Financial Inclusion of Women: Current Evidence from India

Financial inclusion is critical to achieving the economic empowerment of women—one of the targets under the fifth Sustainable Development Goal on gender equality. In India, one in every five women lack access to a bank account. Although the country’s programmes promoting financial inclusion have increased the percentage of women having access to a bank account, wide gaps remain in account use, and access to savings and credit. Women continue to face barriers to accessing financial services for various reasons: they are more likely to lack proof of identity or a mobile phone, live far from a bank branch, and need support to open and effectively use a bank account. This brief analyses the gender gaps in financial inclusion in India, outlines the impediments, and examines the potential of digital services in creating solutions.

Attribution:

Sunaina Kumar, “Financial Inclusion of Women: Current Evidence from India,”ORF Issue Brief No. 600, December 2022, Observer Research Foundation.

Introduction

Access to financial services[a]gives opportunities for generating income, accumulating assets, and participating more fully in economic activities,[1]thereby promoting social and economic empowerment. Financial inclusion also offers resilience from shock events like the COVID-19 pandemic, which highlighted the need for ensuring that the poorest populations have access to formal financial services.[2] For women, in particular, financial inclusion is an indispensable goal. Research indicates that financial inclusion has a positive impact on women’s control over household resources by increasing their savings. Yet globally, women continue to face barriers to accessing financial services. Data from the Global Findex Database 2021 shows that women and the poor are more likely to lack proof of identity or a mobile phone, live far from a bank branch, and need support to open and effectively use a bank account.[3],[4]

India, in 2014, launched the Pradhan Mantri Jan Dhan Yojana (PMJDY) to promote financial inclusion in every household in the country. The aim of the initiative is to provide the ‘financially excluded’ access to financial services such as basic savings bank accounts, need-based credit, remittances facility, insurance, and pension. Since then, according to data from the Ministry of Finance, over 460 million bank accounts have been opened; 67 percent of them are in the rural and semi-urban districts, and 56 percent are owned by women. The average deposit amount in PMJDY accounts has increased by nearly three times, from INR 1,279 in 2015 to INR 3,761 in 2022.[5]However, nearly 20 percent of women in India remain without access to a bank account. Among those who do have a bank account, there are gaps in use of such accounts, and they also continue to lack access to savings and credit.

The imperative is for these gaps to be filled, as financial inclusion is recognised as a key driver of economic growth and poverty alleviation. It ensures universal access to useful and affordable financial services delivered in a responsible and sustainable manner.[6]The Reserve Bank of India, releasing the National Strategy for Financial Inclusion (2019-2024), defined ‘financial inclusion’ as “the process of ensuring access to financial services and timely and adequate credit where needed by vulnerable groups such as weaker sections and low-income groups at an affordable cost.”[7]

Indeed, financial inclusion is considered a critical indicator of development and is identified as an enabler for at least eight of the 17 Sustainable Development Goals (SDGs).[8]Access to bank accounts, loans, insurance, and other financial services, result in direct improvements in outcomes of health, education, and employment. In turn, such progress helps achieve collective goals of eradicating poverty, promoting inclusive growth, and reducing inequality.[9]

The rest of this brief analyses the gender gaps in financial inclusion in India. It utilises literature review, consultations with experts, and data sets from the Global Findex Database 2021, the latest rounds of the National Family Health Survey 2019–21, and the All-India Debt and Investment Survey 2019, to present current evidence on the gender divide. The brief underlines the potential of digital services in closing the gaps.

The Context: Women Left Behind

Global Landscape: Findex Survey 2021

The Global Findex Database of the World Bank gathers data on global access to financial services, including payments, savings, and borrowings. The 2021 edition surveyed 128,000 adults in 123 economies during the period of the COVID-19 pandemic and contains indicators on access to and use of formal and informal financial services and digital payments.

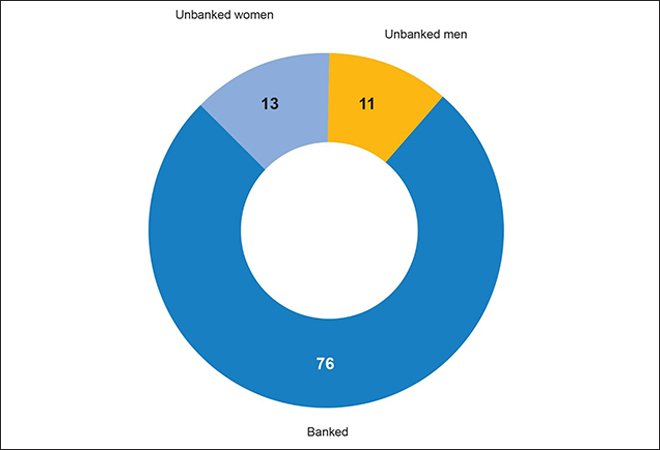

Figure 1: All Adults With and Without an Account (Global Percentage, 2021)

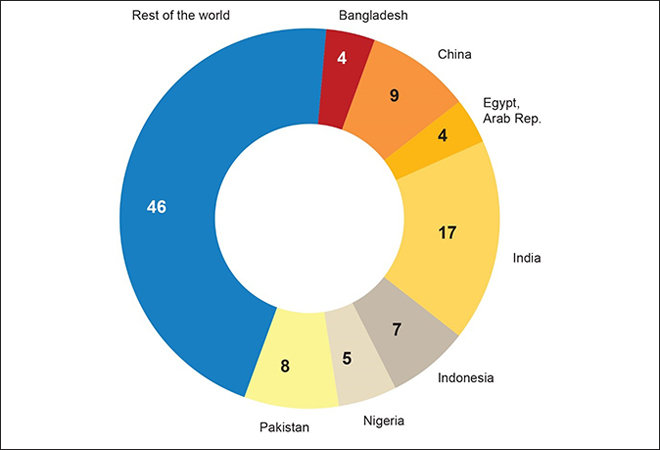

Figure2:Adults With No Account (%, 2021)

Source:Global Findex Database 2021

According to the Findex survey, 13 percent of those who are unbanked globally are women. This index defines ‘account ownership’ as ownership of an account at a regulated institution, a bank, credit union, microfinance institution, post office, or mobile money service provider. It allows account owners to store money, build savings, pay bills, access credit, make purchases, and send or receive remittances.

Between 2011 and 2021, the gender gap in account ownership in developing economies declined from 9 percentage points to 6 percentage points. In 2021, 74 percent of men and 68 percent of women in developing economies had a bank account.

More than half of the world’s unbanked adults live in only seven economies, including India and China. Despite having high rates of bank account ownership, China and India have large shares of the global unbanked population (130 million and 230 million, respectively) because of their sheer size.

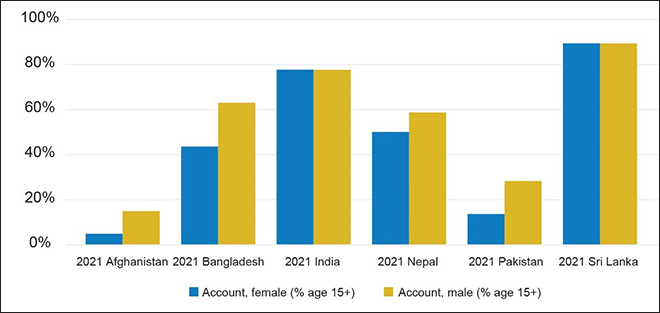

In South Asia, barring Sri Lanka and India, all countries are experiencing significant gender gaps in bank account ownership.

Figure3: Bank Account Ownership, South Asia (2021)

Source:Global Findex Database

Crucial trends

i) There are various reasons why significant proportions of women in different parts of the world do not have a bank account. These include: the prohibitive nature of most financial services; lack of necessary documentation; and distrust of the financial system. Other reasons include lack of proximity to financial institutions, which can impact women more than men, given the restrictions on mobility that women are often confronted with.

ii) The gender gap in access to mobile phones has an impact on financial inclusion. Globally, financial inclusion has been accelerated by the increase in use of mobile phones and the internet. In Kenya and Ghana, for example, women are as likely as men to own a mobile phone, and mobile money has helped women gain access to the formal financial system. However, in many other countries across the globe, there continues to be a gender divide in access to mobile phones. For instance, all countries in South Asia have gender gaps in mobile ownership.

iii) The adoption of digital payments across the world was boosted by COVID-19 and digital payments, in turn, have widened financial inclusion. At present, there is a gender gap of 17 percentage points in the use of digital payments. The share of adults making or receiving digital payments in developing economies grew from 35 percent in 2014 to 57 percent in 2021—an increase that outpaces growth in account ownership over the same period. In developing economies, 36 percent of adults received a payment into an account, such as private or public sector wage payments, government transfer or pension payments, payments for the sale of agricultural products, or domestic remittances. The majority of adults who received a digital payment also made a digital payment, and were more likely than non-recipients to save, borrow, and store money.

Focus on India

The findings from the surveys used in this brief show certain variations, reflecting differences in methodology and measurement.

a. National Family Health Survey 2019–21

A number of measures of women’s financial resources were included in the latest round of National Family Health Survey (NFHS-5, 2019-21).

Crucial trends

i) The percentage of women who have a bank or savings account that they themselves use has increased from 53 percent in NFHS-4 (2015-16) to 79 percent in NFHS-5.

ii) Women’s access to credit remains low, even as awareness about microcredit programmes has increased from 41 percent in NFHS-4 to 51 percent in NFHS-5. Only 11 percent have ever taken a microcredit loan. Women’s use of microcredit programmes is higher in rural areas (12 percent) than in the urban regions (9 percent).[b]

iii) The digital gender divide remains pervasive, both in terms of access and literacy—53.9 percent of women have a mobile phone that they themselves use; 71 percent of women who have a mobile phone can read text messages. Only 22.5 percent of women with mobile phones use them for financial transactions.

Figure 4: Women’s Ownership of Financial Assets and Mobile Phone (% of Women 15-49 Years Old)

Source:National Family Health Survey 2019–21

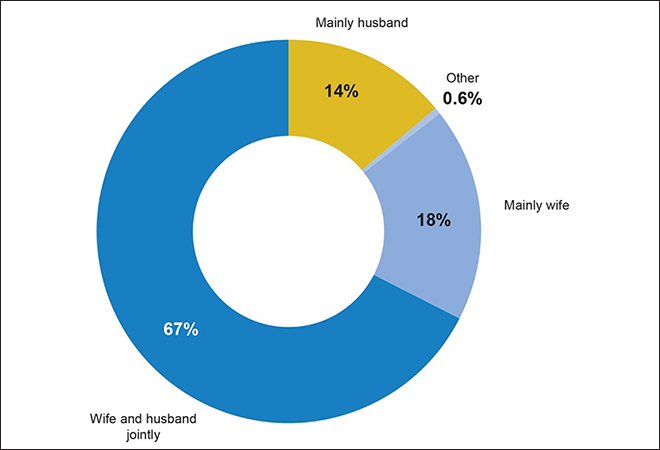

iv) Only 18 percent of married women with earnings made autonomous decisions on how to spend their money. The majority, 67 percent, made decisions jointly with their spouses.

Figure 5: Control Over Women’s Earnings

Source:National Family Health Survey 2019–21 Note:Percent distribution of currently married women (age 15-49) with cash earnings in the 12 months before the survey by the person who usually makes decisions about their use.

b. All-India Survey (AIDIS)

The All-India Debt and Investment Survey (AIDIS), which has historically collected household-level data, in 2019 for the first time collected information on financial inclusion of every member of the household. The results corroborate the findings of other surveys discussed earlier in this brief, like Findex and NFHS.

Data from AIDIS showed that nine in every 10 households own bank accounts, but ownership of other financial products remains low. These include Pradhan Mantri Jeevan Jyoti Bima Yojana (government-backed life insurance scheme), Pradhan Mantri Suraksha Bima Yojana (government-backed accident insurance scheme) and Atal Pension Yojana (APY, the government-backed pension scheme).

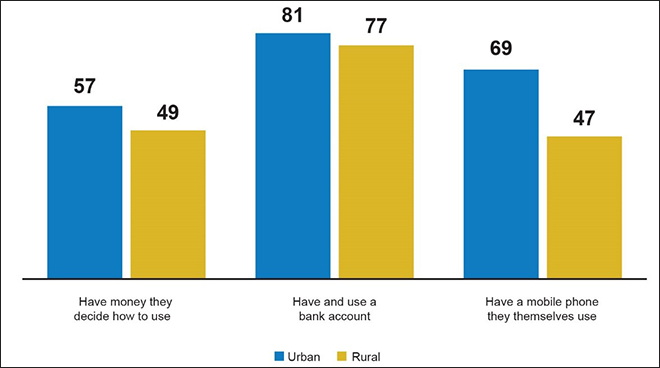

It also showed that there was little difference in access in urban and rural India—80.7 percent of women had deposit accounts in rural India compared to81.3 percent of women in the urban districts. In comparison, a higher 88.1 percent of men in rural India had deposit accounts, and 89 percent of men in urban India did.[10]

While AIDIS provides gender-disaggregated data on only one indicator—i.e., bank accounts—other data sets can give corollary insights on this subject. The Economic Survey (2021-22), for example, found that the gender gap in enrolments under APY had narrowed, as participation of female subscribers increased from 37 percent in March 2016, to 44 percent as of September 2021.[11]Similarly, the number of women beneficiaries under Pradhan Mantri Suraksha Bima Yojana (10.26 crore women ) and Pradhan Mantri Jeevan Jyoti Bima Yojana (3.42 crore women) have increased, according to 2021 figures from the Ministry of Finance.[12]

Current Initiatives on Financial Inclusion

India’s history of financial inclusion began with the nationalisation of banks in 1969 and in 1980. The nationalisation of banks has a contentious legacy,[c]but one of its aims was to expand the banking network to rural areas of the country. Though inclusion did take place, a large part of the population remained outside of the formal financial system.[13]

The Reserve Bank of India incentivised banks to expand their outreach to all sections of the population from 2005 onwards by offering no-frills account services with low minimum balance, if at all. The last Census of 2011 showed only 58.7 percent of households had access to banking in the country. By 2016, a household survey by the not-for-profit ICE 360, would show that 99 percent of households in both rural and urban India had access to banking.[14]

Targeting women, in particular, with financial inclusion brings benefits not only to the individuals but to entire households and communities. This is because, according to research, women contribute larger portions of their income to household consumption.[15]

Pradhan Mantri Jan Dhan Yojana (PMJDY)

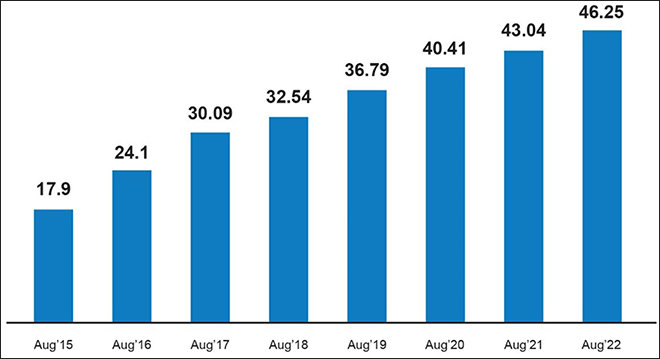

Between 2014 and 2017, India’s gender gap in access to bank accounts fell from 20 to 6 percentage points. The push was provided by the Pradhan Mantri Jan Dhan Yojana (PMJDY), launched in 2014 to integrate Jan Dhan bank accounts—a basic savings bank account with no requirement for minimum balance—with direct biometric identification under Aadhaar, and mobile phones, to enable direct transfers of funds. The so-called JAM trinity (Jan Dhan, Aadhaar, Mobile) demonstrated that financial services, when accessed and delivered through digital technologies, have the potential to lower costs, and increase speed and volume.[16]

Figure6: PMJDY Accounts (in crore)

Source:Ministry of Finance

The PMJDY initiative was backed by efforts from the government to help women obtain basic bank accounts. First of all, it dispenses with lengthy paperwork, helping expand the outreach to those who faced issues of illiteracy. Figures from 2022 show that more than 55 percent of accounts under PMJDY are held by women.[17]

A 2021 report by Women’s World Banking, a global non-profit that works on women’s financial inclusion, analysed how PMJDY has succeeded in addressing women’s need for discretion and financial independence. PMJDY offers an overdraft facility of INR 10,000 to the woman of the household for operating the savings account satisfactorily, without asking for security or how she will spend the money.[18]

It is estimated that public sector banks could attract INR 250 billion in deposits by serving 100 million low-income women across the country.[19]There is evidence that women Jan Dhan customers are more profitable than men, as women are committed savers. A female Jan Dhan customer’s lifetime revenue is at least 12 percent higher than that of a male customer’s.[20]

Figure7: Lifetime Revenue of Jan Dhan Customer, by Gender

Source:Women’s World Banking Note Savings, OD (overdraft), Cross-sell (additional financial products for existing customers like credit, insurance)

Direct Benefits Transfer (DBT)

A key policy driver in women’s uptake and use of financial services in India has been the Direct Benefits Transfer (DBT) initiative for women account holders. Through the DBT system, the government directly transfers cash into the bank account of beneficiaries. Since its inception in 2013, the Indian government has cumulatively transferred INR 16.8 trillion to beneficiaries through DBT.[21] Of this amount, 33 percent were transferred in the period between 2020-21, reflecting the uptick in cash transfers since the pandemic.

DBT covers 319 schemes, the biggest ones including wages for the Mahatma Gandhi National Rural Employment Guarantee Act, LPG subsidy, and free food grains under the Public Distribution System. PMJDY accounts are also eligible for DBT for schemes like Pradhan Mantri Jeevan Jyoti Bima Yojana, Atal Pension Yojana, and Micro Units Development & Refinance Agency Bank (MUDRA). These have all positively impacted women financially over the years, according to analysis by Women’s World Banking.[22]

Other reviews of cash transfer programmes across developing countries suggest they can increase women’s decision-making within households and have a positive impact on education and employment.[23]For example, a 2019 study by the Inclusion Economics India Centre at Krea University in Madhya Pradesh found that greater control over earned income can increase women’s household bargaining power.[24]According to the study, women who received MGNREGA wages directly into their own accounts (and not through the account of a male household member) were more likely to find employment than those paid in cash; they also stayed longer in the labour force. An evaluation by Microsave Consulting in 2022 on the impact of DBTs on women beneficiaries and their experience in accessing, withdrawing and utilising DBT funds in India, found that it increased women’s disposable income and financial decision-making.[25]At the household level, it ensured that children stayed in school and contributed to better health outcomes and food security for the family.

The DBT also brings benefits to the government: it eliminates intermediaries, brings in transparency, and lowers the costs of distributing social security. In fiscal year 2020-21 alone, the Indian government saved an estimated INR 44,000 crore as a result of the reduction in fake beneficiaries and duplicate names.[26]

In what was perhaps the government’s most ambitious cash transfer programme yet, it transferred INR 500 per month, for three months, to women to support households during the pandemic in 2020. It was facilitated in no small measure by the availability of gender-disaggregated data under PMJDY, which allowed the concerned government agencies to identify where the women beneficiaries are. At the same time, however, those who did not have PMJDY accounts were likely excluded from the cash transfers, as shown in research by the Yale Economic Growth Centre.[27]

Issues Beyond Access

The principles of financial inclusion aim to equip women not only with access to a bank account, but with affordable financial tools that will allow them to save money, access credit, make and receive payments, and access insurance and pension to manage risk. However, gaps remain in savings and credit—what can be considered the essentials of financial inclusion.

India has the highest share of inactive bank accounts globally, at 35 percent.[28]According to the Findex survey 2021, of the women-owned bank accounts in India, more than 32 percent are inactive. The gender gap in account inactivity is highest in the country at 12 percentage points. Of the women who have a bank account, less than one-fifth save formally with the bank; for many, usage is limited to withdrawal for emergencies, withdrawing salary, or availing government benefits. Women continue to save in informal systems such as community-based savings groups.

The landscape for women borrowers is even more challenging. The lack of collateral due to limited access to assets and property impedes their ability to avail loans. Even as the overall shares of women and men in total bank credit have increased over the past decade, the rise in women’s share has been far slower than men’s; it also remains low in absolute terms.[29]In 2017, women accounted for only 7 percent of total bank credit compared to 30 percent for men.[30]

The Pradhan Mantri Mudra Yojana targets the financial inclusion of women by providing collateral-free loans up to INR 1 million for small and micro enterprises. Under the scheme, 68 percent of the loans were disbursed to women entrepreneurs in 2021, yet 88 percent of these were under the ‘Shishu’ category (covering loans up to INR 50,000 in Mudra Yojanas).[31]Though women clearly benefited from the scheme, the loans have largely been small-ticket.

COVID-19 and the gendered digital divide

There is limited data on how COVID-19 has impacted digital financial inclusion. As noted in a 2021 report by the World Bank, the pandemic increased the need for contactless financial products and services, accelerating the shift to digital finance in many economies.[32]In response to the crisis, many governments used digital payments to provide relief to individuals and businesses.

However, the tools and skills required to use digital financial products and services are not available to all, which has brought attention to the digital divide that affects women in particular. According to GSM Association, which represents the global mobile communications industry, the progress India had made in bringing women and girls online for the first time through mobile internet was stalled with the pandemic. Indian women using mobile internet remained at 30 percent this year, whereas the proportion of Indian men using mobile internet has grown to 50 percent.[33]

The data from NFHS-5 which mapped digital access and literacy, shows ownership of a mobile phone that women themselves use increases with age, from 32 percent among women age 15- 19 to 65 percent among women 25-29, and then decreases among older women. When it comes to literacy, among women with a mobile phone, the ability to read text messages, however, declines with age from 89 percent among women age 15-19 to 53 percent among women 40-49.

Recommendations for Women’s Financial Inclusion

This brief offers the following recommendations to expand the financial inclusion of women beyond access to bank accounts.

Appoint more womenBusiness Correspondents. Business Correspondents (BCs) are retail agents that provide doorstepbankingservices in rural areas. Introduced in 2006, BCs have emerged as the predominant delivery model in the country for financial services.[34]Women prefer visiting a female BC as they find them easier to approach and more trustworthy. As of March 2022, less than 10 percent of BCs are women.[35]The BC model circumvents the challenges women face with mobility and literacy.

Promote women’saccess to, and literacy in digital tools. An underlying factor that restricts women’s use of formal financial services is the lack of capability to conduct transactions.[36]Women are less likely to own a mobile phone, which limits their learning of digital financial skills. Policy initiatives on digital literacy and skilling, such as the 2014 National Digital Literacy Mission, demonstrate how the private sector and CSOs can work with the government in promoting digital literacy.[37]

Deepen convergence with self-help groups. In India, self-help groups (SHGs) have historically played an important role in the financial inclusion of women through the SHG-Bank Linkage Programme. The Bank Sakhis programme by the National Rural Livelihoods Mission trains SHG members to work as BCs in the rural districts. The programme has improved women’s exposure to financial services, in turn driving up transactions in rural India. SHGs can also be tapped to run financial literacy centres for women. Livelihood and skill-development programmes by SHGs can be integrated with other initiatives in digital financial inclusion.

Collect gender-disaggregated data and develop strategies to form women-centric approaches. India is a member of the Alliance for Financial Inclusion (AFI), a policy leadership alliance led by central banks and financial regulatory institutions. As such, it has pledged to close the gender gap in financial inclusion by implementing the Denarau Action Plan adopted in 2016 by members of the AFI. One of the commitments under the Plan is to promote best practices in collecting, analysing, and using sex-disaggregated data to promote financial inclusion for women. India can take this up as a policy objective.

Promote digital credit for medium and small businesses. India has anywhere from 13.5 to 15.7 million women-owned enterprises, up to 95 percent of which are micro-businesses. Women-run businesses in India face a huge credit gap due to social biases on the part of financial institutions on assessing their creditworthiness.[38]Furthermore, due to limited access to assets and property, women face difficulty in obtaining collateral. Fintech can play a role in bias-free digital lending to women-led enterprises.[39]This can bring in formalisation and make women’s contribution to the economy more visible.

Conclusion

Financial inclusion is essential for economic growth and sustainable development; for women, it is a pathway to economic and social empowerment. Expanding financial access for women is proven to have a positive impact not only on the women themselves but, consequently, on household incomes.

The momentum created by policy responses to the pandemic and the consequent shift to digital services, offers the opportunity to address the gender gap in financial inclusion in India. The barriers that women face are gendered: restrictive social norms, mobility constraints, lack of identification, limited financial literacy, insufficient assets for collateral, and low levels of digital literacy. These challenges must therefore be addressed through a women-centric approach to financial inclusion that prioritises equal access for women to the full range of financial services available to men. This will allow them the same opportunities as men to participate fully in economic activity.

Endnotes

[a]This brief defines this concept as access to and use of affordable, convenient and sustainable financial services, including banking, credit, payments,insurance, and pension.

[b]This refers to women as individual bank account holders and not as groups, as the majority of borrowing for microcredit happens through self-help groups.

[c]These initiatives were undertaken to expand the outreach of banking facilities and increase the flow of credit to the rural areas. However, the broad approach towards financial inclusion followed in India in the 1970s and the 1980s was more oriented towards credit requirements of specific sectors/segments and there was less emphasis on individual/household-level inclusion, according to analysis by the Reserve Bank of India.

[8]Financial inclusion is an enabler for SDG1, on eradicating poverty; SDG 2 on ending hunger, achieving food security and promoting sustainable agriculture; SDG 3 on profiting health and well-being; SDG 5 on achieving gender equality and economic empowerment of women; SDG 8 on promoting economic growth and jobs; SDG 9 on supporting industry, innovation, and infrastructure; and SDG 10 on reducing inequality.

The views expressed above belong to the author(s). ORF research and analyses now available on Telegram! Click here to access our curated content — blogs, longforms and interviews.

PDF Download

PDF Download