Like any other country Indian economy is dealing with a once-in-a-lifetime tectonic disaster.

Exactly 101 years after 1918 flu pandemic, the world is again back to square one; widespread COVID19 lockdown has taken the global economy to a grinding halt and policymakers into uncharted territory; the responses till now have exposed the faultlines in the existing economic and healthcare models all over the world. Today’s connected globalised world facilitated the spread more rapidly than the earlier pandemic a century back. It would not be an overstatement to make that human civilisation forgot the lessons taught by history faster than the time required to spell ‘pandemic’.

However, a preliminary US research study found that an earlier and aggressive intervention to mitigate 1918 pandemic not only lowered mortality, but also lessened the adverse economic consequences of the pandemic. The regions which acted early and aggressively to contain pandemic showed a tendency to recover faster when the disaster was over.

Having noted that nugget of optimism, there is no denying that the world economy has been brought to its knees by the virus. According to the 2020 Q2 Global Forecast by the Economist Intelligence Unit (EIU), this game changer pandemic is expected to contract global output by 2.5% or more.

EIU forecast expects a modest rebound in the second half of 2020, assuming that the spread of coronavirus is largely contained and there is no second or third wave of the pandemic. If those assumptions fail, then impact will be harsher and longer.

| TABLE 1: Real GDP growth rates estimates, quarter on quarter (in percentage) | |||

| October - December 2019 | January - March 2020 | April - June 2020 | |

BRICS |

|||

| Brazil | 0.5 | -1.0 | -11.0 |

| China | 1.4 | -10.9 | 9.2 |

| India | 1.2 | 5.0 | -9.3 |

| Russia | 0.4 | -0.1 | -10.5 |

| South Africa | -0.3 | -3.0 | -7.7 |

G7 |

|||

| Canada | 0.1 | -0.3 | -4.5 |

| France | 0.8 | -2.0 | -10.0 |

| Germany | 0.0 | -3.0 | -10.0 |

| Italy | -0.3 | -5.0 | -10.0 |

| Japan | -1.8 | -0.5 | -0.4 |

| UK | 0.0 | -1.4 | -9.3 |

| USA | 0.5 | -1.3 | -5.9 |

| Source:Q2 Global Forecast 2020, Economist Intelligence Unit |

China, the epicentre of this pandemic, is expected to rebound but all other major economies are on the breakdown road in the April–June quarter of 2020 (Table 1). India’s contraction in this quarter is estimated to be -9.3%.

If we apply this negative rate of growth to the corresponding quarter’s GVA (Gross Value Added) of last financial year (at 2011-12 prices), Indian economy’s contraction in April–June 2020 is expected to be more than ₹3.1 lakh crore — roughly more than $40.87 million (if converted by current going exchange rate of $1 = ₹76.18). Conversion in constant prices and/or PPP (purchasing power parity) dollar terms would make this figure larger.

It is a no-brainer that the negative impact will be spread across sectors. To estimate the possible sectoral spread of the impact, sectoral shares in GVA are calculated using the First Advanced Estimates of 2019-20 at 2011-12 prices. In the next step, corresponding sectoral GVAs and growth rates are estimated accordingly (Table 2). The spread of the negative impact, thus, averaged out corresponding to the last year’s sectoral contributions to the GVA.

| TABLE 2: Sectoral GVA and growth rates estimates in April – June 2020 quarter | |||||

| April-June 2019 (in ₹ Crore) | GVA in 1st AE 2019-20 (in ₹ Crore) | Sectoral Share in 2019-20 GVA (in %) | Estimated GVA in Apr-Jun 2020 (in ₹ Crore) | Sectoral Gr. Rates in Apr-Jun 2020 (in %) | |

| Agriculture, Forestry & Fishing | 433547 | 1907605 | 14.1 | 427810 | -1.3 |

| Mining & Quarrying | 98887 | 376119 | 2.8 | 84351 | -14.7 |

| Manufacturing | 568104 | 2374176 | 17.5 | 532446 | -6.3 |

| Electricity, Gas, Water Supply & Other Utility Services | 78682 | 301966 | 2.2 | 67721 | -13.9 |

| Construction | 281262 | 1087210 | 8.0 | 243824 | -13.3 |

| Trade, Hotels, Transport, Communication & Services Related to Broadcasting | 649698 | 2616095 | 19.3 | 586700 | -9.7 |

| Financial, Real Estate & Professional Services | 821198 | 3027407 | 22.4 | 678943 | -17.3 |

| Public Administration, Defence & Other Services | 416628 | 1849803 | 13.7 | 414847 | -0.4 |

| GVA at Basic Price | 3348005 | 13540380 | 100.0 | 3036641 | -9.3 |

|

• Sectoral shares in 2019-20 are calculated on the basis of First Advanced Estimates of 2019-20.

• Estimated sectoral GVAs in April – June 2020 quarter are calculated assuming a -9.3% deceleration in overall GVA.

• Sectoral growth rates in April – June quarter are based on calculated estimations of GVA.

Data source: National Statistical Office (NSO), Ministry of Statistics & Programme Implementation, Government of India |

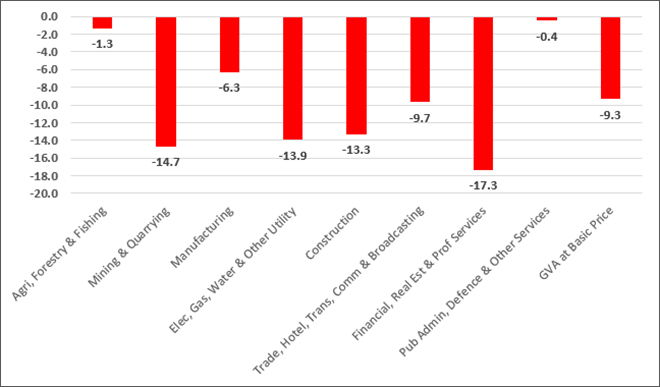

Financial, real estate & professional services are expected to be the worst-hit; followed by mining & quarrying; then electricity, gas, water supply & other utility services; and construction. Trade, hotel, transport, communication & services related to broadcasting, and manufacturing sectors are the next adversely affected sectors. Expectedly, agriculture, forestry and fishing, and public administration, defence & other services are the sectors relatively less affected in the short run.

Usual disclaimers apply here. The impact spreads are estimated with the overall base deceleration at -9.3%, as projected by the EIU estimates. Since economy is always in a dynamic mode, the sectoral shares in the gross output or GVA also tend to change every year. Mapping them on current fiscal year may have slight statistical discrepancies. So, any actual deviation in these assumptions or subsequent change in the estimates of GVA will obviously lead to change in absolute figures and the growth rates.

However, in the current scenario the trend in very short-term sectoral impacts is expected to follow the pattern described in Figure 1. Except for the agriculture, forestry & fishery and public administration, defence & other government services, all other sectors will suffer badly as the lockdown continues.

FIGURE 1: Estimated sectoral growth rates in GVA in April – June quarter (in percentage)

Data source: National Statistical Office (NSO), Ministry of Statistics & Programme Implementation, Government of India

Data source: National Statistical Office (NSO), Ministry of Statistics & Programme Implementation, Government of IndiaAmidst calamitous tidings, one small piece of good news has arrived in the form of rising IIP (Index of Industrial Production) in February 2020. Factory output grew by a seven-month high of 4.5%, buoyed by a rise of 10% and 3.2% in mining and manufacturing respectively.

Nonetheless, like any other country Indian economy is dealing with a once-in-a-lifetime tectonic disaster. These small marginal pre-lockdown advantages are likely to vanish in thin air. In the absence of a vaccine, lockdown and restrictive measures are undertaken as Hobson’s choice. But longer the lockdown continues, shriller will be the clamour for a gigantic fiscal stimulus eventually when it is lifted.

The views expressed above belong to the author(s). ORF research and analyses now available on Telegram! Click here to access our curated content — blogs, longforms and interviews.

Abhijit was Senior Fellow with ORFs Economy and Growth Programme. His main areas of research include macroeconomics and public policy with core research areas in ...

Read More +