In the last five years, when there were major concerns over the country’s economic growth, the Indian health insurance industry was doing surprisingly well. In fact, it had been growing at more than

double the rate of the overall economy, according to data from Insurance Regulatory and Development Authority (IRDA).

Such explosive growth, though, hasn’t translated into population coverage, which kept declining until 2013. At around 288 million persons covered in 2015, it has only marginally improved from the 2011 level of 254 million.

What is alarming, though, is the difference in the benefits of such coverage extended to men and women, wherein the latter are clearly at a disadvantage.

Private health insurance

To begin with, actual insurance coverage in India is in sharp contrast to the highly optimistic projections of major agencies.

In 2012,

a World Bank group publication estimated that by 2015, more than 600 million people in India will have access to some form of health insurance. The actual number in 2015 was around 288 million, according to IRDA. In fact, National Sample Survey Office (NSSO) data for 2014

puts the figure at an even lower 170 million.

This being the story of overall coverage, there is a need to consider the type of coverage and expenditure protection that health insurance offers. This is particularly relevant in the context of the sustainable development goals (SDGs) that India is implementing from this year, under which health insurance coverage is an indicator.

A paper presented at the International Population Conference (2013) based on 2009 data from the health insurance industry

hinted at gender-based discrimination. This is corroborated by an analysis of data collected by the Insurance Information Bureau (IIB), established by IRDA to meet the industry’s data needs.

Startling numbers

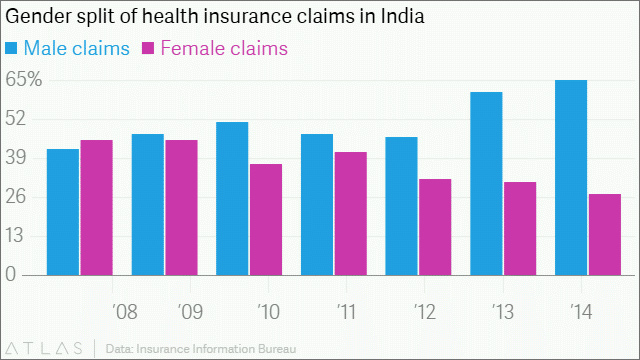

The latest IIB report, analysing data for 2013-14, puts the total number of health insurance claims in the country at just over 30 million. Of these, nearly 8% did not have gender-related information; so these could be either male or female.

For the rest, the analysis shows three alarming findings:

First, in 2013-14, around 70% of the total claims honoured were those of males; only the rest went to females. In 2012-13, too, it was roughly the same, suggesting that this wasn’t a new trend.

Second, of the total claim amount disbursed by the industry in 2013-14, around 72% went to males and 28% to females. The proportion was roughly the same the previous year, too.

Finally, the average claim amount paid to males was ₹31,949 and that to females was ₹29,136 that year. The figures were ₹29,688 and ₹26,688 respectively for males and females in the previous year.

However, even these stark differences pale when once looks at age-specific numbers.

Age and payouts

For the age group of 70 and above, for every claim paid to a woman, more than 11 were paid to men. In the 0-5 years group, for every claim paid to a female, more than four were paid to males.

While IRDA does not provide gender-segregated enrolment numbers for health insurance, the 2014 NSSO health survey shows that the coverage itself was well-balanced across genders — across government-funded insurance schemes, employer-supported health insurance, and private health insurance.

In fact, as a proportion of total population, more women are covered by government-funded insurance schemes across urban and rural India.

However, the IIB numbers ask an important question: how much of insurance coverage gets converted to actual financial protection and for whom?

The industry in India is

known for its iniquitous coverage.

Maharashtra alone, for instance, accounts for 23% of all health insurance claims across India. Six states account for 70% of all claims and 73% in claim money paid. Also, the six metro cities account for 25% of all health insurance claims across India, as well as 30% of total claim money paid.

Gender-based exclusion may very well be the latest manifestation of the industry’s ingrained inequity.

It can be reasonably argued that these numbers represent some form of exclusion, which needs to be explored further using a systematic study.

The analysis is based on transaction-level data supplied by third-party administrators alone, who cover 55% of all health claims. However, IRDA also states that given the large sample, the trends or conclusions arrived at can be sufficiently representative of the whole population.

Given the scale of the issue, industry regulators will have to quickly step in, get expert help to see to what extent the industry has been a willing partner in limiting healthcare access to Indian women and girls.

Perhaps, IRDA can begin by publishing the number of persons covered by health insurance as well as the rejection ratios segregated by gender, for the years in question.

This commentary originally appeared in Quartz.

The views expressed above belong to the author(s). ORF research and analyses now available on Telegram! Click here to access our curated content — blogs, longforms and interviews.