.[47]

Indonesia

Indonesia’s semiconductor industry consists primarily of assembly facilities established by foreign companies such as Linde (Germany), which processes gas and chemicals for semiconductors, and Panasonic (Japan).[48]

Recognising this gap, the Making Indonesia 4.0 strategy, released in 2018, outlines as one of its aims taking Indonesia’s electronics sector from low-tech assembly to high-tech, high-value exports.[49]It identifies reliance on imports for key components like semiconductors as a challenge. Concurrently, Jakarta is also looking to attract more semiconductor manufacturers to Indonesia, courting companies from Taiwan and elsewhere.[50]

Malaysia

Malaysia houses operations of several global semiconductor companies and has also built its own enterprises including the state-owned SilTerra, which offers both foundry and design services, First Elterra and Symmid, both fabless semiconductor companies, as well as a host of pure play foundries.[51]

The Malaysian Investment Development Authority (MIDA) has begun to offer incentives for design and development (D&D) activities in the electronic industry, including for ‘higher value’ activities in integrated circuit design packaging.[52]

Singapore

More than 200 semiconductor companies operate in Singapore – a mix of foreign-owned, joint ventures and home-grown companies, including both pure play foundries and fabless facilities. In 2019, the semiconductor industry constituted 7.8 per cent of the country’s GDP.[53]

Even as its economy shrunk in 2019–20, hit by the US–China trade war and the COVID-19 pandemic, the semiconductor industry in Singapore saw ‘stronger than expected demand’, buoyed by demand based on 5G, cloud services, and data centres.[54]

Vietnam

Vietnam became a favoured destination of a wave of reshorings from China to Vietnam for electronic manufacturing, and other labour-intensive industries starting in the mid-2000s, a trend accelerated by the US–China trade war.[55]In 2006, for instance, Intel announced plans to build a USD 300 million semiconductor assembly and test facility in Ho Chi Minh City and, in 2019, Seoul Semiconductor announced plans to move 60 per cent of its production to Vietnam.[56]The semiconductor market in Vietnam is forecast to grow by USD 6.16 bn during 2020–24 at a CAGR of 19 per cent.[57]

Much of the semiconductor industry in the country is in ‘low-value’ assembly activities, such as the Intel plant. Consequently, in a bid to move up the value chain, the Vietnamese Government has pushed for building domestic semiconductor fab capabilities, investing USD 300 million in the country’s first wafer fab in Saigon Hi-Tech Park.[58]Between 2013 and 2020, the Ho Chi Minh City Integrated Circuit Development Programme researched and promoted investment in ‘minimal fab’, a low-cost, low-capital alternative to existing fab methods.[59]

Key Takeaways

The US–China imprint is prominent in REEs and semiconductors. In REEs, China’s edge lies in the massive volumes of investments poured into extraction and processing, a short-term cost that was untenable for India and Vietnam, both of which possess sizeable untapped reserves. India, Australia, and Vietnam are, however, undertaking feasibility studies, re-opening defunct projects, and injecting investment into this area in view of its increasing strategic importance.

Most high-value activities like semiconductor design or integrated device manufacture (design and assembly) remain heavily concentrated in the United States. Consequently, the countries under study primarily specialise in ‘pure play’ foundries that supply services to semiconductor giants based outside their borders. Nevertheless, India is home to a handful of semiconductor design firms, including those in the defence sector, and Singapore is a major semiconductor manufacturing hub, with over 200 fabless and pure play manufacturers operating in the city-state. Malaysia, Indonesia, and Vietnam are all incentivising semiconductor manufacture and India too is off to a sputtering start on its ambition to build a full semiconductor fab facility.

Digital Economy and Adoption

The Indo-Pacific region is home to some of the largest digital economies in the world. The focus countries (India, Australia, Cambodia, Indonesia, Malaysia, Singapore, Vietnam, ) are home to a fifth of the world’s internet users, accounting for nearly 1 billion people online. The total size of the digital economies in the region stands at nearly USD 400 billion, with India commanding half the share,[60]followed by Australia at USD 122 billion[61]and Indonesia, Malaysia, Singapore, and Vietnam collectively at USD 75 billion.[62]In the Southeast Asia (SEA) region, Indonesia and Vietnam are pacesetters with annual growth rates at over 40 per cent.[63]

SEA and India are witnessing a rapid growth in their internet user bases. Indonesia and India have the fastest digital adoption growth rates amongst 17 major digital economies in the world.[64]India has added over half a billion internet users since 2013 and, as of December 2019, the country has 718.74 million internet subscribers.[65]Furthermore, users in SEA and India spend a significant time on the internet, and the average amount of time spent per day exceeds the global average.[66]Indian mobile data users consume an average of 10.4 GB of data each month,[67]and this is growing at an annual rate of 171 per cent – more than twice the growth rates in United States and China.[68]Internet speeds in the region – both mobile and broadband – exceed 10 Mbps,[69]which is considered as the ‘minimum speed required for consumers to fully participate in a digital society’.[70]Most of the region’s users connect to the internet primarily through their mobile phones.

Driving Factors: Digital Economy and Start-up Ecosystems

A highly connected and growing internet community coupled with changes in consumer behaviour has led to the mushrooming of several digital businesses and start-ups that have propelled extraordinary growth in the region’s digital economies.

Rising Consumerism

The region’s digital economies, particularly India and SEA, have been propelled by the rise of the e-commerce, ride-hailing, food delivery and hyperlocal service sectors.[71]

In SEA, e-commerce is the biggest sector . Within four years, it grew sevenfold, from USD 4.1 billion to USD 31 billion, and is projected to reach USD 123 billion by 2025. Ride-hailing is the second-best performer in the region with a booming food delivery sector.[72]Similarly, in India, e-commerce, consumer services (hyperlocal delivery) and transport tech (ride sharing and food delivery) featured in the top four most funded sectors – together making up 43 per cent of the total funds raised.[73]In India, a rise in consumerism due to a burgeoning middle class with increasing expendable incomes led to a mammoth wave of activity in these sectors.[74]On the other hand, with a modest population of 24.6 million, Australia’s business to consumer e-commerce has been driven by a ‘healthy economy and strong internet infrastructure rather than a high volume of customers’.[75]The sector has had a double-digit growth rate over the last few years and is worth USD 33.1 billion.[76]However, the majority of Australians buy from overseas and cross-border e-commerce generates more sales than domestic retail e-commerce.[77]

The Fintech Boom

The rise of e-commerce and internet-based services has led to a rapid adoption in digital payments. Australia, India, and Singapore have a thriving fintech landscape. Fintech adoption is being led by India at 87 per cent in 2019. This is followed by Singapore and Australia, which recorded adoption rates of 67 and 58 per cent respectively.[78]

In India, three factors have resulted in a fintech boom: 1) the creation of favourable regulatory environment;[79]2) the launch of the Jan Dhan Yojana scheme that resulted in 405 million entering the formal banking system across India;[80]and 3) the United Payments Interface (UPI), an open and interoperable architecture that enables instant real-time payments between bank accounts using smartphones. In August 2020, UPI clocked 1.62 billion transactions, cumulatively worth ₹2.98 trillion (USD 40 billion).[81]The ‘open rails’ system of the UPI has lowered entry barriers for new businesses. Innovative business models that extend credit and insurance based on cash-flows have also taken root.[82]To this end, fintech is the second highest-funded start-up sector in India, raising USD 10.32 billion since 2014.[83]

With the financial sector delivering a significant part of Australia’s economic growth in the last three decades,[84]the sector has been quick in embracing the digital pathway. Roughly 650 fintech companies are based or operate in Australia,[85]and two of the three unicorns (Airwallex and Judo Bank) in the country belong to the fintech sector.[86]In 2018, Australia launched the New Payments Platform (NPP) and Fast Settlement Service (FSS), which together enable real-time payments between customers of different financial institutions.[87]While the NPP’s roll out has been roadblocked by delays, it witnessed a rapid growth in the second half of 2019, processing an average 1.1 million payments per day with a total value of USD 700 million.[88]The NPP coupled with the Open Banking initiative – enabling the safe transfer of banking data to accredited third parties – are expected to open a range of new functions through overlay services, enable innovative capabilities, and spur competition amongst financial service providers.[89]

In the SEA region, with the rapid growth of e-commerce, digital payments are growing in a double-digit range.[90]However, digital lending is nascent, and a significant portion of the population in Vietnam and Indonesia remains unserved. Moreover, with a fragmented landscape, clear leaders are yet to emerge.[91]In 2018, the ASEAN Financial Network launched the API Exchange (APIX),[92]an online marketplace and sandbox for fintech APIs that will allow financial institutions and fintech businesses to find partners[93]and discover innovation for SEA and the world.

Start-up Ecosystems

Digital innovations in the region are being powered by start-ups and several young entrepreneurs. The Indo-Pacific region is home to a total of 55,200 start-ups as of 2020. India is home to 72 per cent of these, followed by the SEA region at 24 per cent and Australia hosting a modest 4 per cent.[94]

India’s start-up ecosystem is the third largest in the world and has cumulatively raised USD 63 billion in funding since 2014.[95]Apart from a large consumer market, the ecosystem has also immensely benefited by piggybacking on the expertise and R&D infrastructure made available by India’s robust software and IT services industry. The country is home to the third highest number of unicorns (35) in the world,[96]some of which have expanded aggressively in the Indo-Pacific region.[97]

As of 2018, the SEA region was home to 13,500 technology start-ups, of which two-thirds were based in Singapore and Indonesia – accounting for 34 per cent and 31 per cent respectively.[98]The 50 most funded digital start-ups in SEA all had their origins from the four focus SEA countries under study.[99]

In both India and the SEA region, hyperlocal and regional start-ups have displayed tremendous success. In India, regional players like Flipkart (now acquired by Walmart), Ola, Swiggy, Zomato, and PayTM have competed strongly against well-funded and mature global players like Amazon, Google, and Uber – unlike their Chinese counterparts that grew in a protected market.[100]Similarly, Grab, the biggest unicorn and ride-hailing company in the SEA region (based in Singapore), acquired Uber’s business in the eight SEA countries it was present. This also included the acquisition of Uber Eats.[101]

SEA’s digital start-ups are expanding regionally through intra-ASEAN investments, and mergers and acquisitions. Apart from contributing to innovation, digital commerce and operations of major players are significantly advancing/strengthening intraregional investments and connectivity.[102]Moreover, major players, by the virtue of their large consumer bases, are expanding their portfolio of services on their platforms by entering new sectors. For example, Grab, has diversified into financial services. Similarly, Indonesia-based ride-hailing unicorn Gojek operates in Singapore, Thailand, and Vietnam, and offers more than 18 services including financial and lifestyle services.

The Indo-Pacific App Economy

With rapid digital adoption rates and extremely high online engagement (in terms of time spent), the digital population in the region is increasingly frequenting mobile apps to run their personal and professional lives – whether it be to socialise, order food, watch movies, track their health, play games, communicate, learn, manage finances, access to government services and information, or improve productivity. Apps also represent the first ‘truly global market’ for digital goods, as they can be produced and accessed anywhere across the globe through an internet connection.[103]Consumer apps collect significant behavioural data of users to provide targeted and personalised services. This also opens potential room for malicious actors to exploit end users. The invasive nature of apps has come under scrutiny across geographies, and countries are trying to respond with appropriate measures. Understanding the app economy of the region thus becomes crucial.

In all case countries, WhatsApp, Facebook, Facebook Messenger, and Instagram featured in the top three to five apps in terms of monthly users. In Australia, US-based mobile apps were widely used and Singapore had good mix of US and locally made apps (see Annexure). However, amongst the rest of the countries, apps made in China also featured in the top 10.[104]Chinese companies featured in the top app companies in the region and outnumbered local and US companies in India, Malaysia, and Indonesia. TikTok, an entertainment app by Chinese firm ByteDance, which has been a major source of controversy and discussion in national security debates, featured in the top 10 apps in terms of downloads in 2019 in all countries. The App Annie ‘State of Mobile’ reports of 2019 and 2020 indicate a strong increase in popularity in Chinese-made applications in the region.[105]

Chinese internet companies are (1) subject to the country’s 2017 National Intelligence, 2014 Counter Espionage, and 2016 Cybersecurity laws that mandate data sharing with the government under secrecy for national security and intelligence,[106]and (2) have close ties with the Chinese Communist Party (CCP) through the presence of party committees in respective companies.[107]This creates a concern that these companies act on the behest of mandarins in Beijing. ByteDance, on its TikTok app, is said to have censored anti-China content in Indonesia from 2018 to mid-2020.[108]It is alleged that a former government official ran TikTok’s content policy globally.[109]A study by the Australian Strategic Policy Institute analysed the growing global censorship on WeChat and TikTok (with 700 million global users) and the covert control of information flows globally by parent companies Tencent and ByteDance.[110]

The United States has banned WeChat and TikTok under national security concerns.[111]India, in the aftermath of border clashes with China in June 2020, banned 117 Chinese mobile applications citing the concern that the apps ‘engaged in activities which is prejudicial to sovereignty and integrity of India, defence of India, security of the state and public order’.[112]

The recent clarion call of the CCP to realise leadership over the private sector, mandating companies to maintain conduct in accordance with party ideologies and policy objectives, further blurs the lines between the state and enterprise and exacerbates concerns over the security of apps by Chinese internet companies.[113]

The increasing popularity of Chinese apps and their respective security concerns highlight the need for robust data protection and privacy regimes for the fast-growing digital economies in the region.

Investments in the Digital Indo-Pacific

As Chinese apps have penetrated the region, so to have their investments. China’s economic success coupled with the rise of major internet companies and venture capitalists (VCs) have led to a significant outflow of investments into various digital economies globally. The Indo-Pacific region’s digital economies have been important beneficiaries of Chinese investments. This section aims to take a deep look into Chinese investments in the region and juxtaposes them with investments from other regions.

India

Over the period 2014-2020, Chinese investments in India’s tech sector stand at an estimated USD 4 billion. As of March 2020, 18 of India’s 30 unicorns have been funded by Chinese investors. Over two dozen Chinese technology companies and funds have made investments in India.[114]Alibaba and Tencent together command investments that exceed over USD 3 billion, and have been the two biggest investors in the country followed by Xiaomi.[115]

Alibaba, along with its affiliate ANT Financial, first led the way with a USD 680 million investment in One97 communications (parent company of PayTM with over 350 million users in India) for a 40 per cent stake. Alibaba’s portfolio includes investments in BigBasket (online grocer), SnapDeal (e-Commerce), Zomato (restaurant aggregator and food delivery), Xpressbees (logistics), and TicketNew (online ticketing platform).[116]

Tencent is the biggest investor in India’s tech space and has a diverse portfolio ranging from transport (Ola), food delivery (Swiggy), social media (Hike Messenger), gaming (Dream11 Fantasy), education (Byju’s), health (Practo) to music streaming (Gaana) and news aggregation (News Dog). Its biggest investment of USD 700 million was in India’s leading e-commerce platform Flipkart.[117]Xiaomi, and its affiliate investment firm Shunwei Capital, have a total portfolio of USD 500 million spread across several smaller investments. In 2018, prior to India banning Chinese apps, 44 of the top 100 most downloaded apps were made by Chinese companies.[118]

Southeast Asia

While there does not exist a comprehensive study on Chinese investments in the digital economy in SEA, preliminary evidence suggests Chinese technology companies are significant investors in SEA’s major unicorns.

Didi Chuxing is a major investor in Grab, a Singapore-based ride-hailing company.[119]Alibaba has made significant investments in two major e-commerce players: acquiring Singapore Lazada for USD 4 billion and investing USD 1.1 billion (along with Soft Bank) in Indonesia-based e-commerce Tokopedia.[120]Indonesian ride-hailing firm Go-Jek raised nearly USD 3.7 billion across three rounds that were led by Tencent along with other investors that included Google, JD, and Blackrock.[121]Apart from this, in 2017, Chinese investors and technology companies were active investors in SEA’s fintech sector. Twelve of the top 50 most funded fintech start-ups in 2017 had Chinese investments.[122]

Australia

Chinese companies do not have a major presence in Australia’s technology sector.[123]According to media reportage, there exist only two investments by a major Chinese technology company. Tencent has invested in two fintech start-ups: USD 13 million in Airwallex[124]and USD 300 million in Afterpay.[125]

Comparing Investments

In India, Chinese investments since 2014 in the start-up and technology sectors are considerably low when compared to investments from US and Japanese counterparts. While the US and its private sector have played a key role in building India’s software industry since 2000. Since 2014, US investments, in India’s start-up and technology sector alone stand at roughly USD 30 billion.[126]Japanese investors have also actively invested in India’s start-up economy since 2014 and funnelled in nearly USD 12 billion, with SoftBank alone investing nearly USD 10 billion.[127]

ASEAN presents a similar picture (see Table A.2 in Annexure). In the information and communications sector, intra-ASEAN investments are the highest. Between 2015 and 2018, they stood at roughly USD 3.8 billion. This was followed by inflows from Japan and Hong Kong that stood at roughly USD 1 billion each, the European Union at USD 825 million, and the US at USD 367.6 million. The least was from mainland China at around USD 200 million.

While Chinese investments are not significant when compared to other investors in the region, their footprint is the region is patchy yet increasing. While some hold majority stakes and have acquired top companies, the others have significant yet not majority investments.

While there is concern around the security of Chinese apps and potential investments, it is in the region’s interest to benefit from Chinese capital. However, it is also important to have necessary regulations to ensure a particular country or actor does not dominate the digital economy. strong foreign direct investment (FDI) rules that support competition is important.

According to the World Bank’s Worldwide Governance Indicators, countries in the Indo-Pacific region, barring Australia, Singapore, and Malaysia, score low on regulatory quality, rule of law, and control of corruption.[128]In particular, Cambodia, Lao PDR, Myanmar and Vietnam perform poorly in all of these indicators compared to their peers in the ASEAN region. Control of corruption has particularly deteriorated and regulatory quality is a problem. Cambodia faces challenges regarding judicial independence and enforcement of law. Vietnam, on the other hand, needs to work on simplifying an ‘overcomplicated, restricted and unclear licensing and regulatory environment’.[129]

Investors from countries with higher levels of corruption find it easy to negotiate with officials from countries that have similar corruption levels. This adversely impacts the quality of investments, and positive spill overs from such foreign investments are less likely to occur thereby making it difficult for countries to foster innovation and create socioeconomic benefits.[130]

Countries in the region are embracing digital technologies to solve the hard problems endemic to their contexts. Hyperlocal innovation is touted to thrive, and this requires patient, committed, and strategic financing, which is often difficult to find from within the region. With the world’s economic centre of gravity increasingly moving towards the Indo-Pacific region, finance from the developed and capital-intensive parts of the globe is being increasingly deployed. It is in the interest of the region to foster stronger institutions and rules to generate the best value from such investments.

The 5G Conundrum

The future of the digital economies of the region hinges upon advances in wireless communications technology – especially 5G.[131]With its significantly higher speeds, capacities, and ultra-low latency, 5G will power emerging technologies such as AI, robotics, quantum computing, and internet of things (IoTs) to unlock a host of opportunities across sectors that can enable sweeping socioeconomic transformations across the globe.[132]Given that countries in the region continue to invest significant resources for the provision of social infrastructure, 5G can be a game changer and countries in the region are keen on deploying it.

However, it has emerged as a critical flashpoint in global geopolitics today. 5G’s superior ability to support advanced technologies and critical infrastructures of countries can allow suppliers/vendors of 5G to potentially dominate a given country’s data economy. Currently, Chinese telecommunications giant Huawei Technologies Co., Sweden-based Telefonaktiebolaget LM Ericsson (Ericsson), and Finland-based Nokia Corporation (Nokia) are the competitors for supplying end-to-end 5G equipment.[133]Amongst them, Huawei leads the pack with the most affordable and technologically advanced (in terms of number of patents) technology.[134]In the backdrop of the ongoing economic and technological rivalry between the US and China, the question of 5G vendor choice has thus become a critical issue. Western countries have raised their concerns on Huawei’s opaque ownership structure, close ties to the Chinese Communist Party (CCP), and the potential subversion of the independence of data regimes to Beijing if Huawei’s equipment is deployed.[135]This has therefore presented a dilemma for countries in the region that all have close economic linkages with China: either ban Huawei and face potential repercussions from China or deploy Huawei and face potential retaliation from the US in the realms of technologies in which it will continue to be a leader for the foreseeable future.

Table 1 captures the responses of the countries under study. Currently, only Australia and Singapore have begun to deploy 5G in their telecom networks.

Table 1: The State of 5G in the Indo-Pacific

Country

Current Status of 5G

Position on Huawei

Indigenous Alternatives

Official Policy

Other Notes

Australia

Deployed

Ban

No

Yes | ‘5G—Enabling the future economy’ launched in 2017 by Australian Department of Communications and the Arts

Banned ‘high-risk vendors’ in August 2018 and allayed concerns on vendors who could be subject to extrajudicial directions from foreign governments. Huawei Australia later confirmed that both Huawei and ZTE were banned.

Singapore

Deployed

Contract not awarded despite inclusion in trials

No

Yes | 5G Vision prepared by Infocomm Media Development Authority (IMDA) – a statutory board under the Ministry of Communications and Information.

Nokia and Ericsson chosen as vendor after involving Huawei for trials.

Indonesia

Trials

Allowed for trials

No

No

Following a multi-vendor model.

India

Trials to start

Allowed for trials | Unlikely to be used

Yes

No

Trials yet to start. Local telecom major Reliance Jio recently tested, 5G solution developed with Qualcomm.

Vietnam

Trials

No official statement | Unlikely to be used

Yes

No

So far trials carried out with Nokia and Ericsson. No official statement banning Huawei. State telecom provider Viettel is developing indigenous 5G hardware and software.

Malaysia

Trials

Allowed for trials

No

Formed a National 5G Task Force that released a report in December 2019

5G spectrum allocated to five companies through backdoor mechanisms. Four of five countries were to partner with Huawei. Spectrum allocation revoked in June 2020.

Cambodia

Trials

MoU signed by government to build 5G infrastructure. ZTE to be involved as well

No

No

Cellcard to partner with ZTE, Metfone to partner with Huawei, Smart Axiata to partner with Huawei.

While Australia has banned Huawei and ZTE from providing its 5G technology,[136]Singapore has gone ahead to deploy 5G without Huawei[137](despite involving them in trials)[138]Ericsson and Nokia were respectively chosen as vendors by Singtel and StarHub-M1.[139]

The remaining countries under study are conducting trials for deploying the technology. Cambodia has openly embraced the use of Chinese technology. Malaysia, which had allocated 5G spectrum to five telecom companies by bypassing tenders, recently revoked the contracts due to ‘technical and legal issues, and the need to follow a transparent process’.[140]Four of the five companies were planning to use Huawei as a vendor for 5G infrastructure.[141]

On the other hand, Indonesia, Vietnam, and India have been ambiguous about using Huawei. India has allowed Huawei to participate in 5G trials despite banning 117 Chinese mobile applications and ordering state-owned telecom companies to stop sourcing gear from Chinese companies.[142]Recently, homegrown telecom major Reliance Jio successfully tested 5G solutions with Qualcomm.[143]Indonesia has allowed Huawei for 5G trials[144]and most telecom companies in the country are following a multi-vendor model.[145]Officials and telecom companies have not ruled out partnering with Huawei and are not in a ‘rush’ to adopt 5G.[146]While Vietnam has not issued any official statement on Huawei, major telecom carriers are exploring options other than Huawei by conducting trials with Nokia and Ericsson.[147]The country, through its state-owned telecom company, Viettel, operated by the country’s military, claimed to have developed indigenous 5G technology and plans to begin mass production of software and hardware this year.[148]

Against the backdrop of a technology war and security concerns over 5G, the choices of 5G vendors by countries in the region might also determine the standards adopted and thus the interoperability of technologies across borders. This in turn will impact the extent to which integration and connectivity can be fostered within the region’s digital economies.

Inclusive Digital Transformation

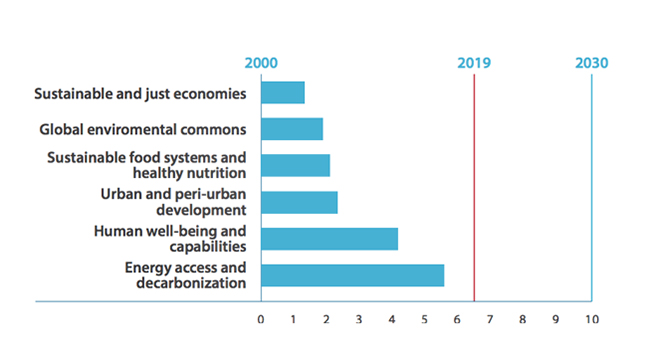

The Asia-Pacific region is witnessing a digital transformation boom, poised to accelerate due to the technology-biased disruption caused by the COVID-19 pandemic. However, the goals of increased regional resilience and connectivity advocated by this paper cannot just be predicated on increased digital economy growth and greater export sophistication. Resilience requires inclusive and broad-based growth, which implies a shift away from technological determinism to people-centric growth. With this in mind, the region committed to the framework set out by the Sustainable Development Goals (SDGs) in 2015, which binds the region to a sustainable growth trajectory, seeking to ensure ‘no one is left behind’.[149]

Fig 5: The Asia-Pacific region’s progress towards the Sustainable Development Goals[150]

Emerging technologies possess considerable scope to reduce traditional barriers to connectivity and knowledge sharing.[151]However, technology diffusion requires systematic, context-specific policy interventions and strong institutions as well as broad-based capabilities. Broad-based digital transformation will fundamentally entail:

A) Inclusive and high-quality internet access.

B) Capacity: hard and soft infrastructure.

C) Digital literacy and capabilities.

Inclusive, High-quality Internet Access

The Asia-Pacific remains one of the world’s most digitally divided regions.[152]Nearly 52 per cent of the region is still offline, according to the UNESCAP, which believes that the pandemic could render the digital divide ‘the new face of inequality’ in the region.[153]

Digital accessand adoption continue to be determined largely along the axes of class, gender, and race. Poverty persists in the region despite high economic growth: about 400 million people still live in extreme poverty (below USD 1.90 a day), and this number is expected to inflate considerably due to the impact of the COVID-19 pandemic.[154]Inequality is also sharply escalating: the Asia-Pacific has seen income inequality rise by over 5 per cent since 2000.[155]Indonesia, India, and China have seen a spike in the Gini coefficient, as has Vietnam (the country’s 210 super-rich people reportedly earn enough annually to lift 3.2 million out of poverty).[156]Cambodia has also reported a 4 per cent increase in income inequality from 1990–2008.[157]Australia is contending with very high wealth inequality (income inequality is low in the country).[158]Singapore and Malaysia, on the other hand, have registered significant improvement on this front, with Singapore’s Gini coefficient falling to 0.452 in 2019 (its lowest since 2001) and Malaysia’s falling to 0.40 in 2016.[159]

Gender equalityis an area in which the region is particularly lagging. Countries are still struggling with first-order issues like violence against women, which are compounded by the digital gender divide and growing precariousness of work. The ratio of female-to-male labour force participation in the region has deteriorated from 0.67 in 1990 to 0.61 in 2015. India’s numbers are especially alarming in this regard – it has the lowest female labour force participation rate at 20 per cent.[160]

According to GSMA’s 2020 Mobile Gender Gap report,[161]India (20%) and Indonesia (10%) have particularly large gender gaps in terms of mobile ownership and internet use. This is especially significant as two-thirds of the countries’ internet users access the internet on their mobile phones.[162]The South Asian region has the largest mobile gender divide, with women 28 per cent less likely to own a mobile phone and 58 per cent less likely to use mobile internet; whereas in East Asia, the numbers are 1 per cent and 4 per cent respectively. It is not just barriers like affordability and lack of skills that are responsible for the digital gender divide, but also social and cultural norms that inhibit women’s participation in the economy.

There is not enough reliable data available for the Asia-Pacific region to elaborate upon the racial and ethnicity digital divide; however, anecdotal evidence and a few studies in the US and Japan have indicated that discrimination on the basis of race and ethnicity carry over into the technological domain, determining access to technology and infrastructure more generally.[163]

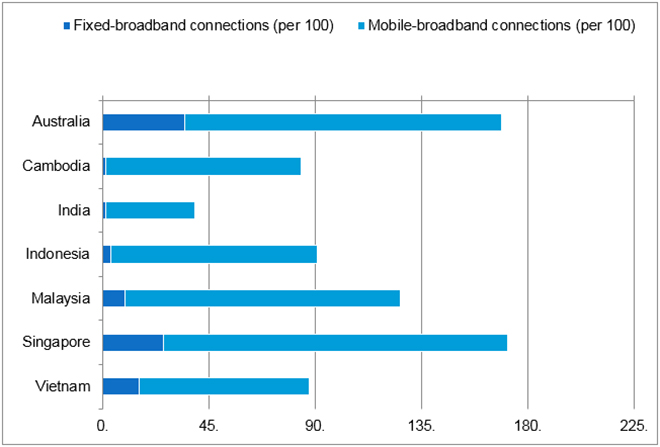

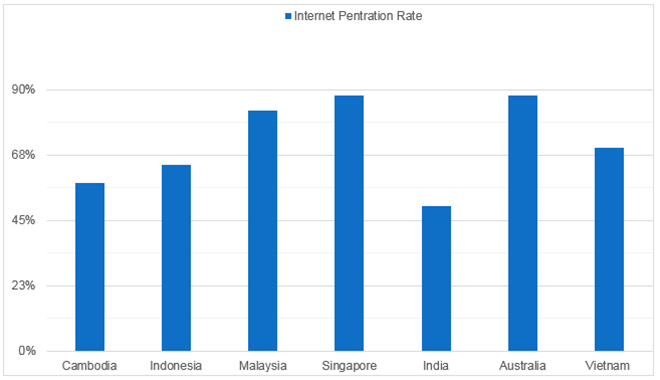

There remains considerable untapped potential in terms of access to the internet, even in what is the fastest growing regional internet user base in the world. Mobile internet penetration is very high in the region, but internet uptake is quite low. The graph below (Figure 6) demonstrates theheterogeneity of internet accessin the region. While Singapore, Australia, and Malaysia have high rates of internet penetration, much of Cambodia, Indonesia, and especially India (which stands out for its relatively dismal 50 per cent internet penetration rate) is not connected to the internet.

Fig 6: Internet penetration rate in case countries

In Cambodia, internet penetration is especially high in the age group of 15–25 (86%), but the country needs to focus more on its below-15 age group.[164]India’s and Indonesia’s internet penetration is geographically driven, with the poorer rural regions having lower penetration compared to the cities.[165]Both Indonesians and Indians spend quite a lot of time on the internet, and use social media and e-commerce heavily – their social media usage is among the highest in the world – and therefore an expansion in the market holds significant potential for the internet economy.[166]Indonesia could benefit from the speedy allocation of digital dividend to mobile broadband services; effective spectrum allocation will help expand network coverage and improve internet penetration in rural sections.[167]India requires significant infrastructure investment and public–private partnerships to expand access to rural areas – its BharatNet program is an endeavour towards this end.

High-speed internetis still beyond the reach of many in the region. Increased broadband connectivity is conducive towards greater digital adoption and productivity in the region; in low- and middle-income countries in particular, analyses have shown that a 10 per cent increase in broadband-penetration creates a 1.38 per cent boost in economic growth.[168]Access to high-speed broadband varies across the region. Figure 8 provides a nuanced picture.

Fig 7: Broadband connections in the Asia-Pacific region (adapted by the author from World Bank data and the WEF Global Competitiveness Report 2019)

Internet usage in Indonesia, Cambodia, and India is largely reliant on mobile-cellular data, which provides unreliable and patchy coverage, with very low-take up of broadband. India’s broadband download speeds, along with Indonesia, Cambodia and Vietnam’s are all below the global average.

India’s mobile download speeds are also woeful (12.08 Mbps, well below the global average of 34.51 Mbps), as are Indonesia’s (16.94), Cambodia’s (17.54), and Malaysia’s (24.44), though Vietnam is doing considerably well on this count and is at the global average.[169]Australia’s broadband download speeds (53.36 Mbps) are also below the global average (85.72Mbps),,behind peers Singapore (213.18 Mbps) and Malaysia (86.82 Mbps). Telecom Cambodia has signed an MoU with Chinese-owned Seatel, which has invested USD 300 million into developing fibre-optic cable networks in Cambodia. Smart Axiata – a Cambodia company – is collaborating with Huawei for 5G network development in the country.[170]

Priceis also an important barrier for technology adoption and access in the region. Broadband is prohibitively expensive in Cambodia with a fixed-broadband basket costing 10.4 per cent of GNI per capita, as well as in Indonesia, at 8.7 per cent of GNI per capita. Malaysia and Australia are also encumbered by a lack of affordable broadband.[171]Most of the region still accesses the internet through their phones. Even as internet subscription costs have become increasingly affordable in the region, they remain prohibitively high for a large chunk of the region still living in extreme poverty (likely to exacerbate due to the pandemic). This problem therefore requires a systemic solution.[172]

Finally, an underestimated component of access is therelevance of contentand theissue of language.A whopping 85 per cent of user-generated content on Google currently originates in the West.[173]The market is skewed towards big technology firms, and local content creators face formidable barriers ranging from high content creation costs, lack of capability, costs of translation, and relative lack of revenue generation potential from ads and subscriptions.. Buoyed by the power of network effects, big technology firms based in a handful of countries have become the ‘gatekeepers’ of content.

A large majority of languages are virtually absent on the internet: 80 per cent of online content today is written in just about 10 languages. English is the language of the internet, and the dominance of a few languages impedes broad-based regional connectivity.[174]Increased demand in the digital economy will be driven by relevance of content and greater awareness and knowledge of the opportunities presented by the internet.[175]This will require considerable effort towards investing in an internet of the people, as well as for the people of the region.

Capacity

Infrastructure is a public good, and innovation and regional connectivity require both physical infrastructure and an enabling ecosystem to flourish. The Indo-Pacific region is currently constrained by a massive infrastructure gap, in terms of both hard and soft infrastructure. TheAPEC Economic Policy Report 2019indicated that the APEC economies would need to spend USD 2 trillion annually from 2020–25 on infrastructure.[176]Infrastructure, therefore, needs to be a priority for the region, to foster an inclusive digital economy.

Hard infrastructureimplies logistics networks, transport infrastructure, telecommunication networks, undersea cables as well as the diffusion of old technologies like electricity that are the building-blocks of innovation economies.[177]

(1)Electricity access and high-quality supplyis a prerequisite for a modern economy. Singapore, Australia, Vietnam, and Malaysia face no trouble in this regard, placed at the technology frontier with 100 per cent of their population having access to electricity, even though the quality of Malaysia’s and Vietnam’s electricity supply is sub-par. However, there’s considerable scope for improvement in India (87.5 per cent of the population has access to electricity and very poor supply quality – ranking 108th in the world),[178]and it is also a serious issue for Cambodia (only 60.6 per cent of the population has access to electricity, and has poor quality of supply).[179]

Over 1 billion people within the Indo-Pacific region lack any access to electricity, which has had a large impact on their productivity and living standards. India needs to increase efficiency in power generation and transmission, and invest in digitalisation in order to have better grid stability and access to system intelligence, in order to bring about transparency and be able to map distribution networks to reduce electricity fluctuations and power outages.[180]Indonesia needs a little improvement with 94.8 per cent of the population having access to electricity and moderate electricity supply quality. In Cambodia, much of the power supply is concentrated in urban areas, which leaves the rural areas without access to sufficient grid electricity. Therefore, people in these areas are often forced to illegally purchase electricity at much higher prices and through unreliable infrastructure.[181]

(II) The countries in the region have varying capacities with respect totelecommunication systems.High-speed broadband and fibre connections are a requisite for greater productivity and increased digital adoption. However, currently only Australia (134.1 connections per 100 people) and Singapore have an adequate rate of fixed-broadband penetration and fibre-internet subscriptions are only just beginning to catch on. There is a need for regulatory reform for more players to emerge, and for telecom companies to invest more. Cambodia also requires a more transparent regulatory framework to benefit a larger chunk of the economy. Telecom Cambodia has signed an MoU with Chinese-owned Seatel which has invested USD 300 million into developing fibre-optic cable networks in Cambodia, and Smart Axiata – a Cambodia company – is collaborating with Huawei for 5G network development in the country.[182]

On the subject of undersea cables, Singapore is the forerunner and the most wired country in the world.[183]Vietnam has six submarine cable systems currently, and the somewhat-fragile Asia America Gateway handles 60 per cent of Vietnam’s international internet traffic.[184]Australia has also invested in undersea cables at a huge cost of USD 91 million.[185]

(III) Expensivelogisticsare a formidable barrier in SEA and India for cross-regional trade and connectivity – among the highest in the world.[186]This is due to both geographical and regulation reasons. The World Bank’s Logistics Performance index indicates that Vietnam (rank 39) and Malaysia (rank 41) need to work on customs procedures – Vietnam’s logistics costs are among the highest in the world, roughly 25 per cent of GDP.[187]India (rank 44) and Indonesia (rank 46) are performing poorly on customs procedures and logistics infrastructure, and Cambodia (rank 98) needs to work towards improving logistics competence, customs, and infrastructure capacity.

(IV) OnICT infrastructure, the GTCI ranks India very low (score of 24.43), along with Vietnam (39.06), Cambodia (31.55), and Indonesia (40.33). Singapore is an outperformer in this regard, with Australia on its heels and Malaysia somewhat further behind.

(V) Ontransport infrastructure, Singapore has set the bar for the region. Australia has excellent road, railroad, and air connectivity, and has good shipping connectivity and moderately efficient ports. India’s and Malaysia’s road connectivity needs improvement, their train services are comparatively better and airport connectivity is well-performing – India’s outperforms, ranking 4th in the world. Vietnam’s road connectivity is poor and railroad services are moderate, but airport and sea connectivity are good, even as efficiency of air services and port services is low. Cambodia’s transport infrastructure is in poor shape;[188]in lieu of partner-funded infrastructure projects, it needs increased capital spending from the government to plug the gap, according to the World Bank.[189]

The region has a lot to learn from Singapore’s Smart Nation Initiative. The country is working towards streamlining its public transport and reducing congestion, moving towards an autonomous vehicle future.[190]India already has a partnership in this regard with Singapore and formed an Innovative Corridor in 2018 for knowledge-sharing, but there remains much scope to expand this partnership.[191]

Soft infrastructure and enabling ecosystemsform the second half of the architecture needed for digital transformation. This is explored in detail in the ‘Regimes’ section of this paper.

Capabilities

The availability of a technologically savvy skilled workforce is a crucial ingredient in determining an economy’s ability to push the innovation frontier, as well as adopt technology to produce goods and services adapted to local needs. It is essential for the success of regional connectivity endeavours. Several factors feed into the skill quotient of the workforce, including formal educational attainment, digital literacy, the capacity for lifelong learning and up-skilling, research output, firm-level capabilities, and labour-force productivity. These are explored in the section below.

Educational Attainment

Data for mean years of schooling and educational attainment enable us to form an estimate of how broad-based the knowledge economy’s foundations really are in the region.[192]

Country

Mean Years of Schooling

Educational Attainment

Status

Australia

12.7

93.4

Aspirational

Singapore

11.5

81.4

Aspirational

Malaysia

10.2

74.2

Good

Vietnam

7.6

65

Catching up

Indonesia

8

50.9

Catching up

India

6.0

37.6

Laggard

Cambodia

4.6

12.3

Laggard

Table 2: Educational attainment in case countries (based on World Bank and UNDP databases)

World Bank data indicates that India’s educational attainment rates are worryingly low, as are Cambodia’s. One factor influencing poor educational attainment in Cambodia is its secondary enrolment rate – the World Bank estimated this at 45 per cent.[193]

Thequality of educationis just as significant: basic competencies such as numeracy and literacy are key to building robust innovation capacity.[194]PISA scales in reading, math, and science point towards the quality of primary and secondary education. Singapore and Australia have high PISA scores and Vietnam is a relatively new outperformer with PISA scores at 502. Malaysia is doing relatively well at 430.9; however, India and Cambodia have not taken part in PISA at all for the past few years – India stopped in 2009 after it performed very poorly on the test.[195]India is planning to re-enter the ranks of PISA-takers in 2021 and is preparing for the test cycle. There is tremendous scope for improvement for both India and Cambodia in terms of catching up on basic numeracy and literacy skills. Their education systems have realised the need to gear towards being more competency-based rather than reliant on rote-learning.[196]

Tertiary educationis crucial increasing product sophistication and moving up the global value chain.[197]UNESCO’s figures for tertiary enrolment across the region suggest that Australia and Singapore have an impressive record, with Malaysia and Indonesia quite some way behind with enrolment rates of 45 per cent and 36 per cent respectively, and India, Vietnam, and Cambodia lagging far behind.[198]There are significant variations even among the laggards: only about 32 per cent of those with tertiary education in Cambodia are using digital skills, as compared to 88 per cent in Indonesia for example.[199]

A look at the percentage of graduates from STEM programs in tertiary education in these countries provides further nuance. Here, India, Singapore, and Malaysia outperform, with 31.73 per cent, 34.93 per cent, and 40.77 per cent of STEM graduates, respectively. India evidently has a high-performing class of STEM graduates cornering the gains of education and technological diffusion – also due to its eminent research institutions (ranking 8th in the world).[200]However, the majority of the Indian population lacks basic numeracy, literacy, and digital familiarity. This is a significant barrier that impedes sustainable growth for India’s digital economy. The data also suggests that Australia (whose numbers are quite low for a high-income country with eminent research institutions, at 18.43 per cent), along with Cambodia (15.43 per cent) and Indonesia (19.42 per cent), need to push STEM education further in their education systems.[201]

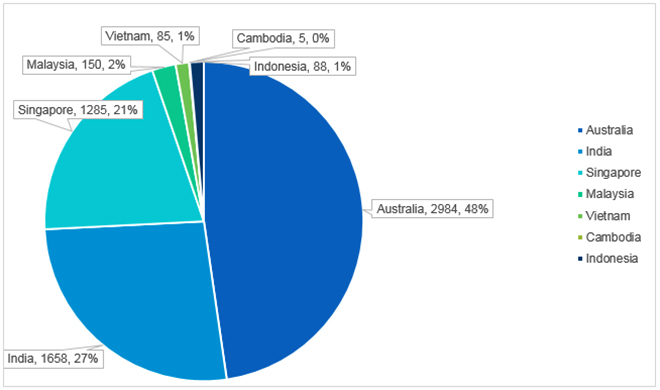

India, Australia, and Malaysia also need to inculcate research talent: India scores very poorly on this, and Australia and Malaysia are performing far below potential.[202]The following pie chart shows the STEM research output in the region, as calculated by the Nature Index (2019–20).[203]

Fig 8: STEM research output in case countries (2019-20)

Digital Skills and Literacy

The 2016 Thomson Reuters Foundation poll ranked Malaysia as the 9th best country to be a social entrepreneur in the world, pointing to the country’s technologically skilled population.[204]Google Indonesia’s managing director Randy Jusuf cited a lack of digital skills as the primary component holding Indonesia’s digital economy back.[205]Less than 30 per cent of Cambodia’s population can copy/move a file on the computer, compared to about 60 per cent of Indonesians and 56 per cent of Singaporeans.[206]

The development of on-the-job learning has been impeded in Cambodia, which is further affected by its weak position in GVCs – Cambodia’s workers perform simple assembly tasks instead of complex production activities and therefore are stuck in a vortex of developing weak productive capabilities as compared to the region. Breaking out of this vortex requires concerted effort – Malaysia and Singapore benefited from a skills levy, which is something others in the region including Cambodia can look at.[207]This is especially relevant for countries like India and Cambodia where vocational enrolment is very low (receiving a score of 2/100 in the GTCI) and within-firm training is still picking up.[208]

Australia is facing a shortage of advanced digital skills,[209]including cloud computing, AI, and digital design – a shortage that can be filled by countries like India and Malaysia. Countries also need to leverage their own workforces better – a spike in illicit activities like hacking in Vietnam etc. illustrate a supply of tech talent in the informal sector that has not been channelled correctly. Initiatives like crowdsourcing and opening government R&D facilities to all through an online portal – undertaken by Singapore and India respectively – and organising hackathons and competitions can encourage mobilisation and collaboration.[210]

Lifelong learning and up-skilling of the existing workforce is a crucial aspect for a resilient workforce – Vietnam and Cambodia have considerable scope to improve in this area, as per the Global Talent Competitiveness Index’s assessment.[211]They could take a leaf out of Singapore’s book: its Skills Future initiative is an exemplar in this regard.[212]

Firm-level Capabilities

Productive capabilities must also be necessarily gauged at the level of the firm, since this is the site for a large chunk of innovation and learning-by-doing in an economy. This is especially true for developing nations – innovation data is often unable to capture the true extent of innovation taking place in developing countries since it is unable to capture learning taking place through apprenticeships and shop-floor experience, and does not account for frugal innovation (adaptation for a cost-conscious market), being often restricted to R&D numbers.[213]

Capabilities necessarily require productive capacity for on-the-job learning and practice to take place. Often, political economy factors such as financing constraints and the lack of scalability and small firm-size are responsible for low productive capabilities, rather than an absence of skilling. Research suggests this is true for both India and Indonesia, for instance. India has a considerably large micro, small and medium enterprise (MSME) sector as well as a high level of informality, which have impeded the development of productive capabilities.[214]Indonesia’s large firms have shown considerable productivity gains and largely drive innovation in the country. Indonesia’s regulatory landscape discourages smaller start-ups and new entrants, regulation is complex, and the ease of doing business is very low.[215]The expansion of digital platforms could be one medium for Indonesia to coordinate its informal, small enterprises for greater efficiency and scale.

Due to a paucity of comparative data, an elaborate assessment of firm-level capabilities requires relying on national-level surveys and is beyond the scope of this paper.

Key Takeaways

Inclusive Access and Capacity

Building broadband infrastructure requires regional collaboration and the alignment of telecom rules and regulatory frameworks to attract and accumulate investment for this purpose. The region could take a leaf out of the book of recent harmonisation efforts by EU countries in this regard.

Foreign aid and the efforts of international development organisations can play an important role in boosting investing in internet connectivity in the region, particularly in low-income countries. Efforts in this area so far have been fragmented and require greater coordination and alignment with national strategies to make a tangible difference.

The role of competition: The region requires stronger competition policies, both to ensure the presence of a sufficient number of mobile network operators and competition in international mobile roaming. An expansion in regional connectivity will require greater competition in the telecommunications space to enable reduced prices and better coverage. A lack of competition has been impeding Malaysia’s ambition of becoming the regional hub for telecoms traffic and data centre development; the subsidies given to state-owned Telecom Malaysia have stifled the broadband market and driven up costs. Greater broadband access requires the entry of more players in the space and better regulation.

To reduce costs, countries could also explore sharing infrastructure for multiple uses and co-investing in network deployment to share risk and costs. This would require clearer regulatory frameworks.

The region could develop Internet Exchange Points (IXPs) for reducing the burden on regional links and facilitate internet traffic.

The region requires efficient allocation of spectrum and urgent regulatory change to release digital dividend to mobile broadband services, enabling high-speed connectivity. It will also need optimal use of spectrum resources, through spectrum sharing and license-exempt access models. Countries are increasingly committing themselves to the uptake of digital dividend band plans and globally harmonised bands like 1.8 GHz. Expansion in investment for increased digital connectivity and infrastructure will also require stable markets and sound policy targets.

International bandwidth capacity is still quite low in the region. Indonesia, for example, has an international capacity of 0.01 Mbps per user (for comparison, Singapore’s is 2.74 Mbps per user). Therefore, most of the traffic is currently being routed through Singapore. This has made for excessive concentration and lower regional resilience and needs to be remedied.

Capabilities

The region could benefit from fostering people-to-people knowledge networks and providing for increased mobility and knowledge-sharing across the region seamlessly.

To facilitate innovation diffusion, the region must invest in clusters and open innovation networks, especially links between public universities and the private sector.[216]

Greater investment from governments must be directed towards mission-oriented innovation activity. Sponsoring basic research would have tremendous spillover benefits.[217]

Greater trade openness is a very important factor in knowledge and technology transfer across countries.[218]While a detailed discussion of trade policy is beyond the scope of this section, trade is a crucial vector for innovation and learning, and foundational for regional connectivity. This includes South–South trade, as absorptive capacities are often higher for similar levels of technologies.[219]

Data from the Network Readiness Index 2019 suggests that India and Vietnam need to worry about their low labour productivity, a threat to their economies’ competitiveness. India’s labour productivity has been falling significantly over the past decade, affecting workforce quality. India needs more flexible and much less complex labour laws, as well as better product market efficiency, a higher female labour force participation rate, and better social protection for workers. India has made a beginning by simplifying its labour regulations into four codes.[220]Cambodia also needs to shore up its labour productivity to match increasing wages or the economy will be rendered less competitive.[221]

Regimes

Regimes are the final and most important ingredient of regional resilience. Robust data protection, privacy frameworks, and sectoral regulations are the undergirding upon which innovation ecosystems are built, while balancing the interests of businesses, governments, and users. Most of the case countries have in place a constitutional right to privacy; however, progress on data governance and data-sharing frameworks remains patchy, and the region is several milestones away from true interoperability.

Privacy and Data Protection

There is substantial variance in the Indo-Pacific region when it comes to legal and policy frameworks governing privacy and data protection.

In India, Indonesia, Vietnam, and Cambodia, the right to privacy is constitutionally guaranteed. The constitutional text of Cambodia explicitly mentions privacy as a fundamental right,[222]whereas it is implicitly guaranteed by others like the constitutions of India,[223]Indonesia,[224]and Vietnam,[225]often crystallised by way of judicial interpretation. In all these jurisdictions, the constitutional guarantees of privacy are built around the concepts of territorial, bodily, and informational privacy or some subsets thereof, which then serve as the foundations for additional privacy-centric laws and policies.

Right to privacy is perhaps most visibly manifest in data protection laws, whereby the personal information of citizens and/or residents is sought to be protected from unauthorised collection, use, and disclosure by private and government entities, placing control over such information firmly in the hands of its originators, i.e. the people themselves. Of the countries discussed above, none have enacted dedicated and comprehensive data protection legislations, but they are being actively drafted in all these jurisdictions except Cambodia.

A few provisions inIndia’s Information Technology Act 2000,[226]read with the Information Technology (Reasonable Security Practices and Procedures and Sensitive Personal Data or Information) Rules 2011, address data protection in the country at present. These laws define ‘personal information’ and ‘sensitive personal information’, prescribe the baseline security safeguards to be observed by entities handling either category of information, and allow individuals to claim compensation if they suffer harm as a result of legal non-compliance by the entities handling information. This regime will soon be replaced by a Personal Data Protection Act, modelled partly after the GDPR, with the Personal Data Protection Bill 2019 already under active review by the Parliament.[227]

InIndonesia, the Electronic Information and Transactions Law 2008, along with the Government Regulation regarding Provisions of Electronic Systems and Transactions, and the Minister of Communications and Informatics Regulation regarding the Protection of Personal Data in an Electronic System, address data protection in a limited way as its own comprehensive data protection is being drafted.[228]