-

CENTRES

Progammes & Centres

Location

With Awami League winning the 4th consecutive term, this re-election opens up interesting implications for the country’s economic future

Since Bangladesh’s independence in 1971, the country has undergone a notable economic transformation, transitioning from one of the world's poorest nations to one of the fastest-growing economies. Despite the country's positive performance in development metrics like the Human Development Index (HDI) and the Sustainable Development Goals (SDGs), the external macroeconomic shocks stemming from the pandemic and the Russia-Ukraine conflict have been detrimental to the nation's financial vulnerabilities. In the face of the challenges posed by the pandemic in 2020, Bangladesh managed to achieve a positive growth rate of 3.4 percent, out-performing many developing countries and garnering accolades for the ruling dispensation.

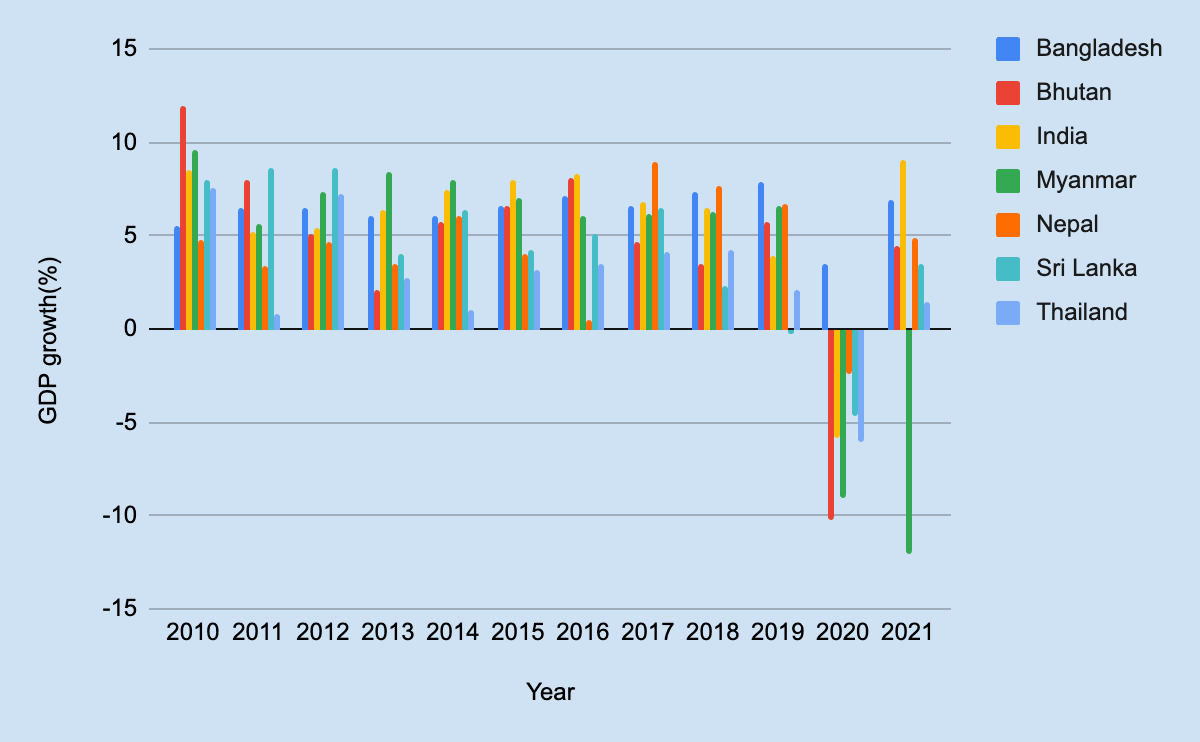

Figure 1: Annual GDP Growth Rates of BIMSTEC Nations (Percentage, 2010-2021)

Source: Author’s own, data from the World Bank

However, in late 2022, Bangladesh attracted international attention by, alongside Sri Lanka and Pakistan, seeking a loan of approximately US$ 4.5 billion from the International Monetary Fund (IMF). While this quest for financial assistance might be viewed as a precautionary measure, the underlying causes of Bangladesh's current economic situation are deeply entrenched in the inherent structure of its economy. As Bangladesh concludes its 12th parliamentary election on 7 January 2024, Prime Minister Sheikh Hasina’s party, Awami League, has won a fourth consecutive term, opening up interesting implications for the country’s economic future.

Despite impressive growth rates, Bangladesh faces challenges in its export basket's low diversification, particularly with heavy reliance on the textile and Ready-Made Garments (RMG) sector. More than 84 percent of Bangladesh's total export earnings in 2019–2020 came from garment exports, underscoring the sector's pivotal role in the country's economic landscape. However, the current volatility in global demand and labour-intensive production methods pose risks. While the service sector provides short-term support, diversifying the export mix in the long run is crucial.

More than 84 percent of Bangladesh's total export earnings in 2019–2020 came from garment exports, underscoring the sector's pivotal role in the country's economic landscape.

At present, Bangladesh maintains a tax-GDP ratio of 8 percent, ranking as the second-lowest in South Asia and lagging behind most lower-middle-income countries by approximately 5 percent. To be sure, the tax administration in Bangladesh faces challenges of institutional corruption that hinder revenue mobilisation and hence negatively correlates with the tax-to-GDP ratio, affecting taxpayer willingness to comply. Additionally, inadequate infrastructure, rising input costs, and stalled projects have widened fiscal deficits. Urgent anti-corruption measures, progressive tax systems, and expenditure rationalisation are essential for fiscal stability, addressing issues of inequality and aiding economic development.

Bangladesh confronts a series of economic challenges, with a significant import-export mismatch exacerbating issues in its current account and overall balance of payments (BOP). The direct impact of fiscal deficits, partly attributed to reduced exports and increased import bills, adds strain to the economic scenario. A decline in Foreign Direct Investment (FDI) further contributes to the fall in the capital account balance. Despite efforts to compress imports, a widening trade imbalance is evident, with a recorded US$ 3.8 billion trade deficit during the July-September quarter of FY 2023-24. Export promotion strategies, reducing dependency on imported inputs, and improving the business climate are necessary to address these macroeconomic imbalances.

Global events have affected interconnected macroeconomic parameters, including decreased remittances, FOREX depletion, and a weakening Bangladeshi Taka. The crises adversely affected businesses, with foreign reserves falling from US$ 39 billion to below US$ 32 billion in six months, alongside a 27-percent depreciation of the Taka in 2023. To safeguard diminishing reserves, the government implemented measures such as halting all non-essential imports and limiting the supply of dollars to commercial banks. Consequently, not only have banks been compelled to decline new letters of credit applications, but the assurance of timely payments to foreign suppliers for past imports has also become uncertain. Complemented by social security measures, urgent government action is crucial to stabilise the domestic economy and protect vulnerable sections.

Global events have affected interconnected macroeconomic parameters, including decreased remittances, FOREX depletion, and a weakening Bangladeshi Taka.

Despite a significant 80 percent increase in electricity generation capacity from 5 GigaWatts (GW) in 2009 to 25.5 GW in 2022, the Plant Load Factor (PLF)—the ratio of power generated to the maximum power capacity—has reached an all-time low for Bangladesh in 2022. It is imperative to confront the energy sector's demand-supply gap through technological upgrades and an accelerated transition to renewable sources. This approach aims to accommodate excess demand without hindering overall economic growth. Recent inflationary pressures, primarily driven by escalating food and fuel prices, further intensified by the Russia-Ukraine conflict, present short- to medium-term financial threats. This underscores the need to enhance domestic capabilities and foster diverse global partnerships, providing added impetus for resilience in these critical domains.

Bangladesh’s economy grapples with persistent inflation, posing challenges for citizens and economic stability. Contributing factors include cost-push elements, notably exchange rate depreciation, leading to a decade-high inflation in FY 2023. Despite a global decrease in inflation rates, Bangladesh has maintained around 10 percent inflation in 2023. Concurrently, the country's banking sector faces significant upheaval, exemplified by the largest private bank, Islami Bank, seeking financial assistance in 2022 to restore depositor trust amid a crisis rooted in loan fraud, capital flight, cronyism, and bureaucratic corruption. These economic challenges are intricately tied to the dynamics of patronage politics in Bangladesh, requiring a comprehensive understanding of both domestic and global economic dynamics for effective resolution.

Bangladesh faces the dual challenges of addressing inequality and managing the economic risks associated with rapid climate change. Despite progress on socio-economic indicators, efforts must be directed towards reducing inequality by allocating more financial resources to social expenditures, stimulating savings and investments, and ensuring inclusive growth. Simultaneously, the country grapples with the threat of climate change, marked by rising sea levels, urbanisation, and deforestation, jeopardising livelihoods and ecosystem services. In May 2020, during the initial surge of the COVID-19 pandemic, Bangladesh encountered its most powerful cyclone to date, Cyclone Amphan – which impacted over a million people across nine districts in the country, resulting in losses amounting to approximately US$ 130 million. Effective mitigation strategies, supported by international grants and technology transfer, are crucial to combat environmental degradation and safeguard economic productivity.

A similar trend was seen in Bangladesh until 2009, with each election year marked by uncertainty, street agitation, strikes, and violence, disrupting economic activities and leading to a decline in GDP growth.

Through the political business cycle theory lens, economic activities fluctuate in response to external interventions by political actors aiming to boost the incumbent government's re-election prospects. For example, an IMF study in 1994 found that governments in developing countries, including Bangladesh, adopt expansionary expenditure policies before elections. A similar trend was seen in Bangladesh until 2009, with each election year marked by uncertainty, street agitation, strikes, and violence, disrupting economic activities and leading to a decline in GDP growth. However, a departure from this trend was noticed in 2014 and 2018, when GDP growth increased during the election years–due to elections being held in the middle of fiscal years, reducing uncertainty about power transfer. Finally, if the newly elected government addresses the ongoing challenges—successfully—the economy may rebound in the latter half of the fiscal year, leading to another period of growth in the next election year.

Soumya Bhowmick is an Associate Fellow at the Centre for New Economic Diplomacy Observer Research Foundation.

The views expressed above belong to the author(s). ORF research and analyses now available on Telegram! Click here to access our curated content — blogs, longforms and interviews.

Soumya Bhowmick is a Fellow and Lead, World Economies and Sustainability at the Centre for New Economic Diplomacy (CNED) at Observer Research Foundation (ORF). He ...

Read More +