This brief outlines a framework for India if it is to play a more proactive role in integrating and reimagining its immediate neighbourhood, in particular with reference to the economic relations with its BIMSTEC partners. The analysis is done in the context of important economic and strategic developments in the Asia-Pacific region in the recent years. It describes how India can navigate between competing economic and geo-strategic imperatives by pulling the region closer to it economically through the promotion and development of local value chains.

Attribution:

Suparna Karmakar, “Reimagining India’s Engagement with BIMSTEC,” ORF Issue Brief No. 404, September 2020, Observer Research Foundation.

Introduction

The winds of change that started blowing in the aftermath of the 2008 financial crisis, and gathered pace since mid-2018, have turned into a gale in 2020. How epic its legacy would be will depend on the actions and judgements that the world’s biggest economic players will take. As China turns revanchist[1] and Asia’s regional powers ring in nationalism (dubbed “Corona nationalism” by some experts),[2] seemingly minor trade scuffles in the Asia-Pacific region can turn into intransigent global conflagrations that might not be easily contained; simply returning to the comfortable assumptions of the earlier status quo may no longer be feasible. Moreover, it is the Asia-Pacific countries that will feel the whiplash the most; indeed, in more limited forms, they are already facing a less permissive environment to pursue their economic and security goals.

One of the key changes expected is in the sphere of economic and trade governance; the COVID-19 crisis has forced a historic collapse of global trade in the second quarter of 2020[3] and fractured established supply chains,[4], thereby leading companies to reassess and expedite planned diversifications[5] in their just-in-time supply chains on which the global economy had come to depend. The geo-political uncertainties and trade policy upheavals in the recent past had revitalised calls for reorganisation of the global production and supply chains, from textiles to technology, especially to reduce the Sino-centrality of global value chains (GVC). India hopes to benefit from the supply chain reorganisation dynamic in the Asia-Pacific, notwithstanding its withdrawal from the Regional Comprehensive Economic Partnership (RCEP) and its repudiation of Beijing’s Belt and Road Initiative (BRI).[6] As building new levels of resilience in supply chains (beyond the ultra-efficient, single-source and just-in-time capabilities of yore) becomes the war cry in the large economies in the post-pandemic world, MNCs that have been pushed to reduce their supply chain dependency on China[7] may open up opportunities for India to be an alternative driver of the next phase of global digital and economic growth. Companies like Apple and Samsung, for instance, and their assembly partners and subcontractors, have already made their moves, targeting the Indian domestic market to begin with.[8]

This brief examines the proactive role that India can adopt in integrating and reimagining the neighbourhood, pushing cooperation rather than competition, with reference to the economic and trade relations with its partners in the Bay of Bengal Initiative for Multi-Sectoral Technical and Economic Cooperation (BIMSTEC).[9] In recent years, with the re-intertwining of strategic and economic interests in the Bay of Bengal as part of a larger maritime strategic space, christened the Indo-Pacific, BIMSTEC as a promising sub-regional grouping is gaining traction. This creates an imperative for India to revitalise its BIMSTEC engagement strategy. Forced to compete in the region with a much richer China, a significant challenge by itself, India should regard the upgrading of its soft (including economic) as well as hard infrastructure in the region as a strategic measure. Clearly, mere geographical proximity has yet to translate to closer economic interaction. Fortunately, the recent initiatives by India and the Asian Development Bank and World Bank investments in stitching together the connectivity infrastructure in the region, and the rising anti-China sentiments in major economies, offers an opening for India to reclaim and re-establish its traditional commercial networks in the region.

India’s Geo-economic Stakes

Emerging from a century-long colonial subjugation around the middle of the 20thcentury, countries in the Indo-Pacific region remain wary of the global powers overwhelming their national priorities and sovereignty. This has created a special problem for India particularly in its natural hegemonic zone—the South Asian region. Here, India’s outreach to the region via the South Asian Association for Regional Cooperation (SAARC) has floundered with the deteriorating India-Pakistan relationship, leaving that organisation essentially defunct.[10] New Delhi has tried to circumvent this obstacle by using other multilateral regional and sub-regional organisations like the BIMSTEC, with somewhat better outcomes.[11]However, changing circumstances and geopolitics of the 21st century—especially with the lengthening Chinese shadow framing India’s relations with every other state in South Asia and in the Indian Ocean Region (IOR)—warrant a new and more granular approach in India’s economic relations with its neighbours.

As the World Trade Organisation (WTO) weakens and its multilateral trade rules become more irrelevant, there is increased interest (at least in the near term) in regional trade agreements and fragmented but locally-relevant economic associations. India will therefore have to simultaneously adopt a narrower focus and a broader context as it reimagines BIMSTEC trade and regional integration.[12] To be sure, the favourable conditions of the 2000s had enlivened the neighbourhood, and as India also embraced the idea of South Asian regionalism and connectivity, it garnered enormous goodwill among both the people and leadership in SAARC member countries. Post-2008, however, the global order where the United States (US) began to co-exist (somewhat uneasily) with a rising China started changing; this has now given way to a post-pandemic world order which marks a fairly public, intensified degree of competition and conflict between the US and China. For India, the more immediate context also changed in the last decade. China is no longer a possible partner; it is now a clear adversary in a region that has become ever more fragile. Political elites in neighbourhood capitals, driven by nationalistic fervour and China’s outreach with generous investments, also seem open to undermine India in these unpredictable times.[13][14]

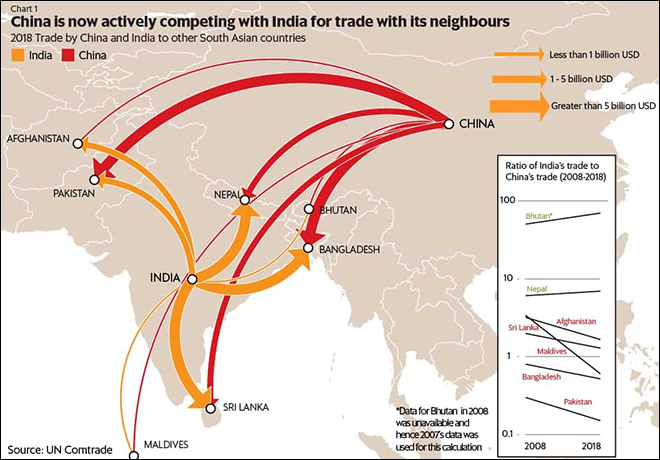

All of the above implies that India — which benefitted from a period of relative international security and a benign economic environment in the earlier decade — must gear up for a more unstable environment and more hostility in its neighbourhood. In particular, over the past decade and half, China has replaced India as the biggest trade and investment partner of several South Asian countries (See Figure 1). China has also strengthened its military-defence ties with most SAARC members. The most visible (and seemingly benign) instrument of Chinese influence in the region is its investment, loans and grants, largely in hard (dual-use) infrastructure projects – power, roads, railways, bridges, ports and airports – under the aegis of the BRI; nearly 80 percent of Chinese investments in South Asia have been in the energy and transport sectors.[15] China has committed more than US$150 billion in the economies of Afghanistan, Bangladesh, the Maldives, Pakistan, Nepal and Sri Lanka, with penetration highest in countries flanking India;[16] it is now the largest overseas investor in the Maldives, Pakistan, and Sri Lanka. India therefore needs to strategically re-examine its trade, technology and investment ties in the neighbourhood at large. In particular, since BIMSTEC suffers from a lack of human and financial resources, analysts are of the view that India needs to allocate more resources and take new initiatives to induce a pro-India momentum in BIMSTEC,[17] thus pushing back on China’s efforts to encircle New Delhi.

Graphic Source: Kwatra and Devulapalli, 2020

Reclaiming the Geo-economic Space in Indo-Pacific through BIMSTEC value chains

While globalisation, since 2018, has been on the ropes from repeated onslaughts emanating from the Sino-American conflicts, it is the ongoing pandemic that has shocked the global economic system most comprehensively. Barriers to trade and immigration, already on the rise due to the ongoing trade and technology war between China and the US, have been joined by border closures and restrictions on food and medical exports even as countries worldwide pushed for greater protection and import-safeguard measures. Consequently, trade volumes are in a free fall, with limited hope of returning to pre-Covid status quo in the near future. The trade deceleration is aggravated by the fact that at an aggregate level, global supply chains account for the majority (about 70 percent) of global trade in goods, and the pandemic-induced shutdown of the world’s factories has had a deleterious impact. This trade pattern is, however, unlikely to change substantially in the near future, even if the proposed GVC restructuring initiatives pick up pace. American (and European) MNCs are not convinced that severing/ any major decoupling from the painstakingly developed China-centric supply chains is yet warranted, or even economically viable.[18]

Notwithstanding the many difficulties, however, India’s ability to foment new regional supply chains by positioning itself as a key node in existing supply chain systems undergoing post-pandemic restructuring will determine its goals of: (i) reversing the secular declining trend of its global exports share; and (ii) capturing a larger pie of the external (in trade and investment) market being vacated by China/the MNCs relocating to improve risk management of their production processes. In a world of GVCs, trade policy cannot solely focus on impediments to trade with direct trade partners. The complete value chain and bottlenecks upstream and downstream among third countries must also be considered in order to boost exports and improve economic performance.[19] This makes closer cooperation with value chain partners and pursuing open, predictable policies and regulatory regimes as important for India as industrial policy and export competitiveness initiatives.

The good news is that this awareness has filtered across the political and governance consciousness, and India has taken tentative steps with the new Atmanirbhar Bharat initiative[a]to reverse earlier policy rigidities in favour of pro-business and more open industrial policies. Insofar as closer engagement with economic partners in the region is concerned, India is proactively engaging with the IOR through Covid assistance and also using the move away from the RCEP to leverage its own mini-lateralist organisations such as the BIMSTEC to re-engage with the Southeast Asian nations. Since the post-pandemic world will most likely be a poorer one[20] rife with disorder and uneasy globalisation—where trade initiatives rapidly regress to an era of power politics for countries to use it as a weapon to economically coerce other countries—narrow regionalism and fragmentation of global production and supply chains appear highly plausible. In such a world, vibrant local value chains offering reasonable resilience to shocks would gain currency over the overextended global ones.

This brief’s proposition is for India to work smartly to get the most from ongoing regional connectivity initiatives and infrastructure projects, and develop local and regional value chains (LVCs) jointly with its BIMSTEC neighbours (i.e. go glocal) to quickly bring back economic vibrancy in the post-Covid era. The current consensus is that it will take at least until 2022 for economies to regain their pre-pandemic state. If India is to benefit from the potential post-Covid reorganisation of the production and (Sino-centric) supply chains around the world, it will have to match both the efficiency and pandemic-crisis-induced lower labour costs of foreign value chains, and also the openness and deep trade integration that these GVCs currently offer and benefit from. This brief acknowledges the popular view that India’s tryst with free trade agreements (FTAs) has not been overtly beneficial. Nonetheless, should India start looking at regional integration from a more bottom-up fashion and with a narrower scope, negotiating future FTAs will have more buy-in and support from domestic stakeholders. This is because a pickup in value chain activity would amplify the positive trade feedback loops and beneficiary voices.

Promoting BIMSTEC local value chains over Global Value Chains

Building on the premise that India and its neighbourhood needs more high-tech industrialisation, climate-friendly and efficient manufacturing, developed employment-generating supply side capacities, and greater participation in international supply chains, policy analysts have been recommending that to revitalise its domestic economy and external economic relations, India should help in pushing for an expeditious implementation of the BIMSTEC Comprehensive Free Trade Agreement (BIMSTEC FTA),[21] the negotiations for which have been ongoing since 2004. In fact, the original intention of the member states of this inter-regional body was inspired by the idea of interlinking the SAARC and ASEAN into a contiguous free trade area zone via BIMSTEC.[22] This would open the door for investment, identifying priority projects on trade, transportation, tourism, energy, health and agriculture through collective action, enhancing not only production and localised investment, but also liberalising trade in both goods and services and facilitating economic integration of the region. Notwithstanding this lofty rationale, and the understanding that while FTAs are no panacea they do represent a crucial first step towards spurring growth and development, an actual conclusion of the FTA negotiations have eluded members for long. Prior to disruptions from the higher-profile RCEP parleys in late 2019 and then the pandemic, the Members had set interim 2019 targets including finalising the trade in goods agreement[23] of the BIMSTEC FTA as well as the supporting agreements on customs cooperation, and launching the BIMSTEC connectivity master plan, involving the BIMSTEC Coastal Shipping Agreement[24] and BIMSTEC Motor Vehicle Agreement (and its subsequent linking with the ASEAN Connectivity Plan 2025).

However, the need for realistic leveraging of the current disruptions in globalisation and assessment of the past low-intensity progress in BIMSTEC FTA negotiations calls for a reassessment of targets and strategies; in particular, it would serve the organisation well to be less ambitious vis-à-vis the depth of BIMSTEC market integration. Sri Lankan analyst (late) Saman Kelegama was prescient in suggesting that both the key functional aspects of BIMSTEC, viz. market-driven integration and government-driven integration, should be utilised selectively to seek quick gains for the region.[25] In a similar vein, this brief argues that conclusion of the comprehensive BIMSTEC FTA and deep-market integration could be facilitated by Indian government-driven investments in creating hyper-local industrial value chains aimed at knitting specific micro-regions together economically.

From 2014 to 2018, India invested around US$1,461 million in regional connectivity projects; in particular, the country is actively upgrading infrastructure in its North Eastern Region (NER) to complement its Act East policy. Therefore, the seeding government-driven industrial clusters towards fostering cross-border LVCs can leverage the ongoing connectivity (viz. the already functional maritime corridor agreements between India and Bangladesh[26] and the ADB-SASEC funded trans-Asian highways, railway and aviation infrastructure) and trade facilitation programmes. Liberal transit, business-friendly customs, transport corridors, and other initiatives help reduce barriers and catalyse production and trade in the region. This in turn induces more private sector activity and deeper market-driven integration. Indian leadership in creating viable and vibrant cross-border manufacturing ecosystems (or cross-border industry hubs by scaling up the existing infrastructure of border-haats, to begin with) for locally relevant sustainable production systems in the neighbourhood calls for various elements. These include: (i) identifying the locally viable industrial (manufacturing or services) activities and zones; and (ii) marshalling BIMSTEC member governments (at both the district or region, and the national levels) into participating along with their private sector stakeholders, and help counter interference from opportunistic non-state and extra-regional actors.

This brief recommends that India locate its NER supply chain hubs in regions close to BIMSTEC border areas. This can lead to an amalgamation of the cross-border economic zones to create larger multinational SEZs as trust builds over time. In this venture, India can also hope to synergise initiatives from the proposed trilateral Supply Chain Resilience Initiative (SCRI) between Australia, Japan and India aimed at reducing dependency on China.[27] While necessitated by Beijing’s aggressive political and military behaviour in the South China Sea, the trilateral envisions turning the Indo-Pacific into an “economic powerhouse” and building complementary supply chain hubs among the partner countries.

To be sure, it could take more than a decade to get the LVCs initiative to bear fruit; patience and long-term planning will be necessary. China in the late 1980s and early ’90s was similarly underdeveloped in global commerce; over the next 20 years, it developed a supply chain infrastructure that today is even more efficient than that of the US. India must delineate an ambitious industrial policy and create a green and (social and environmentally) sustainable business ecosystem[28] that requires the country to (i) leverage its demonstrated IT and digital-telecom advantages; (ii) push for green cargo transport and electric vehicles that complement environmental regulations of India and the needs of the climate-sensitive and geologically fragile NER; and (iii) support the venture with human and financial investments in R&D and energy technology, among others.

Building a Greenfield green-transport and electric battery value chain in the region, for example, would meet these requirements. India does not yet have a commercial Lithium-ion battery-cell manufacturing facility,[29] but the Union government has made ambitious plans to indigenise cell manufacturing and is scouting for plant locations. Locating a LVC supply chain/ industry SEZ, for example, in the multinational Banglabandha-Phulbari-Kakarbhitta stretch or along the developing Dalu-Tura-Goalpara-Gelephu multimodal trade and transport corridors (and potentially also the Imphal-Moreh-Tamu segment of the Asian Highway 1 or AH1[30]) can help energise the regional BIMSTEC economies and improve intra-regional trade. Finally, an LVC focus—by design more sustainable, circular and regenerative—will counter the rising environmental costs of GVCs associated with long-distance trade in intermediate goods and assembly parts.

Indeed, an anomaly of India as a regional economic powerhouse has been its limited trade connection within the region, the poorest performance among all regional trade groupings. For example, India’s trade with its South Asian neighbours has ranged between only 1.7 and 3.8 percent of its global trade. Data from the World Development Report 2020 indicate that while GVC integration has closely knitted regional over global partners, South Asia’s GVCs expanded almost entirely outside the region, including of the region’s biggest economy, India. The mismatch in trade complementarity clearly impedes economic integration in this region. To balance it out, India needs to transform itself into a manufacturing hub, creating an elaborate industrial hub-and-spoke structure within the region. The challenge for Indian policymakers and strategists is to move away from the rigid Make in India and Exported from India measures to “manufactured in and/or serviced from a cross-border multi-national local economic zone” mindset.

This holds true for both manufactured goods and services. Even as services are an invisible but vital part of GVCs in recent years, there remains room for integration, with the back office of many US manufacturers now in India, expanding ICT and business service sectors. Service production is itself being fragmented across countries, such as when preliminary architectural designs, tax returns, and magnetic resonance imaging (MRI) readings are performed in one country and finalised and delivered to customers in another. These are also areas where India can take the lead and weave the region into a more closely knit entity. India can introduce a mix of high- and low-technology service activities in the region, which are scalable in the context of its topography while at the same time has the potential to leverage and synergise Indian service sector proficiency with the ASEAN supply chains.

India would do well to take a nuanced view and focus on regional integration over national exports. Cooperation over competition should be the new norm of engaging with neighbours that are openly hedging their bets. Investing strategically to integrate the economic activities of neighbours through BIMSTEC-focused value chains can help create economic interdependence, which can temper the bilateral tensions that have been fomented in the past decade by the geopolitical developments in the South and South-east Asian regions. Bilateral tensions and national priority conflicts tend to complicate the dynamics within a regional or sub-regional grouping, weakening its collective resolve to strengthen itself. Economic interdependence, on the other hand, has for long proved to be an important means for fulfilling strategic objectives and relieving intra-national stress, especially in neighbourhoods where institutions and governance regimes are underdeveloped and elite interests often determine national interest. Being instrumental in promoting and developing BIMSTEC value chains could help India take the lead in reversing this trend of continual fluidity in bilateral relations and geopolitical unrest, fostering stability somewhat along the lines of the European Union, and also counter the non-benign interference by extra-regional powers. Activating production linkages among neighbouring member countries, and generating new value chains can help the region become more stable and globally attractive, economically as well as geopolitically.

Conclusion

With rising antipathy against China on national security and human rights grounds, and the pandemic-instigated call for reducing supply chain dependence on a single country or region, India has an opportunity to engage with BIMSTEC members through fomenting regional/LVCs, as supply chain integration boosts trade complementarities as well as mutually beneficial economic interlinkages. Given that many of these regional economies also have similarities in their export baskets and competencies, enhancing trade and strengthening economic cooperation will be possible if only multinational joint production facilities are established along the border zones.

To be a regional manufacturing powerhouse would require companies across the border to vertically integrate within the defined geography in the micro-region. Following the experience of the European Union, closely stitching the economies together would both reduce mutual mistrust and strife, and help weaken the influence of mischief-making extra-regional entities and non-state agents. While it is true that parts of critical physical connectivity infrastructure (viz. the AH1 segment near the India-Myanmar border) that is crucial for free trade between the countries is yet to be completed, it is still possible to make a reasonable beginning with what already exists.

This brief’s proposal of LVCs calls for larger regional players to invest in others’ economies, in their businesses, in training foreign people and creating jobs, in innovation and entrepreneurship. They will need to do all of this while still being open to new opportunities to engage in international business and trade. This will also help open up BIMSTEC members into trading with each other without becoming dependent on each other. As trade and geopolitics have now again intertwined, after the colonial centuries, the imperative is for new and bolder imagination on market integration through trade. India today has both the vision and the political clout to lead the change. It can offer leadership and utilise the present geopolitical momentum to remodel BIMSTEC as a sub-regional grouping to be reckoned with. In short, reclaiming its place at the centre of regional geo-economics requires India to pursue a visionary foreign policy and magnanimous domestic politics. A strategy of self-interested benevolence vis-à-vis the neighbourhood might end up being more profitable in the longer term compared to narrow mercantilist policies proffering quick returns.

About the Author

Suparna Karmakar is a consultant economist on issues of trade policy and economic regulations.

Endnotes

[a] Aatmanirbhar Bharat Abhiyaan or ‘Self-Reliant India Mission’ is the Government of India’s new initiative to pursue policies that promote efficiency, equity and resilience, but not protectionism. As part of the Atmanirbhar Bharat package, numerous government decisions have been adopted such as changing the definition of MSMEs, boosting scope for private participation in identified strategic industrial sectors, increasing FDI in the defence sector, etc. Under its aegis, the Centre has announced production linked incentive schemes as well as localisation requirements in the areas of medical devices, pharmaceuticals and electronics, to be extended to as many as 20 major sectors; GoI will also launch the Land Bank Portal soon.

[5] In early June 2020, at the India – Australia Leaders’ Virtual Summit, the two trade partners agreed to work together on “mechanisms to strengthen and diversify supply chains for critical health, technology and other goods and services”.

[6] Unable to persuade India to sign on to its BRI, China had entered the Indian market through venture capital investments in technology start-ups and penetrated the online ecosystem with its cheaper smartphones and their popular applications (apps), according to the Gateway House analysis (Amit Bhandari et al., Chinese investments in India, Gateway House Report No. 3, February 2020). However, this is changing since the April 2020 FDI norm revision and heightened scrutiny of Chinese imports since June 2020; Chinese investors are likely to put their planned India investments on hold, at least in the short run.

[7] Companies could shift upto a quarter of their global product sourcing to new countries in the next five years, according to a new August 2020 Report by the McKinsey Global Institute (Susan Lund et al., Risk, resilience, and rebalancing in global value chains, McKinsey Global Institute Report, August 2020). Also, averaging across industries, companies can now expect supply chain disruptions lasting a month or longer to occur every 3.7 years, the study estimates. Many US companies in particular has concluded that their supply chains have become too long and complex, and locating close to consumers now make good business sense. The AT Kearney State of Logistics Report 2020 had similarly concluded in June that even as technology had already diminished the importance of labour arbitrage, growing consumer demand for rapid delivery was already creating pressure for shorter “multi-local” supply chains.

[9] BIMSTEC is a sub-regional organisation comprising seven Member States around the Bay of Bengal region. The BIMSTEC region brings together 1.67 billion people and a combined GDP of around US$2.88 trillion. The Permanent Secretariat of BIMSTEC is operational since September 2014 in Dhaka. The organisation came into being on 6 June 1997 through the ‘Bangkok Declaration’. It constitutes a unique link between South and South-East Asia with five Members from South Asia (Bangladesh, Bhutan, India, Nepal and Sri Lanka) and two from South-East Asia (Myanmar and Thailand). BIMSTEC not only connects South and Southeast Asia, but also the ecologies of the Great Himalayas and the Bay of Bengal. Importantly, with the exception of India and Bhutan, the other BIMSTEC members are participating in China’s BRI.

[10] The political rivalry between India and Pakistan over the control of the Kashmir Valley, lately also buffered by malign interference from China, has constrained SAARC from realising its potential as a vibrant regional grouping. However, after being put in the freezer since 2018, a fresh attempt via video conferencing was made last April amidst the global health emergency to revive the regional groups’ joint crisis response forum. Fizza Batool, “Why Dismissing Saarc’s Revival Is Premature,” South Asian Voices, Stimson Center, April 15, 2020.

[11] S.D. Muni and Rahul Mishra, India’s Eastward Engagement: From Antiquity to Act East Policy, (New Delhi: Sage India), January 2019.

[12] Remarks by C. Raja Mohan, Director, Institute of South Asian Studies, National University of Singapore, at the ORF Kolkata Colloquium, 2019.

[20] IMF estimates that growth in Asia will not only be harmed substantially, but importantly, the output losses due to Covid-19 will be permanent. Experts at the Asia and Pacific Department of the IMF has pegged the regional growth rate by the end of 2022 to be 5 percent lower than what was predicted before the crisis; excluding China, the output loss for other Asian economies would be even larger. ADB expects India’s FY21 GDP growth to contract by 9 percent, while other forecasters are even more pessimistic.

[21] BIMSTEC officials have estimated that intra-BIMSTEC trade can grow up to US$240 billion from the current estimated US$40 billion. The 21st Meeting of the BIMSTEC TNC in November 2018 had made significant progress in finalising the draft texts of three important agreements relating to BIMSTEC FTA, namely (i)Agreement on Trade in Goods, (ii)Agreement on Cooperation and Mutual Assistance in Customs Matters, and (iii)Agreement on Dispute Settlement Procedures and Mechanisms. The Meeting also made progress on developing texts of three other agreements relating to Investment, Services and Trade Facilitation.

[24] Since coastal shipping is cost effective compared to land and rail transport, it is believed that stronger maritime connectivity will spur global and regional value chains, especially among the Bay littorals.

[25] “As for market integration, BIMSTEC should not have high hopes on an FTA coming into operation. Indications are that it will drag on for a long time”: Saman Kelegama, “Regional Economic Integration in the Bay of Bengal,” Talking Economics, Institute of Policy Studies of Sri Lanka (IPS), June 6, 2017.

[26] In the last few months, and notwithstanding the pandemic, both India and Bangladesh have updated their inland water protocol, including Tripura State into the plans, started a bilateral coastal-riverine cargo ferry service and India has handed over much-needed rail locomotives to Bangladesh. These initiatives will allow export of Bhutanese and NE India cargo to Bangladesh and easy access for traders to the hinterland of that country. In addition, the two sides hope to shortly finalise the Akhora-Agartala rail link, and the long-pending 1320 MW Khulna thermal plant, as a sign of India’s commitment to boost connectivity with its neighbour. Details on recent India–Bangladesh connectivity initiatives in: Suparna Karmakar, “Renewing NE India–Bangladesh Connectivity: Analysis of transport corridors,” FREIT WP1626, 2019.

[28] Usually encompassing well established supply chain relationships between factories, suppliers and customers in the complete input-output production chain, including the necessary telecom, finance, transport and the range of essential business services.

[29] Lithium-ion battery manufacturing consists of three parts. First is cell to battery-pack manufacturing involving a value-add of 30-40 percent. The second is cell manufacturing with a value-add of 25-30 percent. The third involves battery-chemicals with a value-add of 35-40 percent of the total cost of battery pack. While cell to pack manufacturing plants have started functioning, the others need to be encouraged. NITI Aayog researchers have proposed that India should provide MSIPS incentives and tax incentives for promoting such manufacturing.

[30] The viability will improve multi-fold once the India-Myanmar-Thailand Trilateral Highway (part of the AH1) project of ADB connects with the Sittwe deepwater port in Myanmar, and India’s plans to extend the railway connectivity to Moreh on the Myanmar border and beyond to the proposed Trans-Asian Railways are executed.

The views expressed above belong to the author(s). ORF research and analyses now available on Telegram! Click here to access our curated content — blogs, longforms and interviews.

PDF Download

PDF Download