-

CENTRES

Progammes & Centres

Location

PDF Download

PDF Download

Tanu M. Goyal, "Building Future-Proof Global Value Chains," ORF Issue Brief No. 531, March 2022, Observer Research Foundation.

Introduction

The global economy has witnessed a transformative shift in recent years. While global production networks have suffered occasional shocks in the past, recent events such as the COVID-19 pandemic, the US-China trade war, and the setback to the multilateral trading system have highlighted the volatility in global value chains (GVCs).

There have been several debates on the sustainability and fragility of GVCs over the past few years. While gains from specialisation have been acknowledged, there is an ongoing discourse on the risks related to international dependence that result in the transmission of shocks. Thus, most recent discussions focus on strengthening GVCs and making them resilient to global shocks.

Economist and Nobel laureate Wassily Leontief (1941) was among the first to discuss the idea of interconnectedness between different parts of an economy by describing the structure of the American economy between 1919 and 1939.[1] Leontief highlighted the cross-industry relationships and deep links between production structures, such that shocks or disturbances in one industry affected others, even if they were not directly related. With globalisation, such interconnectedness extended beyond national borders. When a multinational company (MNC) engages stakeholders to produce goods or services across multiple geographical locations for worldwide markets, it results in the formation of global production networks.[2] A GVC is formed when different countries are involved in producing or distributing goods. Shocks to GVCs, such as the COVID-19 pandemic, can affect industries worldwide. This brief examines the formation of global production networks, how global shocks and risks are transmitted through the networks (thereby affecting GVCs) and emphasises the need to make the value chains more resilient and sustainable in the long term.

Establishing Production Networks: From Fordism to Specialisation

While globalisation has led to production systems expanding beyond territorial boundaries, such structures have seen significant developments over the span of the 20th century. The first half of the century was characterised by ‘Fordism’,[a],[3] where production systems were dominated by multi-domestic structures that were largely self-sufficient. Although international production did exist at this time, transnational corporations mainly replicated the operations of the parent enterprises.[4] It was only in the 1970s that production systems became ‘flexible and spatially dispersed’,[5] giving rise to what was characterised as global production networks. The trigger for this shift was the rising competition from newly industrialised countries, such as Japan and the ‘tiger economies’ of Hong Kong, Singapore, South Korea, and Taiwan. To address competition, firms in the Western economies began reorganising production processes, taking advantage of the relatively low production costs in the East. Firms gradually adopted flexible specialisation, which resulted in the distribution of production processes into specialised tasks.

A firm can establish production networks either by entering into contract manufacturing agreements or through foreign direct investments (FDI) in the host country. Traditionally, cost was seen as a key determinant of a firm’s decision; for instance, the horizontal expansion of MNCs are likely only when the trade cost of importing the final goods from an existing facility producing such goods is relatively high. This is what influenced firms to locate vertically-linked subsidiaries in countries where intra-firm trade costs are low.[6] These vertically-linked subsidiaries result in the establishment of production networks.

As countries liberalise international trade policies, other factors started to influence a firm’s choice to establish production networks in other countries, such as demand and supply factors. The determining factors include transaction costs (for instance, the costs of writing contracts and doing business); transportation costs, the nature and presence of trade restrictions; the size of the market, and consumer taste and preferences; and investor protection through investor-to-state dispute resolution under investment treaties and comprehensive agreements, among other things. Whether a firm opts for contract manufacturing or FDI is influenced by the transaction cost of entering a contract and the host country’s institutional and governance structures, among other things.

Existing studies highlight various reasons for establishing production networks through FDIs, including market-seeking, efficiency-seeking, strategic asset-seeking, and resource-seeking investment.[7]

Global Value Chains, Trade, and the Transmission Effect

With the establishment of production networks, many products are being made in fragments as firms divide their production worldwide. This is also reflected in a shift in international trade, from the trade of goods to the trade of value-added. Indeed, increased trade in intermediate goods is a novel feature of globalisation. Parent-to-affiliate input trade is an element of vertical production networks and results in intra-firm flows of inputs and output.[9] When firms specialise in a particular set of activities in one country to produce parts and components for other countries, they spread their production process across countries, resulting in the formation of GVCs. The automobile industry and the electronics manufacturing industry are cases in point. Indeed, over two-thirds of world trade currently occurs through GVCs, with production processes occurring in several countries before the final products are assembled.[10] Table 1 shows the foreign content in gross exports and exports of manufacturing products of some of the major trading nations in 2018.

Some large trading nations in South and Southeast Asia, particularly in the Association of Southeast Asian Nations region, have a very high share of foreign value-added content in their exports (see Table 1).

Table 1: Foreign Value-added Content of Exports (percentage share)

| Country / Region | Manufacturing | Gross Export | ||

| 2005 | 2018 | 2005 | 2018 | |

| Canada | 33.3 | 37.2 | 23.12 | 24.88 |

| China | 26.4 | 19.3 | 23.67 | 17.24 |

| France | 28.7 | 33.8 | 21.55 | 24.35 |

| Germany | 23.85 | 27.46 | 22.47 | 22.90 |

| India | 23.2 | 28.9 | 16.42 | 19.85 |

| Italy | 26.1 | 29.1 | 20.63 | 23.15 |

| Japan | 13.2 | 21.1 | 11.19 | 17.21 |

| Korea | 35.7 | 34.9 | 31.77 | 31.99 |

| Malaysia | 53.4 | 42.9 | 43.61 | 34.79 |

| Mexico | 47.5 | 45.9 | 32.76 | 35.92 |

| Russian Federation | 10.2 | 11.8 | 8.06 | 8.56 |

| Saudi Arabia | 13.3 | 11.0 | 3.73 | 3.71 |

| Spain | 33.1 | 34.9 | 24.28 | 23.81 |

| Switzerland | 30.9 | 29.8 | 25.02 | 23.95 |

| Thailand | 48.0 | 42.1 | 40.93 | 34.58 |

| United Kingdom | 23.8 | 30.0 | 15.22 | 17.83 |

| United States | 16.6 | 15.8 | 10.95 | 9.50 |

| Association of Southeast Asian Nations | 40.2 | 37.4 | 32.71 | 32.01 |

| European Union | 16.1 | 18.6 | 13.38 | 15.83 |

Source: Data extracted from the Trade in Value-Added (TiVA) database, and shares calculated by the author

One of the world’s largest exporters, China has some of the largest assembling factories, especially in the consumer electronics sector, telecommunications, information technology, and automotive industries. China is also at the end of several value chains, originating in Asia and Western market economies. The share of foreign content in China’s export and manufacturing sectors remains high despite some reduction in recent years.

According to the World Trade Organization (WTO),[11] nearly two-thirds of all intermediate imports of information and communication technology products from Asia—specifically from Japan, South Korea, and Taiwan—and Europe and North America are used as inputs into Chinese exports. Moreover, data shows that intermediate goods exports exceed capital goods and finished products exports as an increasing volume of parts and components are traded for use in subsequent international production and exports.[12]

At the same time, several events have caused disruptions in global production networks. The Asian financial crisis, the global financial crisis, geopolitical or trade disputes between nations, and the COVID-19 pandemic have severely impacted GVCs.[13],[14] For instance, when the US closed a bridge connected to Mexico in the aftermath of the 2001 terror attacks, several auto plants shut down because of input shortages.[15] Interconnected networks result in a transmission of shocks (see Figure 1). Indeed, production functions can act both as a mechanism to propagate shocks throughout the economy and as a means of translating microeconomic disruptions into macroeconomic ones.[16] Given the level of trade through GVCs, this may also be reflected in global trade and the trade of manufactures.

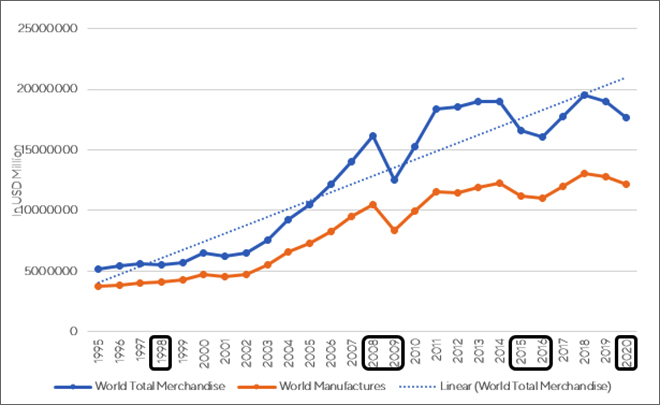

Figure 1: Trends in Total Merchandise Trade and Trade in Manufactures (1995-2020)

Between 1995 and 2008-09, there has been a rise in the total merchandise trade and trade in manufactures. The rise was steeper after 2001 when China joined the WTO, a phase often referred to as a period of hyper-globalisation.[17] While overall total merchandise trade and world trade in manufactures indicate rising trade, there are clear dips, particularly around the global financial crisis (2008-09), the US-China trade war (2015-16), and because of the ongoing pandemic (2020).

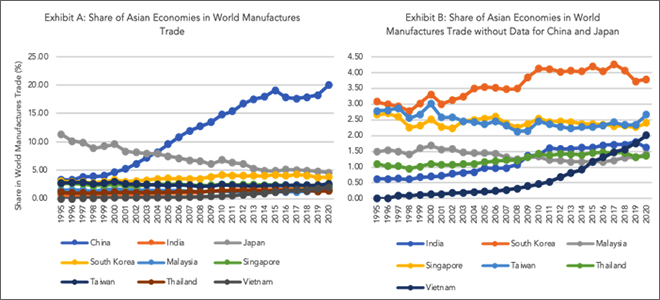

The share of certain Asian economies[c] in the total trade of manufactures shows that there has been a shift in the share of trade in manufactures of different economies (see Figures 2A and 2B).

Figure 2A: Share of Select Asian Economies in World Manufactures Trade (1995-2020)

Figure 2B: Share of Select Asian Economies in World Manufactures Trade, Excluding China and Japan (1995-2020)

China’s share in world manufactures trade steadily increased over the years before experiencing a slight dip after 2015, attributable to the US-China trade war (see Figure 2A). The US imposed a tariff of around 25 percent on nearly half the products imported from China, which affected China’s share of global trade and disrupted major production chains. Nevertheless, in 2020, China accounted for nearly 20 percent of the world manufactures trade. In comparison, Japan has seen a consistent drop in the share of manufactures trade over the past 25 years. This is because the total output in Japan continues to decline, and the country is also relocating its production to other lower-cost destinations in Asia, such as Taiwan.[18] In the first quarter of 2021, Japan experienced a 1.3-percent reduction in output, while China registered a 13.6-percent increase.[19]

South Korea has one of the largest shares of manufactures trade among the other Asian economies (around 3.75 percent in 2020), which broadly shows a rising trend with occasional dips (see Figure 2B). The shares of Singapore, Thailand, Taiwan, and Malaysia have remained constant, with a slight increase in 2020. India’s share increased after 2008-09, only to decline marginally in 2020, and Vietnam’s share in total manufactures trade saw a steep rise after 2008-09. Vietnam could experience further growth if the US and other states relocate their production networks to that country.[20]

Falling trade shares are also an outcome of a fall in manufacturing output. In 2020, global manufacturing output declined due to disruptions caused by the pandemic—China and some other East Asian countries (such as Vietnam, Thailand, and the Philippines) experienced nearly immediate impacts from the crisis, while industrialised economies saw delayed effects.[21] While there has been a gradual recovery in 2021, especially in the manufacturing sector—with China, India, Vietnam, South Korea, Taiwan, and Singapore recording increases in output, largely attributable to the positive performance of the computer, electronics and pharmaceuticals industries—the pandemic has exposed the vulnerabilities in GVCs and the need to enhance supply chain resilience.

Boosting Supply Chain Resilience: Recommendations

Events of global significance, such as the COVID-19 pandemic, have highlighted the adverse impacts of localised and systemic risks to the functioning of GVCs. During the pandemic, both supply and demand shocks were rampant—a supply shock in China was followed by a demand shock across the world. Countries increased trade restrictions and adopted inward-looking strategies to protect domestic markets. For instance, some countries imposed temporary restrictions on non-commercial exports of protective equipment or implemented export licensing requirements for essential commodities to ensure sufficient supply domestically. The exports of certain medicinal products were temporarily prohibited. There was greater political and economic pressure to create jobs locally and increase domestic output. Overall, there was a need for greater competitiveness and lean manufacturing practices, and to make supply chains resilient.[22]

Asian economies, particularly China, were the first to experience the crisis’s adverse effects, which affected production. Due to the interconnected production networks, China’s supply-side disruption of manufacturing output of other nations resulted in a “supply chain contagion”.[23] The disruption of a country’s domestic production depends on its direct and indirect exposure to foreign production. As multi-country production networks have grown more complex, indirect exposure has become an increasingly important consideration. As a result, the pandemic reignited the debate on building supply chain resilience, especially to ease the vulnerabilities of production networks.

Building supply chain resilience can minimise the impact of external shocks and systemic risks. This can be done in two ways—diversifying the supply chain and shortening it to reduce the dependence on many external suppliers.

Conclusion

Global production networks have made vast contributions in emerging markets and developing economies by setting up manufacturing facilities, creating jobs, and generating income. But disruptions in such supply chains, as seen during the COVID-19 pandemic, can result in many economic risks. This has highlighted the importance of making GVCs more resilient.

Going forward, there is a need to diversify GVCs to include new commodities and services and make them leaner. MNCs must look beyond the traditional methods of organising production and regions. Digital technologies and new methods of organising production are critical to strengthening GVCs. Digital technologies can be deployed in processes such as customs clearance to reduce the time, paperwork and number of processes involved. Similarly, a leaner supply chain—arrived at by reducing the number of fragments involved in the manufacturing process and ensuring that most of the goods produced in a country are consumed domestically—will also boost resilience to external shocks. Indeed, several large firms are already experimenting by deploying these into their manufacturing processes, a development that must be considered more widely.

Endnotes

[a] Fordism, as a specific form of microscale organisation of mass production, first emerged in the US in the early 20th century at the Ford Motor Company and is named for Henry Ford. Ford’s mass production model built upon previous advances in manufacturing methods.

[b] North-South investments refer to investments from developed countries to developing/least developed countries.

[c] The countries have been selected based on their share in the total trade of manufactures.

[1] Wassily W. Leontief, The Structure of American Economy: 1919-1939 (New York: Oxford University Press, 1941)

[2] Neil M. Coe and Henry Wai-Chung Yeung, Global Production Networks: Theorizing Economic Development in an Interconnected World (Oxford: Oxford University Press, 2015)

[3] Ray Hudson, “Fordism”, International Encyclopaedia of Human Geography, (2009): 226-231

[4] Coe and Wai-Chung Yeung, Global Production Networks

[5] Coe and Wai-Chung Yeung, Global Production Networks

[6] Maggie Xiaoyang Chen, “Interdependence in Multinational Production Networks”, The Canadian Journal of Economics, 44, no. 3, (2011): 930-956

[7] John, H. Dunning, “Re-evaluating Benefits of Foreign Direct Investment” in Transnational Corporations, 23-51 (Geneva: United Nations, 1994); John, H. Dunning “Determinants of Foreign Direct Investment: Globalization-Induced Changes and the Role of Policies” in Toward Pro-Poor Policies: Aid, Institutions and Globalization, 279-290 (Washington: The World Bank, 2003)

[8] Gordon H. Hanson, Raymond J. Mataloni Jr. and Matthew J. Slaughter, “Vertical Production Networks in Multinational Firms,” The Review of Economics and Statistics, 87, no.4 (2005): 664-678

[9] Hanson, Mataloni Jr. and Slaughter, Vertical Production Networks in Multinational Firms

[10] World Trade Organization, Technological Innovation, Supply Chain Trade and Workers in a Globalised World: Global Value Chain Development Report 2019, WTO, 2019.

[11] Global Value Chain Development Report 2019

[12] Coe and Wai-Chung Yeung, Global Production Networks

[13] World Trade Organization, Measuring and Analyzing the Impact of GVCs on Economic Development. Global Value Chain Development Report 2017, WTO, 2017.

[14] Piergiuseppe Fortunato, “How COVID-19 is changing global value chains,” UNCTAD, September 2, 2020.

[15] Hanson, Mataloni Jr. and Slaughter, Vertical Production Networks in Multinational Firms

[16] Vasco M. Carvalho and Alireza Tahbaz-Salehi, “Production Networks: A Primer,” Annual Review of Economic, no. 11 (2019): 635-663.

[17] World Trade Organization, Global Value Chain Development Report 2021: Beyond Production, WTO, 2021.

[18] United Nations Industrial Development Organization, World Manufacturing Production: One Year of Covid-19 (Statistics for Quarter 1), UNIDO, 2021.

[19] World Manufacturing Production: One Year of Covid-19 (Statistics for Quarter 1)

[20] NITI Aayog, Government of India, Export Preparedness Index 2020.

[21] World Manufacturing Production: One Year of Covid-19 (Statistics for Quarter 1)

[22] Willy C. Shih, “Global Supply Chains in a Post-Pandemic World,” Harvard Business Review, September-October 2020.

[23] Richard Baldwin and Eiichi Tomiura, “Thinking Ahead About the Trade Impact of Covid-19” in Economics in the Time of COVID-19, (London: Centre for Economic Policy Research, 2020): 59-71

[24] Asia Briefing, “Why Companies Relocate to Vietnam”.

[25] Baldwin and Tomiura, Thinking Ahead About the Trade Impact of Covid-19

[26] Global Value Chain Development Report 2019

[27] Global Value Chain Development Report 2021

[28] Shih, Global Supply Chains in a Post-Pandemic World

[29] Global Value Chain Development Report 2021

[30] “Factoryless Goods Producers”, Eurostat.

The views expressed above belong to the author(s). ORF research and analyses now available on Telegram! Click here to access our curated content — blogs, longforms and interviews.

Tanu M. Goyal is a Consultant at the Indian Council for Research on International Economic Relations (ICRIER) New Delhi. She has over ten years of ...

Read More +