Utilising blockchain for cross-border payments: Implications for India

Cross-border payment is one part of the banking sector that has yet to benefit from recent progress in digitalisation. Most international transactions are still processed using a 600-year-old correspondent banking system devised by the Medici.[1]However, this system of manual entry of transactions is not a scalable solution for the burgeoning digital payments space. While this may seem like an issue for institutions, a huge segment of the population can benefit from the technological advancements in this sector.

Introduction

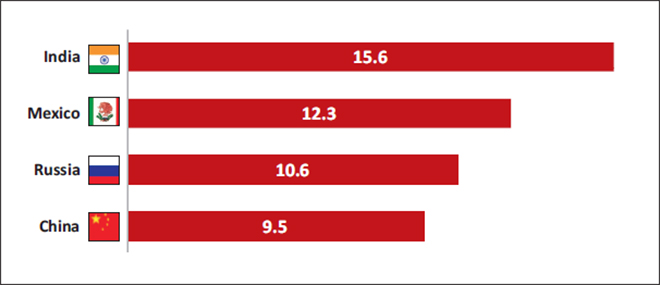

Remittances are the second-largest source of income for poor countries, contributing more than capital flows and development assistance. According to the Financing Facility for Remittances of the International Fund for Agriculture Development (IFAD), some 40 percent of global remittances—around US$200 billion—go to the rural areas, which are dominated by lower-income populations. Close to 200 million migrant workers support some 800 million family members globally. India alone received US$62.7 billion in international remittances in 2017, making it the largest recipient in the world.[2]To put this figure in perspective, the amount of Foreign Direct Investment (FDI) India received in 2016 was US$44.5 billion.[3]While FDI has fluctuated over the last couple of years due to financial instability around the world, remittances have been a steady source of foreign-exchange reserves for India.

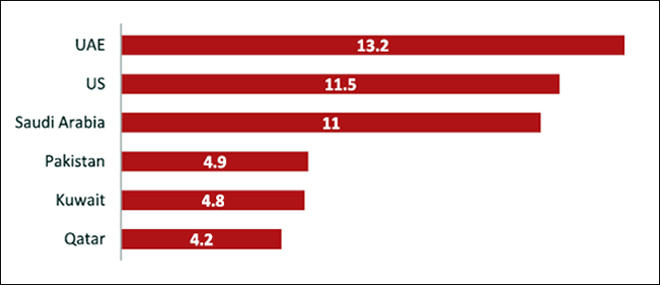

As given in Fig. 2, the top three remittance corridors (US, UAE and Saudi Arabia) contribute disproportionately more than the rest. What helps in understanding this skew is the fact that India has been among the countries with the highest number of emigrants, and was first in 2013. Therefore, most of these cross-border payments are a source of income for the Indian families who have at least one member working abroad.

Fig. 1

Source:United Nations.

Fig. 2

Source:Business Standard.

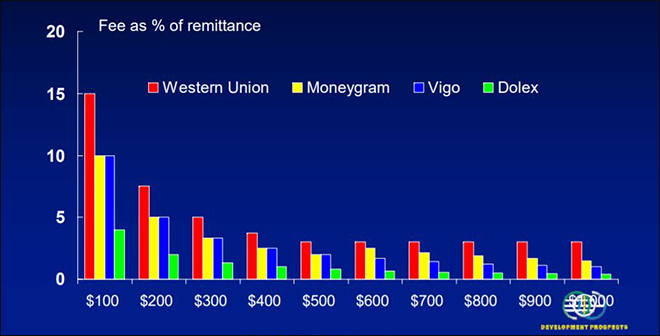

There are two key issues with the prevailing system of cross-border payments: the cost of transfers and their duration. On average, most transactions take two to three days to process. The lack of traceability does not help. On the cost front, post offices and money-transfer operators charge over six percent of the amount remitted; commercial banks charge 11 percent.[4]New and improved technologies, such as prepaid cards and mobile operators, result in lower fees for sending money home. However, these technologies are not yet widely available or used for many remittance corridors. The United Nations, as part of its Sustainable Developments Goals, has set the cost-per-transaction target of three percent. While the difference may look minuscule, it will magnify as the small transfers of US$200 and US$300 sent by migrants make up more than 50 percent of their family’s income.

Although the current system has multiple problems, it is deeply integrated and thus difficult to disrupt. As of 2015, SWIFT (the most widely used payment interface) linked more than 11,000 financial institutions in more than 200 countries and territories, who were exchanging an average of over 15 million messages per day. It has become as ubiquitous as VISA and MasterCard in the international payments space. It does not mean, however, that it is as efficient. The presence of a large number of middlemen (correspondent and respondent banks) makes SWIFT sluggish.[5]The majority of its clients have huge transactional volumes, making manual entry of instructions impractical. The need for automation of SWIFT message creation, procession and transmission is urgent.

Banking on Blockchain

This is where the Distributed Ledger System (DLT) holds promise. DLT, better known as blockchain, is a digital record of transactions maintained and validated by a network of computers via a cryptographic audit trail.[6]A distributed ledger means that no single authority, like a clearinghouse, needs to verify or execute transactions. Instead, the participants themselves have computers that serve as ‘nodes’ within the network, which add time-stamped blocks of transactions to form an immutable chain (thus, blockchain).

There are various factors that make up the transaction costs, which can be eliminated through the application of blockchains. The slow-moving nature of these remittances forces the banks to hedge against volatile movements and foreign-exchange risks. It also forces the banks to address liquidity needs due to massive amounts being transmitted. These costs also include compliance to regulations and requirements such as Basel III and capital ratios. The numerous intermediaries in the whole process adds to the costs through the various commissions.

Blockchain helps in addressing these issue through its decentralised ledger, consensus protocol, and use of digital assets and ‘smart contracts’.[7]

Distributed Digital Ledger:Traditionally, asset and transaction information was stored within physical books to independently reference previous actions internally and externally. As technologies advanced, physical books were translated into digital ledgers. Blockchain removes the need for a central entity to store and process these ledgers. Instead, the ledger is replicated among many different nodes in a peer-to-peer network, securing each transaction with a uniquely signed cryptographic private key. This eliminates the need for inter-party reconciliation in cross-border payments. Since all the transactions are permanently recorded, it leaves no room for manipulation while establishing an audit trail.

Consensus Mechanism:A method of authenticating and validating a transaction without the need to rely on a single authority. These transactions are verified and executed based on an agreed-upon arrangement, while invalid transactions are immediately discarded. It allows the connected organisations to work together as a group, which can survive even if some of the members fail. The ability to sustain individual failure is a big advantage and helps in increasing the integrity and efficiency of the system, while also leaving room for other validators such as various stakeholder companies, internet service providers and other such institutions. The validation of transactions—currently done through a manual entry system—is automated, thus allowing real-time tracking of transactions. The process allows for a risk-based approach to the transactions instead of screening every single one.

Digital Assets:The use of digital assets solves the issue of multiple currencies and improves the liquidity and capital compliance costs, while also allowing the possibility of micropayments. Instead of hedging against the various currencies, the banks only need to take care of the digital token, thus cutting the operational costs of maintaining multiple debit/credit accounts in varying currencies. The rapid nature of the transactions eliminates any kind of liquidity risk that banks might have to hedge against and enables almost-real-time settlement between banks.

Smart Contract:Smart Contracts are self-executing contracts, based on the fulfilment of the terms of agreement between multiple parties. The terms and conditions, written into lines of code, exist across the distributed ledger network. Thus, financial agreements can be executed automatically as long as the mutually agreed conditions and the regulatory requirements are met. It transforms compliance from post-transaction to immediate and on-demand. IBM, while developing their blockchain-based payment solution, gave the example of a farmer in Samoa who would soon be able to draw a contract with a buyer in Indonesia and use the blockchain to record everything from the farmer’s collateral to letters of credit to payment.

Blockchain’s Benefits to India

India, the biggest receiver in the cross-border remittance market, can benefit immensely by adopting the blockchain technology. One hindrance in the current system of payments is that there is an inverse relationship between the size of transfer and the fees charged due to “economies of scale.” Since blockchain does not discriminate between the transaction sizes, the low cost of transactions will allow a whole new demographic to participate in the cross-border payments space. Much of the population still relies on an informal or alternative remittance system (called“hawala”in Hindi) that allows both domestic and international transfer of funds due to its cheap and fast nature. The informal and illegal aspect of that system makes it difficult to estimate its exact size, but there are reports approximating it to be around US$100–200 billion[8](domestic and international). Formalising even a fraction of this amount will be of great benefit to banks and citizens alike; it will also be the ultimate test of this technology.

According to Ripple, the leading blockchain network in the banking sector, the global payments costs can go down by 42–60 percent through the implementation of its blockchain network.[10]India’s incoming remittance market stood at US$62.7 billion in 2016. Assuming the global average cost of 21 basis points on payments volume, blockchain can help Indian banks save around US$80 million annually. This will be a huge boost to the already ailing banking sector. The inbound new wave of transfers, which till now have been priced out of the market, will be an additional benefit.

Developments in the Blockchain Field

Ripple and Stellar are the major actors leveraging the blockchain in India’s banking sector—and the only ones addressing the cross-border payments—but with different approaches. Ripple has used the consortium of banks that use its technology to form a ‘global payments steering group’ to take advantage of the network effects. It includes some of the biggest banks around the world, including Bank of America, Standard Chartered, Mitsubishi, Barclays, and Santander. Axis Bank and Yes Bank are the only Indian banks that are a part of it. Stellar, on the other hand, is an open-source platform that can be adopted by any organisation. Recently, IBM decided to partner with Stellar to develop a solution addressing the issue.

In this battle of cross-border payments, the incumbent SWIFT is still the Goliath. It is not easy to topple a recognised organisation such as SWIFT, which has a significant advantage with its 11,000 partners. Recently, however, even SWIFT has decided to test the blockchain technology. As part of its global payments innovation (GPI) initiative to modernise the cross-border payments system, it has tested some proof-of-concepts to supplement its current framework.[11]

While these are the established blockchain networks, Indian banks have taken an unusual yet lauded route of forming its own consortium ‘bankchain’ on a separate blockchain platform. Announced in February 2017 by SBI, the network has grown to 24 members, including international banks, with the aim of exploring, building and implementing blockchain solutions in the banking sector. It currently has 10 active projects underway, such as shared KYC, syndication of loans, virtual currencies and cross-border payments.[12]While it is an exciting initiative with bright prospects, it will be interesting to see if they embrace or fight the international counterparts who benefit from a broader global network and have already started gaining traction in India.

Difficulties in Implementation

As with any new technology, there are some difficulties to adopting the blockchain. Even with all its benefits, the technology brings with it the notorious reputation of cryptocurrencies (the common name for digital currencies). Since its inception, Bitcoin (the biggest cryptocurrency) has been associated with illegal activities such as drug trafficking and extortion, due to its ownership anonymity. Although, recently, exchanges have been forced to implement KYC (Know Your Customer) and AML (Anti-Money Laundering) norms, the anonymity aspect remains.

Other cryptocurrencies, too, have faced their fair share of controversy. Unlike Bitcoin, whose creator is still unidentified, XRP (Created by Ripple) is backed by an enterprise that makes it easier to be held accountable for its actions. In May 2015, the Financial Crimes Enforcement Network charged Ripple with a US$700,000 fine due to its non-compliance with the KYC and AML laws.[13]Going forward, while it may be easier for Ripple to monitor its transactions due to its B2B nature, authorities will still be sceptical of other cryptocurrencies that make it difficult to track their holders.

Apprehension regarding virtual currencies persists globally. The European Central Bank in its 2015 paper[14]on virtual currencies said, “The overall situation as regards to payment system stability might change if: i) large financial sector players interconnected to the global banking system started offering services related to VCS (Virtual Currencies); and/or, ii) a significant increase in users and the volume of transactions took place.” Both these things have already occurred. While there are reports of Russia coming out with stricter regulations regarding these virtual currencies, China has banned ICOs (Initial Coin Offering) completely,[15]which is a new form of crowd-funding through virtual currencies.

Along with government regulations, there are laws governing the Indian banking space. The Foreign Exchange Management Act, 1999 governs cross-border transactions and related activities.[16]This supports, among others, certain banking and other institutions to be licensed as authorised dealers in foreign exchange. An entity proposing to deal in foreign exchange must obtain this FEMA licence, in addition to the regular banking licence from RBI. If the entity is listed, SEBI regulations also apply. The complex governance structure of these disparate systems further increases the challenge.

Adding to all these complications is the issue of scalability and stability. While Bitcoin is currently the largest application of blockchain, it is nowhere near the size of the global remittance market. Vast amounts of metadata and volatility associated with these transactions make the implementation process more complex.

Conclusion

While governments are trying their best to safeguard the interests of their citizens, the blockchain technology powering these currencies must be preserved. Some governments have made efforts in this area. In July 2017, Bank of England tested several fintech proof of concepts, Ripple being one of them.[17]Various central banks around the world have started testing their own digital currencies, which is to be accepted as a legal tender within their respective countries.[18]While these centralised digital currencies are a redundant solution that do not leverage the blockchain technology, they are a step towards digitalisation of the prevalent fiat currency system.

RBI has been keeping a trailing eye on the world of cryptocurrencies and blockchain. In addition to issuing minor warnings regarding virtual currencies, in its 2015 Financial Stability Report,[19]RBI acknowledged the benefits of blockchain and said, “Regulators and authorities need to keep pace with developments as many of the world’s largest banks are said to be supporting a joint effort for setting up of ‘private blockchain and building an industry-wide platform for standardising the use of the technology.” In January 2017, IDRBT—the research arm of RBI—came out with a white paper, “Applications of Blockchain Technology,”[20]which laid out favourable blockchain concepts but, in the end, cautioned against the hype surrounding the cryptocurrencies. Recently, the Director of IDRBT said in a press conference, “We will be launching this [blockchain] platform very soon.”[21]This open and innovative attitude can go a long way in benefitting the citizens.

It is rare for the lower strata of the society to become the primary beneficiaries of a cutting-edge technology. Therefore, it is imperative that the Central Bank comes out with a concrete policy framework for this burgeoning sector. In its move towards a digital-first economy, India must learn to harness blockchain technology.

Endnotes

[1]House of Medici and Armand Grunzweig, Correspondance de la filiale de Bruges des Medici(Bruxelles: M. Lamertin, 1931).

[2]“With $62.7 Billion, India Top Remittance-Receiving Country In 2016: UN Report,”Firstpost, 2017.

[3]Asit Mishra, “India Climbs To 9Th Position on FDI Inflow List, US Retains Top Spot,” 2017.

[4]World Bank,Global Economic Prospects 2006: Economic Implications of Remittances and Migration(Washington, DC: The World Bank, 2005).

[5]Yoon S. Park,The Inefficiencies of Cross-Border Payments: How Current Forces Are Shaping the Future, George Washington University, 2017.

[6]Consensus: Immutable Agreement for The Internet of Value(ebook), KPMG, 2016.

The views expressed above belong to the author(s). ORF research and analyses now available on Telegram! Click here to access our curated content — blogs, longforms and interviews.

PDF Download

PDF Download