-

CENTRES

Progammes & Centres

Location

Since 2019, inflation has been a major cause of concern for the economy, having breached the Reserve Bank of India’s inflation target levels. In recent times, COVID-induced consequences have managed to keep inflation well beyond the RBI limit. This article analyses the trends in inflation bringing to light the reasons underlying it while concluding that nothing much beyond a patient wait and watch policy can be assumed by regulatory authorities to correct the inflationary trends.

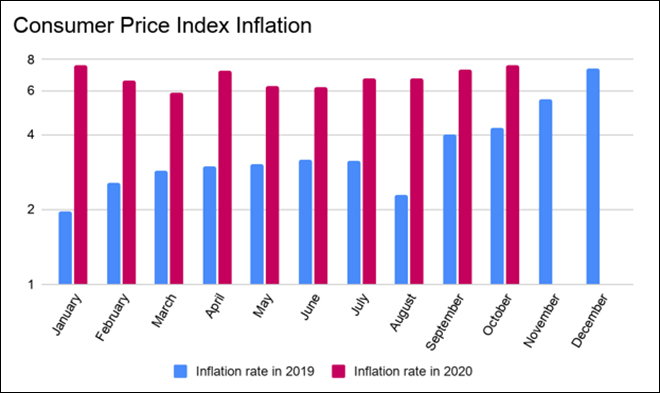

| Month | Inflation rate- 2019

(in percentage) |

Inflation rate- 2020

(in percentage) |

| January | 1.97 | 7.59 |

| February | 2.57 | 6.58 |

| March | 2.86 | 5.91 |

| April | 2.99 | 7.22 |

| May | 3.05 | 6.26 |

| June | 3.18 | 6.23 |

| July | 3.15 | 6.73 |

| August | 2.28 | 6.69 |

| September | 3.99 | 7.27 |

| October | 4.26 | 7.61 |

| November | 5.54 | - |

| December | 7.35 | - |

Source: Ministry of Statistics and Programme Implementation

The tabulated data can be visually compared in the graph below.

The data informs us that inflation increased at a rapid rate in 2019. At the beginning of the year, the inflation rate was at 1.97 percent which surged to 7.35 percent by the end of the year. The month-on-month inflation rate continued to grow and was the highest by the end of the year.

The graph shows a huge gap in inflation rates of the same month between the two years. The largest gap can be observed in January. In January 2019, the inflation rate was 1.97 percent while the inflation rate in January 2020 is 7.59 percent.

An interesting observation is that even before the onset of the COVID-induced lockdown, the inflation was as high as 7.35 percent in December 2019. The fundamental cause of this surge was the rise in vegetable prices because onions became more expensive. The primary reason for onion prices shooting up was the unseasonal rains received in major onion-producing states. This unfavourable situation not only damaged the kharif onion crop, which is usually harvested at the end of the year, but also took a toll on the existing supply of stored onions. The limited stock of onions coupled with scarcity in the incoming supply of the kharif onion made the prices of existing quantities of onion spiral up to as high as INR 200 per kilogram.

Before this, an inflation rate of around 7 percent was last experienced in 2014. The government could control inflation back then due to easy domestic and international economic conditions, especially the falling crude oil prices that otherwise extensively add to India’s import bill and hence inflation. In 2019, the Government undertook several measures to curb inflation, such as releasing the buffer stock of onions, prohibiting onion export and resorting to importing onions. But neither measures helped ease the upward pressure of inflation, which eventually increased to 7.59 percent in January 2020. Finally, in February 2020, the retail inflation eased to 6.58 percent and further down to a 5.91 percent in March with an incoming fresh stock of onions lowering their price.

The Indian economy was gradually recovering from the onion crisis accompanied by a decline in oil prices, when it suffered a massive blow from the nationwide lockdown imposed to deal with COVID-19. It resulted in inflation rates soaring up once again.

Historically, the buffer stock of food grains has always rescued India during periods of high food inflation despite the inflation numbers going up to double digits. With demand-pull inflation, the aggregate demand exceeds the aggregate supply. However, in the lockdown months of March to June, while the demand for essential food commodities started increasing the agriculture sector production also rose by 5.6 percent. The primary problem during the COVID-19 lockdown that led to a rise in inflation, despite having sufficient food stock, were several disruptions in the supply chain rather than failure in production. With constraints in logistics (transport, warehousing, storage etc.) and manufacturing, the economy faced a supply shock.

Moreover, the rise in inflation in October 2020 is higher than that of January 2020. The easing of lockdown restrictions has not eased retail inflation. The price of vegetables has flared up to 22.51 percent, which is the highest in the commodity basket. The prices of eggs have risen to 21.81 percent while that of meat and fish has increased to 18.7 percent. Staple food has become unaffordable to some segments of the society.

The COVID-19-triggered unemployment has disproportionately worsened the economic situation of informal constituencies rather than those operating in the formal sector. India’s informal employment accounts for about 90 percent of the workforce. Millions around the country are still below the poverty line. The pandemic has led to a further increase in the number of poor. The Phillips curve hypothesises an inverse relationship between inflation and unemployment, which is intuitively plausible as well. On the contrary, in April, the unemployment rate skyrocketed to 27.1 percent while retail inflation also stayed as high as 7.22 percent.

The government measures taken to curb inflation by imposing stock limits, reducing import duties and importing onions and potatoes proved ineffective. The stimulus package announced at the beginning of lockdown did not do much in reviving the economy or in boosting the supply either. The relaunch of the lockdown situation in several areas has made economic recovery difficult by creating additional problems in the functioning of the economy and is threatening the possibility of a revival. The government has done a satisfactory job in attempting to control inflation. Nevertheless, beyond the measures taken, there is very little that the government can do when it comes to tackling the problem of food inflation. No wonder then that inflation has risen to 7.61 percent in October 2020.

The economy is already reeling under the burden of stagflation. There is a rising fear that retail food inflation may spiral into other forms of inflation and reflect in the prices of various commodities that use agricultural produce as an input. Wages may well be revised upwards if inflation expectations are adversely influenced by the current inflation.

The RBI previously anticipated a reduction in inflation but with a steep rise in the October inflation numbers, any possibility of the Monetary Policy Committee making rate cuts to support economic revival is ruled out. But the good news is, the RBI hopes that with an incoming bountiful harvest of the kharif crop, the food inflation is expected to recede in December. If that happens, the RBI can work towards rate cut decisions and enable economic recovery.

Akanksha Shah is Research Intern at ORF Mumbai

The views expressed above belong to the author(s). ORF research and analyses now available on Telegram! Click here to access our curated content — blogs, longforms and interviews.

Renita DSouza is a PhD in Economics and was a Fellow at Observer Research Foundation Mumbai under the Inclusive Growth and SDGs programme. Her research ...

Read More +