Latin American companies that have invested in India since the 1990s have had varied experiences: some have achieved considerable success and remain in business, while a number of them have exited. This paper is a primer on enterprises from the Latin American region that have engaged the Indian market in the past 30 years. It finds three key factors that have pulled these businesses into India: the country’s myriad value chains, the massive consumer market, and the vibrant services sector. The collective experience of Latin American investors in India can provide lessons for the government as it aims to attract more foreign investments.

Attribution:

Hari Seshasayee, “Latin American Investments in India: Successes and Failures,” ORF Occasional Paper No. 321, June 2021, Observer Research Foundation.

Introduction

In 2020, foreign direct investment (FDI) inflows to India reached US$57 billion, a 13-percent rise from 2019.[1] The allure of India’s massive consumer market and expanding middle class, which is estimated to reach 583 million people by 2025,[2]remains a key pull for investors. As corporate revenues and profits fell owing to the fallout of the COVID-19 pandemic, company valuations declined, providing a boon for those on the lookout for mergers and acquisitions (M&A). Foreign investors betting on India’s future set their sights on the country’s consumer brands, e-commerce and infrastructure companies, primarily through M&As. This was a quicker and arguably safer way to enter the market. As a result, cross-border M&As increased by 83 percent in India in 2020, rising to US$27 billion. The most notable was Facebook’s 10-percent acquisition in Jio Platforms, for a hefty US$5.7 billion.[3]

Latin American companies are among those that have made recent inroads to the Indian market. Following initial negotiations towards the end of 2020, the Mexican bread and bakery multinational, Bimbo Group, acquired India’s iconic Modern Foods, the first Public Sector Undertaking (PSU) privatised by the Government of India in 2000.[4]With little fanfare, by February 2021, Bimbo has effectively become the largest bread company in India, edging out its chief competitor, Britannia Industries. This is Bimbo’s second acquisition in India, following its buyout of Ready Roti Limited’s Harvest Gold brand in 2017.[5]

While Bimbo’s acquisition of Modern Foods may not make headlines, it deserves some attention. In its heyday, as the first branded bread company in India and one of the country’s illustrious PSUs, Modern Foods held 40 percent of the national bread market. This was before it was sold to Hindustan Unilever Ltd in 2000, and later to Everstone Capital in 2016.[6]Today, it is safe with Bimbo, the world’s largest bread company with annual sales of US$15 billion, 203 manufacturing plants, and nearly 3 million points-of-sale across 33 countries.[7]

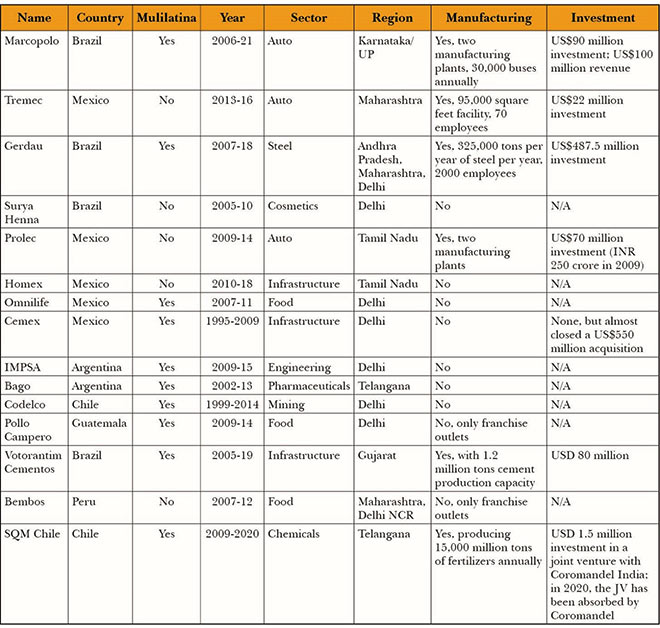

However, not everyone can prosper during times of crises. Some investors are forced to cut their losses and exit investments. This was the case with Marcopolo, a bus manufacturing company from Brazil. Through its joint venture (JV) with Tata Motors in 2006, Marcopolo invested US$90 million, manufacturing some 30,000 buses annually from plants in Dharwad, Karnataka and Lucknow, Uttar Pradesh. Millions of Indians ride the Tata-Marcopolo buses, from passengers in public transportation buses in Delhi and Mumbai to children in private school buses equipped with GPS trackers and CCTV cameras. Still, in late 2020, Marcopolo announced its exit from India by selling its 49-percent stake for a meagre US$14 million to its JV partner, Tata Motors.[8]

Bimbo and Marcopolo are two examples of multinational companies from the Latin American region (or simply, Multilatinas[a]) who have a penchant for the Indian market. Their experiences are illustrative of the mixed success of Multilatinas in India: some have achieved considerable success over the medium or long term, while others have endeavoured but ultimately given up.

This paper studies 50 Latin American companies that have invested in India since the 1990s. The companies are classified by country of origin, sector, manufacturing capacity, and the scale of investment. So far, 15 companies have exited or sold their investments to Indian partners, while the remaining 35 continue to strive to succeed in what is arguably one of the world’s most competitive and challenging corporate environments.

Their collective experience holds lessons for foreign investors interested in the Indian market. This is especially true for those from developing countries that may find certain familiarities in India, be it the large rural consumer base, relatively lower levels of financial inclusion, competitive prices, complex tax systems, or an unrelenting bureaucracy. There are lessons here for the Government of India too, specifically on the motivations behind these foreign investments and the sectors that hold most potential for investment. Also, the potential Indian joint venture partners and Indian companies looking for foreign capital can learn about the nuances of foreign partners’ motivations and how to utilise their expertise to leverage local and regional markets.

The Story of ‘Multilatinas’ in India

The term ‘Multilatinas’ was first used in 1996 in a magazine,América Economía,[b]which in the same year began publishing lists of the top 100 Latin American companies in the region. These include the region’s top companies in varied areas—from energy and infrastructure, to agro-industry and telecommunications; they all enjoy varying degrees of success.

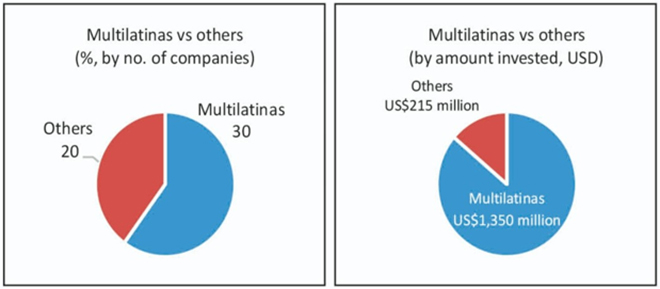

Thirty of the 50 Latin American companies in India are Multilatinas, while the remaining are mostly the region’s small and medium-sized enterprises (SMEs). Though the SMEs do not belong to the Multilatinas category, they still maintain a considerable international footprint. The Multilatinas make up the large majority (86 percent) of the total US$1.56 billion investment by Latin American companies in India (see Figure 1).

Figure 1: Multilatinas Investing in India

Source:Author’s own calculations, based on primary research

Many of these Multilatinas can compete globally, be it in India, China, Europe or the Americas. For some, such as Peru’s Grupo AJE, which squares off against Coca-Cola and Pepsi, or Mexico’s Cemex, the third-largest cement producer in the world,[9] the Indian market forms only part of their global ambitions. This is also why some of the Multilatinas that fail in India can afford to leave, while relying on other markets in Asia to hedge their losses. For instance, the 10 Multilatinas that have so far closed or sold their India businesses, even after investing US$619 million in the country, have sizeable operations in China, Southeast Asia, and other emerging markets. On the contrary, smaller Latin American companies that invest in India tend to persevere despite losses, as they cannot afford to simply write-off their investments. Also, most of these SMEs have only a small presence in other Asian countries. As a result, the ratio of Multilatinas that continue to stay in India versus those that have exited is currently 2:1. The ratio of other Latin American investors (non-Multilatinas) is 3:1 (15 companies continue to stay in India, five companies have exited).

Drivers of Latin American Investments in India

The story of Latin American investments in India runs parallel to that of the country’s economic growth. India’s gross domestic product (GDP) grew at an impressive average of 7.5 percent in the first decade of the 21stcentury.[c]Prior to the global financial crisis, India’s FDI inflows rose from a paltry US$3.5 billion in 2000 to US$43.4 billion in 2008.[10]

Some Latin American companies took notice of India’s growth story and decided to invest in the country. The first to do so were mining, automobile and service companies, all of which held dominant market positions in their home countries as well as in the larger Latin American region. Soon, companies vying for the Indian consumer market followed, in the food, entertainment and fashion segments. A host of companies specialising in engineering and machinery also joined India’s manufacturing value chains. Most investors from the Latin American region came from Brazil and Mexico, while a handful made their way from Argentina, Chile, Colombia, Guatemala and Peru. Their interest in India can be categorised broadly thus:

Value Chains:The primary motivation is to be part of India’s myriad value chains, including in automobiles, engineering, chemicals, and extractive industries. These investors usually look at establishing themselves in the long term and are willing to risk short-term losses. They are ready to infuse a sizeable amount of capital and often invest in manufacturing plants. These relatively cost-effective investments[d]sometimes position India as the hub for a broader Asian regional value chain, as companies often export from India to clients in East and Southeast Asia. Those in extractive industries provide services to India’s northern and central mineral belts; auto-part companies cater to India’s automobile manufacturing hubs in Chennai, Jamshedpur and Pune; and engineering and chemical companies supply the vast industrial corridors that run across the length and breadth of India. Most Latin American investors in India form part of this primary group. Thirty companies have invested in total, nine of whom have exited or closed their India operations. These companies form a diverse group, ranging from electrical motors and ATM machines to autoparts and centrifugal pumps. Notably, most of these companies maintain manufacturing facilities in India. These companies have invested nearly US$1 billion in India. However, a large chunk of investors, including Gerdau (Brazil’s largest steel producer), Votorantim Cimentos (Brazil’s largest cement company) and Tremec and Prolec (two Mexican autoparts companies) have sold their stakes to local Indian partners.Sustaining in India’s value chains is a tough prospect even for Indian companies, so it comes as little surprise to see foreign investors opting to cut their losses by exiting. Still, many have already spent decades in India and are well-established in their respective value chains. Mexico’s Katcon, for instance, began constructing a manufacturing plant for catalytic converters and exhaust systems in 1996; till date, they have produced and sold more than 2 million units.[11]The relative success of these companies in numerous value chains, along with India’s rapid industrialisation, has spurred more Latin American investments. This can also be seen as an example of the synergies between Indian and Latin American industrial value chains, each bringing their own expertise and catering to domestic, regional and global clientele, from Latin America to Middle East, Southeast Asia, and East Asia.

Consumer Base:The next group of investors are those that are lured by India’s massive consumer base. The sheer size of the Indian economy (estimated by the International Monetary Fund [IMF] to reach US$3.05 trillion in nominal GDP by 2021)[12]and the massive population of 1.4 billion people (exceeding that of Europe and North America combined)[13]is an enticing prospect for most companies. An entry into the Indian market could mean significant long-term profits, which is unimaginable in any of the Latin American countries. At the same time, however, there is cutthroat competition in India’s market, and only a few survive in the long run. In addition to domestic contenders, various international companies compete for India’s enormous consumer base. It can be a difficult task for any foreign investor to comprehend and adapt to the Indian consumer’s peculiarities, including numerous regional and linguistic distinctions, demands in quality and pricing, and the brand’s image and ability to connect with the consumer. In the early stages of investment, it is essential for companies to study and understand the truly diverse profile of the Indian consumer. In the long-run, no foreign investor is likely to succeed in India without vast amounts of gumption. Mexico’s Cinépolis has had much patience and a truly long-term vision, since opening its first screen in India in 2009. They began cautiously with multiplexes in Tier II and Tier III cities, such as Ambala, Bhatinda, Dibrugarh, Hubli, Kota and Panipat and learned from these small operations before setting their sights high. They not only acquired 100 screens from Fun Cinemas and DT Cinemas, both recognised brands in western and northern India, respectively, but also built their own cinema halls. Others like Mexico’s KidZania, which establishes ‘edutainment’ centres for children, have been quite innovative in their India approach.

Peru’s Grupo AJE, the fourth-largest producer of non-alcoholic beverages in the world, which has presence in 14 Asian countries, including China, Thailand and Vietnam, has used its considerable international experience to formulate a suitable strategy for India. However, not all companies have the amount of time and patience that Cinépolis has shown for India, or the innovative spark of KidZania, or the vast global experience that Grupo AJE brings with it. It is no wonder that five of the 13 Latin American companies that were tempted by the Indian market exited just within a few years of their entry. Of the eight that remain, three have already been in the Indian market for more than a decade—Cinépolis, KidZania and Grupo AJE—and are models worthy of emulation. Some of the newcomers have already shown promise. For instance, Alpargatas, with its celebrated Havaianas flip-flops, has managed to establish its brand in India in just two years’ time, and its products are now available across 176 retail stores in India.

Services:A third group of investors are drawn to India’s vibrant service sector. As India’s Economic Survey 2020-21 indicates, “the services sector accounts for over 54% of India’s Gross Value Added (GVA) and nearly four-fifths of total FDI inflow into India.”[14]India’s service sector is gigantic and besides the plethora of local firms, whether in information technology (IT), financial services, real estate or hospitality, there is plenty of foreign competition to contend with. This sector has the least number of Latin American companies, totalling only seven. Six of these seven companies are still in India. The one company that closed its offices, Argentina’s IMPSA, continues to maintain a steady client base in India. Three of Latin America’s largest IT companies, Globant from Argentina, Stefanini from Brazil and Softtek from Mexico, have managed to increase their presence in India over the past two decades. Together, these three companies employ nearly 3,000 staff in India’s tech clusters in Bengaluru, Hyderabad, Noida and Pune, and have invested more than US$32 million. There are few other niche Latin American companies that provide services to India’s extractive industries, health sector and engineering firms. One such company is Techint, a globally renowned engineering and construction company with 180 employees in Mumbai, who have executed projects across the globe, from methanol plants in Egypt and natural gas terminals in France to a nuclear power plant in the Czech Republic and a steel pipe rolling mill in Texas, US.[15]Techint is a compelling example of a Latin American company using India as a hub not for manufacturing exports but for service exports, specifically in high-value sectors such as engineering. Given that the service sector is generally more people-centric, as opposed to manufacturing or value chains, which are capital-intensive, the total value of investment tends to be lower.

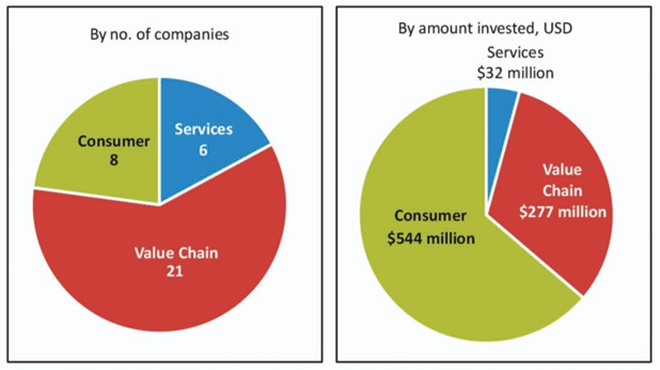

One potential addition could be startups looking for cross-border opportunities in similar developing economies. Companies from Latin America’s accomplished food and beverage sector are also eying India’s growing consumer market. Moreover, the pace of India’s industrial growth is bound to expand value chains and spur new opportunities for foreign investors of all sizes and appetites, including from Latin America. India’s service sector also has immense potential for future Latin American investment, especially given the dual advantages of nearshoring and offshoring to maintain operations round the clock.[e]Although a majority of the current Latin American investors (21 companies) in India are those present in value chains, the companies targeting the Indian consumer invest nearly double the amount in comparison (see Figure 2). This is because the large consumer base demands a high level of investment to capture the burgeoning middle class.

Figure 2: Current Latin American Investments in India, by type

Source:Author’s own calculations, based on primary research

Regional and Country-Specific Trends

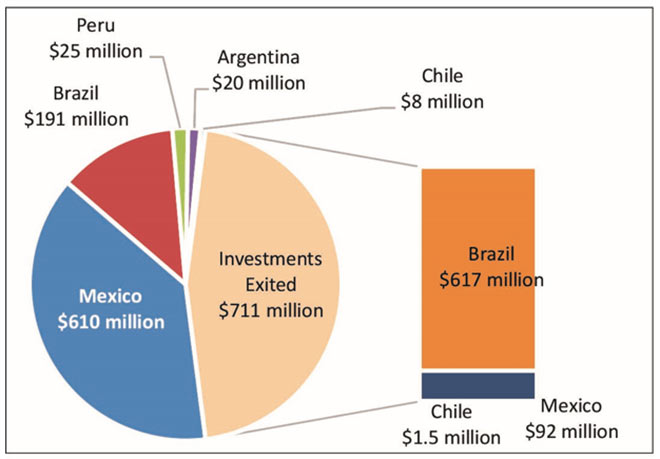

Most Latin American companies investing in India tend to be from the region’s two powerhouses—Brazil and Mexico, the ninth and fifteenth largest economies in the world by nominal GDP.[16]Roughly half of the total investments from Latin America have been made by Brazilian companies, at US$808.5 million. But a sizeable amount, US$617.5 million, has been sold off to Indian companies after more than a decade of operations in India. So far, Mexican companies seem to have had a more positive experience in India. They have invested US$702 million since 1995, and have divested only US$92 million.

Of the 50 Latin American companies that have invested in India over the past three decades, 18 are from Brazil, while 14 are from Mexico, comprising nearly two-thirds of the total (see Figure 3). The remaining are from Argentina (6), Chile (5), Peru (5), Colombia (1) and Guatemala (1). These numbers mostly correlate with the relative size of their economies, with a few minor exceptions. More importantly, for nearly all these companies, India is not their only major investment destination in Asia. Most of these companies are also present in East and Southeast Asia. Much of the total investment, i.e., US$1.56 billion has come from Brazil (51%) and Mexico (45%), with the remaining five countries contributing just US$54.5 million (see Figure 3).

Figure 3: Current Latin American Investments in India, by country

Source:Author’s own calculations, based on primary research

Given the scale of investments by the two Latin American giants, the regional and country-specific trends have been classified under Brazil, Mexican and other Latin American countries:

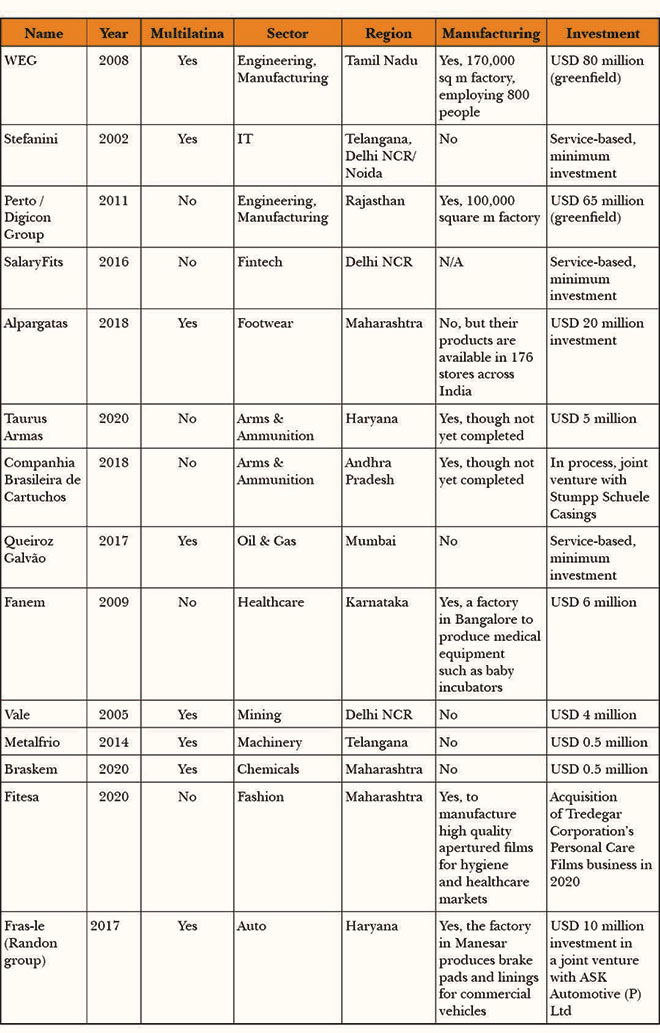

Brazilian investments in India:Across sectors, a total of 18 Brazilian companies have invested in India since 2002. Of these, 14 continue operating in India (see Table 1), while four have exited the country. Out of these 14, 11 companies are part of different value chains in India and form a diverse group. Their success thus far is an encouraging sign for the relatively new Brazilian companies in India. Of the remaining three companies, two provide different services to the Indian market, while one company, Alpargatas, courts the Indian consumer. In comparison to the companies with manufacturing units, the operations of these three companies are much smaller in scale; however, they have so far fared reasonably well and have much scope for expansion.

Table 1: Current Brazilian Investments in India

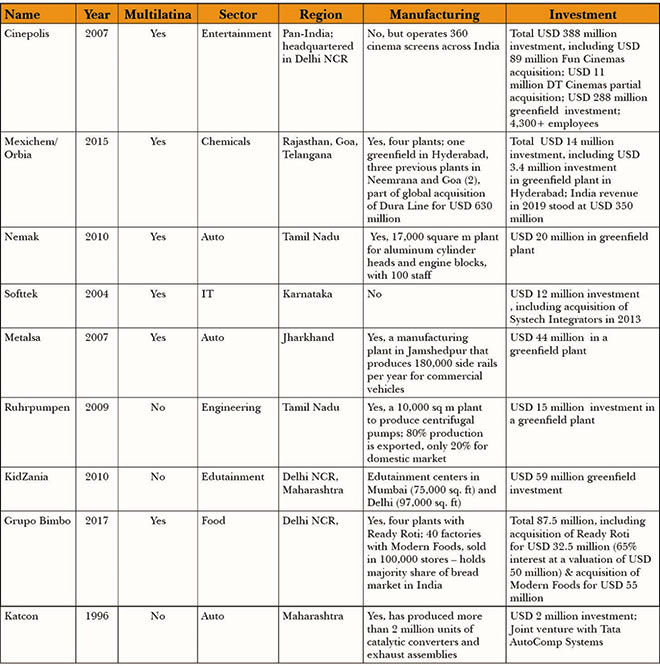

Mexican investments in India:At present, Mexico is the largest Latin American investor in India, with a current FDI stock of US$610 million. Fourteen Mexican companies have invested in India since 1995, of which nine currently maintain operations in India (see Table 2), while five have shut their offices or manufacturing facilities in the country. Five of the current nine form part of the automobile, chemicals and industrial value chains, all with relatively large manufacturing units and total investments nearing US$100 million. Till date only one Mexican company, Softtek, has entered India’s services market. However, the most impressive are the three Mexican companies that directly court the Indian consumer—Cinépolis, which has invested US$388 million in India, operates 360 cinema screens and employs more than 4,300 people across India; KidZania, which maintains edutainment centres of 75,000 sq. ft. in Mumbai and nearly 100,000 sq. ft. in Delhi; and Grupo Bimbo, presently India’s (and the world’s) largest bread maker.

Table 2: Current Mexican Investments in India

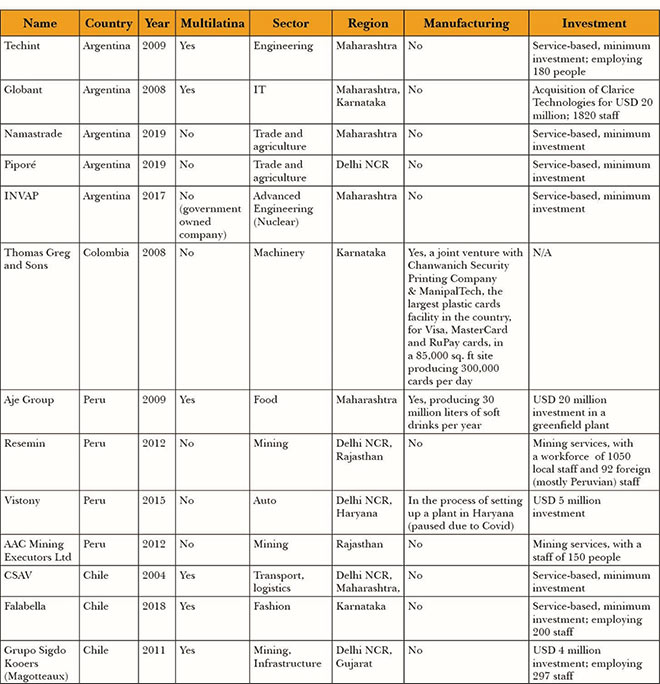

Other Latin American investments in India:Besides Brazil and Mexico, a handful of Latin American countries have invested in India. While these are not large investments, such as those by Cinépolis or Marcopolo, they remain significant and have gained momentum over the past decade. Between Argentina, Chile, Colombia, Guatemala and Peru, 18 companies have invested in India, of which six have closed operations (see Table 3). Of the 12 companies that remain in India, four each are from Argentina and Peru, three from Chile and one from Colombia. Of the four Argentine companies, two are large Multilatinas, Techint and Globant, that provide services to the Indian market; while the remaining two are SMEs with representative offices meant to help increase exports to India. The four Peruvian companies in India have a decent presence in their respective fields. Peru’s AJE Group, however, stands out with US$20 million invested in a manufacturing plant in Maharashtra, which since 2010 produces 30 million litres of soft drinks annually. The other three companies from Peru are part of the mining and automobile value chain. The three companies from Chile provide different services, though they are yet to scale up their businesses in India to match their Latin American counterparts. The lone Colombian firm in India has an impressive JV with ManipalTech and a Thai partner to produce 300,000 plastic cards per day for clients such as Visa, MasterCard and RuPay cards. Still, the total investment of these firms is just a notch above US$50 million, because only three of these companies currently have manufacturing facilities in India, while the rest focus on services and increasing exports to Indian clients.

Table 3: Current Investments from other Latin American countries in India

The Other Side: Missteps in Latin American Investments in India

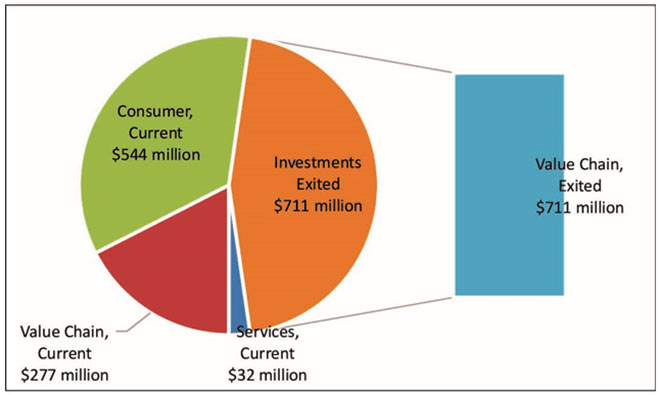

The story of the 35 Latin American companies currently operating in India would be incomplete without that of the 15 on the other side of the aisle, which gave up on their India plans. Of the total US$1.56 billion that Latin American companies have invested in India; 15 companies have left—these invested US$711 million, or about 45 percent of the total investments (see Figure 4). Why did these companies exit and what can other foreign investors learn from these experiences? Are there any discernible trends of the Latin American divestments or exits from India? These questions are worth probing and merit further examination.

Figure 4: Total Latin American investments in India, by type (value of investment, US$)

Source: Author's own calculations, based on primary research

The first observation is that all the large exits have been by companies that invested in India’s myriad value chains with large manufacturing units. It can be a truly cumbersome process to navigate India’s bureaucracy to secure all the required permits, manage a large labour base, iron out differences with JV partners and still make a profit. Most of these Latin American companies endured difficulties and gave up only after about a decade. It is worth studying the five largest exits (cumulatively worth US$710 million) in the value chain—three from Brazil and two from Mexico. This could shed more light on why such large-scale projects ultimately failed.

1. Brazil:

Gerdau: The Brazilian steelmaker entered India through a JV in 2007 with Kalyani Steel, and both companies soon acquired SJK Steel. With a production capacity of 300,000 tonnes of rolled steel, the plant employed 3,000 people at its peak. After a whopping US$487.5 million investment—by far the largest Latin American investment in India—the company posted a net annual income for the first time in March 2016, after nearly a decade of losses. In 2018, Gerdau sold 100% of its stake to ADV Partners, an Asian private equity firm, for only US$120 million, noting that it had “decided to exit from non-strategic markets and assets in a bid to focus on Latin American and North American markets and assets.”[17]India’s extractive industry is notoriously difficult for foreign investors, and the experiences of steel companies, such as ArcelorMittal and Posco, both of which abandoned their plans, are proof that Gerdau’s exit is likely part of this trend.

Marcopolo:It had a JV for nearly 15 years with Tata Motors to manufacture buses, but finally announced its exit in late 2020. They got most things right: partnered with a highly credible and reputed company, operated a top-class manufacturing facility and managed to secure some of India’s most high-value clients, including numerous state governments. In just a few years’ time, Tata-Marcopolo buses dotted the streets of India. The company did face challenges, some of which can be attributed to the general slowdown in India’s automobile sector, but more important was the strong competition from local bus-maker Ashok Leyland, currently the market leader with a 45% share.[18]Still, Marcopolo’s exit leaves some questions unanswered and is a tale of caution even for large, globally competitive Multilatinas.

Votorantim Cimentos: This company was eyeing the large Asian cement and construction market, specifically India and China, since 2005. In 2012, they entered India through an acquisition and asset swap with Cimpor, a Portuguese cement group,[19]for the Gujarat-based Shree Digvijay Cement and its Kamal Cement brand. Their plant in Jamnagar produced 1.2 million tonnes of cement per year and employed 300 people. Nevertheless, as theEconomic Timesnoted in its April 2018 article, “the Brazilian promoters failed to turn around the company in the past eight years when other midlevel Indian cement companies had done extremely well.”[20]When Votorantim took over in 2012, the company made a net profit of US$9 million. By 2017, however, they posted a net loss of US$1.25 million. By April 2019, Votorantim Cimentos sold its 75% stake to True North, a private equity firm in India, for US$22 million,[21]about half the value of their initial investment.

2. Mexico:

Two of Mexico’s autoparts companies, Tremec and Prolec, decided to exit after a relatively short period of time. Both these companies had manufacturing units in India. Tremec, which opened its manufacturing plant in Pune for rear-wheel drive transmission and drivetrain components in 2013, closed by 2017. The company was unable to compete against local prices and was producing technology that did not suit the needs of the then Indian market. However, unlike the other Mexican autoparts companies currently in India, Tremec did not have a confirmed long-term client or a JV partner. Prolec, on the other hand, had quite a different experience. Itself a JV between General Electric and Mexico’s Xignux, Prolec entered India in 2009 through its acquisition of Indotech Transformers for US$70 million. After a decade of mixed results and losses, they sold their majority stake for only US$10 million to Shirdi Sai Electricals Limited.[22]

Besides these five companies, comprising 99 percent of the total investment value of Latin American divestments from India, a few other smaller operations and representative offices have also shut shop over the past two decades. These include Cemex, one of the world’s largest cement and building material companies, which nearly acquired the Nagpur-based Murli Industries for US$550 million, and reiterated even in 2018 its continued interest in the Indian market.[23]

Chile’s SQM, a global supplier of plant nutrients, lithium and chemicals, and one of the largest lithium producers in the world, entered India through a JV in 2009 with India’s Coromandel International, part of the Murugappa Group. By 2012, they inaugurated a 15,000-metric tonne manufacturing facility in Kakinada, Andhra Pradesh, to produce fertilisers. However, the company decided to sell its stake to its JV partner, Coromandel International, at a loss of US$643,000, and exit the market. Another Chilean company, Codelco, a mining behemoth and the single-largest producer of copper in the world, mining 1.7 million tonnes annually and accounting for 6 percent of the global copper reserves,[24]opened an office in Delhi, represented by Trikona Services, way back in 1999.[25]India is a natural partner for Chilean copper, and about 60 percent of India’s copper ore is currently sourced directly from Chile, with Codelco being the main supplier.[26]After about 15 years in operation, they closed their office in India,[27]and now manage sales directly from the headquarters. While the closure of their office has not stopped exports of copper ore to India, if they had stayed on, they could certainly have had a larger footprint in the country.

Besides those in the value chain, six other Latin American companies have also exited their India offices. Five of these had targeted the Indian consumer and one the service sector. Omnilife, a large Mexican multi-level marketing company that distributes dietary supplements, never managed to take off in India as the country deems such ‘network marketing schemes’ as illegal under the Prize Chits & Money Circulation Schemes (Banning) Act 1978.[28]

Two Argentine companies, Laboratorios Bagó (a pharmaceutical company with 148 patents and sales across 50 countries,[29]opened an office in Hyderabad and even had an agreement to market products to Southeast Asia) and IMPSA (a high-tech service company specialising in renewable energy, extractive industries and even nuclear power, had opened an office in Gurgaon) had to close their respective offices. They, however, remain interested in the Indian market and continue to engage with Indian clients.

Perhaps most illustrative are the experiences of two food companies from the Latin American region courting Indian consumers—Peru’s Bembos (a burger chain that out-competes McDonald’s and Burger King back in Peru) and Guatemala’s Pollo Campero (a chain of fried chicken restaurants akin to KFC that serves about 80 million customers annually across 12 countries). Both opened franchise outlets in the late 2000s in India, but were unable to cultivate a strategy to win over Indian customers. With outlets in the hyper-competitive megacities of Delhi and Mumbai, where restaurants are often destined to fail, clubbed with a lack of brand recognition in India, it was never an easy prospect to begin with. Perhaps a better strategy could have been to enter in smaller, less competitive environments, such as Pune and adapt their products to the Indian palate, as KFC did with its large vegetarian offer. In the meantime, the companies should have invested in marketing to build brand recognition.

Table 4: Latin American investments in India, now exited or sold to Indian partners

Lessons from Latin America’s faux pas in India

Overall, there is little that ties together the 15 Latin American companies that have exited from India. The larger investors with manufacturing units witnessed failures with or without JV partners. Some of the companies became entangled in India’s bureaucratic web, specifically those dealing directly with the central and state governments; others succumbed to the fierce competition in India’s massive consumer market. A more in-depth study could reveal gaps in management decisions, legal and tax issues with mergers and acquisitions, and sometimes simply the inability to adapt to local realities. Some companies, such as Codelco and IMPSA, continue to work closely with Indian clients from their headquarters or through other regional offices.

The lapses of the three large Brazilian companies provide a lesson in caution and patience for the Indian market. The numerous challenges India poses can be quite overwhelming, even for large companies that possess capital. Marcopolo and Gerdau both had local partners, yet they chose to exit after a decade of rather moderate performance and multiple years of losses. Votorantim, on the other hand, had no local partner and exited just six years after their acquisition. All these three companies entered the Indian market with manufacturing facilities and were an integral part of the value chains in their respective sectors and the states they invested in. The exits of Gerdau, Votorantim Cimentos and Marcopolo (totaling US$617 million) need further probing. What is clear is that they are not encouraging signs for future Brazilian investors (see Figure 5).

Figure 5: Total Latin American investments in India, by country (value of investment, US$)

Source: Author's own calculations, based on primary research

The Indian market is not for beginners. This is certain for all Latin American, and perhaps all foreign, investors. The sheer size of the Indian market and the competition it invites is a challenge for any investor. Two key lessons hold true for any foreign investor entering any sector in India:

First, think of India as acontinentrather than a country. After all, India’s population is larger than every single continent in the world, besides Asia. India’s myriad states are akin to countries. India’s largest state, Uttar Pradesh, has the same population as Latin America’s largest country, Brazil. There are vast differences in doing business from one state to another. Andhra Pradesh, which regularly tops India’s ease of doing business rankings, has so far been the destination of only 5 percent of Latin American investment in India. However, Delhi and Maharashtra, ranked 12thand 13th, respectively,[30]are the destination for nearly 50 percent of Latin American investments in India. Delhi and Mumbai, India’s largest cities, may be an obvious choice for setting up foreign offices, but less-populated cities like Bangalore, Chennai, Hyderabad or Pune may be a safer bet, at least to begin with. Latin American investors need to have an in-depth understanding of India’s 36 states and union territories, if they are to improve their chances of succeeding in India.

India is all about thelong game. If investors are looking for returns in the short or medium term, they are likely to be disappointed. For those in extractive sectors, transport and infrastructure, the long term may not even be a decade, but multiple decades. In addition, they need to be prepared for years of potential losses and be ready to infuse capital required to compete against other foreign and domestic players. Many foreign investors, and even start-ups reach break-even after years (or even decades) of starting their India ventures. The Multilatinas that have endured for more than a decade in India are now reaping the benefits of their patience and perseverance.

Conclusion

Latin American investors in India have thus far had mixed success, especially given the more recent exits of relatively larger Multilatinas such as Gerdau and Marcopolo. Still, there are 35 companies from the region that remain in India and are fighting for their share of the market. Even today, there is a healthy mix of Latin American investors with manufacturing units, those in the service sector, and others that bet on the Indian consumer.

Many Latin American investments in India have been through greenfield projects or joint ventures, while a smaller proportion have been through brownfield investments or acquisitions.[f]This is a good sign for India, which actively seeks greenfield or ‘new’ investments. The proportion of JVs is also healthy, at about a quarter of the total Latin American investments in India. Another important lesson, specifically for the Government of India, is that most Latin American investors come to India not because it is a destination for low-cost production or services, but rather they see it as a long-term market. Quite a few companies use India as a hub for their Asia clients, from the Middle East to Southeast Asia.

The Government of India can proactively work to accelerate the pace of Latin American investment, whether through entities like ‘Invest India’ or its embassies abroad. India can selectively target some Multilatinas that are keen on entering the market. Such a proactive approach is likely to yield more results, especially given that India’s embassies in the Latin American region are already short-staffed, with just a handful of diplomats handling a region of 650 million people. Entities like Invest India can also afford to include a Latin America desk to attract the numerous Multilatinas that are yet to enter India.

While FDI in some of India’s massive or labyrinthine sectors, like retail, defence, insurance and even e-commerce, can be cumbersome, most Latin American investments in India remain in the relatively uncomplicated sectors, such as engineering and machinery, automobiles, chemicals and entertainment. These sectors are free from FDI caps and onerous regulations. Yet, there remains much potential for Multilatinas and Latin American SMEs to invest in myriad sectors in India.

The biggest potential lies in food, where Latin American giants like JBS, Minerva, Agrosuper, Gruma, BRF Foods, Camposol and Nutresa can thrive, if they follow a cautious route and adapt to the taste of the Indian consumer. While there are many Latin American food and beverage companies that export products to India, only Grupo AJE and Bimbo have a significant physical presence in India. Chile’s retail giants such as Falabella, Ripley and Cencosud are yet to target the fast-growing consumer retail space in India. Others such as Cemex and Argos can be part of the more than US$1 trillion infrastructure investment, as India actively seeks to build its roads, highways and buildings. Another big opportunity lies in the financial sector, given that none of Latin America’s gargantuan banks have yet explored this space.

Although these cross-border investments are primarily commercial in nature, they also increase people-to-people exchanges and socio-cultural interactions between India and Latin America. It is part of the growth story of the Global South, of which India and Latin America remain an integral part.

About the Author

Hari Seshasayee is a Global Fellow at the Woodrow Wilson Center, and a trade advisor with ProColombia, a Colombian government agency. The opinions expressed within the content are solely the author’s and do not reflect the opinions of the Colombian government.

Endnotes

[a]‘Multilatinas’ is a term used frequently by economists, international financial institutions and consultancies to refer to Multinationals from the Latin American region. The Inter-American Development Bank defines Multilatinas as companies that have “leveraged domestic positions to expand their operations throughout Latin America.”

[b]A Chile-based print magazine and website,América Economíacovers everything to do with business, economics and politics in the Latin American region. It regularly publishes updated lists of Multilatinas.

[d]In comparison to other Asian markets in East and South East Asia, which require more capital and have higher labour costs.

[e]Both terms, nearshoring and offshoring, are specific to the IT sector. Nearshoring is the practice of outsourcing work to nearby countries, while offshoring refers to outsourcing to distant countries in different time zones. A company with offices in India and Mexico, for instance, could easily service clients in Asia from a Bengaluru-based office for one part of the day, while serving North American clients from a Mexico City-based office for the other half.

The views expressed above belong to the author(s). ORF research and analyses now available on Telegram! Click here to access our curated content — blogs, longforms and interviews.

Hari Seshasayee is a visiting fellow at ORF, part of the Strategic Studies Programme, and currently serves as an advisor to the Foreign Ministry of ...

PDF Download

PDF Download

Source:

Source: