-

CENTRES

Progammes & Centres

Location

A normal monsoon and the consequently softer inflation in food prices could force RBI’s hand on both its policy stance as well as on the policy rate front

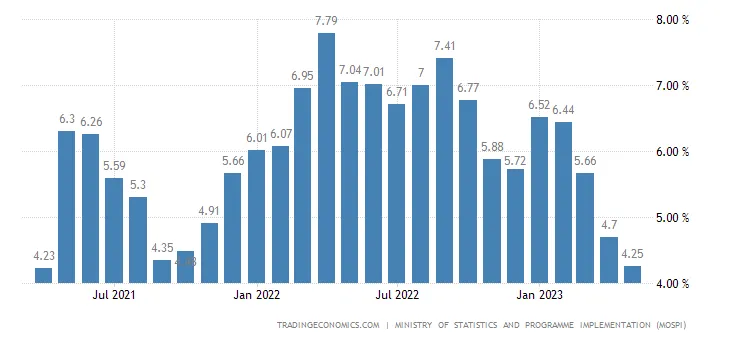

With India’s economic growth momentum expected to ease over the coming months, the Reserve Bank of India (RBI) was expected to shift focus from inflation targeting—not that there is much inflation left to target—to stimulating demand. This is especially true given that retail inflation now stands at its lowest since April 2021 (see Figure 1), while wholesale deflation has hit a multi-year high (see Figure 2). Even the extra gross domestic product (GDP) growth during the last quarter of FY2022-23 was driven significantly by the sharp downward revision of the trade deficit by 28 percent between the second advance estimate in February 2023 and the provisional estimate released in May 2023.

Figure 1: India’s consumer price index (CPI) based inflation rate over time

Figure 2: India’s wholesale price index (WPI) based inflation rate over time

On the other hand, the real concern is about the key role of crude oil prices and trade deficits, with the possibility of cheap crude oil from Russia—which helped curtail India’s import bill and trade deficit—soon becoming a thing of the past, and thereby, hindering the latter’s economic growth.

On the consumption front, while enhanced passenger vehicle sales, domestic air passenger traffic, and credit card outsourcing may indicate a pick-up in urban demand, aggregate private final consumption expenditure remains largely non-discretionary—typical of an economy with low income per capita and high-income inequality. Investment activity is also underwhelming, with growth in steel consumption, and cement output resulting more from increased investment in housing and services sectors, rather than manufacturing.

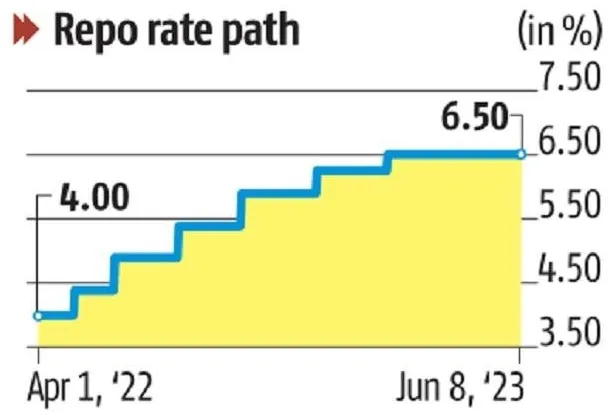

On 8 June 2023, however, the six-member monetary policy committee (MPC) of the RBI surprisingly opted to persist with the status quo in the repo rate for the second consecutive review meeting, justifying itself on the basis of lower inflation and a supposedly encouraging growth outlook. Concurrently, the RBI chose to prioritise inflation targeting, which was ostensibly suspended over the past three years because of successive external shocks to India’s economy, never mind the central bank’s cumulative repo rate hike of 2.5 percent since April 2022 (see Figure 3).

Figure 3: The trajectory of RBI’s repo rate since April 2022

Source: Business Standard

Further, the central bank decided to maintain uncertainty over when it may consider changing its policy stance, with perspectives differing among the MPC members.

The MPC’s decision to maintain rates in successive policy meetings is inducing investments in duration schemes since there are expectations that rates might have peaked. Most debt mutual funds (MFs) are of the view that up-to-three-years is the choicest tenure, while some are even endorsing longer duration papers, with bond yields likely trending downwards. The appeal of the latter category is based on the fact that inflows into fixed income—particularly duration funds—are far below expectations since a significant proportion of inflows into the three-year-plus tenure materialised in the final week of March. Notwithstanding this, it is the short end of the yield curve which seems to be offering attractive accruals without assuming notable duration risk. This is despite the 10-year bond yield currently trading at 7 percent (see Figure 4).

Figure 4: India’s 10-year bond yield over time (Source: investing.com)

Despite the uncertainty, it is important to monitor whether policy rates peak sooner rather than later. A perception of a nearer peak would incentivise inflows into funds with tenures of at least three years, in spite of indexation benefits having been removed. This is because a parallel downward shift in the yield curve is likely at first, but the curve will steepen when central banks start cutting rates two-to-three quarters down the line.

Since the repo rate has been maintained at 6.5 percent, external benchmark lending rates (EBLRs) linked to the repo rate will not rise. For existing home loanees, the rate hike pause entails that equated monthly instalments (EMIs) are likely to remain stable over the short run. This is because EBLRs—81 percent of which are linked to the benchmark repo rate—now dominate the mix of outstanding floating rate loans, with their share rising from 48.3 percent by December 2022, while the share of such loans based on marginal cost of funds-based lending rate (MCLR) eased to 46 percent. Home loan interest rates from most banks will therefore persist in the higher single digit percentages, probably just sufficient to sustain the sales momentum witnessed over the past quarter.

With the pause in rates, banks are not expected to tinker with their term deposit rates either. Any change on this front could only result from surplus liquidity in the banking system due to increases in low-cost current account and savings account (CASA) balances following the withdrawal of INR 2,000 currency notes.

Home loan interest rates from most banks will therefore persist in the higher single digit percentages, probably just sufficient to sustain the sales momentum witnessed over the past quarter.

On the economic growth front, external Monetary Policy Committee (MPC) member Jayant Varma opines that the monetary policy is now in precarious proximity to levels at which it can significantly harm the economy. With inflation expectedly on the decline, fellow external MPC member Ashima Goyal feels it is salient to guarantee that the real repo rate does not rise too high and damage the economic cycle. However, in RBI Governor Shaktikanta Das’s view, India’s macroeconomic fundamentals are strengthening and growth prospects are steadily improving and becoming broad-based.

The Standard & Poor's (S&P) Global rating have maintained its GDP growth forecast for India at 6 percent, claiming that the country’s economy will be the fastest growing amongst Asia Pacific countries. The status quo in the forecast has been partly attributed to India’s domestic economic resilience. The rating agency expects the RBI to cut interest rates only early next year.

While pegging its FY2023-24 growth forecast at 6.3 percent, fellow ratings agency Fitch Ratings is concerned that the complete effect of the 2.5 percentage points of rate hikes by the RBI is yet to be experienced. It added that “consumers have also experienced a drop in purchasing power as inflation increased sharply in 2022, and household balance sheets have also weakened through the pandemic.” The trepidation is shared by the Organization of Economic Co-operation and Development (OECD), which has set its growth forecast for India at 6 percent, while retaining that soft global demand and the impact of monetary policy tightening will restrict economic growth in FY2023-24.

The grouping of wealthy nations expressed particular consternation over RBI’s monetary tightening depressing purchasing power and household consumption, especially in urban areas, and admitted that most risks to its growth forecasts for India are inclined toward the downside. “Tighter financial market conditions are reflected in weakening credit-supported demand for capital goods, a good proxy for business investment,” it said.

With India’s economic growth expected to cool off over the foreseeable future due to lacklustre growth in discretionary consumption and underwhelming animal spirits, the government may have little option but to step in and support the economy’s momentum, especially with the general elections less than a year away.

On the other hand, the RBI seems quite sanguine on economic growth having reiterated its projection of 6.5 percent GDP growth, as even the World Bank cut its forecast by 30 basis points (bps) to 6.3 percent and the International Monetary Fund (IMF) by 20 bps to 5.9 percent.

While some international ratings agencies may link a rating upgrade for India to fiscal discipline, the RBI’s dogmatic pursuit of inflation targeting is set to hurt aggregate demand. With India’s economic growth expected to cool off over the foreseeable future due to lacklustre growth in discretionary consumption and underwhelming animal spirits, the government may have little option but to step in and support the economy’s momentum, especially with the general elections less than a year away.

As such, a fiscal stimulus through tax incentives or increased government spending may boost economic growth over the medium term. Moreover, the inflationary risks would be limited given that unemployment at 7.33 percent is above its natural rate of 5 percent. The resulting job growth would also bolster the ruling political dispensation’s electoral prospects, further incentivising such a move. It remains to be seen whether New Delhi’s economic planners bite the fiscal deficit bullet to do what appears increasingly necessary.

Aditya Bhan is a Fellow at Observer Research Foundation.

The views expressed above belong to the author(s). ORF research and analyses now available on Telegram! Click here to access our curated content — blogs, longforms and interviews.