-

CENTRES

Progammes & Centres

Location

A careful reading of the first quarter estimates of 2022-23 raises quite a few questions about whether the Indian economy is back on the growth path.

Preliminary estimates of the first quarter (Q1) gross domestic product (GDP) in 2022-23 are out. Real GDP at constant (2011-12) prices in Q1 of 2022-23 is estimated at INR 32.46 lakh crore, registering 13.5 percent year-on-year growth over the last financial year. Nominal GDP (at current prices) in Q1 of 2022-23 is estimated at INR 64.95 lakh crore, showing a growth of 26.7 percent over the first quarter GDP in the last financial year. The gap between nominal and real GDP clearly underlines the prevailing inflationary situation in the economy. A GDP growth of 13.5 percent is indeed an encouraging sign for the Indian economy. However, this growth is lower than the 16.2 percent forecast by the Reserve Bank of India and the 15.5 percent projection by a Bloomberg poll of economists. After the negative impact of different waves of COVID-19 in Q1 for two consecutive years (2020-21 and 2021-22), this year’s Q1 rebound was expected to be bigger than the actual.

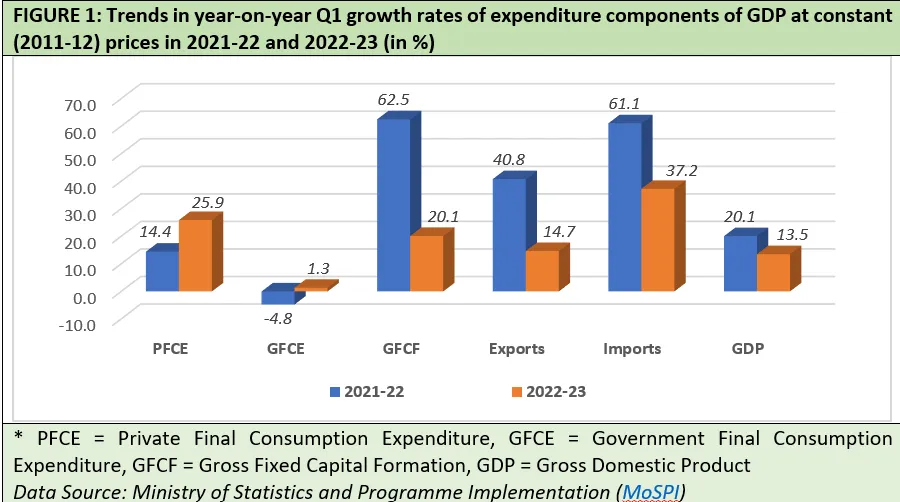

Private consumption and investment (GFCF) have revived well in Q1 of 2022-23. Exports growth is also healthy. However, imports growth is quite high at 37.2 percent. Compared to growth rates in Q1 of 2021-22, growth rates in different macro expenditure components may seem relatively lower, but one has to remember that Q1 2021-22 growth rates were on a very low 2020-21 base (Figure 1). First quarter of 2020-21 was the severe lockdown period when there were bare minimum economic activities.

With a decent revival in GDP, the growth rates in all components have now started to moderate. This is due to the phased withdrawal of whatever fiscal boost was being provided for the last two years. Only time can tell whether this is a wise move or not.

As rupee slid lower vis-à-vis the US dollar in recent times, import bills increased and resulted in a sizeable 37.2 percent growth in Q1 of 2022-23. This can turn out to be a teething trouble for the economy in near future. During the pandemic, government expenditure largely kept the economy running. With a decent revival in GDP, the growth rates in all components have now started to moderate. This is due to the phased withdrawal of whatever fiscal boost was being provided for the last two years. Only time can tell whether this is a wise move or not.

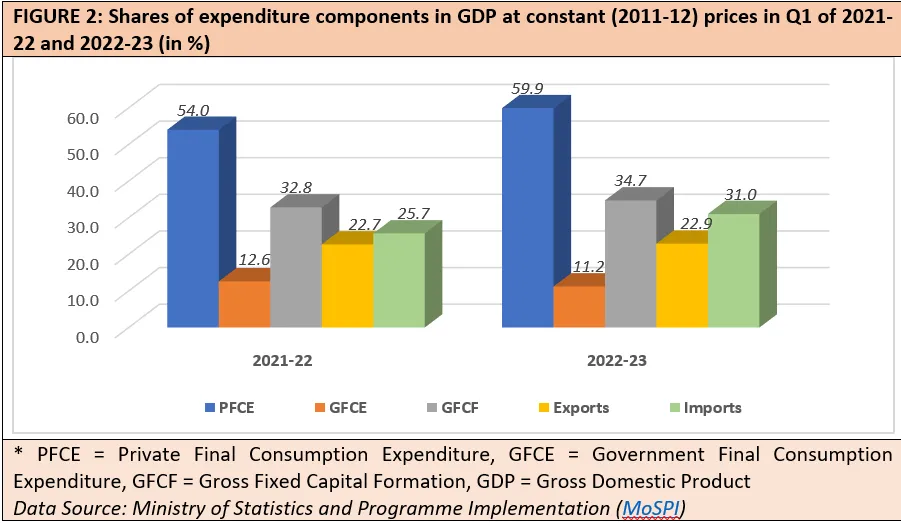

When one looks into the trend in shares of expenditure components in GDP, then these broader directions appear more prominent. The good news is that private consumption and investment appear to be driving the revival of GDP. With the assumption that this trend will continue, government expenditure growth is on the decline. But the spoiler element is provided by unexpected rise in imports, fuelled by rupee depreciation as one of the principal factors (Figure 2).

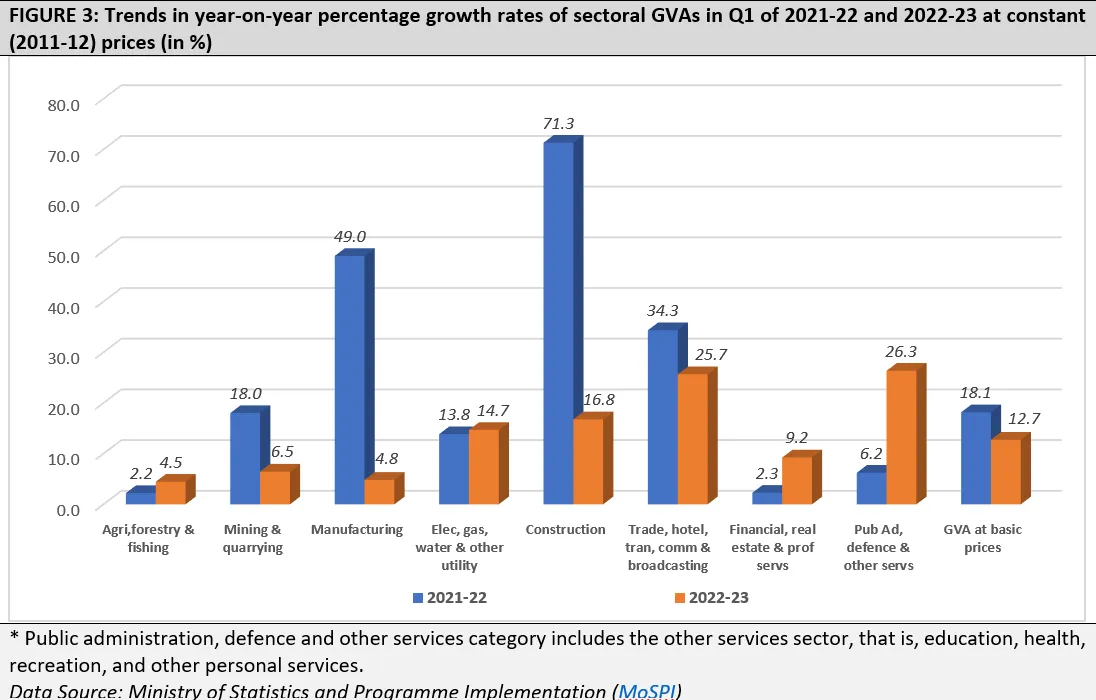

However, estimates of sectoral Gross Value Added (GVAs) in Q1 of 2022-23 provide more clarity in current state of the economy. In Q1 of the last financial year, manufacturing growth was very large at 49 percent. This growth, of course, was calculated on a negligible statistical base as the previous year’s first quarter was characterised by strict large-scale lockdowns. The manufacturing growth rate has now fallen down to 4.8 percent in Q1 of 2022-23 (Figure 3). This is not a good sign.

The construction growth rate has also moderated from 71.3 percent last year to 16.8 percent in Q1 of 2022-23. With heightened economic activities across the sectors, the growth rate in electricity, gas, water, and other utilities has marginally increased from 13.8 percent last year to 14.7 percent in this year’s Q1. For the same reason, financial, real estate, and other professional services experienced a larger growth rate at 9.2 percent in Q1 of 2022-23. These two sectoral growth rates matched the expectations.

However, the two largest growth rates have been observed in the public administration, defence, and other services sector, and trade, hotel, transport, communication, and broadcasting services sector respectively. The release of pent-up demand helped in achieving a higher growth rate in sectors like the tourism and hospitality industries. That helped in revival, but the continuation of consumer demand at the same level in near future may not be a realistic assumption to make.

Fiscal interventions are withdrawn with an assumption that the economy is already back on the growth path. But a careful reading of the first quarter estimates of 2022-23 raises quite a few questions about that assumption.

The highest sectoral growth rate is observed in the sector which includes public administration, defence, health, and education. Most sections of this sector are not exactly market-oriented and heavily dependent on government support. Gradual decline in overall government expenditure may adversely affect future growth of this sector.

Agriculture showed a lower but steady growth at 4.5 percent in the first quarter of 2022-23. However, this year’s erratic rainfall and subsequent diminished harvesting are likely to slow down crop production. This can potentially fuel another round of food inflation. If that happens, then there will be adverse impacts across all sectors.

Investment in industries, particularly in manufacturing, will be the key to returning to a sustainable economic growth path. There are indications in the economy that informal sector enterprises in the services sector of the economy remain the weakest link in post-pandemic economic recovery. This has resulted in a K-shaped recovery where established big businesses are driving the GDP, but the vast expanse of informal sectors is still languishing on the verge of survival. This can lead to chronic problems in creating enough consumer demand in future.

In this situation, the gradual withdrawal of various fiscal stimulus measures may backfire on the economy. Fiscal interventions are withdrawn with an assumption that the economy is already back on the growth path. But a careful reading of the first quarter estimates of 2022-23 raises quite a few questions about that assumption.

The views expressed above belong to the author(s). ORF research and analyses now available on Telegram! Click here to access our curated content — blogs, longforms and interviews.

Abhijit was Senior Fellow with ORFs Economy and Growth Programme. His main areas of research include macroeconomics and public policy with core research areas in ...

Read More +