This article is part of the series Comprehensive Energy Monitor: India and the World

This article is part of the series Comprehensive Energy Monitor: India and the World

Background

On 1 July 2022, the government announced a windfall tax of

INR23,250/tonne (t) on domestic crude oil production,

INR6/litre(l) on the export of petrol and aviation turbine fuel (ATF), and

INR13/l on the export of diesel. Three weeks later, the government reduced the export tax on diesel and ATF by

INR2/l and removed the tax on petrol. The tax on domestically produced crude was reduced to

INR17,000/t. A fortnight later, the government removed the export tax on ATF and reduced the tax on diesel by half to

INR5/l and increased the tax on domestically produced crude oil to

INR17,750/t. The economic rationale for imposing windfall taxes was that India’s trade deficit had increased to record high levels and a weak rupee had increased the value of India’s imports.

In 2008, when oil prices increased to about US$100/barrel (b) some sections of the Indian government demanded the imposition of a windfall tax on oil companies. But the government refused to say that there was

no economic rationale for such a tax. This week, UN Secretary General Antonio Guterres commented that it was

"immoral" for oil & gas firms to profit from the ongoing geopolitical crisis and called for oil & gas companies to face special (windfall) taxes. Is profit, especially unexpected profit, a sin that must be taxed away or is it a sin to tax oil company profit?

The economic rationale for imposing windfall taxes was that India’s trade deficit had increased to record high levels and a weak rupee had increased the value of India’s imports.

The Economic Logic

Production of scarce, depletable energy resources such as oil and natural gas command an

‘economic rent’ which is central to natural resource valuation.

Economic rent is defined as the return to any factor of production over the minimum amount required to retain it in its present use. It is broadly equivalent to the profit that can be earned from a factor of production (for example, a natural resource stock such as oil) beyond its

normal supply cost. Discovered reserves of mineral resources such as oil and gas gain value over time as

depletion increases their replacement cost. In theory, it is natural for oil and natural gas prices to reflect their

current marginal cost.

A price exceeding long-run marginal cost is ‘

monopoly profit’ which can only be achieved through collusion between producers or by government decree. The distinction between ‘economic rent’ and ‘monopoly profit’ is not merely semantic. Economic rent provides the incentive and cash flow necessary to simulate new supplies at ever rising

replacement costs. The consequence of disallowing economic rents associated with depleting resources is future

shortages of the resource. Economic rent is by no means limited to energy fuels. Still, energy’s social and economic significance instigates public antipathy towards economic rents that accrue to the energy industry in general and the oil industry in particular. The oil industry is singled out for attack as it is seen to be the beneficiary of both

economic rent and monopoly profit, with collusion with OPEC (organization of the petroleum exporting countries) contributing to the monopoly component.

According to some interpretations, ‘windfall profit’ is distinct from that of both ‘

economic rent’ and ‘monopoly profit’ and is defined as the ‘profit earned unexpectedly, through circumstances beyond the control of the company concerned’. As the profits are neither expected nor the result of efforts of the firm, it is assumed that taxing the firm would not harm the . A finer distinction could also be made in terms of whether the windfall profits arise out of the

cyclical nature of the market or structural features of the industry. Studies have found that a tax on windfall profits arising out of the

structural nature of the industry does not affect company behaviour whilst a tax on profits arising out of short term or cyclical factors affects company behaviour resulting in resource misallocation and distortion and is best avoided.

The oil industry is singled out for attack as it is seen to be the beneficiary of both economic rent and monopoly profit, with collusion with OPEC (organization of the petroleum exporting countries) contributing to the monopoly component.

The empirical relevance to the case of oil depends on whether the supply of oil is given and limited for all times

as is that of land. If the supply curve for oil is responsive to prices and therefore indicates that more oil is supplied at higher than lower prices, then the taxation of the windfall profits induces the

misallocation of resources in the economy and leads to a reduction in public welfare.

American Experience

The American example of imposing

windfall taxes in 1980 is widely quoted. When the Carter Government came to power,

price decontrol was the only available instrument to curb growing demand for oil amidst the supply crisis set off initially by the OPEC embargo against America and its allies in 1973 and later in 1979 by the Iranian Revolution. Removing controls on domestic oil prices was expected to

produce additional revenue of US$1 trillion, translating into more than US$300 billion of additional profit for oil companies. ‘

Windfall profit tax’ was designed to capture this additional profit.

Unlike the ‘

excess profits tax’ collected during the World Wars which was a supplementary tax on corporate income, the crude oil windfall profit tax collected in the United States had nothing to do with profits. It was a

tax on oil price and was paid before profits made by an oil company were calculated. The

price of oil in 1979 was assumed to be reasonable, and any price above that was taxed at rates between 15 and 70 percent. When the windfall tax bill was being debated in 1979 the

Washington Post observed that the proposed tax was merely ‘an excise on every barrel of oil produced’. When the bill was passed, the

Wall Street Journal described it as the ‘the Death of Reason’ which had ‘sacrificed the nation’s security to its thirst for revenues’.

Removing controls on domestic oil prices was expected to produce additional revenue of US$1 trillion, translating into more than US$300 billion of additional profit for oil companies.

Most analysts who studied the US crude oil windfall profit tax have concluded that it was

not a great success. Against a revenue projection of over US

$300 billion over ten years only US$80 billion was generated. Oil prices did not increase as anticipated through the 1980s, but the base price indexed to inflation continued to rise. In addition, administering the tax proved to be more complicated and expensive than originally thought. During the period of the tax’s existence, America’s reliance on foreign oil increased from

32 percent to 38 percent. This increase was partly attributed to windfall profit tax inhibiting domestic production.

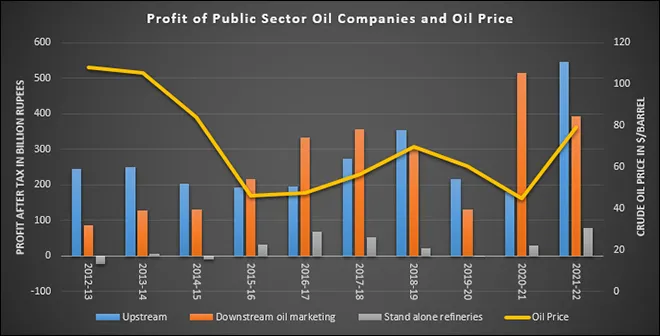

The Indian Case

In the upstream sector

production sharing contracts (PSC) allow the government to get a higher share of profits when oil prices increase. If a windfall tax is levied, oil companies will pass the cost to the government by way of reduced profit. Royalties levied by central and state governments under PSC are on an

ad-valorem basis, which means that government revenue increases with an increase in oil prices. The downstream sector (refining) is a ‘margin’ business and

gross refining margins do not necessarily follow crude price fluctuations. Given the competitive nature of the

refining business and the fact that there is a global shortage of refining capacity, improvement of margins is attributable to enhanced productivity and not to high oil prices. Based on these fundamentals, it is possible to stay at the granular level and illustrate, balance sheet by balance sheet, that Indian oil companies do not make ‘windfall profits’ on account of high oil prices. But a more useful exercise would be to look at broader questions: What purpose would an additional tax on oil companies serve? Would it contribute to India’s energy security? Would it improve redistribution of wealth and

quality of life for the poor?

Given the competitive nature of the refining business and the fact that there is a global shortage of refining capacity, improvement of margins is attributable to enhanced productivity and not to high oil prices.

The

Chaturvedi Committee Report treated windfall profit as resource rent and recommended that revenue from windfall taxes could be used for supporting the subsidy mechanism as a ‘short term measure’. The report treated the government as the rightful owner of ‘

resource rent’ and argued in favour of using the revenue to bridge budgetary gaps and support redistributive policies. Whilst this may sound reasonable, introducing subsidies with new revenue streams would only increase inefficient consumption. It is known that subsidies drive up energy

consumption by middle class & rich households rather than facilitate consumption by the poor.

If windfall profit taxes are used to sustain price distortions or make up for budgetary shortfalls, even in the short term, it will comfort policymakers that they can always tap on this new revenue source to sustain their policies. In addition, windfall profit tax will reduce the incentive for domestic exploration and production of crude oil increasing import dependence. By skimming off the profit streams of oil companies, the government will not only compromise India’s energy security but also sustain its own inefficiency.

Source: Petroleum Planning & Analysis Cell

Source: Petroleum Planning & Analysis Cell

The views expressed above belong to the author(s). ORF research and analyses now available on Telegram! Click here to access our curated content — blogs, longforms and interviews.