-

CENTRES

Progammes & Centres

Location

PDF Download

PDF Download

Arjun Gargeyas, “India in the Era of ‘Silicon Diplomacy’,” ORF Issue Brief No. 593, December 2022, Observer Research Foundation.

Introduction

The semiconductor value chain is intricate and complex, with the ecosystem comprising multiple components such as raw materials for wafers, software licences and intellectual property (IP) for chip design, equipment or tools in the fabrication process, and different technical standards on assembly and packaging of final products. The manufacturing process of a semiconductor and chip[a] involves a number of supply routes and hand-changes before the final product is finally delivered. Therefore, countries recognise the necessity of multilateralism and the futility of any drive for self-sufficiency in the semiconductor industry. Even semiconductor powerhouses like the United States (US), Taiwan, and China are focusing on their areas of expertise in the supply chain and engaging in diplomatic engagements to offset their gaps in other areas. This has led to increased outreach between states to address issues at various stages of the semiconductor supply chain, in what is coming to be known as ‘techno-democratic alliances’.[b]

The biggest elephant in the room continues to be China’s rise as a semiconductor powerhouse. As the country seeks to cement itself as a leader in the global semiconductor ecosystem, other players are working to counter Chinese hegemony in such a critical industry. The United States, for example, in 2020 imposed an embargo on the export of American semiconductor technology to all Chinese semiconductor firms.[1]

Two years since, China appears to have remained the industry leader, as 19 of the top 20 fastest-growing semiconductor firms in the world are from China.[2] Under the ‘Make in China 2025’ initiative, the China Integrated Circuit Industry Investment Fund (also called the ‘Big Fund’), set up in 2014, has raised 140 billion yuan (approx. US$22 billion) for its first fund; it set up a second, roughly 200-billion-yuan fund in 2019 to support the domestic semiconductor industry.[3] Additionally, China has become the world’s largest importer of semiconductor manufacturing equipment over the last two years, with a growth rate of 58 percent in 2021.[4]

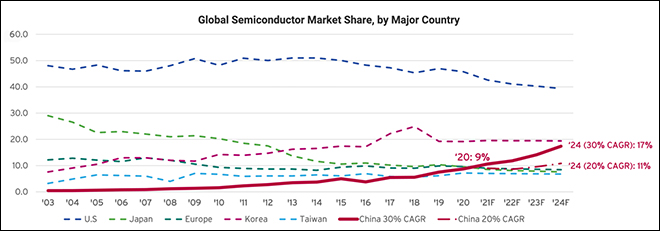

Indeed, China’s share in global chip sales surpassed that of Taiwan[c] two years in a row, and in 2020, the industry recorded a Compound Annual Growth Rate (CAGR) of 30 percent. If China maintains such a CAGR for the next three years—and assuming the growth rates of the rest remain the same—its share of the global market will increase from the current 4 percent to 17.4 percent, putting it behind only the US and South Korea.

Figure 1. Global Semiconductor Market Share Projection, by Major Country

In October 2022, the Biden administration imposed additional restrictions and export controls related to semiconductor products and equipment on China. While these sanctions effectively stop all American chip technology from reaching China, the long-term political and economic effects remain unclear, given the failure of previous sanctions to stunt China’s semiconductor growth. This has also put the limelight on other techno-democracies using diplomacy to stave off the Chinese semiconductor industry’s influence on the global semiconductor ecosystem.

India, for one, has created new policies to build its domestic semiconductor ecosystem. In December 2021 the government released the Semiconductor Fab Ecosystem Programme, covering all aspects of the supply chain.[6] The country is also reaching out to like-minded partners such as Taiwan to support them in financing and building the necessary infrastructure.[7]

Now that the era of silicon diplomacy has been kickstarted, it is imperative to understand the current bilateral diplomatic initiatives that help establish the sector as a unifier for technological powers.[8] The rest of this brief describes the proposed multilateral alliances between different states, examines the foreign policy decisions by specific powers related to semiconductors, and explores the public-private sector initiatives across countries that seek to strengthen the existing supply chain.

Current Techno-Democratic Alliances

The Quadrilateral Security Dialogue (or Quad, comprising India, Australia, Japan, and the US) has evolved from a purely strategic security dialogue to a more holistic alliance between the four countries in the Indo-Pacific. As the Covid-19 pandemic exacerbated the global chip shortage and exposed the bottlenecks and dependencies in the supply chain, the Quad in 2021 decided to include semiconductors as an area of collaboration.

The Quad leaders announced the ‘Quad Semiconductor Supply Chain Initiative’ at the September 2021 summit, designed to map capacity, identify vulnerabilities, and bolster supply-chain security for semiconductors and their vital components.[9] The initiative’s primary objective is to ensure a competitive market, prevent monopolies, and strengthen the current supply chain against future shocks. This is one of the first multilateral engagements to involve semiconductors as part of technology diplomacy. It bodes well for the initiative that each member has something unique to contribute to the efforts for strengthening the global supply chain.[10]

The US undoubtedly leads the world in chip design with its private sector design behemoths[11] (such as Intel, Qualcomm, NVIDIA and AMD). The country’s firms also own all Electronic Design Automation (EDA) software licences used in chip design.[d] Japan has expertise in the production of silicon wafers (substrates on which designs are imprinted) and semiconductor manufacturing materials such as photoresists or etching gas, and remains critical to the fabrication process. Meanwhile, Australia is an important source of minerals such as silica, gallium and indium, which are essential for developing silicon-based and composite semiconductor products.[12] India, for its part, can provide the required human resources, especially in the chip design services segment.[13]

The Quad states are therefore looking to utilise each of their respective comparative advantages in the semiconductor value chain to make their efforts on silicon diplomacy work.

In early March this year, news reports said the US government had proposed setting up a semiconductor industry alliance with its allies in Asia, including South Korea, Japan and Taiwan. The supposed aim is to keep mainland China’s fledgling semiconductor industry at bay.[14]

Examining the splits in the different countries’ contributions to the supply chain, there are clear winners. The US, being a design powerhouse holding all EDA tools licences, controls the fabless market[e] with its private firms. It has the most number of semiconductor fabrication facilities in the world. Taiwan is the global epicentre of semiconductor manufacturing, with over 60 percent of the world’s chips being manufactured by the country’s giants—Taiwan Semiconductor Manufacturing Company (TSMC) and United Microelectronics Corporation (UMC).[15] It also remains a hub for all Assembly, Testing, Marking and Packaging (ATMP) processes with its domestic firms like Foxconn and Winstron. For its part, South Korea is home to semiconductor behemoth Samsung, which has design and manufacturing capability. Lastly, Japan has dominance over the production of critical manufacturing equipment and materials such as photoresists.

The Chip4 alliance therefore covers all the key areas of the value chain, and these four countries can together run the semiconductor ecosystem with greater efficiency. A caveat, however, could prevent this alliance from making a mark in the supply chain: China and its market.[16]

In 2021, China imported US$350 billion worth of semiconductors, with the US and South Korea being its biggest suppliers.[17] As a major consumer of electronic goods, the exclusion of China from the export market will also significantly hurt the finances and profits of American firms.

One of the more interesting diplomatic engagements with regard to semiconductors was witnessed last year in the Trade and Technology Council (TTC) Agreement signed between the US and the European Union (EU).[18] The agreement aims to improve cross-border flow of goods and services across critical technology sectors, including the semiconductor industry. It seeks to address the vulnerabilities in the semiconductor supply chain while anticipating future shortages of the global chip supply.[19]

The allies aim to do this in two primary ways. One is to coordinate their respective chip investments so that they do not end up engaging in a ‘subsidy race’ to the bottom. In practice, this means that the US and EU are likely to share information with each other on issues such as their planned fab investments and the companies they plan to target. Cross-border information dissemination regarding the EU Chips Act and the US’s CHIPS and Science Act elucidates the incentives for boosting semiconductor manufacturing capacity for both parties. Ideally, they would want to reach a stage where the EU has enough production capacity for automotive chips. In contrast, the US would want to invest in production capacity for leading-edge nodes. In the future, the two parties could agree on preferential treatment for their own fabless companies to access the fabs in each other’s national jurisdiction.

The second area is to develop an early warning detection system for supply chain disruptions. This idea was earlier announced as part of the Quad Semiconductor Supply Chain initiative as well, where the four members agreed to “map capacity, identify vulnerabilities, and bolster supply-chain security for semiconductors and their vital components.” The motivation appears to be to keep a closer eye on wafer capacities across the globe so that stockpiling or additional capacity addition can be coordinated.

In the long run, subsidising semiconductor firms with the goal of achieving national self-sufficiency will continue to be counterproductive and futile. Futile in the limited sense that such measures will not achieve the aim of full indigenisation. Counterproductive because a sole focus on domestic subsidies would displace the opportunity to make a resilient, China-independent, cutting-edge semiconductor supply chain. The initiative as part of the TTC Agreement indicates the US’s and EU’s willingness to nurture collaborative efforts with partners.

Chips as a Political Weapon

Semiconductors and chips have become a political weapon in the recent years, as seen in like-minded states forming alliances, and the use of semiconductors as a punitive tool to hurt certain economies. Various restrictions have been imposed on exports, trade, and access to semiconductor technology that prevent certain states from moving up the value chain.[20] With semiconductors and chips being integral to the basic functioning of several sectors, these restrictions can potentially hurt the economies of these countries.

Export control mechanisms have been put in place for semiconductor technology considering its dual-use and military capabilities.[21] This is in the form of multilateral agreements such as the Wassenaar Agreement, under which more than 150 semiconductor products and 20 types of semiconductor manufacturing equipment are included as part of the export control regime. There is also the possibility of unilateral controls on countries’ export of emerging technologies. The best example is the US’s Export Control Reform Act (ECRA 2018), which identifies export controls essential for technologies directly related to the country’s national security.[22] Unilateral controls by a semiconductor giant such as the US can hamper the chances of other countries accessing critical materials and equipment.

It was in 2020 that the US decided to impose sanctions on its rival, China, especially related to semiconductors and chips.[23] The US government directed all its firms to immediately stop exporting American semiconductor technology to Chinese chip companies. It also directed other companies, such as ASML Holding, a Dutch company known for their photolithography lithography tools—an integral semiconductor manufacturing equipment—to halt any exports to China.

In 2022, the Biden administration issued new restrictions and export controls related to semiconductors. The most recent sanctions are so extensive that they could cause an economic fallout for China and other semiconductor manufacturers.[24] Due to their possible use in creating high-end weapon systems, new sanctions have made it illegal to sell advanced computing chips, such as Artificial Intelligence (AI) chips and cutting-edge chipsets, to any Chinese companies or the military without licenses— thereby preventing China from developing and accessing advanced computing hardware. The sanctions apply to any company employing American technology to create products.

At the same time, semiconductor technology is being used in the diplomatic and geopolitical space as a tool of punitive action. This was demonstrated earlier in the year when Russia commenced a military offensive invading its neighbour, Ukraine. One of the responses, especially by the West, was the imposition of technology sanctions to punish Russia. Semiconductors and chips were central to the sanctions.[25]

The US government’s Bureau of Industry and Security (BIS) under the Department of Commerce, said as it announced the secondary and primary sanctions on Russia on imports of computers, chips, and other commodities:[26] “The new controls mean the American government is in effect claiming jurisdiction over any person or company in the world that uses American technology to make products for sale in Russia. It forces anyone who wishes to sell a vast array of technologies, including semiconductors, to request a licence—which is denied by default.”

The punitive move effectively stopped Russia from importing chips. What is remarkable, though, is that the sanctions bar Russian imports of both American goods and those made in other countries exclusively using American technology. This would imply that no company anywhere in the world would be able to export those goods, even if they were designed and produced in their territory, if they used American technology in any way.

The Imperative for Open-Source Hardware

Apart from states engaging in bilateral and multilateral conversations, private sector companies in the semiconductor space have been driving initiatives to reduce bottlenecks and dependencies in the existing supply chain. One of the critical aspects in the value chain is the licensed architecture for chip design processors. Till now, the company Arm Holdings, based in Cambridge in UK, licences its processor core architecture to all chip design firms. Arm, as a single entity, owns nearly 90 percent of the mobile phone processor designs worldwide, creating a monopoly and major dependency in the field.[27]

The OpenRISC Project (the flagship project of the OpenCores community[f]) seeks to develop open-source hardware to eliminate bottlenecks via licences and royalty fees.[28] The project includes the development of the RISC-V (Reduced Instruction Set Computer), an open-source licenced instruction set architecture, as an alternative to the Arm processor architecture patents.[29]

This has gained traction amongst both private sector players and governments. The Indian government has launched the Digital India RISC-V (DIR-V) program to propel its semiconductor ambitions. In April 2022, it was announced that the program would involve state-to-state and state-to-private sector collaboration to contribute to the RISC-V project and ensure the creation of homegrown chip design IP.[30] Under the US Department of Defence, the Defence Advanced Research Projects Agency (DARPA) also contributed funding to critical military projects developed using the RISC-V infrastructure. DARPA believes in the use of open-source technology in its military systems to identify vulnerabilities and has encouraged the use of RISC-V architecture as part of its outreach.[31]

With RISC-V offering rising powers flexibility, interoperability, and licence-free access to designing new semiconductor technology, tech powers have begun advocating for and financing open-source projects in the semiconductor domain through their private sector players. This has improved the cross-border engagement between manufacturing firms and collaborative efforts across the global ecosystem.

Indeed, as the criticality of chips and semiconductors has been pushed to the forefront in recent years, technological powers are leaning more towards cooperative endeavours. It is unlikely that any country will dominate the industry, and silicon diplomacy will continue bringing more economies together in the coming years.

India’s Priorities

India, as a fledgling semiconductor power, has an important role in the current setup of the industry. While the domestic industry contributes to the functioning of the global ecosystem, it has a long way to go before becoming an indispensable part of the supply chain. India must devise its own strategy while navigating the contours of semiconductor alliances. This brief makes the following recommendations.

1. Kickstart a Quad Semiconductor Resilience Fund.

Considering the multiple diplomatic engagements that have taken place in the semiconductor domain, India’s best bet remains collaboration with its fellow Quad members in strengthening the supply chain. While the Quad Semiconductor Supply Chain Initiative was announced during the September 2021 Summit, there has been negligible movement on the front since then. The Indian semiconductor industry can also benefit from the help of established powers such as the US and Japan. There are mainly three ways that the resilience fund can establish the Quad as a strong and formidable alliance in the semiconductor ecosystem:[32]

2. Increase cooperation amongst other semiconductor alliances.

India has the opportunity to become an integral part of other existing semiconductor diplomatic initiatives, either directly or indirectly. The availability of a skilled workforce in semiconductor design, as well as the low-cost labour needed for Assembly, Testing, Marking and Packaging (ATMP) facilities, can help India attract other potential diplomatic partners. For example:

3. Champion free and open semiconductor technologies.

A priority for India in the semiconductor diplomacy arena would be to serve as a leading voice for emerging semiconductor powers. A way to achieve this can be through leading efforts to make different technologies in the domain more accessible and cost-effective for countries’ respective private sectors. This can be achieved through two main processes:

Conclusion

The Covid-19 pandemic exposed the fragilities of the semiconductor supply chain in the form of dependencies and bottlenecks, and multilateral cooperation in the industry is no longer a choice but a necessity. With semiconductors becoming a critical geopolitical focal point, technology alliances and diplomatic initiatives are being championed as the pathway toward building supply chain resilience.

While still a novice, India has specific strengths that can be leveraged and is therefore an important player in the ecosystem. The country’s market share may be negligible, but key partnerships and alliances can help the local ecosystem grow. In this era of silicon diplomacy, India must tread a path favourable to international cooperation, which can help its domestic industry specialise in a specific area of the supply chain. India must aim to utilise diplomacy and collaboration to become an indispensable part of the global semiconductor ecosystem.

Endnotes

[b] As authoritarian regimes make rapid advances in technology development and the use of emerging tech for ‘digital authoritarianism’, democracies are working together to promote collective technology leadership, in what is coming to be known as ‘techno-democratic alliances’. See: Sameer Patil, “Tech collaboration between democracies”, Observer Research Foundation, September 15, 2022.

[c] Taiwan accounts for over 50% of global chip manufacturing output and is the de-facto leader in the semiconductor manufacturing space. Led by its homegrown firms, Taiwan Semiconductor Manufacturing Company (TSMC) and United Microelectronics Corporation (UMC), Taiwan has effectively captured the market share and created a massive dependency in the supply chain. With China’s posturing in the region and potential military aggressiveness across the Taiwan straits, Taiwan’s most lucrative industry remains under threat.

[d] Three firms own these licenses: Cadence, Synopsys, and Mentor Graphics.

[e] The ‘fabless’ market refers to the semiconductor firms which do not have an in-house fabrication facility or foundry and outsource their chip designs to contract manufacturers like TSMC, UMC.

[f] OpenCores is a hardware community developing digital open-source hardware through electronic design automation, with the aim to eliminate redundant design work and reduce development costs.

[g] Leading and trailing edge refers to the generation of the semiconductor manufacturing process and the minimum feature size indicated by the transistor gate length in nanometers. ‘Leading edge’ implies advanced semiconductor products with lesser size, greater density and a greater number of transistors giving better computational power. ‘Trailing edge’ implies elementary semiconductor products with greater size, lesser density and a lesser number of transistors giving low computational power.

[1] “China’s SMIC Warns of ‘Rapid Freeze’ as Smartphone Demand Skids”, Bloomberg, August 11, 2022.

[2] “US Sanctions Help China Supercharge its Chip Making Industry”, Bloomberg, June 21, 2022.

[3] Shunsuke Tabeta, “‘Made in China’ chip drive falls far short of 70% self-sufficiency”, Nikkei Asia, October 13, 2021.

[4] “Global Total Semiconductor Equipment Sales on Track to Record $118 Billion in 2022”, SEMI Press Release, SEMI, July 12, 2022.

[5] “China’s Share of Global Chip Sales Now Surpasses Taiwan’s, Closing in on Europe’s and Japan’s”, Semiconductor Industry Association (SIA), January 12, 2022.

[6] Programme for Semiconductors and Display Fab Ecosystem, Ministry of Electronics and Information Technology (MeitY), Government of India.

[7] Rezaul H Laskar, “India, Taiwan in talks on semiconductor hub, free trade and investment pacts”, Hindustan Times, December 16, 2021.

[8] “TSMC Announces Intention to Build and Operate an Advanced Semiconductor Fab in the United States”, TSMC Press Release, May 15, 2020.

[9] “Fact Sheet: Quad Leaders’ Summit”, White House Statements and Releases, Government of the United States of America, September 24, 2021.

[10] Pranay Kotasthane, “Siliconpolitik: The Case for a Quad Semiconductor Partnership”, ISAS Working Paper, Institute of South Asian Studies (ISAS), NUS, April 26, 2021.

[11] “Semiconductors: U.S. Industry, Global Competition, and Federal Policy”, Congressional Research Service Report, Government of the United States of America, October 26, 2020.

[12] “Australian mineral facts”, Geoscience Australia, Government of Australia.

[13] “Semiconductor Chip Designing and Manufacturing”, Press Information Bureau, Ministry of Electronics and IT, Government of India, April 6, 2022.

[14] Che Pan, “US-China tech war: Washington said to eye chip alliance with Japan, South Korea, Taiwan to squeeze China”, South China Morning Post (SCMP), March 30, 2022.

[15] Gabriel Honrada, “Taiwan to safeguard chipmakers from China espionage”, Asia Times, April 13, 2022.

[16] “Taking Stock of China’s Semiconductor Industry”, Semiconductor Industry Association (SIA), July 13, 2021.

[17] Philippe Mesmer, “South Korea’s chip industry is at the heart of China-US rivalry”, Le Monde, August 18, 2022.

[18] “U.S.-EU Trade and Technology Council (TTC)”, Bureau of European and Eurasian Affairs, U.S Department of State, Government of the United States of America.

[19] “U.S.-EU Joint Statement of the Trade and Technology Council”, White House Statements and Releases, Government of the United States of America, May 16, 2022.

[20] Ana Monteiro and Eric Martin, “US to Limit Exports of Some Chip Tech to Cut ‘Nefarious’ Use”, Bloomberg, August 12, 2022.

[21] Saif M. Khan, “U.S. Semiconductor Exports to China: Current Policies and Trends”, Centre for Security and Emerging Technology (CSET), Georgetown University, October 2020.

[22] Elena Lazarou with Nicholas Lokker, “United States: Export Control Reform Act (ECRA)”, European Parliamentary Research Service, European Parliament Briefing, November 2019.

[23] Alexandra Alper, Karen Freifeld and Stephen Nellis, “U.S. mulls fresh bid to restrict chipmaking tools for China’s SMIC”, Reuters, July 8, 2022.

[24] Ana Swanson, “Biden Administration Clamps Down on China’s Access to Chip Technology”, New York Times, October 7, 2022.

[25] Yang Lie and Jiyoung Sohn, “Chip Sanctions Challenge Russia’s Tech Ambitions”, The Wall Street Journal, March 19, 2022.

[26] “Commerce Implements Sweeping Restrictions on Exports to Russia in Response to Further Invasion of Ukraine”, US Department of Commerce Press Release, Government of the United States of America, February 24, 2022.

[27] “ARM reaps benefits of quiet mobile monopoly”, Nikkei Asia, July 20, 2016.

[28] “OpenRISC Project Overview”, OpenRISC.

[29] “About RISC-V”, RISC-V.

[30] “India launches Digital India RISC-V (DIR-V) program for next generation Microprocessors to achieve commercial silicon & Design wins by December 2023”, Press Information Bureau (PIB), Ministry of Electronics and IT, Government of India, April 27, 2022.

[31] Katyanna Quach, “DARPA adds RISC-V to its Toolbox: Defense researchers can get special access to SiFive chip designs”, The Register, April 7, 2021.

[32] Tripathy et al., “India’s Semiconductor Ecosystem: A SWOT Analysis“, Takshashila Discussion SlideDoc 2021-02, The Takshashila Institution, August 2021.

[33] “EU-India: Joint press release on launching the Trade and Technology Council”, European Commission Press Release, European Commission (EU), April 25, 2022.

[34] Arjun Gargeyas and Pranay Kotasthane, “Complement to Succeed: A Case for India-Taiwan Collaboration on Semiconductors”, Taiwan and India: Strategizing the Relations (February 2022), pp 84-94, Taiwan-Asia Exchange Foundation (TAEF), February 2022.

[35] “What are open standards?”, Opensource.com.

[36] “Individual SEMI Standards”, SEMI.

[37] Gagan Gupta, Tony Nowatzki, Vinay Gangadhar, and Karthikeyan Sankaralingam. “Kickstarting semiconductor innovation with open source hardware.” Computer 50, no. 6 (2017): 50-59.

[38] James Morra, “Google Partners With SkyWater to Drive Open-Source Chip Design”, Electronic Design, July 30, 2022.

The views expressed above belong to the author(s). ORF research and analyses now available on Telegram! Click here to access our curated content — blogs, longforms and interviews.

Arjun Gargeyasis an IIC-UChicago Fellow and was previously a researcher with the High-Tech Geopolitics Programme at the Takshashila Institution.

Read More +