-

CENTRES

Progammes & Centres

Location

PDF Download

PDF Download

Soumya Bhowmick and Debosmita Sarkar, “Localising Globalisation in the Bay of Bengal: The Indian Imperative,” ORF Occasional Paper No. 394, March 2023, Observer Research Foundation.

Changing Contours of Globalisation in the Bay of Bengal

In 1911, when the capital of British India was shifted from Calcutta (now Kolkata) to Delhi, it dampened India’s prospects of regional connectivity with the littoral countries in the Bay of Bengal (BoB) region—i.e., Bangladesh, Indonesia, Myanmar, Sri Lanka and Thailand.[1] Those countries themselves, except Thailand, were also largely inward-looking and their economies relied more on the State than on market forces. Upon the transition to a market-driven economy in many countries in the region around the 1990s, the BoB countries again started participating in the Global Value Chains (GVCs). The countries adopted policies to enable the free flow of goods, services, capital, technology, and information.

Since then, the BoB countries, and the larger Indo-Pacific, have become a robust market for economic partnerships. The region, after all, is home to approximately 60 percent of the world population,[2] and some of world’s fastest growing emerging market economies and busiest marine trade routes.[3] There is greater vigour in partnerships between countries in the region, and with extra-regional actors, to counter China, which holds a key position in the regional value chains and is a significant trade and investment partner for almost every Indo-Pacific country, including India. Indeed, trade volumes with China have increased over the years (see Appendix 1). India-China trade, for example, reached a record high of US$ 135.98 billion in 2022.[4]

Prior to the COVID-19 pandemic in late 2019, as the threat of China’s Belt and Road Initiative (BRI) and ‘String of Pearls’[a] strategy loomed large, India showed enthusiasm for establishing links between the Southeast Asian countries through its ‘Act East’ policy. The United States (US), Japan and Australia have also been trying to contain the Chinese threat through the development of Indo-Pacific links. These include the US-led Indo-Pacific Economic Framework (IPEF) and the Comprehensive and Progressive Agreement for Trans-Pacific Partnership (CPTPP) that represents 11 Asia-Pacific countries, both of which seek to lower barriers to trade in goods and services, and associated trade costs. In the case of Bangladesh and Sri Lanka, developing strong links with countries in the region means lessened reliance on China for trade and commerce. Therefore, active engagements among these economies towards countering China’s presence pushed the BoB region to the forefront of the world economy within the larger Indo-Pacific as the centre of gravity for global trade and economic activities.

The eruption of the COVID-19 pandemic in the latter part of 2019 had massive repercussions on the global economy. Most importantly, the over-dependency on Chinese manufacturing had started to hurt global economic growth by then.[5] The intermittent lockdowns and other restrictions interrupted the market demand-supply dynamics from approaching equilibrium, and led to devastating supply chain disruptions and resource crunches across sectors.

Since 2020, the COVID-19 pandemic has offered the global economy a two-fold lesson. First, it reinforced the need to mitigate the over-reliance of value chains on the Chinese economy. The first pandemic-induced lockdown measures quickly led to the deterioration of the factor and product markets across the globe—a significant component of which had emanated from the supply-chain disruptions in China. Additionally, against the backdrop of the US-China trade war, countries such as the US and Japan hastened efforts to find alternatives to manufacturing bases in China, with countries such as Vietnam, Thailand, Malaysia, Taiwan, and India competing for investments fleeing China (see Table 1).[6]

Table 1: International Policy Signals

| Country | Examples of Policy Signalling |

| Japan | In early April 2020, the government earmarked a stimulus package of $2.3 billion to help its manufacturers shift production out of China to relocate to alternate locations or move back to Japan.[7] |

| US | Imposition of tariffs applied exclusively to Chinese goods worth $550 billion between 2018-20. Multiple statements by former President Donald Trump suggested that American companies were to immediately search for bases other than China to avoid tariffs.[8] |

Source: COVID-19: FDI dynamism in South and Southeast Asia, ORF[9]

Assembly partners of giant players in the electronics segment have shown interest in moving from China to other countries in South and Southeast Asia. Apple, for instance, has plans to expand manufacturing in India, with its supplier Foxconn also planning to invest up to US$ 1 billion in India over the next three years.[10] Manufacturers of automobile parts, footwear and equipment are also keen to diversify or shift their supply chains.

Second, the transportation hurdles during the pandemic provided an impetus for governments to shift from leveraging inter-country comparative advantages to intra-regional and domestic sufficiency in value chains. This charted the path towards resilient domestic capacities and created alternatives to China in sourcing both essential and non-essential commodities at competitive prices. Most importantly, countries have also become more cautious in terms of their involvement in economic groupings and multilateral platforms, adding new dimensions to globalisation trends in the post-pandemic world.

For example, in 2020, India chose not to join the Regional Comprehensive Economic Partnership (RCEP), the world's largest trading bloc, for twin reasons: to protect the interests of the robust domestic market and to dissociate itself from China’s involvement in RCEP.[11] Again, the historic Comprehensive Economic Partnership Agreement (CEPA) signed between India and the United Arab Emirates (UAE) in early 2022 could help Indian exporters access African and Arab markets, increasing two-way trade from the current US$ 60 billion to US$ 100 billion in the next five years.[12]

This India-UAE effort is only one of many that are attempting to pave the way for post-pandemic recovery. There are massive challenges, however, including China’s ‘zero-COVID’ policy in 2022 that has provoked unprecedented domestic protests, as well as criticisms from the international community for further dampening global prospects for rebuilding. China’s radical measures of massive lockdowns and restrictions added fresh blows to economic sectors ranging from retail traffic to automobile manufacturing. In November 2022, the International Monetary Fund (IMF) Managing Director Kristalina Georgieva urged Beijing “to adjust the overall approach to how China assesses supply chain functioning with an eye on the spillover impact it has on the rest of the world.”[13]

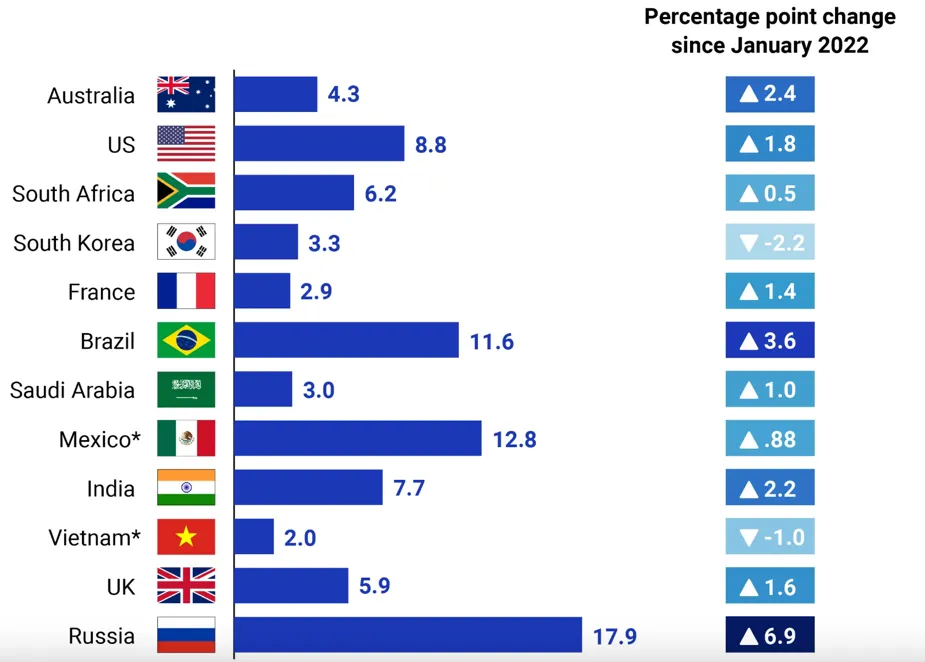

To be sure, the magnitude of the recent COVID-19 surge in China is bound to worsen the trade and supply chain disruptions to other countries. The timing of the outbreak adds to the criticality of the looming global economic crisis. While the BoB neighbourhood is in flux—with a complete economic collapse in Sri Lanka, a military coup and huge unemployment situation in Myanmar, inflation and volatility of domestic currency in Bangladesh and India, political turmoil and financial emergency in Pakistan, and widening trade deficits and declining FOREX reserves in Nepal—the Ukraine-Russia conflict has thrown the energy markets in Global South nations in disarray. Additionally, supply cuts by edible-oil exporting countries and the impact of energy price rise on food prices (see Figure 1) have made food security a significant concern, especially for the poor.

Figure 1: Annual Increase in Food Inflation in Select Countries, as of March 2022 (in percentage)

Source: Trading Economics[14] | *Data for Mexico and Vietnam is from April 2022

The US and the European Union (EU) are both pursuing a policy of industrial sovereignty[b] to decouple from current GVCs that are reliant on China. They have penned agreements such as the EU-US Trade and Technology Council (TTC) and the Indo-Pacific Economic Framework for Prosperity (IPEF) that exclude China and focus on “like-minded nations.”[15] In 2022, on the sidelines of the G20 Leaders’ Summit in Bali, the US reiterated its focus on “managed competition” with China—which the latter continues to disapprove of.[16] The US and EU have heightened their efforts to create regional value chains amidst the Russia-Ukraine conflict. The continuing rise in energy prices has had massive effects on the EU, whose countries import 40 percent of their energy requirements from Russia. Along with energy, key metals such as aluminium and nickel also saw an increase in their price, driving up the factor market prices.[17]

Evidently, the slowdown in the Chinese economy in the recent years has made the global economy vulnerable.[18] While the slump in domestic demand hurt foreign exporters, the strict lockdown measures impacted the supplies to manufacturers, especially in other Asian countries. Compounding the challenge are the inflationary pressures in US and Europe, along with the rising interest rates and a looming economic recession—all of which have exposed the fault lines in the complex interplay of global macroeconomic parameters.

Indeed, the patterns of globalisation as the world knows it, are evolving across the world. A policy paradox appears where the policymaker must choose between globalisation, localisation, or ‘glocalisation’. When exploring the third choice, policymakers must decide the extent of localisation to be pursued within the globalised economy. In India’s case, it is clear that ties with the other countries in the region can focus on the creation of regional value chains that will boost self-reliance. Developed countries are pursuing a policy of industrial sovereignty due to geo-political events, which necessitates that India perform a diversification analysis to identify new products and suppliers. This is where policies such as production-linked incentives and ‘Make in India’ come into play as they help domestic firms achieve the goal of commodity parity and price competitiveness with the rest of the world.

Applying the ‘Gravity Model’ to the BoB

Against the backdrop of a changing global economic order and heightening imperative to reduce over-reliance on the Chinese economy, countries in the BoB region must examine their internal dynamics on trade and regional economic integration. Furthermore, certain countries’ insulating tendencies, rising nationalistic fervour, and the COVID-19 pandemic—are all posing challenges to the status quo of the global economy. While potential security arrangements like the Quadrilateral Security Dialogue (Quad) have attempted to combat these emerging waves of transition, their influence in the economic sectors have remained limited.[19]

As India balances China’s growing economic influence in the Indo-Pacific, it is pushing the strengths of BoB countries, as an economic bloc, to the forefront of its growth agenda. The renewed impetus to regional groupings such as the Bay of Bengal Initiative for Multi-Sectoral Technical and Economic Cooperation (BIMSTEC)[20] and the Asian Development Bank’s (ADB) investments for improving connectivity in the region[21] are all efforts to inject vigour in developing the region as a trade and investment hub. The littoral countries in the BoB region—India, Bangladesh, Indonesia, Myanmar, Sri Lanka and Thailand—are home to more than 25 percent of the global population[22] and together account for a GDP of US$ 5.46 trillion.[23] They all make the region a critical player in both global product and factor markets.

Boosting regional commercial ties can directly contribute to the growth prospects and long-term economic resilience of countries in the region, while presenting trading partners like the United States and the European Union a sustainable alternative to China. US and EU efforts to turn inward and fend off Chinese influence have ramifications on other countries in the Global South that could lose out on potential trade flows. In turn, this bears on how these developing countries will continue to lag behind the Global North in economic outcomes. Like other institutional factors, the economic convergence of countries is also conditional to the degree of their integration in the global economy.[24] Therefore, positing the BoB countries as an economic bloc that is a viable alternative to China, can enable these countries to play catch-up on the global economic ladder.

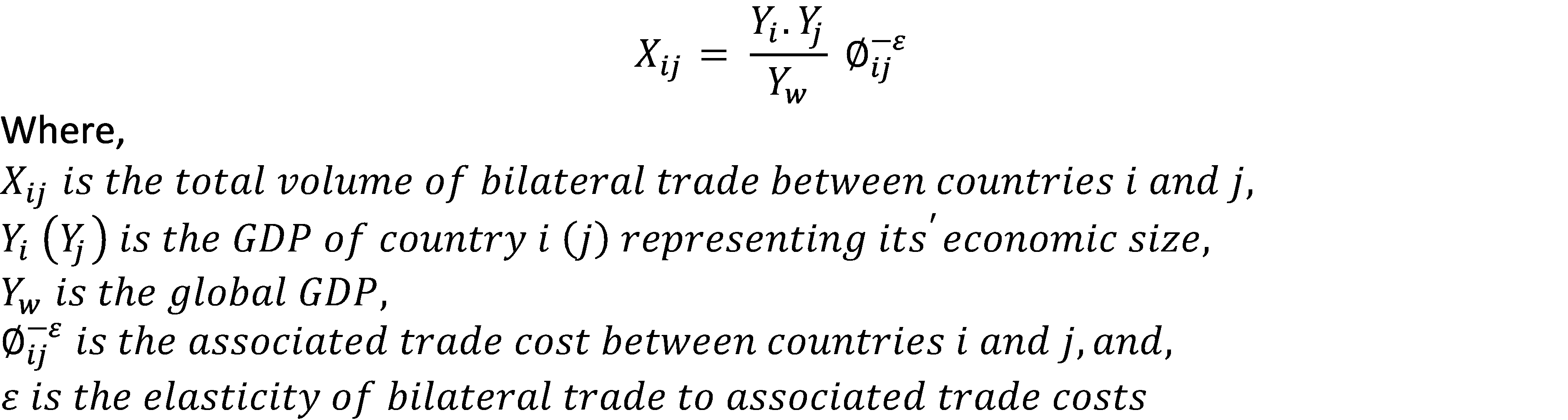

Bilateral trade ties between the BoB countries and the US or EU have historically remained limited, in comparison to their trade with China.[25],[26] In 2022, China was the US’s third largest trading partner accounting for 13.2 percent of its total trade; it was the third largest trading partner for the EU as well. Abstracting from specific factors that have influenced the volume of bilateral trade between these countries, the structural gravity model of international trade suggests that the volume of goods and services traded between two countries is directly proportional to its economic size (serving as a proxy of the production capacity of each trading partner as well as the market demand each represents) and inversely related to the associated trade costs. [27] The structural gravity model can be represented as:

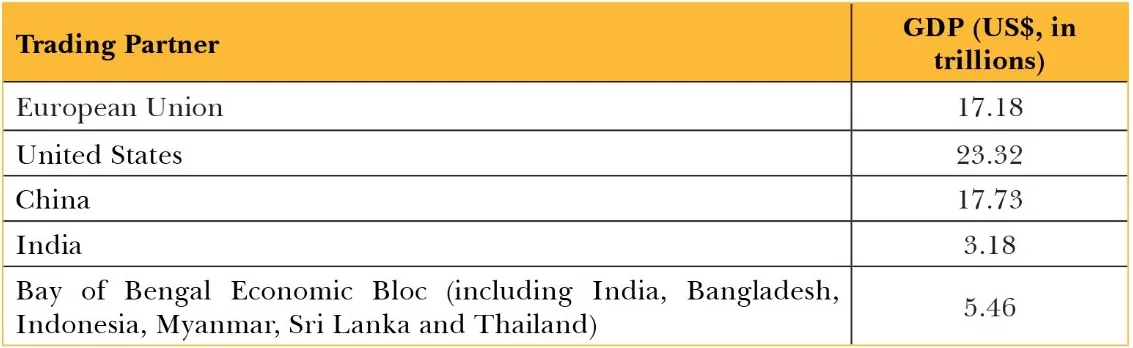

Empirical evidence from the gravity model can explain how trade relations have developed between wealthy economies like the US and EU and their developing counterparts in Asia.[28],[29],[30] First, other factors notwithstanding, the relatively large size of the Chinese economy—reflecting the static economies of scale of its production, and therefore, its comparative advantage in global markets, as well as the demand generated by its large domestic market—have contributed to its flourishing trade relations with countries across the globe. Table 2 shows the aggregate economic size of major trading partners of the US and the EU in the BoB region. In comparison to China, the relatively smaller economies in the BoB littorals have fallen short. The regional integration of the BoB countries into a larger economic bloc can therefore lead to increased bilateral trade flows between the BoB region and countries in the Global North. This could reduce the regional and global trading partners’ over-reliance on China.

Table 2: Aggregate Economic Size for US, EU, China and the BoB, by GDP (current US$, 2021)

Source: World Development Indicators[31]

Evidence also suggests that other than the aggregate economic size of trading partners, bilateral trade flows between countries also increases as the relative difference in their income levels declines.[32],[33] It is the overlapping representative demand of the trading partners that translates into universal demand, necessitating product differentiation and intra-industry trade among them. Thus, nations with similar representative demands are likely to develop similar industries and trade with each other in similar but differentiated goods. This similarity in demand with other countries is influenced by the similarity in per capita income levels.[34] The integration of the BoB countries into an economic bloc can reduce the relative differences in income levels of the individual countries and the US or EU, allowing specialisation due to demand bias and representative demands to operate as a basis for trade.

Second, bilateral trade is significantly influenced by associated transaction costs. These include natural trade costs induced by geography (more simply, the distance between trading partners contributing to transportation costs and reducing price advantage) or unnatural trade costs (induced by cultural linkages, logistical hurdles or trade barriers).[35] The dynamic economies of scale associated with productive activities and long-term trade relations have accorded China a comparative advantage over other potential trading partners from the region. Over time, dynamic economies of scale have helped the country build up synergies that are beneficial in terms of greater productivity, more sophisticated networks, and consequently greater integration into the global and regional value chains. All these factors have eventually lowered the associated trade costs and increased bilateral flows between China and its trading partners.

As the supply chain disruptions emanating from the Chinese economy threaten to overturn these gains, especially after the pandemic, the BoB countries are well positioned to substitute China in the GVCs. To achieve this, the regional grouping must strive to lower the associated trade costs. In the medium- to long-run, enhancing physical and digital connectivity, diversifying trade networks, and building resilient communication and infrastructure systems can help boost regional and global commercial ties.

These goals will necessitate three critical checkpoints in the long run. First, it is essential to understand the optimal scope of such a market within the GVCs. Second, there is a need to identify the potential forward and backward linkages and the nature of trade arrangements that would be most favourable for the region. The third are the trade-offs and synergies between national economic and broader regional goals.

Within the broader ambit of the global economy, regional economic blocs can serve purposes other than stimulating bilateral trade flows and enhancing economic convergence. These can enable localisation of productive activities that benefit from the coordination and the existing complementarities among the regional trading partners. While self-sufficiency within the domestic economy may be a distant goal, strengthening regional value chains can contribute to self-reliance among clusters within a globalised framework. Such self-reliance also provides a degree of insulation in times of global crises such as the COVID-19 pandemic.

Most importantly, regional economic integration of countries plays a crucial role in highlighting their shared internal and external vulnerabilities, aligning their mutual interests, and working out feasible pathways for advancing their common agenda of building economic resilience in the long run. In the present context of the economies in the BoB region, three specific sectors can be critical to the vision of long-term resilience. As food security and energy security are increasingly threatened by the rapidly evolving geo-economic and geo-political tensions around the world, economies and regional groupings in the Bay of Bengal region can focus on creating a strong regional value chain that can promote self-reliance across these two sectors. Connectivity becomes the most important aspect to achieving the goal of an effective regional economic order; technology and digital connectivity can play a crucial role.

As India presides over the Group of Twenty (G20)’s convenings over the year 2023, it can amplify these priorities of the BoB region, and of the developing world at large, on a global platform. For example, India’s G20 presidency is economically crucial for BoB countries such as Bangladesh and Myanmar because of the existing Indian trade ties with the latter nations, access to India’s Northeast, and their centrality in India’s ‘Neighbourhood First’ and ‘Act East’ policies to forge better multilateralism.[36] With the G20 forum bringing some of the most advanced and emerging economies of the world together to address issues or challenges related to global governance, India can highlight the importance for the Global South of achieving self-reliance through promotion of regional value chains. Furthermore, as some of the most vulnerable countries and societies in its neighbourhood continue to reel under the economic fallout of recent global disruptions with little attention from the developed world, the Indian Presidency can create solutions—sometimes drawing from its own experiences—and drive global consensus on key issues related to the three priority sectors of food, energy, and technology. The Indian imperative of localising globalisation in the BoB region, if successful, can be an inflection point in the current global economic order and further strengthen India’s role as a global economic power and key geo-political actor in the coming years.

Outlining the Priority Sectors

The challenge of food security has taken centrestage following the eruption of the Russia-Ukraine war. Both Ukraine and Russia are cogs in the global food supply chains, and their conflict has had massive implications on low- and middle-income countries and vulnerable populations, including the BoB economies, which are already grappling with hunger in the post-pandemic world.

Since Russia and Ukraine together export more than one-third of the world’s wheat and barley, and more than 70 percent of sunflower oil, countries around the world were badly hit as the war stopped exports of around 20 million tons of Ukrainian grain.[37] Before the invasion, an estimated 6 million tons of agricultural commodities were being exported monthly to Asia, Africa, and West Asia. As of June 2022, this number shrank to one-fifth of its value.[38] According to the UN Food and Agriculture Organization (FAO), global food prices have risen by 33 percent between 2020 and 2023.[39] It further predicts the rise in undernourished population from 7.6 million to 13.1 million due to the ripple effects of the war on food prices and availability.[40]

Figure 2: Prevalence of Food Insecurity (Population Percentage)

Source: Authors’ own, data from World Bank[41]

The economic meltdown in Sri Lanka has not helped, wreaking havoc[42] on the food security of the local population; Bangladesh is also facing the wrath of food inflation.[43] For Sri Lanka, the sudden switch to organic farming in 2021 worsened its trade performance in the agricultural sector. The conditions deteriorated rapidly until the country was forced to import essentials including rice and sugar, and various other commodities including intermediate goods which the economy had historically produced in surplus. By 2022, the tea industry—which was a key commodity of exchange for the economy—incurred losses reaching US$ 425 million which further worsened the country’s foreign exchange situation.[44] In this context, it becomes imperative for regional groupings to create safeguards against crises where their food security is affected by geopolitical events and domestic macroeconomic threats.

The idea of a food bank for the BIMSTEC countries, modelled on the Association of Southeast Nations (ASEAN) Food Bank, is a good start as it will aid in stabilising prices.[45] In November 2022, India hosted the second Agriculture Ministerial-level meeting of the BIMSTEC nations where it urged the member countries to develop a regional strategy for transforming agriculture and promoting millet as a staple in food systems.[46] Promotion and intra-regional trade of food items such as millet, where the countries have surplus production, can help ameliorate food insecurity.

Data on energy imports show that all the countries in BIMSTEC—particularly India, Myanmar and Bhutan—are heavily reliant on energy imports (see Table 3). The region’s trade dependency on fuel has made it highly vulnerable to exogenous macroeconomic shocks, such as the Russia-Ukraine conflict.

Table 3: Fuel Imports in BIMSTEC Economies (as percentage of merchandise imports)

Source: Authors’ own, data from World Bank[47]

Unable to set in motion the transition to renewable energy, alongside heavy dependence on fuel imports, Bangladesh especially has been placed in a precarious situation concerning energy security. The Ukraine war has only added to the difficulties. With energy prices climbing upward and subsidy bills increasing, the fiscal balances and current account deficits have been worrisome for the economy. The government had to finally put in place certain austerity measures in August 2022.[48] The domestic prices of fuel (per litre) were increased: diesel (by 42.5 percent, to Tk 114); kerosene (42.5 percent, to Tk 114); octane (51.6 percent, to Tk 135); and petrol (51.1 percent, to Tk 130). These were the highest increases in almost 20 years.

To be sure, the BIMSTEC countries released a ‘Plan of Action for Energy Cooperation in BIMSTEC’ many years ago, in October 2005, and signed a Memorandum of Understanding (MoU) for the establishment of the BIMSTEC Grid Interconnection in August 2018. However, the absence of required infrastructure and adaptive power market, the lack of synchronisation of the grid system and grid codes to electric power and natural gas pipeline technology, absence of appropriate financial policies, and other related issues have impeded energy cooperation among the countries in the region. In 2021, the BIMSTEC Grid Interconnection Coordination Committee aimed to create a policy framework for trading and exchanging electricity, and establishing a tariff mechanism. It is also working on the BIMSTEC Grid Interconnection Master Plan Study (BGIMPS).[49]

The region’s economies have huge potential to invest in research for green technologies that can help them develop self-reliant energy markets. For instance, FDI from Japanese firms has had positive spillovers on the Indian economy, with over 1455 Japanese companies operating across sectors.[50] If the scale economies and potential of Japanese firms in developing green energy technologies could be fully utilised, it will reduce the regional dependence on China, which is currently the dominant player in solar energy.[51] At the 27th Conference of Parties (COP27) in 2022, India unveiled its long-term commitment to phase out all forms of fossil fuels including coal and oil by the year 2070.[52] Led by India, the Bay of Bengal region can share knowledge and learnings in innovations in renewable energy such as solar and wind. India’s National Green Hydrogen Mission can boost the manufacture, use, and export of green hydrogen in the country, besides promoting self-reliance in the region’s energy sector and accelerating decarbonisation of the industrial and transportation activities of the regional value chains.

Integration is no longer just a physical concept and digital connectivity has become an equally important domain. Digital technologies also facilitate psychological connectivity by enabling people-to-people engagements/networks.[53] Digital technologies are continuously expanding, and India must promote the creation of a regional digital cooperation framework that will promote e-commerce, digital innovation, cyber-security, and resilient supply chains.

There is no doubt that Information Technology (IT) has aided the Fourth Industrial Revolution (4IR) as technological progress impacts various spheres including trade cooperation and pandemic response. Developments in Artificial Intelligence (AI), data processing and transfer, and data security can play a central role in informing and shaping the domestic and international policies of nations.[54] The neoclassical, as well as endogenous growth theories, point to variations in technology levels as a cause behind poverty in developing countries.[55] This also suggests that, as technology progresses, the wedge between the rich and poor narrows with convergences in their per capita income levels.

Even as the countries in the Bay of Bengal were late entrants to the IT revolution, the import of advanced technology vastly improved the total factor productivity (TFP) of these economies. Upon its inception in 1997, BIMSTEC had already identified technology as one of its priority areas for cooperation. At that time, the BIMSTEC states sought to create and exchange technology towards the achievement of goals in agro-based industries, food processing, herbal products, biotechnology, and ICT-related industries.[56] Given that South Asia and East Asia were predominantly agrarian during that period—and their state of industry were younger than that of the Western world—the use of technology in the region was predominantly aimed at moving agrarian goods up their value chains.

Taking the lead in BIMSTEC’s science and technology initiatives was Sri Lanka. As early as in 2008, the BIMSTEC leaders had envisioned the establishment of the BIMSTEC Technology Transfer Facility (TTF) in Colombo.[57] The group’s efforts, however, have been rather piecemeal in the last two decades (see Appendix 2).

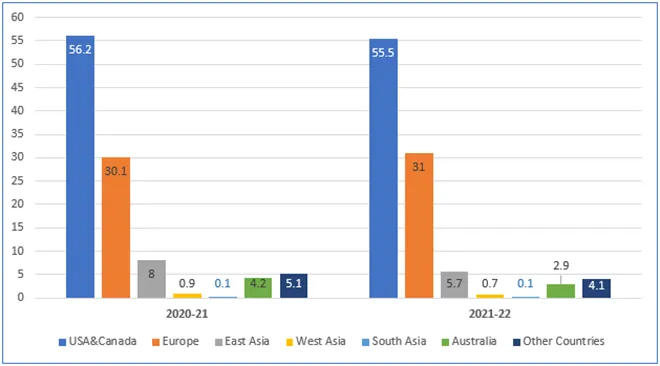

The Bay of Bengal region has tremendous human resources potential that can be utilised by the countries to advance innovation in the field of technology. This is necessary, given how the software services exports from India to the South Asian region, for example, have remained consistently low at 0.1 percent of total exports between 2020 and 2022 (see Figure 3).[58] The ‘Make in India’ scheme launched in 2014, could be leveraged for economic progress in the BoB region. To optimise this potential, the BoB countries will have to invest in upskilling their youth through strategies that include regional collaborations. India’s digital economy is estimated to grow to an US$ 800-billion consumer market by 2030, with e-commerce being one of the fastest sectors to grow, especially owing to changes in consumer behaviour in the post-pandemic scenario.[59]

Figure 3: India’s Software Services Exports (percentage share)

Source: Authors’ own, using data from the Reserve Bank of India[60][/caption]

The India-Japan digital partnership formalised in 2018 in a Memorandum of Cooperation (MOC) seeks to promote start-ups and enhance digital security through inter-company collaboration (including startups) and R&D in the AI domain for next-generation networks.[61] Meanwhile, the Australia-India Cyber Partnership, launched in April 2021, has resulted in advancements in the field of quantum computing and the Internet of Things (IoT). In April 2021, Japanese firm Fujitsu also opened a research centre in Bengaluru to accelerate Research and Development (R&D) in AI and Machine Learning (ML).[62] Similar efforts can help countries in the region tap each other's strengths and jointly move up the technology value chains. Japanese investments in this region have mostly been focused on Bangladesh, where more than 300 Japanese firms in the exports business operate from. This is unlike the Japanese firms in India, whose business model is domestic-oriented. The free flow of technology and capital between the two countries could help each contribute their strengths to the creation of regional value chains that benefit the entire BoB region.

Regional cooperation can also play a role in promoting cyber security. The Quad, for instance, incorporates cyber security as a pillar that is built on each country’s strengths. Australia contributes towards ensuring the safety of critical infrastructure, Japan leads workforce and talent development while the US focuses on software security. India steers cyber security for supply-chain resilience and can therefore play a critical role in the technological integration of BoB economic bloc into the regional value chains. Following the Quad’s model, such regional groupings should interact with each other in the interest of technological progress in the BoB. Cooperation is also essential for fostering advancements in the digital components of maritime networks and using technology-driven public goods such as common internet zones that can utilise the scale economies in the region.[63]

Connectivity Challenges Dampening the Regional Value Chains

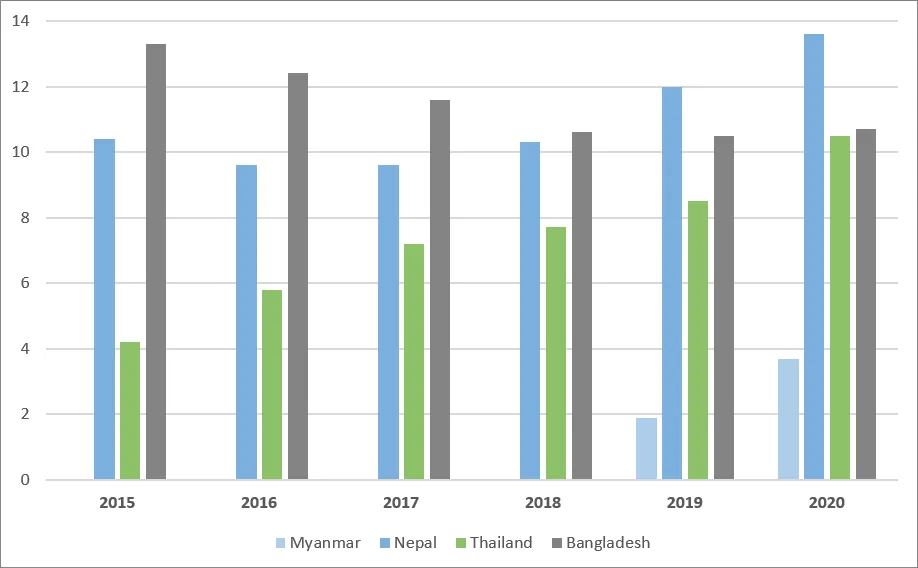

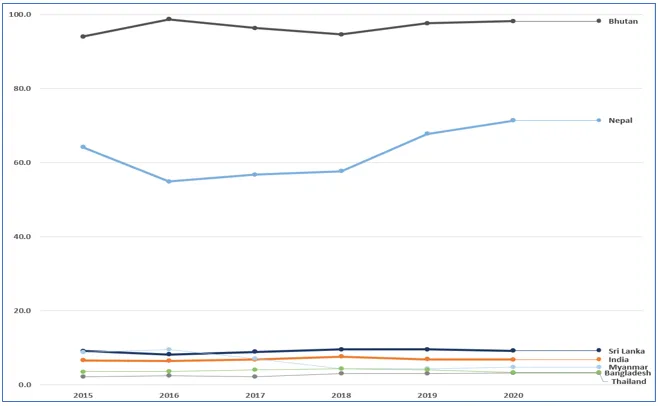

Physical connectivity is one of the biggest obstacles to regional partnerships in key economic sectors. In 2020, intra-regional trade in South Asia contributed only 5.6 percent to the total trade volumes of the region, compared to 22 percent of total trade being intra-regional in Sub-Saharan Africa.[64] Without the free flow of information, capital and technology, the economies in this region are unable to create an integrated regional value chain. For instance, although Bangladesh and India have complementary strengths, hurdles in customs clearance raise the requirements in time and production costs. This disincentivises firms from investing in regional manufacturing businesses. Defying the logic of proximity, only about 2-4 percent of India’s total trade is with its immediate neighbours in the BoB region.[65] According to trade data for the BIMSTEC countries and low and middle-income economies in South Asia, the percentage of total merchandise exports is less than ten percent for five out of the seven countries of the grouping (see Figure 4).[66]

Figure 4: Merchandise Exports to Low- and Middle-Income Economies in South Asia (percentage of total merchandise exports)

Source: Authors’ own, data from the World Bank[67]

The average time taken for cross-border trade in South Asia is 53.4 hours; it is 16.1 hours for Europe and Central Asia (ECA), and for the high-income Organisation for Economic Cooperation and Development (OECD) countries, 12.7 hours.[68] When it comes to border compliance costs, the cost for South Asia stands at US$ 310; for ECA it is US$150 and for OECD, US$ 136.8.

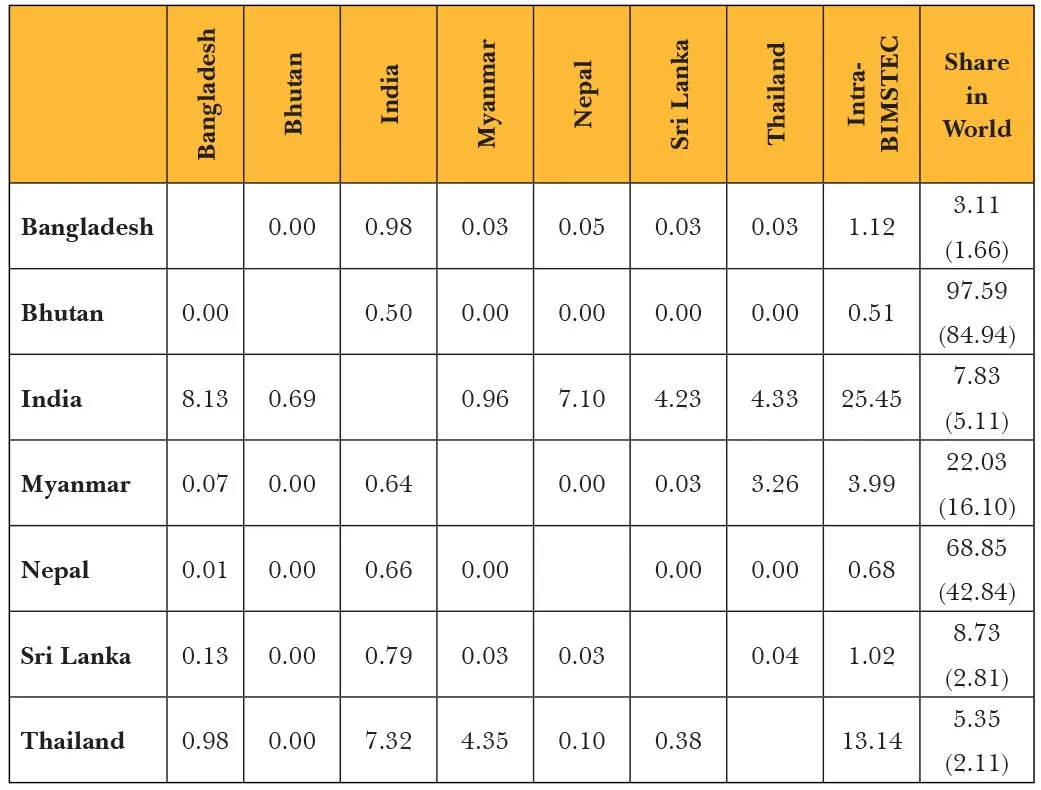

The Bay of Bengal region has abysmally low levels of integration, which creates a gap between South Asia and Southeast Asia. This constrains the countries from accessing the opportunities available in their immediate neighbourhood. For example, Myanmar, Nepal and Bhutan have an abundance of hydropower infrastructure, but they are not interested in tapping it in the absence of domestic demand that would justify the project costs.[69] On the other hand, India and Bangladesh import massive amounts of energy and act as excellent markets for this hydropower. These complementarities should be harnessed to create robust regional production networks. The lack of subregional ties is visible when looking at the intra-BIMSTEC trade matrix shown in Table 4. A careful analysis of the resource base of the regional economies, their existing production capacities and networks, and the market demand structure can help boost intra-regional trade among the BIMSTEC countries.

Table 4: Intra-BIMSTEC Trade (Exports, percentage)

Source: UNESCAP (2021)[70] | *Numbers in parentheses show corresponding data for the year 2000

Regional integration, especially in the energy sector, requires support from multilateral agencies such as the ADB given the exceptionally large amounts of investments; countries like Myanmar and Nepal would not be able to finance them on their own. Until recently, China was a significant investor in Nepal’s hydropower sector. However, with one of its largest export market, India, willing to step in, Nepal has diversified its hydropower projects to Indian companies.[71] India-Bhutan hydropower cooperation has been crucial to the mutually beneficial expansion of their bilateral economic linkages.[72] Similarly, India must take the lead in providing knowledge inputs and bilateral funding for renewable electricity projects in other countries in the neighbourhood and aid in the setting up of companies that can own and operate these projects. A Bay of Bengal Power Grid can be created with local governments as the key stakeholders and the Bay of Bengal can function as a springboard for trading energy resources between other regions.

To create regional value chains, the countries in the BoB region require efficient connectivity networks. Ports are the central part of maritime connectivity that links the various supply chains. The United Nations Conference on Trade and Development (UNCTAD) estimates that global maritime trade is set to grow at a rate of 3.5 percent in the 2019-2024 period. The maritime potential of the Bay of Bengal is immense and effective diversification of investments on connectivity infrastructure becomes crucial to counter Chinese hegemony in the region.[73]

Against this backdrop, it becomes particularly important for the countries in the region to maintain a fine balance between their overall external debt and their debt to China—at present the developing world’s largest creditor nation. This is particularly true for countries in the BoB that are part of the BRI, such as Sri Lanka which is still reeling under the economic crisis that started in 2022. For Sri Lanka, the Hambantota port reflects unrealistic projects built on foreign loans that created highways, airports and convention halls. Despite rejection of the concept by the Ministerial Task Force[c] in 2003, the port was erected near the hometown of the president at that time, Mahinda Rajapaksa, and paid for with US$1.1 billion in Chinese financing.[74] Due to the port's failure to become commercially viable, Beijing bailed it out in 2017 by purchasing a 99-year lease for US$1.1 billion from a state-owned corporation, the China Merchants Group.

Many analysts concur that Sri Lanka had fallen victim to China’s ‘debt-trap diplomacy’.[75] Although China does not account for the highest percentage of Sri Lanka’s outstanding external debt, China’s liquidation techniques and hidden debts in various infrastructure projects also reflect the problematic outcomes of Beijing’s aggressive distribution of loans. According to analysts at Advocata Institute, a Colombo-based think tank, the amounts owed by Sri Lanka to Chinese creditors as of 2022 were the following: US$ 119 million owed to the China Development Bank Corporation; US$ 232 million to the China Development Bank; and US$ 232 million to the Export-Import Bank of China.[76]

The Andaman and Nicobar Islands can provide an impetus to New Delhi’s ambitions if utilised correctly through the International Container Transshipment Terminal (ICTT) at Great Nicobar Island, that will be a hub in the East-West International shipping corridor.[77] The logistical issues present in the ports on India’s East coast, such as congestion and lack of storage space must be eliminated to foster a cordial relationship between the ports and the user countries.[78] India can also encourage more investment in the private ports on the East coast that include Kattupalli, Krishnapatnam and Ennore, which have deep water channels, improved connectivity, and efficiency in operations.

The relaxation of cabotage laws has increased direct shipments in the Indian ports, and similar moves for vessels operating between the countries in the Bay can further encourage the easy movement of cargo between the neigbouring countries.[79] India’s strength lies in its investments in road and rail transport connecting it with Nepal, Bangladesh and Myanmar, which it started many years ago. The scale of these projects can be expanded to provide direct connectivity with the neighbourhood. Indeed there is the BIMSTEC Master Plan for Transport Connectivity, which is a 10-year strategy aimed at enhancing the domestic and regional connectivity of the BIMSTEC member states.[80] At the Fifth BIMSTEC Summit in 2022, India also pledged an amount of US$ 1 million to increase BIMTEC’s operational budget.[81]

Another crucial aspect to enable connectivity networks and trade, is robust security. Relevant information must be shared freely to foster a rule- and order-based environment in the Bay. Maritime surveillance and infrastructure investments must be undertaken by the region, especially in the context of China’s expansionist policies. A good model for the countries to follow would be the Indonesia-Malaysia-Philippines agreement in 2016 which created a hotline for quick response to piracy and kidnapping incidents.[82] Initiatives such as the multi-modal logistics park set up by the Indian government can help enable localisation in the BoB region. When it comes to trade, facilitation of trade has shown better results than reduction tariffs when the tariff levels are already low.[83] Market-led integration and government-led initiatives must be used to create hyper-local industrial value chains that will link the Bay’s micro-regions.[84]

Other Developmental Priorities

The glocalisation policies in the BoB must also incorporate the aspects of climate mitigation and adaptation, alongside equitable growth. Countries in the region are vulnerable to various non-traditional security (NTS) threats owing to sinking landscapes, frequent cyclones and floods, loss of livelihoods and mass migration driven by climate change. According to the Global Climate Risk Index, all countries in the BoB region are ranked among the 20 most vulnerable countries around the world.[85] Moving beyond the existing system of trade and cooperation, adopting clean energy partnerships can make climate goals achievable for the countries in the region.[86] Sustainability targets must be localised by engaging local businesses and local governments.

To advance the objectives of sustainable livelihoods in the Bay, the countries must nurture their Blue Economy, which will require cooperation between the countries as well as the participation of the private sector. Existing studies have revealed the Maritime Renewable Energy (MRE) potential of the Bay, particularly in ocean wave[87] energy generation and tidal energy.[88] To harness this, the countries must cooperate to map MRE in the region and invest in R&D and infrastructure to lower the Levelized Costs of Energy (LCOE) from the existing US$ 0.20/kWh-0.45/kWh for tidal and US$ 0.30/kWh-0.55/kWh for wave energy.[89] The LCOE can further be reduced by the provision of an efficient interconnected grid as well as robust supply chains in this sector.

Given the vulnerabilities of BoB economies to extreme climate events, the issue of Humanitarian Assistance and Disaster Response (HADR) also becomes important as it is a post-disaster task comprising of rehabilitation of climate disaster victims as well as rebuilding the infrastructure.[90] The countries in the Bay must cooperate and build their HADR capabilities, and the Indian National Centre for Ocean Information Services (INCOIS) can coordinate. The adaptation strategies must be driven up based on the Global Goal on Adaptation (GGA) to improve the adaptive capacity, increase resilience, and be less susceptible to climate disasters. The BIMSTEC can lead the creation of a fund to aid adaptation and promote climate-resilient development in the region. [91]

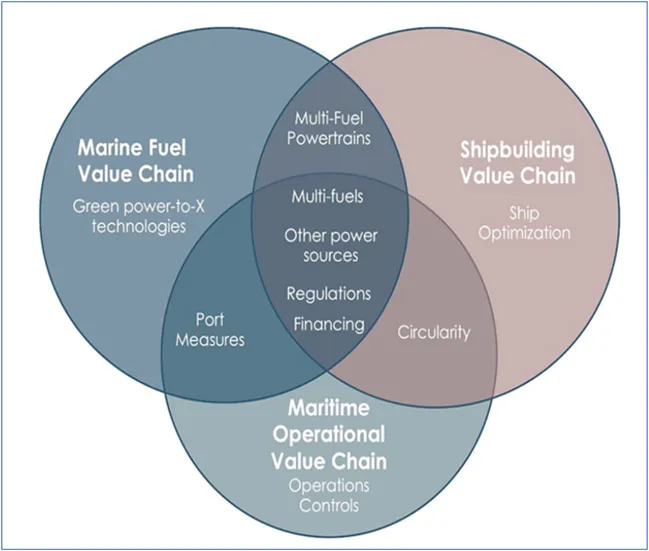

When expanding maritime connectivity, it is imperative that the high fossil fuel-dependent maritime industry is decarbonised in the region as its emissions are not considered in the nationally determined contributions (NDCs) of the countries.[92] Decarbonisation of the maritime industry is dependent on three main value chains (see Figure 5): the first is the fuel chain, where the non-availability of a green fuel chain has forced vessels with dual-fuel engines to run primarily on conventional fuels. The countries in the Bay must cooperate with one other in the development of low-carbon/zero-emission fuels such as Liquefied Natural Gas (LNG), green methanol, and green hydrogen.[93]

Figure 5: Value Chains and Select Decarbonisation Enablers in the Maritime Industry

Source: UNCTAD, Transport and Trade Facilitation Newsletter[94]

The second component is the shipbuilding chain where R&D is required in making the ships more energy-efficient and less polluting. Possible avenues to do this are through optimising the hydrodynamic hull design, utilising wind while sailing, multi-fuel engines, technology-based solutions that can provide efficient routes and port operations and incorporating circularity in the design and construction process.[95] Similar to the carbon credit system introduced by India in the domestic market, the other countries in the Bay can also institute a carbon credit system that will incentivise shipbuilding to transition to a low/zero emissions system.[96]

The operational aspect of the maritime industry is the third component, which includes fueling, loading, and travelling. The countries in the region can enable decarbonisation by developing infrastructure in their ports to facilitate the storage of alternate fuel systems. The ship operators must be incentivised to manage the size and speed of their fleet, incorporate hydrodynamic design and dual-fuel engines, and use more green fuels.

Finally, the implementation of the 2030 Sustainable Development Goals in the region requires collaboration between all stakeholders across the BoB littoral countries. The SDG 17 (Partnership for the Goals) aims to “strengthen the means of implementation and revitalise the global partnership for sustainable development.”[97] The pandemic should not lead to calls for the SDGs to be revised but instead be used as a catalyst for collaboration in the Bay.[98] It brings to the forefront issues related to access: the consequences of not having adequate healthcare; not having potable drinking water and sanitation facilities; and not having basic civil rights for immigrants, among others. A universal roadmap for resilient societies in the BoB should take into account the three broad pillars of sustainable development—people, planet, and prosperity—with the overarching objective to “leave no one behind”.

Conclusion

Globalisation, historically envisaged as an all-encompassing arrangement, has no doubt led to greater regional and global integration. It has opened up channels of international trade in goods and services, paved the way for the vertical disintegration of production lines and enhancing comparative price advantages, greater market access, financial market liberalisations, and knowledge spillover as well as spread of technological innovations. Supported by market-driven policies, this has generated a steep increase in average income levels and overall economic development.

However, current geo-political and geo-economic contexts have pushed the global economic order to the cusp of a transition—necessitating that countries find a balance between the contending forces of ‘localisation’ and ‘globalisation’. The threats posed by China’s economic expansion and integration into the GVCs, the tensions generated by the US-China trade wars, the supply chain disruptions emerging since the onset of the COVID-19 pandemic and further exacerbated by the Russia-Ukraine conflict—have all heightened the intent of Global North countries to uphold their industrial sovereignty and look inward to reduce over-reliance on the Chinese economy. This, however, has economic implications for the entire South Asian and Southeast Asian regions.

To turn the tides favourably, India can play an active role in the creation of ‘glocalised’ models of economic partnerships, encouraging robust regional ties among the littoral countries in the BoB. The region has immense potential in building self-reliance of regional value chains across sectors such as food, energy and technology, which can be harnessed with targeted policymaking. As India prepares to overtake China in 2023 as the most populous country and emerge as a regional economic power, it can take the lead in bringing all stakeholders to the table to create the conditions necessary for developing these regional value chains in the BoB littorals. [99]

In the food sector, regional partners must collaborate to set up safeguards against food shortages that result from crises elsewhere, build regional strategies for transformation of agriculture, and ensure sustainability of food systems. Moreover, the Indian experience with renewable energy can be leveraged for the creation of self-reliant energy markets in the region that will mitigate Chinese influence in the global renewables market. In the domain of technological advancements, regional collaboration for digital upskilling and investments in innovation remain imperative for the region’s technological integration into the GVCs.

To achieve all this, a prerequisite is smooth connectivity, with investments focusing on maritime connectivity promising the most returns. Creation of multi-modal connectivity networks within and from the BoB region to the rest of the world can enable better trade facilitation, and reductions in associated trade costs; in turn, these will incentivise increased bilateral or multilateral flows between the BoB countries and the US or the EU.

While setting out to achieve these economic goals, the BoB countries must adopt a comprehensive approach where carbon neutrality and inclusive development are embedded in all future policies. The priorities being highlighted by the Indian G20 Presidency too, caters to these three goals of efficiency, equity and environmental sustainability. As such, while facilitating global dialogue on how to achieve these goals for the world at large, India can represent the priorities of the BoB region and work to facilitate solutions for a smooth transition to a model of ‘glocalisation’ based on the self-reliance of regional value chains within the ambit of a global economy.

At the outset, however, India’s geo-political presence in the region assumes a critical significance, especially for the bilateral relationships among the BoB littoral countries. First, while disengagement from Chinese-dominated value chains might be feasible for the Global North, the story is different for the BoB countries (including India) given the direct challenge posed by their geographical proximity with China. For instance, most countries in the region already have expansive trade ties and inter-connected connectivity networks with China. Decoupling from these networks would entail significantly more costs for the developing countries in the region. Second, the China and India factor operating in the BoB region is significantly more complex. For relatively smaller nations in the region, these two players serve to counterbalance the regional dominance. It will be crucial for India to consider this factor through the process of development of these regional value chains at its initiative, in order to ensure their sustainability and best protect its own interests.

Soumya Bhowmick is Associate Fellow at ORF’s Centre for New Economic Diplomacy.

Debosmita Sarkar is Junior Fellow at ORF’s Centre for New Economic Diplomacy.

The authors acknowledge former ORF intern Aravind J Nampoothiry at NLSIU, Bengaluru for his research assistance.

The views expressed above belong to the author(s). ORF research and analyses now available on Telegram! Click here to access our curated content — blogs, longforms and interviews.

Soumya Bhowmick is a Fellow and Lead, World Economies and Sustainability at the Centre for New Economic Diplomacy (CNED) at Observer Research Foundation (ORF). He ...

Read More +

Debosmita Sarkar is an Associate Fellow with the SDGs and Inclusive Growth programme at the Centre for New Economic Diplomacy at Observer Research Foundation, India. Her ...

Read More +