This paper examines China and India’s economic engagements at the bilateral, plurilateral and multilateral levels. The evaluation is made in the context of the Regional Comprehensive Economic Partnership (RCEP), the mega-regional trade agreement in the east in which both nations are parties. The paper argues that irrespective of the nature of the two countries’ relationship, at its core is not cooperation, but mutual mistrust aggravated by China’s perceived “market imperialistic” predatory behaviour and India’s “protectionism”. The paper ponders the likelihood of India entering into a regional trade agreement such as the RCEP.

Introduction

China and India have an extremely complex relationship. To begin with, they are geographically contiguous and share a long border. They also have a comparable past. From ancient eras to the middle ages, China and India were dominant players in global trade and commerce. Around the late 19thcentury, both these countries were occupied by foreign powers. After their independence and during the Cold War period, it was believed that China, India, and the Soviet Union can form a strategic triangle to counter the threat of unilateralism that was then looming. The relationship between China and India soon deteriorated, however, owing to various reasons such as the border skirmishes during the 1960s. Since then the relationship has not normalised. China still retains its claims on some Indian territories, though these are readily refuted by India. India does not support China’s endeavours in the political sphere, including its control of Tibet and its relationship with Pakistan.

With the advent of the new wave of globalisation, both China and India have made remarkable economic progress. To be sure, China’s success is more remarkable than that of India (Bardhan 2012), with its economic clout growing among developing countries. Since 2000, for example, China has emerged as Africa’s largest economic partner (Sun et al 2017). It was the largest trading partner of 16 Asian countries in 2018 (Tian 2018). China is making heavy investments in resource-rich countries of Asia, Africa and Latin America. As Prasad (2017) points out, over the past decade, China’s cumulative investment in sub-Saharan Africa was US$290 billion, and in South America, US$160 billion. The growing influence of China has also been bolstered by a generous flow of aid and loans to a number of countries that are struggling to secure capital from conventional donors from the West. In the domain of geoeconomics, Blackwill and Harris (2016) have shown how and why the US is losing its ground as a world power, as China is rapidly increasing its influence. India, for its part, has lacked such strong economic stories to back its growing influence. Though the tag of “fast growing” has given India a stronger foothold among the global community, its leadership among developing countries is more due to its stature as one of the largest democracies in the world (Bardhan 2012).

In spite of their emergence as the two fastest growing large developing countries, China and India have remained circumspect and skeptical about each other for reasons that are strategic and related to military defence. This mistrust has been further fueled by the Doklam incident in 2017, where Indian and Chinese troops had a lengthy face-off over Chinese construction of a road in the area. Though the issue seems to have been resolved diplomatically it has only raised India’s apprehensions about Chinese ambitions in South and Southeast Asia, especially in light of China’s One Belt One Road (OBOR) or Belt and Road Initiative (BRI).

This brings to the fore the important issue of political relations and their geopolitical implications often being critical drivers of economic and trade relations between nations, and determinants of their interactions in multilateral and plurilateral economic forums. Luttwak (1990) documents the importance of geopolitics over the role of ‘geoeconomics’ in the world economy. The increasing importance of geopolitics in international trade and trade relations between nations is well documented in a recent volume edited by Baru (2015). While Wigell defines ‘geoeconomics’ as the geostrategic use of economic power, Mattlin and Wigell (2016) attribute the renewed interest in the concepts of ‘geopolitics’ and ‘geoeconomics’ among the new economic powers such as China, India and Brazil. The typology constructed thus far in these two research papers allow for an analytical understanding of possible empirical variation in the geostrategic uses of economic power between regional powers, and provide for an important variable when attempting to explain different forms of regionalisms. Csurgai (2017) sheds light on the mounting importance of geoeconomics in current power rivalries, represents tactical aspects of the function of state in the establishment and harmonisation of a national geoeconomic disposition, and highlights the role of the strategic organisation of information to support geoeconomic strategies. A recent study by Vihma (2017) explains how the concepts of geoeconomics are changing and how often the concept becomes overly extensive and loses its analytical power.

An analysis by Katherine (2005) discusses the importance of international trade in promoting peace. On the other hand, increased nationalist and militarist sentiments are negatively associated with trade (Acemoglu et al 2010). Acemoglu et al (2010) report that between 1985 and 2005, a 10-percent increase in military spending has been associated with a two-percent reduction in the trade share of GDP.

The objective of this paper is not to decipher the geoeconomic forces, but to look at the direction in which the economic relations have moved so far, the drivers of such movements, and the possible trajectories of their economic relations in the near future. Despite tensions, China and India have intermittently shown signs of cooperation, however dim, in multilateral forums such as the World Trade Organization (WTO) and BRICS. They are considering connectivity projects and are negotiating a mega regional trade agreement, the Regional Comprehensive Economic Partnership (RCEP).

This paper analyses the rapport between the two countries in international forums, regional connectivity projects, and future trade agreements with a special focus on the possibility of China and India coming together in the RCEP. It analyses the present Indian position with respect to the RCEP, and presents an analysis of the various impediments to the process, as well as the potential benefits from the agreement. Accordingly, the paper examines the developments in the relationship between the two countries at: a) WTO; b) BRICS; c) Regional Connectivity Projects like BCIM; and d) RCEP.

The paper is divided into four sections. Section 2 presents an assessment of China-India relations in various economic and trade platforms—namely, the World Trade Organization (WTO), BRICS, regional connectivity projects that include the Bangladesh-China-India-Myanmar or BCIM economic corridor (which is a component of the BRI scheme) vis-à-vis the India-proposed Bangladesh-Bhutan-India-Myanmar connectivity, and the RCEP. The third section then discusses the state of Indian trade with RCEP nations, followed by a section on the implications of the RCEP on India, as well as the economic priorities that can drive Indian imperatives related to the agreement. The paper closes with Section 5.

2.China-India Relations in Various Forums: An Assessment

2.1. World Trade Organization (WTO)

India has been a founding member of the General Agreement on Tarriffs and Trade (GATT) since its inception in 1948 and automatically became a member of the WTO when it came into being in 1995. China, for its part, became a member of the WTO in December 2001, after a long and arduous accession process.

China’s accession gave it steady access to world markets for its exports and an increase in its foreign direct investment (FDI). Yet, the impact of China’s entry into WTO has been more complex. On one hand, the Planning Commission (2006) notes that China’s accession has had a negative impact on India’s FDI as well as on its exports of many labour-intensive commodities—such as textiles, garments, leather articles, and light machinery—where the two countries were competitors. However, other studies tend to highlight that China and India’s export baskets are different and therefore they do not directly compete with one another in most third-country markets (Cerra, et.al. 2005). This same study suggests that India may benefit as a supplier of intermediate inputs to the Chinese exporters. The recent US-China trade war[i]has increased the need for stronger cooperation between the two countries. As the US threatens to impose trade barriers on Chinese exports, China is reportedly looking for other markets. In this context, India, as one of the world’s fastest growing economies, is being viewed as a prime target for export expansion (Jennings 2018).

India runs a massive trade deficit with China at US$ 51.11 billion in 2016-17, or 47.1 percent of India’s total merchandise trade deficit that year and double the US$ 16 billion in 2007-08. India imports mostly value added manufactured goods like electronics, chemicals and machineries from China. India’s exports, on the other hand, are mostly primary products. Various analysts in India are of the view that the country’s imports from China are undermining the growth of the domestic manufacturing sector.[ii]India also has a strong suspicion that China is unfairly subsidising its exports to India to capture the market. In the WTO, India has filed the most number of AD and countervailing duties against Chinese exports. In fact, China is the only WTO member against which India has initiated and implemented countervailing measures (Table 1). India has also contested granting China a ‘market economy’ status in WTO on the ground that Chinese firms operate under significant direct and indirect government control and receive concessional pricing in terms of inputs like raw material, power, land and labour (Kaszubska 2017).

Table 1: Anti-Dumping and Countervailing Measures against China

Total Anti-Dumping Initiations

Anti-Dumping initiations against China

Share of China

By India

839

199

23.72

By all WTO Members

5286

839

15.87

By India

Total Anti-Dumping Measures

Anti-Dumping Measures against China

Share of China

By all WTO Members

609

152

24.96

3405

866

25.43

Total CVD Initiations

CVD initiations against China

Share of China

By India

3

3

100.00

By all WTO Members

445

119

26.74

Total CVD Measures

CVD Measures against China

Share of China

By India

1

1

100.00

By all WTO Members

240

74

30.83

Source: WTO (accessed 30 May 2018)

While India and China may have problems in their bilateral relations, they have largely been in agreement with each other at the multilateral front. They both serve as a voice for the concerns of the world’s developing countries. This cooperation is visible in the ongoing Doha Round of trade talks where China and India, along with other developing countries such as Brazil, are the key representatives of the developing country negotiating group, or the G-20.

Further, out of the 23 negotiating groups present in the WTO, China and India belong to four common negotiating groupsviz. Asian Developing Members, G-20, G-33 and W-52 (that is focused on TRIPS issues). These common memberships facilitated the alignment of the two countries on various Doha issues such as fisheries subsidies, special safeguard mechanisms, and food security.

Cooperation between China and India is strong in agriculture, where both have repeatedly raised issues about distortions in global farm trade and the role of developed country subsidies in perpetuating such distortions. In the 11thMinisterial Conference (MC-11) held in Buenos Aires in December 2017, China and India raised concerns about the US’ protectionist moves and its imposition of unilateral trade restrictions. Recent media reports suggest that India has opposed a proposal by the US to unilaterally impose tariffs on Chinese imports for its alleged violations of intellectual property rights (IPR).[iii]India and China have also raised a number of concerns about Special and Differential Treatment (S&D) in the WTO and argued that privileges given under the S&D clauses in WTO should continue. In the Doha Development Round, both countries argued against proposals for plurilateral trade talks and insisted on the continuation of traditional multilateralism as practiced in the WTO. However, in some other areas such as investment facilitation, India has strongly opposed China and other BRICS countries on their proposals not only at the WTO but also at the G-20.

China and India are two of the most active participants in the WTO dispute settlement mechanism after the US and EU. India has participated in 47 disputes (23 as complainant and 24 as respondent), whereas China has participated in 54 (15 as complainant and 39 as respondent). China, despite being a late entrant to the WTO, has emerged as the third-ranked country in terms of the frequency of utilising the WTO dispute settlement mechanism. It is interesting to note that despite being frequent users of the dispute settlement mechanism, the two nations have never filed a case against each other regarding violation of trade rules at the WTO, although their bilateral trade volume is significant.

In a nutshell, China and India have cooperated with each other at the WTO on many issues despite their bilateral differences, forming a common South-centric agenda on certain key areas of negotiations. The G20 group in WTO is a good example of such leadership. The G20 group in general, and India and China in particular, have put pressure on developed countries to reduce their farm supports that distort production and trade. There are examples of such cooperation in other areas of mutual interest as well.

To a considerable degree, the increased cooperation by China and India in the multilateral forum that is the WTO has shifted the global power balance. In the Uruguay Round of trade talks from the mid-80s to the mid-90s, key negotiations happened mostly among the so-called ‘Quad’ of the US, EU, Japan and Canada—and developing countries only had marginal participation. In the Doha round of negotiations that began in the new millennium, larger developing countries such as Brazil, China and India began to assert their positions. Joint representations by these countries in WTO have helped reduce the singular clout of the developed countries that they have used to their absolute advantage in the previous round of multilateral trade talks.

2.2. BRICS

The other international forum where China and India have successfully collaborated is the BRICS (Brazil, Russia, India, China and South Africa). Unlike the WTO, the BRICS forum has an informal structure and imposes limited commitments in the form of an agreement. It is mainly an organisation that encourages commercial, political and cultural cooperation among the member nations.

The term ‘BRIC’ was invented by the chairman of Goldman Sachs in 2001 as a group of four fast growing, large market economies. In a paper titled ‘Building Better Global Economic BRICs’, Jim O’Neill suggested that Brazil, Russia, India and China are likely to be major economic players in the next ten years and given their growing economic and political importance in the global economy, the G-7 (the United States, Canada, France, Germany, Italy, Japan, and the United Kingdom) should be expanded to incorporate these four countries. In 2010, South Africa was added, making it ‘BRICS’; but the political process of forming an economic-political South-based coalition called BRICS in fact began earlier, in 2008. The BRICS forum was launched in 2009, in the aftermath of the financial crisis, to emerge as a strong South-based forum that aims for more equitable global order by challenging Western hegemony in the world economy (Harden 2014).

The logic behind the establishment of BRICS was strong. The multilateral organisations that govern and monitor the global economy today, were designed after World War II and they reflect the international order of that era. The strong emergence of the global South challenged the old international order. It was felt that a greater involvement of the developing countries on the global policymaking stage was warranted. The emergence of G20 as the central forum for international cooperation on financial and economic issues also helped the formation of BRICS, as it allowed the larger developing countries to get a foothold in global policymaking in a direct manner. However, the agenda of the G20 is based on neo-liberalism, limiting the voice of developing countries which may not subscribe to the same principles. It became important to have a grouping of large developing countries not only “to [serve the] common interests of emerging market economies and developing countries, but also to [build] a harmonious world of lasting peace and common prosperity.”[iv]

In the first BRIC summit statement issued in June 2009, it was also mentioned that one of the central objectives of BRIC is to ensure that emerging countries have greater voice and representation in international financial institutions, in improving international trade and investment environment, and in global cooperation. BRICS made it clear that it kept its faith in the WTO and multilateral trading system and that it was not intended to be a trade bloc.

At the same time, BRICS has persisted in its efforts to improve the functioning of other multilateral organisations such as the World Bank (WB) and the International Monetary Fund (IMF). Developing countries have often critiqued both the WB and IMF for their failure to reflect the present global situation, rather serving as relics of the post–World War II era when the world was economically and politically structured in a different way. For example, IMF quotas have remained largely static, failing to reflect the changing nature of the global economy. The World Bank, meanwhile, is perceived as being too slow-moving and bureaucratic to meet the development financing needs of poorer countries. These issues have led many developing country groups to create alternative arrangements for development finance and international liquidity management.

BRICS has an important role to play in the present global scenario where nationalism and protectionism is on the rise. For one, the group has officially opposed protectionist trends and asked for a rollback of these measures.[v]The dynamics of international economics for the past few decades have made many countries specialise in a small set of export goods and thus they are overly dependent on trade. These countries are likely to face problems if protectionism grows in developed countries. For countries with large domestic markets, it is still possible to survive in an era of increased trade barriers; the challenge will be more difficult for smaller countries. BRICS, especially China, can contribute significantly to global trade and act as a driver for the growth of South-South trade.

BRICS also has investible funds to promote industrialisation and development in other developing countries as well as a knowledge base and technical expertise to transfer know-how. These will be important areas of South-South collaboration in the medium term.

Over the years, BRICS has expanded its ambitions beyond the focus areas it conceived of during its inception. There have been nine BRICS summits so far and the eighth and ninth statements (2016 and 2017) covered a wide gamut of issues. These include: global political issues; intra-BRICS cooperation; outreach of BRICS to other regional and economic groupings, including the G20; global governance, including issues related to the United Nations and Security Council; global security challenges and terrorism, including bioterrorism; reform of the IMF and World Bank; regional and multilateral trade and international taxation; energy- and environment-related issues; money laundering and corruption; issues related to information and communications technology (ICT), sustainable development, urban development and gender issues; and space activities.

One of the most important achievements of BRICS so far has been the establishment of the New Development Bank (NDB) in July 2014, and the Contingent Reserve Arrangement (CRA) in July 2015, which can be viewed as anti-thesis to the International Monetary Fund (IMF) -World Bank dominance in the global economic architecture. According to NDB’s latest Annual Report (2016), it has approved seven loans (two each for China and India; and one each for Brazil, Russia, and South Africa) amounting to US$1.5 billion, with a strong emphasis on the renewable energy sector. The BRICS countries have made commitments to the CRA amounting to US$100 billion: China has committed US$41 billion; Russia, Brazil and India US$18 billion each; and South Africa, US$5 billion.

Other initiatives by BRICS have been mostly member-specific. Indeed, the success of BRICS is the sum of the achievements of the individual members. Nevertheless, BRICS can help South-South trade through capacity building, trade facilitation measures, and transfer of knowledge and technology. For example, at the 2017 BRICS Annual Summit, new initiatives were discussed, such as the development of a BRICS local currency bond markets, and further cooperation on research and development, innovation, and energy, including more effective use of fossil fuels, as well as higher emphasis on people-to-people contact.

In September 2017, the BRICS Annual Summit in Xiamen, China, happened right after the Doklam standoff.[vi]The Xiamen talks carefully avoided the subject of Doklam, and the Declaration focused on enhanced economic, political and cultural cooperation as well as peace and security in the BRICS nations. India considered as a diplomatic win, China’s support of the Xiamen Declaration that condemned the activities of specific Pakistani terrorist groups. This shows that despite the existence of controversial issues such as Doklam, China and India have taken initiatives in the BRICS forum to enhance cooperation on certain issues.

Broadly, the BRICS can give voice to the concerns of developing countries in international economic platforms, especially in light of the political backlash against globalisation in many developed nations. BRICS has the potential to be a South-based driver of growth for the developing and least developed countries (LDCs) through increased trade and investment linkages. As Rodrik (2013) points out, given the developmental experience of its members, BRICS can also provide leadership and guidance to other developing countries to look beyond the neoliberal view of market fundamentalism and technocratic elitism. Although BRICS is not a trade bloc, it can help South-South trade through capacity building, trade facilitation measures and transfer of knowledge and technology. There are areas of concern, however. The degree of diversity in economic structure among the BRICS countries is high, potentially giving rise to conflicting interests. Political and domestic compulsions of the economies may also lead to lack of consensus in international policy forums. There are also concerns that BRICS may be harmful for some smaller and less developed Southern countries because the dominant ones in the grouping might absorb foreign capital that is supposed to flow into developing countries. There is also a growing debate on whether more industrially and technologically advanced BRICS countries are pushing the less developed ones towards becoming mere exporters of primary commodities. Are certain BRICS nations replicating the colonial pattern of trade by pushing the less developed ones further down the value chain? This is an important concern and BRICS needs to encourage capacity development and help facilitate industrialisation among developing countries.

As far as India and China are concerned, partnership through the BRICS framework provides an opportunity to address a number of bilateral and multilateral issues. As protectionism rises in developed markets, China is becoming the key target against which trade barriers are being erected. If China’s market access in developed markets shrinks, it will have to look for alternatives. Recent reports indicate that given the possibility of a Sino-US trade war, China is looking to improve economic ties with India.[vii]

2.3. Regional Connectivity Projects

Another crucial facet of the China-India relationship is the regional connectivity projects. At present, India is considering the benefits of being part of either one of two regional blocsviz.BBIN (Bangladesh-Bhutan, India and Nepal) or BCIM (Bangladesh, China, India, and Myanmar).

BCIM is part of China’s One Belt One Road (OBOR) or Belt and Road Initiative (BRI). This economic corridor is envisioned by China to lead to the accrual of gains through subregional economic cooperation. The multimodal corridor, if realised, will be the first expressway between India and China and will pass through Myanmar and Bangladesh. The proposed corridor, covering 1.65 million square kilometres, connects China’s Yunnan province, Bangladesh, Myanmar and Bihar in northern India through a combination of road, rail, water and air linkages in the region (Ghosh 2015, 2016). It is envisioned that this interconnectedness will facilitate cross-border flow of people and goods, minimise overland trade obstacles, ensure greater market access, and increase multilateral trade.

China has a special interest in the BCIM economic corridor, as it is one of six such projects that constitute the BRI. Through the BCIM, China wants to connect its relatively less developed Yunnan province to other parts of South Asia and develop it as an economic hub. Additionally, China’s interest in BCIM stems from the perspective of labour costs, which might negatively affect its labour-intensive industries such as textile and agro-processing. The increase in China’s labour costs is attributable to the consumption-led growth philosophy of its 13thfive-year plan (Ghosh 2016b). For increasing final consumption to 60 percent levels, there needs to be a conscious effort to raise wages, and increase the urban population. Therefore, Chinese industry will accord priority to the BCIM economic corridor, given that it is projected to give ease of access to labour resources at cheaper rates and a ready market. This is evident from China’s interest in funding infrastructure projects in certain parts of the corridor.

Meanwhile, the BBIN road network ties into India’s ‘Look East’ policy aimed at strengthening India’s relations with the Indo-Pacific nations. After India’s signing of the BBIN Motor Vehicle Agreement (MVA) in June 2015, there has been renewed interest among policymakers and scholars to discuss the potential of BBIN as the new emerging economic order of South Asia. A study by the Asian Development Bank (ADB) proposed 10 regional road networks as South Asian Corridors, seven of which have been identified in the BBIN region (see Madhur et al 2009). These road networks will provide the landlocked trading centres of Nepal and Bhutan access to ports in India and Bangladesh as well as facilitate trade between Bangladesh and India. India is the largest trader in the BBIN bloc. India’s trade ties with Nepal and Bhutan comprise a significant share of the total international trade conducted by the latter two countries. For instance, Bhutan’s exports to India account for about 90 percent of its total exports (Ghosh 2015).

From the Indian perspective, the advantages accrued from BCIM seem to peter out significantly when compared with BBIN. While trade may flourish in BBIN through removal of tariff and non-tariff barriers, thereby helping create a free-trade zone, there remain possibilities of having smoother international mobility of capital and labour in the region with the removal of additional restrictions over time.

However, China wants BCIM to flourish more for its own market development. There are apprehensions that China will define oceans off its shores as territory to be owned and controlled. Beijing is poised to assume a more prominent presence in both the Indian Ocean and the South China Sea (Ghosh and Basu 2015). While this in itself may not be an intimidating prospect, the situation may go either way. China, for its part, has dismissed India’s apprehensions regarding its ambitious multibillion-dollar Silk Road projects, stretching across continents to build infrastructure and improve connectivity with the avowed aim of expanding trade and development. It has also sought to assure India that there are benefits for countries joining the projects envisioned under BRI (PTI 2015).

Whichever manner the geopolitical reality unfolds, the real connectivity challenge lies in economic and trade links. China has tried to convince India to put across a positive step towards the BCIM (PTI 2015, Bagchi 2017). However, it is important to note that the macro structure of China’s capital market—currency regulations, fiscal management parameters, and other parameters—is completely different from those of India and Bangladesh. At the same time, China is also in a completely different development trajectory, as compared to the other South Asian nations (Lee et al 2013).

In light of the various geopolitical developments between the two nations and the market imperialistic design of the BRI, India seems to have moved slowly on the China-oriented regional connectivity projects such as the BCIM.

The mega-regional agreement RCEP provides yet another forum where India and China have the opportunity to enhance their trade relations. The RCEP is led by the Association of South East Asian (ASEAN) states along with six ASEAN FTA Partners (i.e., China, Japan, South Korea, India, Australia and New Zealand). It is aimed at increasing economic integration by facilitating trade in goods, services, investments, economic and technical cooperation, competition and intellectual property rights. The RCEP negotiations were launched in November 2012. Though often labeled as ‘China-led TPP’ due to the leadership role taken by China to bring it to fruition, the RCEP is better viewed as an extension of ASEAN+1 free trade agreements (FTAs), as rightly pointed out by Neil (2017). Prospective RCEP member states account for a population of 3.4 billion people with a total Gross Domestic Product (GDP) of US$49.5 trillion, approximately 39 percent of the world’s GDP, with the combined GDPs of China and India making up more than half that amount.

The importance of the RCEP stems from being the single cornerstone of global trade bloc creation due to two factors: (i) withdrawal of the US from the Trans-Pacific Partnership (TPP) agreement, thereby rendering it ineffective; and (ii) the counterbalancing nature of the RCEP as the first trade bloc that groups large economies of the developing world in Asia-Pacific.

In January 2017, as the US formally withdrew from the TPP, the international community shifted its focus to the RCEP. The delay with the RCEP may be attributed to many factors including the diversity among the member countries, though now it is well-acknowledged that the fate of the Partnership is hinged on the geopolitical tensions between China and India (Neil 2017).

As stated earlier, China has been insisting on India to join the Belt and Road Initiative (BRI), with BCIM being an important concern. However, India’s reluctance to jump on the bandwagon is justified given its projected impact on local employment and industry. China is also pushing to get the RCEP pact concluded as early as possible. However, negotiations over the ambitious trade deal, which began more than five years ago, look unlikely to conclude amidst differences over the extent of trade liberalisation. For example, media reports say India is under pressure to open up 90 percent of its goods market even as the other negotiating parties are denying India’s demand for trade in services specifically with regard to movement of skilled labour and professionals across borders (also known as Mode 4 in WTO terminology). India wants maximum liberalisation on services for three reasons: first, services are becoming the dominant driver of growth in both developed and less developed nations; second, the services sector contributes almost two-thirds of India’s GDP; and third, India enjoys a comparative advantage with its vast pool of skilled labour and wants easier movement of its professionals to the RCEP member countries.

At the same time, most of the member countries want to withdraw custom duties on the highest number of goods traded among them, but India is cautious as it has experienced a surge in trade deficit in 2017-18 with seven RCEP countries—Indonesia, Thailand, China, Japan, South Korea, Australia, and New Zealand. The trade deficit with China, South Korea, Indonesia, and Australia was US$51.11 billion, US$8.34 billion, US$9.94 billion, and US$8.19 billion, respectively, in 2016-17; in 2017-18 it increased to US$63.12 billion, US$11.96 billion, US$12.47 billion, and US$10.16 billion, respectively. India has already made an initial offer to provide duty free access to 70 percent of product categories from the ASEAN countries as against 40 percent from the rest, which includes China, Japan, Korea, Australia and New Zealand.

Under pressure to substantially increase its tariff offer under the proposed trade negotiations, India has made counter-proposals to negotiate bilateral services agreement between countries such as Australia and New Zealand, in order to effectively gain from such negotiations.

Although, the RCEP would enhance economic cooperation between India and China—and in turn bring benefits to consumers—there is ample evidence of the negative impact on domestic industry through the removal of tariff and non-tariff barriers (Ghosh et al 2015). Further, India faces a 40-percent trade deficit driven by imports from China. The RCEP may lead to an increase in dumping of Chinese products, as observed by Mazumdar (2018), which can hurt the manufacturing sector of India. Therefore, it is critical for India to evaluate whether entering into the RCEP actually benefits its economy.

3. China-India Relations and concerns with RCEP

3.1. China-India Relations

Strategic concerns aside, there are a variety of forums that enable cooperation between China and India. Why then do China and India have such a strained relationship? It can be attributed, at least partially, to their perception of each other. There is mutual mistrust, reflected as well in the lack of popular support for each other as revealed by public opinion surveys. A study done by Pew Research Center in 2016 shows that only 26 percent of the Chinese people hold a favourable view of India, while 61 percent express a negative opinion. Among Indians, 31 percent of the public hold a favourable view of China, and 36 percent voice an unfavourable opinion. An August 2017 survey by the same research centre found that 44 percent of Indians rank China’s power and influence as a major threat to India, with Indians being the seventh most apprehensive population about China’s power and influence on their domestic economy. The survey also showed that perception of Indian population is at the lowest point over the last five-year period.

Figure 1

Source: Pew Research Centre

Despite the mistrust, however, India is highly dependent on Chinese imports, resulting in a burgeoning trade deficit that is not viewed favourably by policy groups, economists, and business chambers (Gupta 2018).

To measure India and China’s trade, various indices are used such as the Trade Intensity Index, Intra Regional Trade Intensity Index, and Revealed Comparative Advantage Index. This paper uses the TII, which estimates whether the value of trade between two countries is greater or smaller than would be expected on the basis of their importance in world trade. It is the ratio of intra-regional trade to the share of world trade with the region, calculated as follows:

Where Xijand Xwjrepresent the values of country i’s exports and of world exports to country j and where Xitand Xwt, are country i’s total exports and total world exports, respectively. An index of more (less) than one indicates a bilateral trade flow that is larger (smaller) than expected, given the partner country’s importance in world trade. TII is further divided into Export Intensity Index (EII) and Import Intensity Index (III) for looking at the pattern of exports and imports, following Kojima (1964) and Drysdale (1969).

EII is defined as the ratio of export share of a country/region to world exports going to a partner country. It is calculated as follows:

Where Xij= value of exports of country/region i to country/region j,

Xi= value of the exports of country/region i to the world,

Ij= total imports of country/region j,

Iw= total imports of world, and Ii= total imports of country/region i.

Meanwhile, III is defined as the ratio of import share of a country/region to the share of world imports from a partner country. It is calculated as follows:

Where Iij= value of imports of country/region i to country/region j,

Ii= value of the imports of country/region i to the world,

Xj= total exports of country/region j,

Xw= total exports of world,

and Xi= total exports of country/region i

Table 2: India’s Export, Import, and Trade intensity indices with China

Year

Export Intensity index

Import Intensity index

Trade Intensity Index

2008

0.07

2.13

1.12

2009

0.07

2.13

1.08

2010

0.08

3.12

1.00

2011

0.06

3.12

0.97

2012

0.06

2.10

0.82

2013

0.04

2.10

0.81

2014

0.04

3.12

0.87

2015

0.04

1.13

0.95

2016

0.03

2.14

0.86

Source: Authors’ estimates from World Bank data.

As shown in Table 2, the values of India’s import intensity index with China are greater than 1, while the values of the export intensity index are less than 1 over the select period—indicating India’s high dependence on imports from China. The value of trade intensity index of India with China is slightly less than 1 after 2011, which means that trade relation between India and China is slightly lower than China’s share in world trade. The numbers make it clear that China’s dependence on exports from India is substantially low, with India’s EII with China (ranging between 0.03 and 0.08). This does not augur well for the Indian economy.

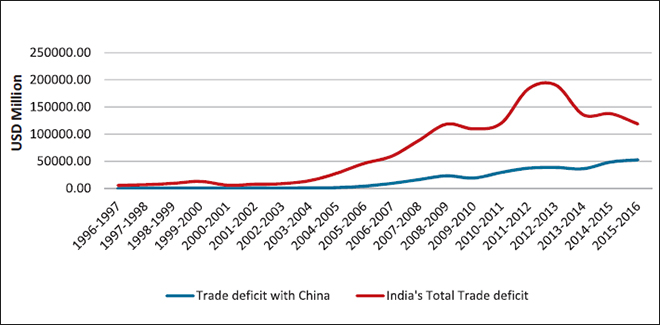

Figure 2: India’s total trade deficit, and with China

Source: Authors’ estimates from Ministry of Commerce and Industry data.

In light of such high import dependency, India also suffers from a significant trade deficit with China (see Figure 2). Overall, the trade deficit of India against China has increased over the years. Moreover, in percentage terms, trade deficit with China contributes substantially to the trade deficit of India, as can be witnessed from Fig. 3. It has been increasing by large margins over the last two decades.

Fig. 3: Share of China in India’s total trade deficit (%)

Source: Authors’ estimates from Ministry of Commerce and Industry data.

Thus, the large Indian trade deficit with China, significant dependence on China imports, the contribution of Chinese imports in Indian trade deficit along with a growing mistrust have not augured well for Indian policy circles and the business sector.

It is important to identify the major drivers of the trade deficit by analysing the top imported goods from China over the years. The top 15 items, recurring over the last 10 years, as given in Table 3, contribute to more than 80 percent of India’s imports from China.

Table 3: India’s imports from China, Top 15

Sl. No.

HS Code

Items

Percentage share in total imports

1

85

Electrical machinery and equipment and parts thereof; sound recorders and reproducers, television image and sound recorders and reproducers, and parts.

32.02

2

84

Nuclear reactors, boilers, machinery and mechanical appliances; parts thereof.

17.10

3

29

Organic chemicals

9.83

4

31

Fertilisers

5.30

5

72

Iron and steel

3.82

6

39

Plastic and articles thereof

2.74

7

90

Optical, photographic cinematographic measuring, checking precision, medical or surgical instruments and apparatus and parts and accessories thereof

2.09

8

89

Ships, boats and floating structures

2.05

9

73

Articles of iron or steel

1.92

10

87

Vehicles other than railway or tramway rolling stock, and parts and accessories thereof

1.81

11

98

Project goods; some special uses

1.62

12

94

Furniture; bedding, mattresses, mattress supports, cushions and similar stuffed furnishing; lamps and lighting fittings not elsewhere specified

1.47

13

38

Miscellaneous chemical products

1.15

14

27

Mineral fuels, mineral oils and products of their distillation; bituminous substances; mineral waxes

1.11

15

76

Aluminium and articles thereof

1.10

Source: Ministry of Commerce and Industry

Lately, India has been using trade policy measures that indicate a rather protectionist stance. For example, India imposed anti-dumping duty on 98 products from China. Further, according to the Directorate General of Anti-Dumping & Allied Duties (DGAD) website, it has initiated anti-dumping cases against 380 products from China and has also imposed countervailing duty on two Chinese productsviz. imports of Castings for Wind Operate and on certain Hot Rolled and Cold Rolled flat products of stainless steel. This indicates that India has repeatedly utilised trade remedies to counteract the surge of Chinese products in the domestic market.

Furthermore, India’s Budget 2018–19 released on 1 February 2018 has increased the MFN tariff rates for a number of products. An extract from the Budget identifying key select items and their increase in tariff rate is provided in Table 4.

Table 4: India’s Budget 2018- 19 – Increase of tariff duty on select goods

Chapter/ Heading/

HS Code

Commodity

Rate of Duty

From

To

Capital goods and Electronics

2

8483 40 00, 8466 93 90,

8537 10 00

Ball screws, linear motion guides, CNC systems for manufacture of all types of CNC machine tools falling under headings 8456 to 8463

7.5%

2.5%

3

70

Solar tempered glass or solar tempered [anti-reflective coated] glass for manufacture of solar cells /panels/modules

5%

Nil

C.

Changes in Customs duty to provide adequate protection to the domestic industry

Automobile and automobile parts

14

8407, 8408, 8409,

8483 10 91, 8483 10 92,

8511, 8708, 8714 10

Specified parts/accessories of motor vehicles, motor cars, motor cycles

7.5% / 10%

15%

15

8702, 8703, 8704, 8711

CKD imports of motor vehicle, motor cars, motor cycles

10%

15%

16

8702, 8704

CBU imports of motor vehicles

20%

25%

17

4011 20 10

Truck and Bus radial tyres

10%

15%

Diamonds, precious stones and jewellery

21

71

Cut and polished colored gemstones

2.5%

5%

22

71

Diamonds including lab grown diamonds-semi processed, half-cut or broken; non-industrial diamonds including lab-grown diamonds (other than rough diamonds), including cut and polished diamonds

2.5%

5%

23

7117

Imitation Jewellery

15%

20%

Electronics / Hardware

24

8517 12

Cellular mobile phones

15%

20%

25

3919 90 90, 3920 99 99, 8544 19, 8544 42, 8544 49

Specified parts and accessories of cellular mobile phones

7.5%/ 10%

15%

26

8504 90 90/ 3926 90 99

PCBA of charger/adapter and moulded plastics of charger/adapter of cellular mobile phones

Nil

10%

27

Any Chapter

Inputs or parts for manufacture of:

a) PCBA, or

b) moulded plastics

of charger/adapter of cellular mobile phones

Applicable rate

Nil

28

8517 62 90

Smart watches/wearable devices

10%

20%

29

8529 10 99 / 8529 90

LCD/LED/OLED panels and other parts of LCD/LED/OLED TVs

7.5%/ 10%

15%

30

8529/4016

12 specified parts for manufacture of LCD/LED TV panels

Nil

10%

31

70

Preform of silica for use in the manufacture of telecommunication grade optical fibres or optical fibre cables

Nil

5%

Furniture

32

9401

Seats and parts of seats [except aircraft seats and parts thereof]

10%

20%

33

9403

Other furniture and parts

10%

20%

34

9404

Mattresses supports;articles of bedding and similar furnishing

10%

20%

35

9405

Lamps and lighting fitting, illuminated signs, illuminated name plates and the like [except solar lanterns or solar lamps]

10%

20%

Watches and Clocks

36

9101, 9102

Wrist watches, pocket watches and other watches, including stop watches

10%

20%

37

9103

Clocks with watch movements

10%

20%

38

9105

Other clocks, including alarm clocks

10%

20%

Toys and Games

39

9503

Tricycles, scooters, pedal cars and similar wheeled toys; dolls’ carriages; dolls; other toys; puzzles of all kinds

10%

20%

40

9504

Video game consoles and machines, articles for funfair, table or parlor games and automatic bowling alley equipment

10%

20%

41

9505

Festive, carnival or other entertainment articles

10%

20%

42

9506 [except 9506 91]

Articles and equipment for sports or outdoor games, swimming pools and paddling pools [other than articles and equipment for general physical exercise, gymnastics or athletics]

10%

20%

43

9507

Fishing rods, fishing-hooks and other line fishing tackle; fish landing nets, butter fly nets and similar nets; decoy birds and similar hunting or shooting requisites

10%

20%

44

9508

Roundabouts, swings, shooting galleries and other fairground amusements; travelling circuses, traveling menageries and travelling theatres

10%

20%

Source: Ministry of Commerce and Industry

The Budget 2018-19 increased tariff rates on around 50 products and it appears that quite a few of them (products with HS code 85, 84, 39, 87, and 94) are products that India imports from China. This again is reflective of India’s increasing cautious approach towards China. It is to be noted that India has not changed any preferential tariff rates and the tariff increases announced in the budget will not affect any of the countries that have entered into FTAs with India such as Japan, Thailand, Singapore and South Korea.

3.2. India’s trade relations with other RCEP countries

While India’s overall trade deficit is increasing over the years, the economy has adverse balance of trade with most of the RCEP members. Though the nation enjoys trade surplus with Philippines, Cambodia, Singapore, and Vietnam, it experiences negative trade balance with the other eleven potential members. The following two tables, 4 and 5, reveal the export and import intensity indices of India with other RCEP countries. Table 6 represents trade intensity index of India with RCEP members except China.

Table 5: Export intensity index of India with RCEP countries

Year

Australia

Japan

New Zealand

South Korea

ASEAN

BRU

CAM

INDO

LAO

MAL

MYA

PHI

SIN

THA

VIET

2008

0.063

0.035

0.048

0.080

0.740

0.095

0.175

0.051

0.194

0.030

0.108

0.220

0.096

0.190

2009

0.059

0.046

0.071

0.075

0.650

0.065

0.224

0.077

0.162

0.045

0.115

0.199

0.092

0.186

2010

0.050

0.043

0.037

0.052

0.850

0.071

0.248

0.050

0.139

0.045

0.089

0.165

0.074

0.184

2011

0.059

0.041

0.039

0.046

1.394

0.082

0.209

0.048

0.118

0.035

0.087

0.229

0.072

0.194

2012

0.054

0.040

0.046

0.047

0.064

0.112

0.160

0.098

0.131

0.040

0.105

0.192

0.094

0.201

2013

0.058

0.048

0.041

0.048

0.053

0.124

0.151

0.112

0.119

0.028

0.126

0.178

0.086

0.240

2014

0.074

0.040

0.046

0.053

0.079

0.126

0.138

0.155

0.169

0.029

0.125

0.145

0.092

0.257

2015

0.106

0.048

0.055

0.052

0.080

0.109

0.128

0.066

0.137

0.041

0.127

0.145

0.096

0.206

2016

0.094

0.038

0.070

0.063

0.080

0.130

0.140

0.120

0.150

0.052

0.137

0.140

0.130

0.190

Source: Authors’ estimates on the basis of data from Ministry of Commerce and Industry

Table 6: Import intensity index of India with RCEP countries

Year

Australia

Japan

New Zealand

South Korea

ASEAN

BRU

CAM

INDO

LAO

MAL

MYA

PHI

SIN

THA

VIET

2008

0.349

0.059

0.081

0.121

0.204

0.004

0.286

0.002

0.212

0.678

0.030

0.141

0.090

0.038

2009

0.394

0.057

0.098

0.115

0.199

0.006

0.363

0.051

0.161

0.596

0.040

0.128

0.094

0.045

2010

0.226

0.050

0.090

0.100

0.164

0.007

0.279

0.001

0.146

0.593

0.037

0.102

0.097

0.065

2011

0.229

0.058

0.087

0.091

0.228

0.005

0.288

0.160

0.165

0.673

0.036

0.091

0.092

0.070

2012

0.206

0.063

0.075

0.096

0.253

0.006

0.316

0.288

0.176

0.629

0.039

0.079

0.094

0.081

2013

0.176

0.060

0.070

0.101

0.301

0.007

0.365

0.054

0.183

0.551

0.031

0.082

0.106

0.089

2014

0.198

0.068

0.066

0.110

0.300

0.009

0.396

0.144

0.221

0.544

0.032

0.090

0.120

0.093

2015

0.232

0.077

0.078

0.121

0.237

0.025

0.428

0.290

0.223

0.396

0.045

0.121

0.128

0.078

2016

0.275

0.071

0.070

0.119

0.330

0.030

0.530

0.280

0.222

0.450

0.050

0.121

0.146

0.074

Source: Authors’ estimates on the basis of data from Ministry of Commerce and Industry

N.B. for tables 5 and 6: BRU= Brunei; CAM= Cambodia, INDO= Indonesia, LAO= Laos, MAL = Malaysia, MYA = Myanmar,

Table 7: Trade intensity index of India with RCEP countries

Year

ASEAN

Australia

Japan

New Zealand

South Korea

2008

1.77

2.23

0.49

0.65

1.08

2009

1.67

2.42

0.51

0.84

1.12

2010

1.57

1.56

0.48

0.69

1.00

2011

1.65

1.72

0.53

0.70

0.95

2012

1.56

1.47

0.53

0.64

1.00

2013

1.60

1.29

0.54

0.58

0.99

2014

1.73

1.44

0.54

0.56

1.06

2015

1.52

1.67

0.62

0.64

1.25

2016

1.29

1.66

0.48

0.52

1.03

Source: Authors’ estimates on the basis of data from Ministry of Commerce and Industry

From Tables 5, 6, and 7, it can be seen that the value of import intensity index is higher than the value of export intensity index. Further, they are less than 1, indicating that there remain opportunities for India to expand its exports with these nations. On the other hand, the trade intensity index represents the overall trade relation between the partner countries. Table 7 also shows that the value of trade intensity index of India with ASEAN and Australia is greater than 1, which means India’s trade is significantly higher with ASEAN and Australia as compared to the share in world trade, whereas it is less than 1 for both Japan and New Zealand over the years.

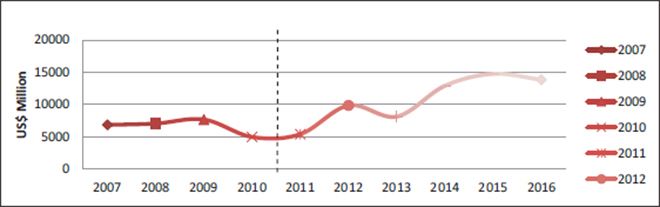

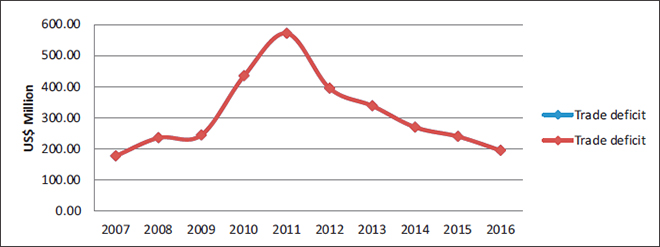

From the perspective of trade deficit, it is evident from Figures 4 to 8 that India’s bilateral trade deficits are increasing with ASEAN, Australia, Japan, and South Korea. Free trade agreement of India with ASEAN came into effect on 1 January 2010, as marked by the fragmented vertical line in figure 3. Similarly, the South Korea-India and Japan-India Comprehensive Economic Partnership Agreement came to effect in 2010 and 2011, as denoted by the broken vertical lines in figures 4 and 5. It is noteworthy that trade deficits have been increasing after signing of the agreements. Figures 6 and 7 suggest that India is having trade deficits with Australia and New Zealand with whom they have been contemplating signing of FTAs over the decade. Interestingly, in both cases, the enthusiasm with which impact assessment studies were conducted seems to have waned.

Figure 4

Source: Computed by authors with data from Ministry of Commerce and Industry, GoI

Figure 5

Source: Computed by authors with data from Ministry of Commerce and Industry, GoI

Figure 6

Source: Computed by authors with data from Ministry of Commerce and Industry, GoI

Figure 7

Source: Computed by authors with data from Ministry of Commerce and Industry, GoI

Figure8

Source: Computed by authors with data from Ministry of Commerce and Industry, GoI

IV. Implications for India with respect to RCEP

This paper has examined the trade relationships of India with China and the other RCEP partners. It is important to take note of three more important issues, before India gets into any form of regional trade bloc with potential partners of RCEP. These are related to sectoral balance of trade, impacts of value chain, and issues of complementarity.

Sectoral Balance of Trade:Saraswat et al (2018), in an important note placed in public domain by the NITI Aayog, argue that the sectoral trade balance does not reveal a rosy picture. They classified sectors as per the UN’s Harmonised system of product classification, with product clusters in 21 sections like textiles, chemicals, vegetable products, base metals, gems and jewelry etc (similar to sector classification). Their analysis brings out that trade balance has worsened (deficit increased or surplus reduced) for 13 out of 21 sectors. In fact, value added sectors like chemicals and allied, plastics and rubber, minerals, leather, textiles, gems and jewellery, metals, vehicles, medical instruments and miscellaneous manufactured items fall in this category. However, they find that trade balance has improved in sectors like animal products, animal and vegetable fat, wood and articles, paper and paperboard, cement and ceramic, arms and ammunitions. They conclude: “… Sectors where trade deficit has worsened account for approximately 75% of India’s exports to ASEAN”. Therefore, Saraswat et al (2018) attribute a large part of the BOT worsening problem to the ASEAN- India FTA.

Impacts on Value Chain:The second is the issue of the impacts of the FTAs on value chain. Ghosh et al (2015) argue that success or failures of FTAs should not be assessed only through the lens of balance of trade, but also with respect to their impacts on the product value chain. Axiomatically, any form of trade liberalisation in a product, in which the economy of import has a comparative advantage, reduces prices and increases consumer surplus. It is axiomatically taken that such a policy will not prove beneficial for domestic industry. However, Ghosh (2009) and Ghosh et al (2015) argue that the impact on the domestic industry need not necessarily be negative due to FTAs, but depends on the impacts on the input markets including the labour market. This position is in contravention to the one taken by Saraswat et al (2018). Even sectoral balance of trade is not the absolute metric of success or failure of FTA going by this argument. One, therefore, needs to look at consumer surplus, producer surpluses (including those of primary producers) or profitabilities, and the overall change in social surpluses caused due to such policy interventions. Such a study is yet to be conducted in the context of RCEP.

Complementarity and Comparative Advantage in services:It is always important that complementarities in trade be looked at while getting into any form of FTA. “Gains from trade” essentially arise from comparative advantages. Trade liberalisation of the RCEP partners with respect to services has been a thorny issue from the Indian perspective. In the cases of FTAs with East and Southeast Asian economies, beginning with Singapore in 2005 to the last one signed with South Korea in 2011, India has been insisting on capitalising on its pool of ‘skilled’ labour force to gain from improved access to employment opportunities in these economies. This has been expected to come about by increasing the ease of movement of professionals through the liberalisation of what is called Mode 4 in services trade. To this end, India has been willing to trade up its remaining tariff policy manoeuvrability in the manufacturing industry (and even in the agricultural sector) (Francis 2017). In the context of RCEP, this is primarily where Indian comparative advantage lies. On the other hand, as pointed out by Francis (2017), RCEP goes far beyond trade liberalisation. In its attempt to harmonise foreign investment rules, intellectual property rights (IPR) laws, and several other laws and standards, beyond what has been agreed by developing countries at the WTO, it takes away an economy’s ability to customise trade policies according to the needs of specific time periods. As Francis (2017) emphasises, “… attempts to harmonise rules related to foreign investments, IPR and every other public policy related to the economy extending across agriculture, manufacturing and services sectors, is even more treacherous”. Quite naturally, this has not gone too well for India, who is yet to accede to this.

At the same time, apart from the initial backlash from the ASEAN with respect to market access in the context of mode 4, India wants that at least the provisions on Mode 4 that were agreed upon as part of the FTA between ASEAN and New Zealand, Australia, should be included in the RCEP. The fresh offers in February 2018 did not really impress India.

4.1. China-India issues in RCEP

Given this background, it is critical for India to take into consideration, when negotiating the RCEP, the implications of greater market access of Chinese goods on the Indian market. Interestingly, though the primary demand of India at the RCEP is for greater market access in services with regard to Mode 4, India does not particularly have great Mode 4 interest in China. This effectively means that India’s resistance in the RCEP is related to goods trade in China, and can only partially be ameliorated with greater market access in services with regard to Mode 4, which still stands as a thorny issue.

Saraswat et al (2018), on the other hand, have pointed out that in the context of ASEAN-China FTA (ACFTA), Thailand and Malaysia are the only countries which have a trade surplus with China, though the surplus has been declining ever since the FTA came to effect from 2010. Taking the example of Indonesia, which they claim, is not adequately integrated in the regional value chain of ACFTA, they have cautioned, “…India should look at Indonesia’s role in China ASEAN FTA and not compare itself to Malaysia and Thailand”.

In light of India’s trade deficit from China and its dependence on Chinese imports, it is critical for India to retain certain policy space to not only to protect its markets but also to develop its domestic industry. Unfortunately, by entering into an ambitious, multiregional agreement such as the RCEP, India will definitely have to forego its policy flexibility to some extent. Due to these reasons, India should refrain from signing the RCEP, unless there are clear benefits for India.

With regard to India and China relationship, irrespective of the variety of forums present for the two countries to cooperate, the countries continue to maintain diplomatic distance, especially in light of China’s rapid development on the OBOR initiative and India’s wariness of the RCEP. Nevertheless, strategic and political concerns aside, greater cooperation between India and China can be beneficial to the world, especially in light of voicing South concerns at multilateral institutions.

Conclusion

Free trade policies open up previously closed areas to competition and innovation, and hold promise of better jobs, newer markets and increased investment. Cooperation in international trade through free trade between nations is deemed to be Pareto-improving for participating nations: thus the emergence of the notion of Regional Trade Agreements (RTAs).

India, throughout the first decade of the present millennium, signed a host of free trade agreements (FTAs) and comprehensive economic cooperation agreements (CECAs) which also include investment agreements. A large part of them have been with the South-east Asian nations. India’s trade deficit only increased after entering into FTAs and CECAs. As far as China is concerned, India faces a massive and growing trade deficit. By signing a multilateral RTA where China is a signatory, imports may further increase by a higher magnitude than exports due to price competitiveness. Indeed, demand for imported commodities has increased, thus far with a decline in or complete elimination of tariffs and non-tariff barriers. This has negatively affected domestic industry, as seen in the sectors of the edible oil processing, automobiles, electronics, telecom and white goods (Ghosh 2015). At the same time, however, these RTAs have widened choices of cheaper products for Indian consumers. Gupta (2018) is of the view that regional economic integration processes would have been natural choices conducive for the flagship ‘Make in India’ call. However, this might not be the case with RCEP, as there are many other concerns that remain, especially on market access with services.

In the 2018-19 budget, the present government announced that it is making a strategic shift away from free trade with higher emphasis towards domestic value addition. Consequently, the government has raised MFN import tariffs on a large number of agricultural and industrial products. While tariff rates applicable to the regional trade agreements (including FTAs and CECAs) have not been touched, there is a possibility that the government may renegotiate these tariff rates on a bilateral basis. Given this change in strategy, and to reconcile between trade and domestic value addition, it might be useful to study the relative role of individual FTAs as possible partners in production networks where Indian manufacturing firms can find their position in the value chain. In the context of RCEP, India already has bilateral trade agreements with most of the RCEP members and it is negotiating trade deals with Australia and New Zealand. Therefore, participation in RCEP is more of a question whether India and China can have a mutually beneficial relationship through international trade and investment. It will also be important to evaluate whether one should really ignore the lure of RTAs, when the trade multiplier of GDP has traditionally been taken as a driver of growth.

Indian indifference towards the Trans-Pacific Partnership, or the Transatlantic Trade and Investment Partnership (TTIP) or even present slow movement with RCEP has been criticised by some (e.g. Sengupta 2017; Nataraj 2016). According to Nataraj (2016), the potential impact of TPP on India will be through three avenues, namely: (a) diversion of trade; (b) decline in FDI; and (c) geopolitical exclusion. Dahejia (2015) argues otherwise: when a country preferentially reduces trade barriers with its partners in a PTA, it is simultaneously keeping in place—or perhaps, even raising — trade barriers against countries that are not members of the agreement.

Therefore, from an economic perspective, policymakers involved in RTAs must take cognizance of the potential trade-offs between the key stakeholders of the economy, including consumer benefits and producer surplus or domestic industries. Further, a crucial concern is that of a rising bilateral trade deficit, given India’s experience with South-east Asian nations. This apparently refutes the existing thinking of pro-RTA groups who propagate the view that “trade is good; more is better”. To be sure, this assumption of “non-satiation” of utility, as it exists in neoclassical microeconomics theory, does not bode well for international trade as far as India is concerned. Given this dilemma, a better decision can be reached only with a comprehensive feasibility study that examines not only the macro-economic impacts (through macro-variables and multiplier impacts on GDP), but also the impacts on the product value chain.

On the other hand, there are geostrategic arguments both in favour and against RCEP. This is where geoeconomics plays a role. There are those supportive of the RCEP who hold the view that India should enter the agreement, considering the diminishing importance of TPP after the US’ exit. The RCEP will pave the way for a new world trade order and have implications on geopolitical concerns. As Marwah (2018) emphasises, the concern is much more than a trade deal for China. As such, “… China’s Belt and Road Initiative, with an investment of more than USD 200 billion and counting, embraced by more than 65 countries is all about strategic influence via its vast network of roads, railways and ports” (Marwah 2018). At the same time, Japan, Singapore and ASEAN reckon that a new world economic order may indeed be created, and therefore have been putting pressure on India for the deal.

The overall mood in Indian policymaking circles, meanwhile, is contrarian. A recent report inThe Mintquoted the Chief Economic Adviser of India, Arvind Subramanian as having said that India will have to take into account geostrategic issues while moving ahead with the RCEP trade deal as it will mean opening up the market to China (The Mint 2018). Even former foreign secretary S. Jaishankar, at a recent presentation before the parliamentary standing committee on commerce, called for “observance of due restraint” with respect to RCEP (The Mint 2018). Of course, the recent border skirmishes often come in the way of negotiations, and Gupta (2018) also notes that nationalist sentiments do not augur well in trade negotiations where China is present.

It is clear from this paper’s discussion that a more holistic cost-benefit analysis is needed to understand the potential impacts of the RCEP on India, both from the economic and political perspectives. There remain critical questions on complementarities in trade negotiations, costs and benefits of standardised IPR regimes, as well as the impacts on the product value-chain. So far, no analysis has been done on those domains with respect to RCEP. Till India properly comprehends the potential benefits, costs, and the associated threats including the geostrategic concerns, it should refrain from signing the RCEP.

At the same time, China and India should improve their level of cooperation in other areas. As the two biggest representatives of the global South, these two countries have roles to play in global economic and strategic cooperation. A stronger BRICS, a more unified voice of China and India in the WTO, IMF and World Bank may help developing countries get their voices heard in the multilateral organisations that have been typically dominated by developed countries. Improved cooperation and partnership in global forums may pave the path for improved bilateral economic cooperation. This could also reduce the mutual trust deficit that serves as a key obstacle in India and China’s bilateral economic cooperation.

About the Authors

Nilanjan Ghosh isSenior Fellow and Head of Economics, Observer Research Foundation, Kolkata. He is also Senior Economic Advisor at the World Wide Fund for Nature, New Delhi. Nilanjan obtained his PhD from the Indian Institute of Management Calcutta. He has been working in the domains of ecological economics, developmental issues, water resources and financial markets, and conducts his research by combining frameworks of neoclassical economics and institutions. Email:[email protected].

Parthapratim Pal isProfessor of Economics, Indian Institute of Management Calcutta, Kolkata. He has a Master’s degree, an MPhil, and a PhD in Economics from the Center for Economic Studies and Planning, Jawaharlal Nehru University, New Delhi. He has also received education from the Cambridge University, UK and the Harvard Business School, USA. His current research interests include international trade, regional trade agreements and regional cooperation, WTO-related issues, and international capital flows. Email:[email protected]

Jayati Chakrabortyis Research Assistant, Economics Division, Observer Research Foundation, Kolkata. She obtained her MPhil in Economics from the University of Calcutta, and her MSc in Economics from the same university. She will be joining the Economics department of the University of Wisconsin, Milwaukee, in the Fall of 2018. Email:[email protected]

Ronjini Rayis Research Assistant, Indian Institute of Management Calcutta, Kolkata. She is a lawyer specialising in international trade and investment laws. After graduating from Symbiosis Law School, Pune, she participated in a Joint Academy on Trade Law and Policy organised by the World Trade Institute, Berne and Centre for WTO Studies, New Delhi. Prior to joining IIM Calcutta, she worked with Clarus Law Associates, New Delhi. Email:[email protected]

REFERENCES

Acemoglu, D. and Pierre Yared (2010): “Trade and militarism: the political limits to globalization”, VoxEU.org, 7 March 2010

Barbieri, K. (2005): “The liberal illusion: does trade promote peace?”, Ann Arbor, University of Michigan, 2005

Bardhan, (2012): “Awakening Giants, Feet of Clay: Assessing the Economic Rise of China and India”, Princeton University Press, ISBN: 9781400845002.

Baru, S. (2015): “Power Shifts and New Blocs in the Global Trading System”, Volume 1 (Routlege)

Blackwill, R.; Harris, J. (2016): “War by Other Means: Geoeconomics and Statecraft”, Harvard University Press: Cambridge, 2016

Cerra, V., S.A. Rivera, and S.C. Saxena (2005): “Crouching Tiger, Hidden Dragon: What Are the Consequences of China’s WTO Entry for India’s Trade?,” IMF Working Paper No. WP/05/101.

Chatterji, R., A. Basu Ray Chaudhury (2016): “Indian Media’s Perception of China: Analysis of Editorials”, Special Report, (New Delhi: Observer Research Foundation)

Chatterji, R., A. Basu Ray Chaudhury (2018): “Indian regional media’s perception of China: Analysis of select editorials from The Assam Tribune and The Arunachal Times”, Special Reportm, (New Delhi: Observer Research Foundation)

Csurgai, G. (2017): “The increasing importance of geoeconomics in power rivalries in the twenty-first century”, Geopolitics,2017

Ghosh, N. (2015): “FTA-fetishism to hurt Indian industry in the long run”, OP-ED column in abplive.in, November 12

Ghosh, N. (2016a): “The Lure of RTAs: Will India or Won’t It?” in R. Passi (edited) Primer 2016 (Observer Research Foundation, New Delhi)

Ghosh, N. (2016b): “The New Pathway: Is Sub-Regional BBIN a Role Model for Asian Connectivity?”, Raisina Files 2016. (Observer Research Foundation, New Delhi)

Ghosh, N., A. Konar, and S. Pathak (2015): “India’s FTAs with East and Southeast Asia: Impact of India-Malaysia CECAon the Edible Oil Value Chain”, Occasional Paper No. 73, Observer Research Foundation

Jennings, R. (2018): “China Eyes Improved India Ties In Case Of Sino-U.S. Trade War”, Forbes, April 3, 2018.

Kaszubska, K. (2017): “Rethinking China’s Non-Market Economy Status Beyond 2016”, ORF Occasional Paper No. 107, (New Delhi: Observer Research Foundation)

Kojima, K. (1964): “The Pattern of International Trade among Advanced Countries”, Hitotsubashi Journal of Economics, Vol. 5, No. 1, 16–36

Lee, H.L., X. Qinjung, and M. Syed (2013): “China’s Demography and its Implications”, IMF Working Paper No. WP/13/82

Madhur, S.; Wignaraja, G.; Darjes, P. (2009): “Roads for Asian Integration: Measuring ADB’s

Contribution to the Asian Highway Network” ADB Working Paper no. 37

Marwah, R. (2018): “RCEP: More Than A Trade Deal”, https://www.eurasiareview.com/05072018-rcep-more-than-a-trade-deal-oped

Mattlin, M.; Wigell, M. (2016): “Geoeconomics in the context of restive regional powers”, Asia Eur. J. 2016, 14, 125–134

Vihma, A. (2017): “Geoeconomics defined and redefined”, Geopolitics 2017

Wigell, M. (2016): “Conceptualizing regional powers’ geoeconomic strategies: Neo-imperialism, neo-mercantilism, hegemony, and liberal institutionalism”, Asia Eur. J. 2016, 14, 135–151.

[iv]Paragraph 15, Joint Statement of BRICS leaders, Ekaterinburg, Russia, 16 June 2009.

[v]“We will continue to firmly oppose protectionism. We recommit to our existing pledge for both standstill and rollback of protectionist measures and we call upon other countries to join us in that commitment.” Para 32, page 16, BRICS Xiamen Declaration, September 2017.

[vi]The2017 China-India border standoff, often referred to asDoklam standoff,involves the border skirmishes between theIndian Armed Forcesand thePeople’s Liberation Armyof China over Chinese construction of a road inDoklamnear the trijunction of Bhutan, China and India. Unlike China and Bhutan, India does not claim Doklam but supports Bhutan’s claim. Chinese troops’ initiation of construction of roads in June 2017 led to retaliation by Indian forces. The situation reached a political and military deadlock and continued till 28 August, 2017 when both China and India announced withdrawal of all their troops from the site.

The views expressed above belong to the author(s). ORF research and analyses now available on Telegram! Click here to access our curated content — blogs, longforms and interviews.

Dr. Nilanjan Ghosh is a Director at the Observer Research Foundation (ORF), India. In that capacity, he heads two centres at the Foundation, namely, the ...

PDF Download

PDF Download