-

CENTRES

Progammes & Centres

Location

While it might be tempting to dismiss the importance of international rating agencies based on periods of robust inflows of foreign investment, the impact of their rating actions are far from trivial

India made a vocal appeal last month to United States (US)-based rating agency Moody for a sovereign rating upgrade, and also inquired over the parametric basis for the firm’s rating actions. The call was made during a meeting between Moody’s Investors Service representatives and Indian government officials, ahead of the former’s yearly examination of sovereign ratings. The Indian side used the opportunity to emphasise the reformed and resilient pillars of the Indian economy.

Going by the buzz on the street, the Indian economy seems a bright spot in a sombre world. Going by the ratings, though, it is just trudging on. Growing at a faster pace than other big economies, India has proved itself a sustained outlier over recent years. However, a superior sovereign rating remains elusive in spite of the purportedly robust fundamentals driving the economic growth.

The Indian side used the opportunity to emphasise the reformed and resilient pillars of the Indian economy.

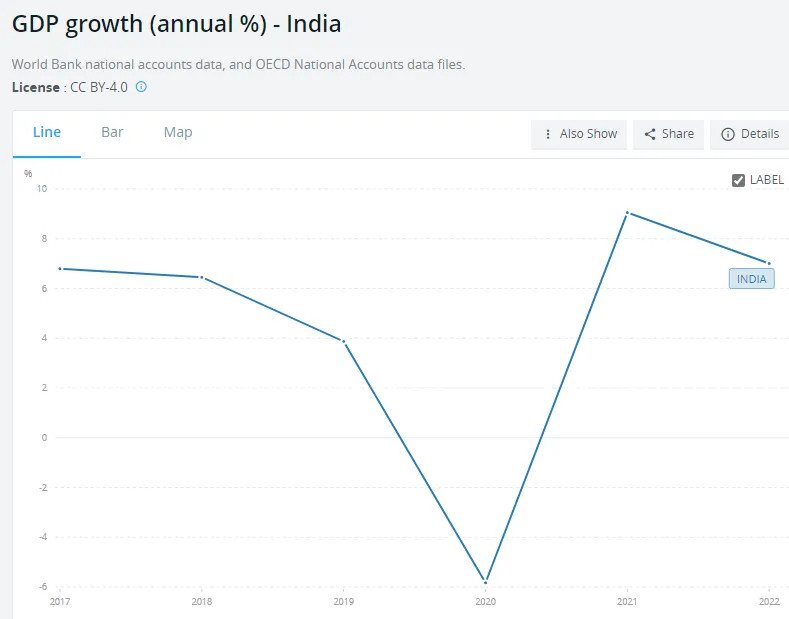

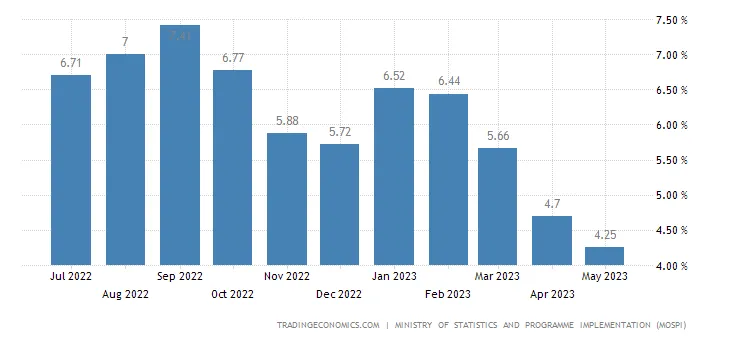

India’s gross domestic product (GDP) surpassed US$3.5 trillion in 2022, with economists opining that the country will remain the fastest-growing economy among the G20 over the coming few years (see Figure 1). While inflationary pressures continue to afflict numerous nations, India has successfully tamed inflation domestically (see Figure 2).

Figure 1: India’s GDP growth rate over time

Source: World Bank

Figure 2: India’s CPI-based inflation over time

It remains a mystery to many, then, as to why the three leading international rating agencies (IRAs) maintain the lowest investment-grade rating on India.

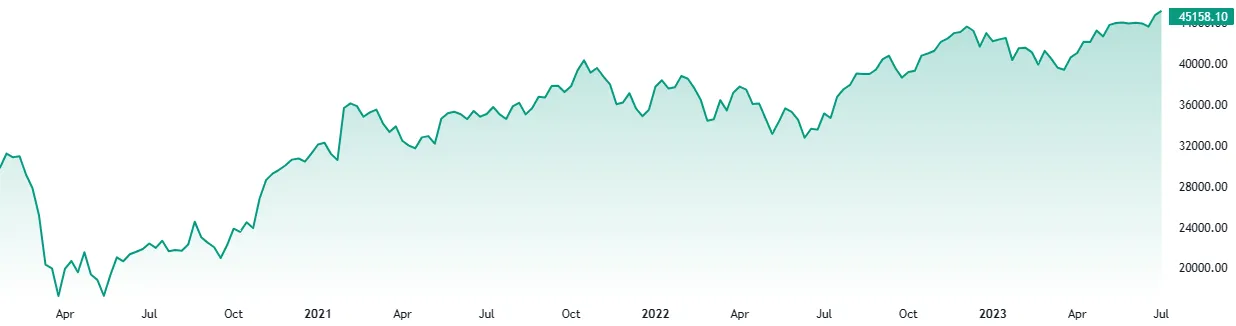

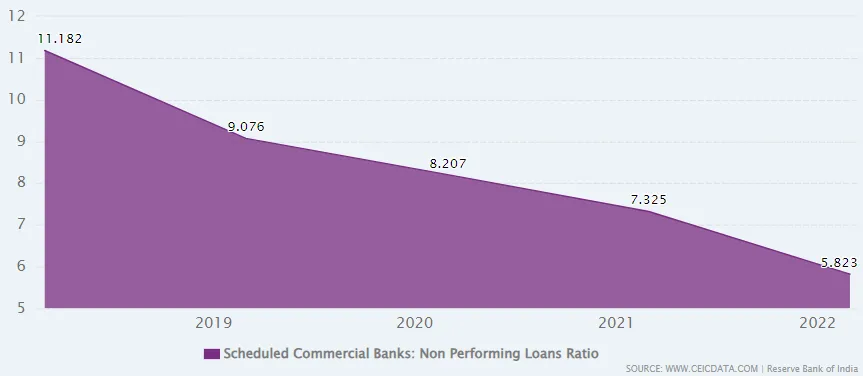

While it might be tempting to dismiss the importance of IRAs like Moody’s, based on periods of robust inflows of foreign investment, the impact of their rating actions are far from trivial. For instance, shares of Indian banks witnessed a sharp decline after Moody’s downgraded the outlook of Indian banks from stable to negative in April 2020, ostensibly based on the deteriorating asset quality of Indian banks due to the COVID pandemic (see Figure 3). The move also created obstacles for banks recovering from prevailing non-performing asset (NPA) problems, due to an increase in the cost of borrowings (see Figure 4).

Figure 3: The value of India’s Bank Nifty index over time (Source: tradingview.com)

Figure 4: Non-performing loans ratio of Scheduled Commercial Banks

The salience of these ratings must not be underestimated as they play a key role in determining how foreign investors assess a country’s creditworthiness, and thereby impact borrowing costs of overseas capital. The ratings impact Indian firms looking to source international finance, as many believe that a firm’s rating cannot surpass that of its nation.

Unfortunately, only three IRAs—namely S&P Global Ratings, Moody’s and Fitch—dominate the global rating landscape. In addition to Moody’s, S&P is also headquartered in the US, while Fitch is headquartered in both the US and the United Kingdom. Interest rates on sovereign debt are determined based on the ratings provided by these firms. Because these agencies constitute a global cartel despite being largely US-based, the US and its companies often receive superior ratings. Many investment decisions internationally are also impacted by the ratings provided by these IRAs.

The ratings impact Indian firms looking to source international finance, as many believe that a firm’s rating cannot surpass that of its nation.

A better rating for India, therefore, would signal that the nation is a safer investment destination, resulting in lower interest rates on borrowings (see Figure 5 and Table 1). At present, Moody’s has a ‘Baa3’ long-term sovereign credit rating on India, with a stable outlook. Notably, ‘Baa3’ is the lowest long-term investment grade rating. It is no wonder, then, that apart from emphasising India’s economic reform trajectory, infrastructure development, and robust foreign exchange (forex) reserves, the Indian government officials also grilled Moody’s on its rating criteria (see Figure 6).

Figure 5: India’s 10-year bond yield over time

Source: Trading Economics

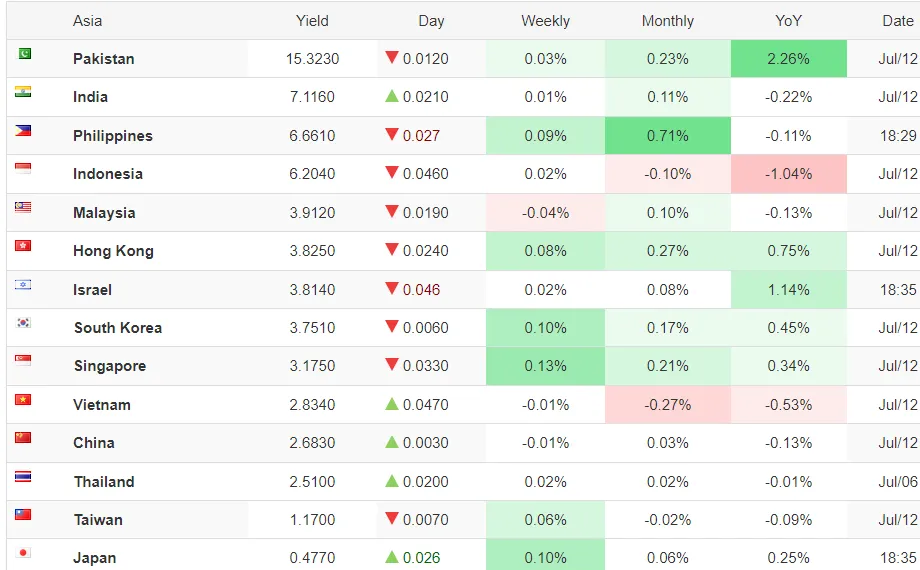

Table 1: India’s 10-year bond yield currently exceeds all its Asian peers except Pakistan

Source: Trading Economics

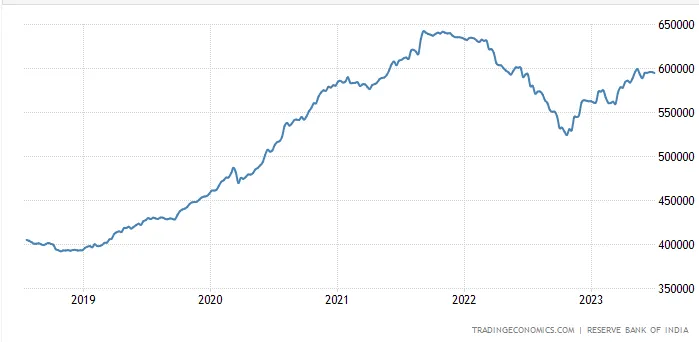

Figure 6: India’s forex reserves (in million USD) over time

In fact, India has been persistently inquiring over the parameters used by IRAs while assigning credit ratings and has encouraged them to embrace transparency while forsaking subjectivity. The country has been appealing for reform in sovereign credit rating methodology to reflect countries’ capacities and disposition to service their debt obligations.

India’s complaint with inferior sovereign ratings is not a new issue. Policymakers, for long, have felt that India’s fundamentals are estimated in conjunction with those of advanced economies. As Finance Minister in 2016, Arun Jaitley had expressed his displeasure publicly by pointing out that given the steps taken by New Delhi on the policy front, India had yet to receive from IRAs “the full recognition of the effort” put in. Even Arvind Subramanian, as then Chief Economic Advisor, had alluded to the “poor standards” of IRAs in the Economic Survey 2016-17.

The Economic Survey 2020-21 was more direct in its criticism of IRAs, stating with historical data and references that “Never in the history of sovereign credit ratings has the fifth largest economy in the world been rated as the lowest rung of the investment grade (BBB-/Baa3). Reflecting the economic size and thereby the ability to repay debt, the fifth largest economy has been predominantly rated AAA. China and India are the only exceptions to this rule.”

The fact is, there is nothing unusual in there being discussions and reviews between governments and IRAs. As on previous occasions, though, no tangible benefit has materialised. And while India’s rating remains unchanged due to a fixed mindset, nations like the US continue to raise debt at roughly half the interest rate applicable to India, with this situation unlikely to change over the foreseeable future.

If objectivity is the aim, then IRAs would do well to evaluate developing countries and emerging markets on the basis of a realistic and tangible yardsticks-based framework, which is applied transparently across the board. This could be achieved by overtly segregating

1) the analysis of simulations and stress tests (fully disclosing the underlying model used); and

2) the more subjective (qualitative) analysis;

with 1) and 2) published distinctly, though within the same report.

Aditya Bhan is a Fellow at the Observer Research Foundation.

The views expressed above belong to the author(s). ORF research and analyses now available on Telegram! Click here to access our curated content — blogs, longforms and interviews.