-

CENTRES

Progammes & Centres

Location

India’s decarbonisation plans rest on its ability to generate green energy. Until then, the energy transition path till 2070 will remain at best, a rule of thumb and at worst, ad hoc.

Differential time horizons for net zero imply that there is no universal price for mitigating carbon emissions. Decarbonisation plans are proliferating globally, including in India. First came the plan to electrify vehicles, even before electricity supply standards had reached international levels of 0.999 reliability. Next, the near-term goal of having 50 percent of electrical energy supply from non-fossil fuel (NFF) technologies (hydro, nuclear, solar, wind, and biomass) by 2030. For this happy outcome, 65 percent of the installed electricity generation capacity must be green by that year (CEA 2023).

The two targets are linked. Electric Vehicles (EV) decarbonise and reduce air pollution only if fed with green energy. The other co-benefit of green EVs is reduced imports of petroleum fuel—an atmanirbahar metric. Along with greater security and stability of energy supply, it also alleviates the pressure on the INR in forex markets. This is an important consideration till the INR gets internationalised on the back of surging exports. We are not there yet.

Electric Vehicles (EV) decarbonise and reduce air pollution only if fed with green energy.

Both the energy share and capacity share of NFF remain aspirational targets with less than seven years remaining for 2030. An additional renewable energy capacity of 322 GW (46 GW per year) is needed by 2030. Of this, 88 percent (283GW) is planned in solar PV and wind with shares of 226 GW and 57 GW, respectively. Recent trends in capacity addition are not encouraging.

The good news is that two-thirds of the electricity capacity added of 85 GW from 2017 to 2022 was in NFF with just one-third in fossil fuel. (National Electricity Plan May 2023). Capacity added in solar was 42 GW and 8 GW in wind power, a total of 50 GW or an average of 10 GW per year. In fiscal 2022-23, a new NFF capacity of 15 GW was commissioned. Whilst this is a ramp-up from earlier years, it still falls short of the required additional capacity of 40.4 GW per year in solar and wind to reach the target of 283 GW capacity by 2030.

The price of delivered solar was artificially increased from 2020 by (increasing the customs duty) on imported solar PV cells and modules. Unlike fossil fuel-based generation, the capital cost of equipment accounts for the dominant share of costs in NFF generation. A high, selective import tax on NFF capital goods serves to level the field, perversely, in favour of carbon-intensive fossil fuel generation. Add to this the need for higher debt financing at the high-interest rates prevailing presently. The Reserve Bank of India (RBI) increased the benchmark policy rate (Repo Rate) from 4.00 percent in April 2022 to 6.50 percent in February 2022 – a 2.50-percentage point increase in less than one year, which translates to a 60-percentage increase in the cost of borrowing assuming that bank lending margins remain unchanged. Whilst necessary to manage inflation it has a chilling effect on capital-intensive technologies like renewable energy.

The good news is that two-thirds of the electricity capacity added of 85 GW from 2017 to 2022 was in NFF with just one-third in fossil fuel.

The Ministry of Power is taking steps to dilute the negative impact of the enhanced import duty on NFF capital goods by exempting NFF projects from Inter State transmission charges and by imposing carbon credit purchase obligations on designated entities on a similar pattern as the Renewable Purchase Obligation (RPO). Sadly, the RPO scheme suffers from lackluster implementation in government-owned entities like DISCOMs which are designated as obligated entities and required to buy either green power or the credits issued to green generators. Financially stressed DISCOMS tend to opt for the cheapest power available and prefer to use within-state fossil fuel generation owned by the state governments. State Electricity Regulatory Commissions (SERC’s) turn Nelson’s eye to DISCOM costs incurred in buying within state expensive power, whilst cheaper power might be available through bilateral exchanges or on the power exchange. The jury is out on whether the Carbon Credits Trading scheme will be more effective in assuring a market-based premium for clean power.

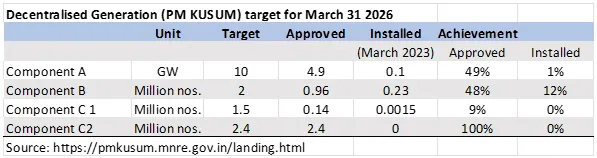

The bulk of NFF capacity is in large projects – many in solar parks. The decentralised solar scheme like PM KUSUM and Roof Top Solarization suffer from unresolved implementation hurdles. The table below illustrates the slow progress in the flagship Pradhan Mantri Kisan Utthan Evam Suraksha Mahabhiyan. This scheme was launched in April 2019. The initial progress was possibly hampered by the COVIDpandemic restrictions during 2020-2021.

The Ministry of Power is taking steps to dilute the negative impact of the enhanced import duty on NFF capital goods by exempting NFF projects from Inter State transmission charges and by imposing carbon credit purchase obligations on designated entities on a similar pattern as the Renewable Purchase Obligation (RPO).

The driving force behind this innovative scheme is the “value stack” of co-benefits which enhance the financial incentive for a farmer to switch from fossil fuel to solar-powered extraction of scarce groundwater resources for irrigating crops. If the pumps are already electrified, an incentive is built in via Feed in Tariff (FiT), determined by the concerned SERC, at which the DISCOM will buy surplus energy saved by minimizing water usage or reducing pumping hours.

Table 1 below lists the four options available under this scheme which was originally till 2022 but has been extended till 2026. (Options B and C)come with attractive subsidy packages of 30 percent of normative cost provided by the Union government (50 percent in special states), state government 30 percent and the residual as loan finance, thereby reducing the upfront cost for the implementor to a maximum of 10 percent of the project cost. It targets the addition of 38 GW of decentralised solar power, solely for agricultural users equal to 17 percent of the additional solar capacity of 226 GW needed by 2030.

Table 1

Component A facilitates the establishment of solar units up to 2 MW by farmer collectives or the DISCOM to solarise grid-connected pump sets. Approvals at 49 percent of the target are high but implementation has lagged.

Component B targets standalone solarisation of individual farmers’ pumps up to 7.5 HP presently outside the grid and using fossil fuel. The farmer’s incentive is to save on the cost of buying diesel at market prices since electric power supply to farmers is at marginal rates or free. Approvals are high at 48 percent and installations at 12 percent of the target are the best across all four components.

Component A facilitates the establishment of solar units up to 2 MW by farmer collectives or the DISCOM to solarise grid-connected pump sets.

Component C1 targets solarisation of the electric pump sets of individual farmers at twice the rated size of the existing motor to generate and sell surplus power to the grid. Both approvals and implementation are dissatisfactory. The farmer already has access to free electricity. The additional incentive of earning by selling power has to compare with the incentive to sell water via informal markets. Component C2 facilitates states to solarize agricultural feeders. To separate agricultural feeders, loans are available from specialised financial institutions like NABARD, PFC, REC, or assistance under the Revamped Distribution Sector Scheme (RDSS) of the Ministry of Power. The use of a renewable energy service company as a managing partner for 25 years is also possible. Approvals are 100 percent of the target, but installation remains pending.

Decentralised solar power struggles versus large-scale solar projects. By 2021-22 against a target of 40 GW of solar rooftop capacity, just 5.87 GW of grid connected capacity had been installed (MNRE Annual Report 2022-23). The biggest hurdle is that cost-conscious, energy-saving consumers enjoy free grid power (with generous differential capped limits) and have no cash incentive to switch to solar power. For better-off customers, roof rights have alternative uses including open space for roof gardens. Multiple or common roof rights are generally not acceptable to scheme vendors due to contractual complexities.

At the root of inefficiencies in retail electricity supply is the warped tariff structure which impedes competition in supply, constrains quality improvements and perpetuates polluting and inefficient, decentralised fossil fuel backup storage.

Meanwhile, standalone grid-scale solar projects now also enjoy the comfort of the Solar Energy Corporation of India acting as the purchaser of power from the generator. This avoids any business risk whilst dealing with illiquid DISCOMs. National Thermal Power Corporation also provides similar intermediation services.

At the root of inefficiencies in retail electricity supply is the warped tariff structure which impedes competition in supply, constrains quality improvements and perpetuates polluting and inefficient, decentralised fossil fuel backup storage. The upside is that with vehicle electrification proceeding apace a new class of customers (potentially 30 million strong by 2030) will enter the retail electricity supply market who will have the capacity to pay cost plus tariffs to charge their EVs.

A market-determined carbon price can help to define a cross-sector subsidy cap for reducing carbon emissions in supply and on the demand side. This amount can then be allocated transparently across technologies to evaluate the elasticities of demand and supply of carbon mitigation options. This will encourage rational allocations of state support to reduce emissions and enhance energy efficiency whilst retaining targeted, life-line energy supply and pricing of energy closest to the normative cost of time and season-differentiated supply. Until then, the energy transition path till 2070 will remain at best, a rule of thumb and at worst, ad hoc.

Sanjeev Ahluwalia is an Advisor at the Observer Research Foundation.

The views expressed above belong to the author(s). ORF research and analyses now available on Telegram! Click here to access our curated content — blogs, longforms and interviews.

Sanjeev S. Ahluwalia has core skills in institutional analysis, energy and economic regulation and public financial management backed by eight years of project management experience ...

Read More +