Regulating the over-the-top industry: A case study of Thailand

This brief discusses Thailand’s Over-the-Top (OTT) industry, focusing on production, consumption and impact. It analyses the rise of online audio-visual business in the country, and the implications for traditional broadcasters. In the context of existing international practices and Thailand’s domestic situation, the brief discusses the current and future regulatory requirements of the OTT industry. It also makes recommendations for a regulatory framework that will promote the creation of quality content and benefit creators, consumers, stakeholders and Thailand’s economy.

Attribution:

Suthikorn Kingkaew, “Regulating the Over-the-Top Industry: A Case Study of Thailand”,ORF Issue Brief No. 315, September 2019, Observer Research Foundation.

This brief is for ORF’s Centre for New Economic Diplomacy (CNED). Other CNED research can be found here.

Introduction

Over-the-Top (OTT) platforms deliver audio, video, and other media content via the internet, eschewing the need for traditional subscriptions, e.g. cable, satellite. This allows consumers to access a wide range of content from around the world.

Traditional broadcasters in Thailand feel that this situation puts them at an unfair disadvantage and are seeking to level the playing field. To this end, they are lobbying the National Broadcasting Telecommunications Commission (NBTC)[1]to expand its scope of regulation to OTT streaming services. However, OTT is not limited to video and video-on-demand services such as the widely popular entertainment streaming service, Netflix. It includes e-commerce, payments, messaging, the sharing economy and transportation services. Therefore, they cannot be effectively regulated under one catch-all “OTT regulation” framework.

Currently, the OTT regulations being adopted by many countries are still in their early stages of development, continuously being reviewed for further improvement. While Thailand can learn from the practices and experience of other countries, understanding the situation in Thailand can also provide pointers for other countries.

The Online Audio-Visual Industry: An Overview

The global online media industry is currently driven by three main factors: demographic change, digital transition, and an increase in the number of smartphone users. These fuel consumer demand for internet-based content, leading to the development of new technology and platforms, which will determine the future of the OTT industry.

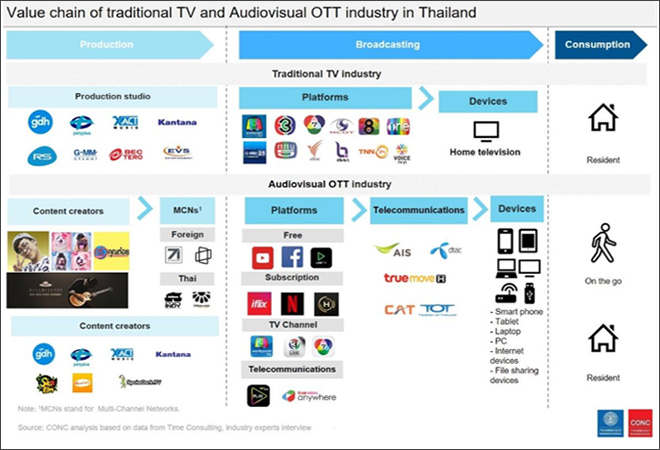

Figure 1: Value Chain of Traditional TV and Audio-Visual OTT Industry in Thailand

Source:CONC Analysis, based on data from Time Consulting.[2]

The Value Chain of Audio-Visual Content

Media Content: Media content is crucial in bringing viewers to the screen. The types of media content available on OTT services include movies, variety and TV shows, sports and user-generated content (UGC). Key stakeholders are the content creators such as production studios, broadcasters or media-rights owners.

OTT Video Platform: OTT service platforms are links between the content owners and the consumers by providing live and on-demand content. The most popular OTT video platforms in Thailand are YouTube, Netflix, Line TV, iflix and Hollywood TV.

OTT Device:An OTT device receives audio and visual signal transmitted from OTT video platforms. The gadgets that support OTT TV service include mobile devices, such as smartphones and laptop; immobile devices, such as smart TV and desktop computers; and digital-media players that can stream content, such as Apple TV, Android box and Chromecast. Key stakeholders are the producers, importers and distributors of all types of device.

End User: The end users are the content viewers, who use OTT video platforms to stream media content on their devices.

Delivery Network: Delivery networks give users access to the media content from OTT video platforms, via an internet connection.

The Growth of the Online Audio-Visual Industry in Thailand

In analysing Thailand’s online audio-visual industry, this brief focuses on two main aspects: production and consumption.

In recent years, the online audio-visual industry has grown dramatically, while the traditional TV industry has experienced negative growth. From 2012 to 2016, Thailand’s OTT industry experienced a compound annual growth rate (CAGR) of 37.6 percent. In 2016, it had a total market value of THB 10,005 million, with advertising-based video on demand (AVoD) accounting for 95 percent of the total industry value. The main driver for this growth is the transition from analogue to digital, which resulted in an increased consumption through free online video platforms, e.g. YouTube, Facebook and Line TV. This, in turn, boosted digital advertising expenditure, especially Facebook Ad, YouTube Ad and Display.

In the same time period, a new potential business model—subscription-based video on demand (SVoD)—increased at a triple-digit CAGR. While SVoD has a smaller market than AVoD, the former has high potential for growth. By 2020, Thailand’s online audio-visual industry is expected to grow at a CAGR of 12.9 percent, owing to the affluence of Thailand’s younger generation and government policies aimed at creating a better internet infrastructure, “Netpracharat.” Compared to this, SVoD is predicted to grow at a much faster rate, with a CAGR of 20.7 percent, due to the increasing number of content providers and the decreasing subscription cost. Since the entry of Monomaxx[3]in the Thai market in 2011, there has been a steady and intense competition amongst local, regional and global players.

Despite the rapid growth of Thailand’s online audio-visual industry, its market value is relatively small compared to the traditional advertising spending, which had a market value of THB 71,009 million in 2016. However, by 2020, the latter is expected to decline to THB 68,991 million, primarily due to the shift in consumer behaviour towards the internet.[4]Audio-visual consumption through online platforms will surpass traditional medium; on average, 76 percent of an individual’s total time spent on audio-video consumption will be on online platforms.

The key drivers of this growth trend include increased internet penetration and the daily average time spent on the internet. The author of this brief conducted an online consumer survey amongst 409 Thai people, at different ages and income levels weighted to correlate with demographics in different parts of Thailand. During 2012–16, the daily time spent on online audio-visual content grew significantly, from 2.4 to 3.8 hours per day, and is expected to reach 4.7 hours per day in 2020, with smartphone being the most used device.[5]The rapid increase in average national income has further fuelled the population of internet users. In 2016, 53 percent of Thai people had access to the internet, 10.7 percent higher than in 2012. In 2018, the number of internet users in Thailand was 47.45 million,[6]of which 90 percent are mobile internet users.[7]Mobile devices provide users with flexibility, privacy, and lower costs, while the traditional medium is limited by its immobility and non-private nature.

The majority of participants in the survey indicated that they watch online audio-visual for entertainment. The most popular platforms were YouTube, Facebook and Line TV, and the most time spent was on drama, movie and animation—both in that order.

Until 2020, the daily time spent on online audio-visual is projected to grow at a CAGR of 5.5 percent, to 4.7 hours per day. This will drive up the total online audio-visual consumption to 54,695 million hours per year. On the other hand, the daily time spent on traditional television dropped from 3.2 hours per day in 2012 to 2.5 hours per day in 2016. By 2020, television watch time is expected to drop further to 1.9 hours per day.[8]In 2016, approximately 63 million Thai people (i.e. 98 percent of the population) accessed the television. However, 28 percent of Thai traditional television was distributed via terrestrial platforms, with six free channels, while the remaining 72 percent was broadcast via cable and satellite. These cable and satellite also broadcast six free TV channels as well as 700 other channels.[9]

The online audio-visual provides countless benefits to key stakeholders in the industry, including consumers and content creators. It also boosts Thailand’s overall economy. The following are some of the key benefits:

Consumers can access the content faster and more easily, with a wider range of content available at lower costs, compared to the traditional medium. They can instantaneously access entertainment, news and information. For example, OrmSchool[10]is a social enterprise that uses YouTube as a platform to provide education to Thai students for free.

Traditional players can complement their existing system by using OTT as a tool to engage and receive feedback from the audience, using features such as comments, live chat, like/dislike and subscription buttons. Online platforms can create great opportunities for traditional creators to expand their audiences, both national and international. The initial success of Mask Singer from Workpoint Entertainment[11]is a great example of traditional channels and online channels supporting each other, as the number of viewers from both channels were peaking at the same time.

Independent artists and creators can use OTT platforms to create original content on a relatively lower production budget and with lower barriers to entry. Many online influencers in Thailand successfully reap the benefit from the donations, merchandising, product placements, partnerships and advertising charges, by delivering content through their own channels. Krit Boonyarang (also known as Bie The Ska),[12]a famous Thai YouTuber, started making videos as a hobby. Now, it has become his primary source of income. He has founded his own production house and hired 17 employees to work on online content.

The drive towards online audio-visual will have a positive impact on the whole economy. Extrapolating from the existing data on input-output models and employment impact, Thai OTT segment is expected to show a revenue growth of 23.9 percent in 2019[13]. The online audio-visual trend will also create extra revenue in each level of value chain, in the form of both corporate and personal income tax. The Digital Advertising Association (Thailand) estimates that the total spending on digital media advertising in 2019 will reach THB 14 million, which is a 21 percent growth from last year. Therefore, NBTC is strongly pushing for a collection of VAT and corporate income tax on the OTT players in the country.[14]

Domestic Regulations

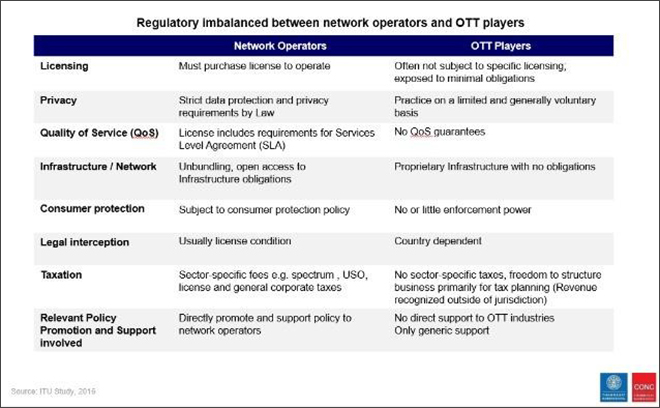

The extensive growth of the OTT market and the excessive disruption to traditional businesses have made Thai regulatory bodies vigilant. Moreover, the TV network operators and traditional media players have protested the loss of their market share to online businesses. They argue that their business models are determined to a large extent by regulatory requirements, whereas OTT players are limited by minimal obligations. The affected players have urged the authorities to act, using its own traditional way of thinking, inclining towards more regulation and control.

Figure 2: Regulatory Imbalanced between Network Operators and OTT Players

Currently, the OTT industry in Thailand is indirectly regulated by several government departments. In the absence of direct control over the OTT players, the NBTC has started to explore possible regulatory frameworks for the industry. It recently decided to lower the licence fee for digital TV operators by using a progressive rate. It has also allowed digital TV licence holders to return their licences without penalty. The authority is also considering broadening the definitions of OTT service providers and governing them through awarded licences. A 2017 NBTC study revealed that the push for OTT licensing and regulation is also a response to the concerns raised by OTT entrepreneurs regarding illegal content, piracy, unfair competition, and the call for standardised supervision.[16]Currently, OTT players have few regulatory requirements, which mostly focus on OTT content and patent regulation.

The Thai government is now promoting business registration and transparent corporate income tax payment. It also suggests regulating OTT providers instead of user content generators. The Thai Revenue Department (TRD) has proposed a new tax scheme to incorporate online businesses into the system.[17]

Figure 3: Regulatory Imbalance between OTT Players and Network Operators

Source:Framework, International Telecommunication Union.[18]

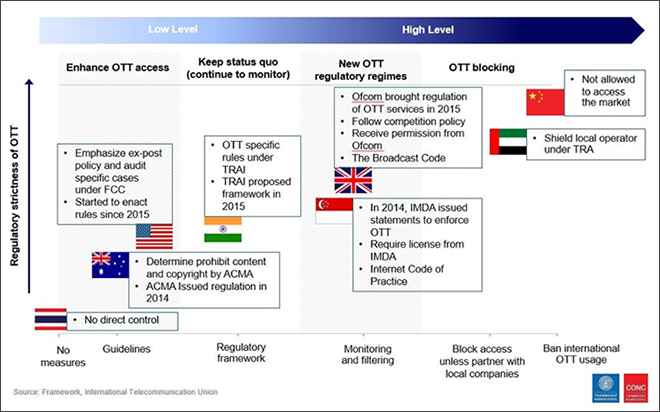

International Practices

Many countries are now adopting guidelines or laws to regulate OTT platforms. Comparing international practices across the UAE, the UK, Singapore, India, Australia and the US, this brief classifies OTT regulation into four levels of intervention, from low to high:

Enhancing OTT access

Maintaining status quo and continuing to monitor

New OTT regulatory regimes

OTT blocking.

Under this classification, Thailand’s OTT regulatory intervention is low, at level two.

India:Net neutrality is a crucial tool for promoting competition in the OTT industry, especially in developed countries with strong net-neutrality rules. The Indian government has recently endorsed net neutrality, which is regarded as the world’s strongest norm. The new rules discourage any form of discrimination or interference in the treatment of content, including blocking, degrading, throttling, zero-rating internet data or granting preferential speed or treatment.[19]Thus, India has ensured improved OTT access; however, little has been done to facilitate fair competition between Telecom Service Providers (TSP) and Internet Service Providers (ISP).

UK:In the UK, the Office of Communication has the authority to regulate the OTT industry under the Broadcasting Act. The EU directives provide guidelines to regulate content, licensing, consumer protection, and the Advertising Standard Authority regulates advertising content. The new regime aims to increase OTT obligations by licensing and making content approval obligatory.

UAE: In the UAE, international OTT platforms are obligated to work with licensed telecom companies. Until recently, there were only two operators licensed to provide public telecommunications services to and within the UAE. The Telecommunications Regulatory Authority is currently not issuing new licences for public telecommunications service.[20]Thus, the UAE protects the market by blocking outside OTT players, unless they partner with local firms.

US: The US Federal Communications Commission (FCC) officially repealed its net-neutrality rules in 2018. The FCC claimed that the regulations were unnecessary and heavy-handed, which hindered innovation in telecom companies. The FCC plans to introduce the practical regulations instead, which will better incentivise investment, high-speed internet upgrades and technological innovations. However, the revoking of net-neutrality laws was met with critics and resistance from several quarters, including state officials, members of Congress, technology companies and various advocacy groups.[21]

Notwithstanding local variations, OTT regulations across most countries involve five crucial aspects: content regulation, licensing, net neutrality, taxation, and supporting policy. However, despite governments being increasingly aware of the need for OTT regulation, there are currently no globally accepted best practices. This is because OTT regulatory developments are in their early stages, and the frameworks are subject to reviews and modifications. Further, there is a lack of industry-specific supporting policies, even though the generic polices do benefit the OTT players by supporting nationwide network infrastructure, including creative and quality content.

Conclusion and Recommendations

To improve the audio-visual industry, the Government of Thailand must foster a competitive market, promote creativity and innovation, ensure consumer welfare, and facilitate future business opportunities. This brief recommends that government regulations for the OTT industry should intervene at low levels.

The NBTC should primarily be an intermediary for coordinating between public and private sectors to achieve two main objectives:

Content regulation: The private and public sector must work together to create a discerning audience that can protect itself from inappropriate content. Amongst digitally literate consumers, self-regulation of content will be a viable alternative to government intervention. Further, it will promote the generation of creative content, the expansion of the online media industry, and the protection of consumer welfare.

Net neutrality: Currently, Thailand has no regulations in this area. The Government of Thailand should implement net neutrality to foster a more innovative and fairer market for competing players. At the same time, it should adopt anex postpolicy to gradually improve any regulatory oversight.

To further improve OTT regulation, the relevant state agencies should consider the following issues:

OTT Taxation: There are two possible approaches for OTT taxation: a) value-added tax and b) withholding tax. The government can collect such a tax by extending the definition of taxable presence in Thailand and assigning an agent to facilitate the taxation process.

Supporting policies: The BOI and other government agencies should incentivise both foreign and local investors to establish their creative content centre and promote local activities. This will subsequently help expand the Thai media industry and increase the overall competitiveness of the country.

The framework proposed in this brief will improve Thailand’s overall economic activity and help increase its GDP. Under the proposed low level of intervention, the online audio-visual industry is expected to provide THB 50,558 million in value to the local economy, approximately 0.30 percent of the Thai GDP in 2020.

Through minimal intervention in the local OTT industry, the Government of Thailand can encourage the generation of creative content while allowing consumers to access a wide variety of content. A competitive ecosystem will also improve content quality and expand the local media industry. Ultimately, such a strategy will contribute to establishing Thailand as a global hub for creative content.

About the Author

Suthikorn Kingkaew is a Lecturer of International Business and the Director of the Consulting Centre at Thammasat University in Thailand.

Endnotes

[1]NBTC currently regulates solely on TV broadcasting, telecommunications and radio communications. See, “NBTC’s Authorization”, Office of National Broadcasting Telecommunications Commission, Thailand, accessed 29 August 2019.

The views expressed above belong to the author(s). ORF research and analyses now available on Telegram! Click here to access our curated content — blogs, longforms and interviews.

Suthikorn Kingkaew is working as an academic practitioner at leading universities in Thailand. He has PhD in Management Studies from Cambridge University. He has conducted ...

PDF Download

PDF Download