-

CENTRES

Progammes & Centres

Location

China’s de-dollarisation and its geopolitical ambitions, especially regarding Taiwan, are contradictory. It cannot disrupt regional peace while trying to establish the RMB as a trusted global currency.

Recent conflicts such as the Russia-Ukraine war and the Israeli-Palestinian crisis have reshaped the global geopolitical landscape. These events have not only heightened concerns about potential flashpoints, particularly between China and Taiwan, but have also highlighted the complex interplay between economic strategies and geopolitical ambitions.

The US Treasury data has thrown light on China’s economic strategies amidst rising geopolitical tensions. It reveals that Beijing sold US$53.3 billion worth of US Treasury and agency bonds, following a larger sell-off of approximately US$300 billion between 2021 and mid-2023. This divestment aligns with China’s apparent acceleration of de-dollarisation, aiming to reduce the dollar’s global dominance and promote the renminbi’s (RMB) international use. These economic moves reflect China’s long-term vision, the “Chinese Dream”. This vision, introduced by Xi Jinping in 2012, aims for national rejuvenation, asserting Chinese cultural superiority, and projecting China as a global leader by 2049.

China’s push for de-dollarisation is globally seen as a response to a perceived weaponisation of the US dollar and aims to protect its economic interests and reshape the global economic order.

De-dollarisation serves two key objectives of the Chinese Dream: firstly, positioning the RMB as an alternative to the US dollar; secondly, circumventing United States-centric sanctions in case of a conflict. This approach gained steam after extensive sanctions froze Russia’s foreign currency reserves following the outbreak of the Ukraine conflict. China’s push for de-dollarisation is globally seen as a response to a perceived weaponisation of the US dollar and aims to protect its economic interests and reshape the global economic order.

However, the question arises whether the balance between China's economic aspirations and its geopolitical goals is compatible. China’s ambitious strategy still faces significant challenges since it must navigate the complex dynamics of regional stability, international trust, and its own geopolitical aspirations.

The escalating tensions surrounding Taiwan have prompted numerous analyses. One notable study by The Diplomat, in 2022, provided insights into the likely positions of various countries in a potential China-Taiwan conflict. The analysis revealed a spectrum of support and neutrality among nations, with Russia, North Korea, and Myanmar offering unwavering support to Beijing. Countries such as Pakistan, Afghanistan, Laos, Cambodia, and Nepal were seen as closely aligned with China while others like Bangladesh, Indonesia, Thailand, and the Philippines were expected to maintain neutrality. India, Singapore, New Zealand, and Vietnam were positioned as leaning towards the US, but without explicitly criticising China. Only Australia and Japan were identified as reliable allies likely to back US interventions alongside Taiwan. Interestingly, many Asia-Pacific countries, including South Korea, a trusted US ally, refrained from issuing a formal statement altogether.

Figure 1

Source: Reuters

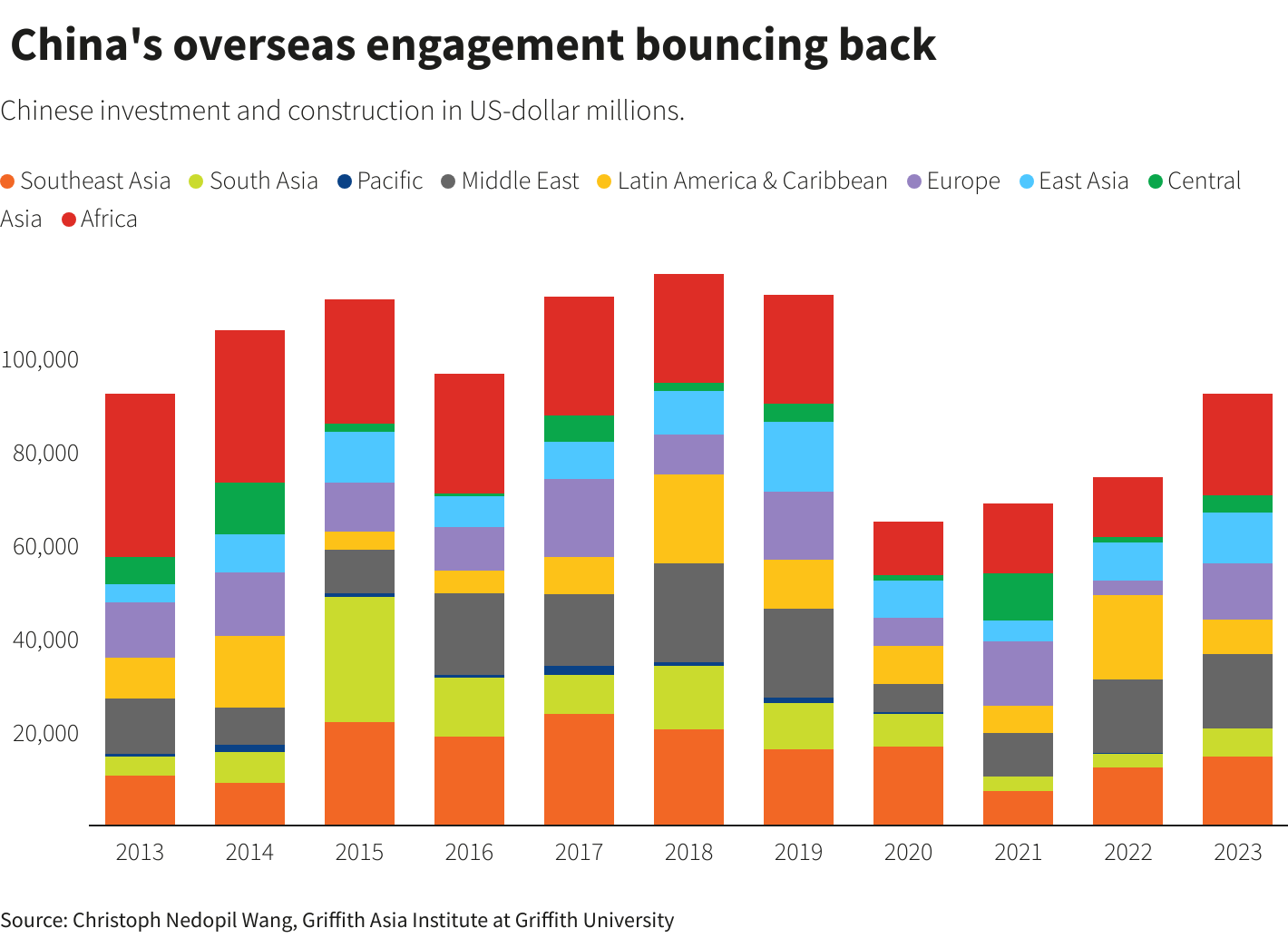

The economic dimension of this geopolitical landscape is equally significant. China's Direct Investment Abroad expanded by US$37.9 billion in March 2024, following a US$43.6 billion growth in the previous quarter. Chinese investment in Asia surged by 37 percent in 2023, particularly in Indonesia. In 2023, the Asia-Pacific region saw increased Chinese engagement through construction and non-financial investments, with about 94 deals worth US$37 billion, compared to US$29 billion in 2022. Contrastingly, Chinese investment in Europe (EU-27+UK) dropped to its lowest level since 2010, reaching €6.8 billion in 2023, from €7.1 billion in 2022. The share of investment in the “Big Three” European countries (France, Germany, and the United Kingdom) declined to 35 percent in 2023, down from an average of 53% between 2013-2022, yet it remains the third largest trading partner of the European Union (EU). The Griffith Asia Institute put China’s total engagement in Africa at US$21.7 billion, denoting a 114 percent growth in investment from the previous year, making Africa the largest regional recipient.

Given Chinese engagement worldwide, potential RMB internationalisation adds another layer of complexity. If the RMB gains prominence as an international currency, it could further influence the stance of countries in a potential conflict. Nations previously aligned with the US, such as India, Singapore, New Zealand, and Vietnam, might shift towards neutrality if the dollar’s dominance wanes.

The international economic environment is witnessing a significant shift away from the US dollar’s dominance, particularly in bilateral trade and national reserves. Russia has almost entirely abandoned the US dollar in their bilateral trade settlements. According to Russian officials, between January and October 2023, 68 percent of Russia-China trade was settled using the respective national currencies, with over 90 percent of mutual payments conducted similarly. This shift culminated in a recent trade deal worth up to US$260 billion, predominantly settled in Chinese yuan (95 percent) and the remainder in rubles and euros.

Source: Yahoo

While Russia and China are at the forefront of this shift, other countries are also exploring alternatives to the dollar. In the global oil trade, traditionally dominated by the US dollar, about 20 percent of the transactions are now conducted in alternative currencies. This shift gained momentum last year when Saudi Arabia expressed openness to settling trade in currencies other than the dollar. This visibly materialised at the end of the year, with a fifth of global oil trade settled in currencies other than the US dollar. The formal “expiration of the petrodollar” system in June 2024 further accelerated this trend, allowing countries to import oil without relying on US currency.

In Southeast Asia, a similar movement is gaining traction. Five of the largest economies in the region—Singapore, Malaysia, Indonesia, the Philippines, and Thailand—have signed a memorandum of understanding (MoU) to encourage the use of local currencies in trade settlements. The ASEAN has formally announced its intention to promote the use of local currencies in cross-border transactions. India, too, is making strides in this direction. The Reserve Bank of India (RBI) has approved 18 countries for rupee settlements. Moreover, India has signed a memorandum of understanding with countries like the United Arab Emirates (UAE) and Indonesia for bilateral currency settlements. These efforts are part of India’s broader strategy to internationalise the rupee and reduce dependence on the US dollar in international trade. The trend extends to Africa as well, where leaders are calling for the adoption of the Pan-African Payments and Settlement System (PAPSS) to decrease reliance on the US dollar for intra-African trade.

India has signed a memorandum of understanding with countries like the United Arab Emirates (UAE) and Indonesia for bilateral currency settlements.

Amidst these shifts, gold also has emerged as a popular alternative to dollar reserves. Countries such as Russia and China have significantly increased their gold purchases in recent years. The People’s Bank of China alone acquired 224.88 tonnes of gold in 2023 and continued this trend into 2024. This Chinese pivot towards gold is driven by the advantages it offers in bypassing sanctions, anonymity, and low traceability. Other countries, such as India, have also increased their gold purchases, obtaining 19 tonnes in the first quarter of 2024, surpassing their total acquisition of 16 tonnes during FY2023. The World Gold Council reported that central banks purchased about 1,136 tonnes of gold in 2022, worth approximately US$70 billion, highlighting the growing importance of gold in national reserves. However, it should also be reflected that this is still an emerging trend, and around two-thirds of total purchases were unreported, most likely from China and Russia, the foremost countries striving for de-dollarisation.

While de-dollarisation could benefit China’s RMB, its aspirations face several obstacles. China’s growing material power is offset by increasing challenges in its regional environment, particularly in the Asia-Pacific, where Beijing struggles to reconcile its desire to be a dominant international power with protecting its national interests. This balancing act has become increasingly difficult under Xi Jinping’s administration, as China’s more assertive stance often contradicts its vision of a “common future community.”

China’s growing material power is offset by increasing challenges in its regional environment, particularly in the Asia-Pacific, where Beijing struggles to reconcile its desire to be a dominant international power with protecting its national interests.

While some countries are increasing their use of RMB in trade settlements, most are not ready to accept it as a major reserve currency as they are pushing for trade in local currencies instead. Therefore, if China were to use force against Taiwan, it would severely disrupt regional peace and make international acceptance of the RMB even more challenging.

In substance, China’s de-dollarisation efforts and its geopolitical ambitions, particularly regarding Taiwan, are incompatible. The nation cannot simultaneously disrupt global peace and aspire to host the world’s most trusted currency. China’s strategy must address these contradictions to achieve its long-term economic and diplomatic goals.

Manini is a Research Intern at the Observer Research Foundation

The views expressed above belong to the author(s). ORF research and analyses now available on Telegram! Click here to access our curated content — blogs, longforms and interviews.

Manini is a Research Assistant at the Centre for Economy and Growth, ORF New Delhi. Her research focuses on the intersection of geopolitics with international ...

Read More +