-

CENTRES

Progammes & Centres

Location

Immediate measures need to be taken to ensure that the economic impact of the pandemic, the domestic political turmoil, or the Ukraine–Russia conflict do not have an everlasting effect on the nation’s future.

Sri Lanka has been making headlines across the globe due to the unprecedented economic crisis that the island nation slid into in the recent past. There is some glimmer of hope as on 18 August 2022 Sri Lanka’s Central Bank Governor mentioned that while the current account deficits are slowly contracting due to the rise in exports and decrease in the import bill, “the forex situation has improved now and we (the Sri Lankan economy) have been able to pay for essentials such as petrol, diesel and medicine”. However, the crisis-hit economy is expected to shrink by 8 percent during this calendar year—which is more than double the contraction of 3.6 percent in 2020 when the pandemic raged. Against this backdrop, it will be interesting to analyse the trends in Sri Lanka’s Balance of Payments (BOP), and how the recurring deficits structurally weakened the macroeconomic stability of the country in the last few years.

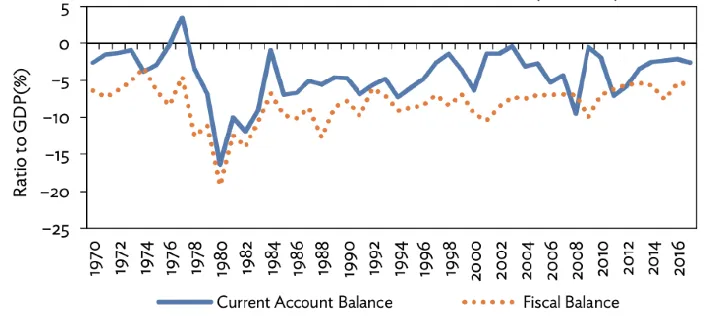

Sri Lanka is a classic case of the ‘twin deficit’ hypothesis which states that a nation’s current and fiscal account balances tend to move in the same direction. This phenomenon is typically true for developing consumption-driven economies, with high levels of debt on both the domestic and the international fronts. As the country holds excess demand levels, which necessitate increased imports to match the consumer’s needs, and further drives inflation—which has happened in the case of Sri Lanka—the commodities thus being produced domestically have often been seen as less competitive in global export markets.

Figure 1: Trends in Sri Lanka’s Current Account Balance and Fiscal Balance (1970-2016)

Source: Asian Development Bank, data from Central Bank of Sri Lanka

There are two main reasons for this; firstly, following the Keynesian approach, the increasing budget deficits lead to domestic absorption causing surging imports that further widen the current account deficits and vice versa. Secondly, drawing from the Mundell-Fleming model, increasing budget deficits causes the interest rates to be revised upwards and the reverse is also true. As the interest rates increase, the domestic economy becomes more attractive to foreign investors causing surging surpluses in the capital account, and rising deficits in the current account. Capital account surpluses can adversely affect a current account, where increased liquidity raises consumption demand, which would bring about the need for increased imports, thus leading to current account deficits. Alternatively, capital inflows may improve the value of the domestic currency which will make imports cheaper and create domestic demand and make exports expensive which in turn will lead them to fall in value, thus, again widening the current account deficits.

The macroeconomic problem standing in Sri Lanka’s way is the argument that such double deficits have continued to increase its reliance on foreign debts. For decades, the country has depended on multilateral and bilateral borrowings to finance its current account deficits as well as key developmental programmes. This has directly contributed to the economy becoming vulnerable to exogenous shocks such as the pandemic, which caused credit availability to dry up in the international markets.

The 2019 tax cuts before the pandemic had already dented the nation’s tax revenues and further increased its fiscal deficits. There was a reported loss of approximately one million taxpayers between 2020 and 2022 at a time when the economy was already suffering from widespread tax evasion. The suddenness of the pandemic and the restrictions induced by it cost a lot to the national exchequer in mobilising the inevitable social security measures, which had further widened the fiscal deficits.

In addition to this, the full-fledged switch to organic farming in April 2021 destroyed some of the robust agricultural sectors in Sri Lanka due to the decline in crop productivity, excess demand in the agricultural sectors, etc. The economy’s self-sufficiency in rice production was completely disrupted, and Sri Lanka had to import rice from countries such as Myanmar and China. Additionally, tea, which was a major commodity of export had also suffered due to the unplanned agricultural reforms in the country. The trade deficits fell from US$1085 million to US$762 million between December 2021 and March 2022. Dwindling forex reserves have hurt the value of the Sri Lankan rupee as well. The currency fell by approximately 7.3 percent in 2021, and sent import costs through the roof, triggering inflation followed by social unrest. The additional pressures on the fiscal and current accounts had further deteriorated the situation in Sri Lanka.

Current and capital account balances in Sri Lanka have historically moved in opposite directions to each other. While the former has languished in disastrous figures for a while, the capital accounts have been in surplus levels. Understandably, the government tried to attract additional foreign investors to steady the ship by allowing the Chinese-built Colombo Port City to operate under a special tax-relief system for the next 40 years, which is another example of the government banking on foreign investors who were hesitant to invest in an economy built on such shaky grounds.

Figure 2: Historical Trends in Sri Lanka’s Current and Capital Account Balances (in US$ million)

Source: Maitra (2017)

The plummeting current account, paired with the relatively slow-growing capital account has led to a huge issue with the BOP deficits over the last year in particular, and the country is unable to fund the people’s demand for essential goods. Immediate measures need to be taken to ensure that the economic impact of the pandemic, the domestic political turmoil, or the Ukraine–Russia conflict do not have an everlasting effect on the nation’s future.

Figure 3: Sri Lanka’s recent Balance of Payments (BOP) Trends (in US$ million)

Source: CEIC, data from Central Bank of Sri Lanka

Sri Lanka is set to ask Japan to take charge of inviting the creditor nations such as China and India for possible talks on bilateral debt restructuring. An immediate International Monetary Fund (IMF) bailout is imperative since it will allow the government access to funds that it desperately needs; along with a pathway to international financial markets that have shown reluctance since Sri Lanka defaulted on its dues when it officially halted payments earlier this year.

The views expressed above belong to the author(s). ORF research and analyses now available on Telegram! Click here to access our curated content — blogs, longforms and interviews.

Soumya Bhowmick is a Fellow and Lead, World Economies and Sustainability at the Centre for New Economic Diplomacy (CNED) at Observer Research Foundation (ORF). He ...

Read More +