-

CENTRES

Progammes & Centres

Location

The likelihood of Pakistan defaulting on its foreign obligations this year appears more imminent than ever

Characterised by a deluge of sweeping civil disobedience movements, nearly empty forex reserves, catapulting prices of essential commodities like wheat, onions, milk, and meat, unabating bouts of power blackouts, and a struggling population that goes to polls this year, Pakistan is on the verge of an economic and political meltdown. Moreover, the government led by Prime Minister Shehbaz Sharif is troubled due to the internal political turmoil stoked by the Imran Khan-led government that was ousted in the country's first successful no-confidence motion since its independence, and external duress from intergovernmental agencies vis-à-vis the International Monetary Fund (IMF).

Disruptions in the supply chain brought on by the pandemic have severely affected economies worldwide, including Pakistan, affecting all sectors, from retail traffic to automobile manufacturing. The COVID-19 surge towards the end of 2022 in China—the second largest economy which contributes to approximately 18 percent of the global GDP, and is inextricably linked across Global Value Chains (GVCs) in South and Southeast Asia — had once again added fresh blows in terms of the spillover impact on the rest of the world.

The country's substantial debt burden of US$ 126 billion primarily comprises external loans acquired from China and Saudi Arabia.

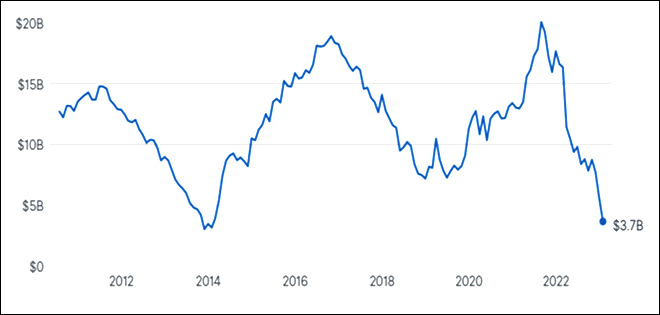

By February 2023, Pakistan's foreign exchange reserves have reached an unprecedented level, plunging to a historic low of US$ 3.19 billion. This amount was only sufficient to cover the nation's import expenses for a mere two weeks, falling significantly short of the three months' import cover mandated by the IMF. The situation is aggravated by the fact that Pakistan is faced with the daunting task of repaying an enormous debt of US$ 73 billion by 2025, all while grappling with a volatile political landscape and unpredictable lending nations. The country's substantial debt burden of US$ 126 billion primarily comprises external loans acquired from China and Saudi Arabia.

Figure 1: Trends in Pakistan's Foreign Reserves

Source: State Bank of Pakistan

Despite the seemingly strengthened ties between Pakistan and China, the security concerns posed by violent separatist groups in Sindh and Balochistan cannot be overlooked. These groups pose a significant threat to the safety of Chinese nationals working in these regions. In response, China has raised the possibility of discontinuing its developmental initiatives under the aegis of the Belt and Road Initiative (BRI) and the China-Pakistan Economic Corridor (CPEC) projects in Pakistan. Moreover, China has proposed the deployment of Chinese security firms to protect its citizens involved in these ventures. However, granting permission for Chinese security agencies to operate within Pakistan would diminish the Pakistan Army's ability to safeguard the well-being of foreign nationals. Additionally, the international perception of Pakistan as a breeding ground for terrorist activities hampers the country's prospects for foreign investments and assistance.

Again, Saudi Arabia has been a relatively stable benefactor except for occasional demands for immediate repayment of a fraction of the debt extended to Pakistan. While the relations between the Royal Family of Saud and Pakistan have evolved into strategic partnerships, with Pakistan buttressing the former's military force and Saudi Arabia providing critical investments in the latter, the future of this friendship is undoubtedly rooted in geopolitical and religious interests.

Pakistan's historical and cultural ties with its two key allies, China and Saudi Arabia, have been deeply rooted, despite contemporary circumstances suggesting otherwise. China's involvement in Pakistan's development and trade can be traced back to the 1960s when they extended interest-free credit of approximately US$ 85 million (equivalent to several billion dollars today) for technological and infrastructural projects. Following the Sino-Indian war, bilateral trade agreements were also signed to accelerate industrialisation in Pakistan.

Saudi Arabia has been a relatively stable benefactor except for occasional demands for immediate repayment of a fraction of the debt extended to Pakistan.

China and its commercial banks have provided approximately 30 percent of Pakistan's total external debt, which exceeds US$ 100 billion. This proportion surpasses even the financial support received by debt-laden Sri Lanka from China, accounting for 20 percent of its total public external debt. Moreover, the recent disbursement of an additional US$ 700 million from the China Development Bank (CDB) in early 2023 to mitigate the impending financial crisis further exacerbates the burden of external debt obligations that Pakistan faces this year.

Again, Saudi Arabia, as Pakistan's steadfast partner in the Islamic world, has been assisting since 1943, in response to Muhammad Ali Jinnah's appeal for support. Pakistan, in turn, has contributed to enhancing Saudi Arabia's military capabilities, particularly in nuclear and arms security. These diplomatic alliances have evolved over the decades within the context of a rapidly changing geopolitical landscape in a highly interconnected globalised world. They serve as a testament to successful international partnerships based on shared interests.

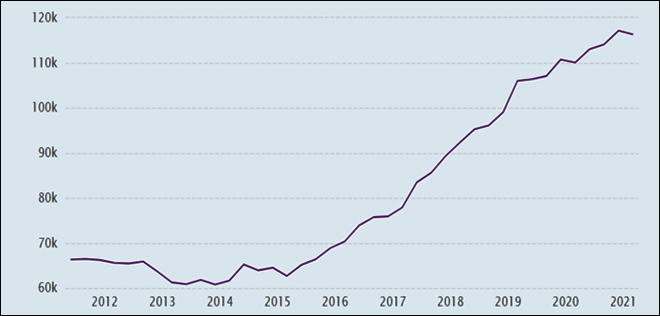

Figure 2: Pakistan's Total External Debt (in US$ million) from 2006 to 2022

Source: CEIC / State Bank of Pakistan

The likelihood of Pakistan defaulting on its foreign obligations this year appears more imminent than ever. The nation's dollar-denominated bonds, set to mature next year, have reached an all-time low, causing investors to anticipate the potential consequences. This situation is worsened by the country's low foreign exchange reserves and upcoming repayments amounting to US$ 7 billion in the coming months, including a debt of US$ 2 billion owed to China. Additionally, Pakistan's fate seems increasingly uncertain as negotiations with the IMF for bailout progress slower than the country's ability to avert a debt default and stabilise the sharply declining bond prices, which have fallen by approximately 60 percent. As Pakistan finds itself sinking deeper into unsustainable debt, it becomes crucial to closely examine the ostensibly advantageous foreign partnerships that have thus far provided some support.

(Note: ORF published a more detailed version of this article by the same author in May 2023. See here: Occasional Paper No. 403 “Debt ad Infinitum: Pakistan’s Macroeconomic Catastrophe”)

Soumya Bhowmick is an Associate Fellow with the Centre for New Economic Diplomacy, at the Observer Research Foundation

(Note – For a more detailed analysis, please see ORF Occasional Paper No. 403 “Debt ad Infinitum: Pakistan’s Macroeconomic Catastrophe”)

The views expressed above belong to the author(s). ORF research and analyses now available on Telegram! Click here to access our curated content — blogs, longforms and interviews.

Soumya Bhowmick is a Fellow and Lead, World Economies and Sustainability at the Centre for New Economic Diplomacy (CNED) at Observer Research Foundation (ORF). He ...

Read More +