ndia is attempting to introduce a streamlined tax system to handle indirect taxation within the country. While the new system has been acknowledged as beneficial in a number of ways, there remain concerns regarding its implementation. If handled poorly, this tax reform could have long-term effects on the Indian economy.

Introduction

As 1 July approaches, India is girding itself for its second historical financial policy shift in the span of 12 months — the advent of the Goods and Services Tax. Unlike demonetisation which was announced by the prime minister without preamble, the implementation of the GST has long been in the works with initial discussions starting almost a decade ago. In formulating and implementing the GST—which is meant to streamline the country’s indirect tax system by amalgamating its many central and state taxes — the government has set ambitious goals for itself. The potential benefits of the tax reform are undeniable: it will help bring India’s informal sector into the fold, lower business costs across most sectors, increase exports, and reduce incidences of unnecessary double taxation. However, there are certain issues related to the implementation of the new tax system, among them — the problematic input tax credit issues, the uncertainty related to the functionality of the GST information technology system, and the ambiguity of the anti-profiteering clause. These challenges could result in the sinking of an otherwise promising policy endeavour.

Goods and Services Tax: An overview

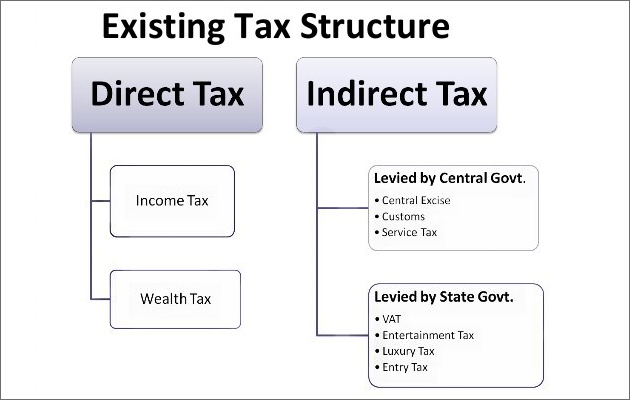

The idea behind the Goods and Services Tax, at least in theory, is simple. To raise revenue for public expenditure, the Government of India levies a series of indirect taxes (along with direct taxes on Income and Capital Gains). The current indirect tax system is complex, with at least seven major multi-stage value added taxes levied on many financial transactions. This has led to an unreasonable burden on taxpayers, who have had to deal with administrative hassles, the detrimental effects of double taxation, and confusion over archaic regulations. [i]

Figure 1.

Source:Beginners Guide to Goods & Services

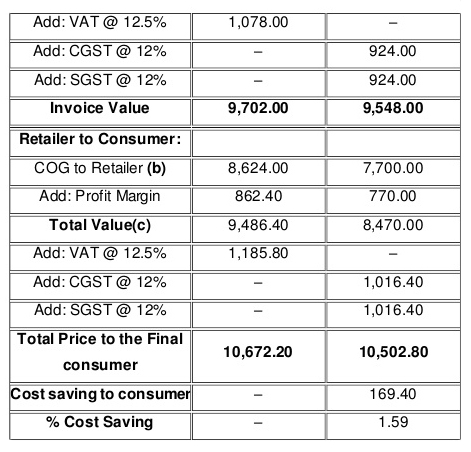

The GST aims to tackle many of the issues plaguing the current system by combining central and state indirect taxes. In their stead will stand two consolidated taxes: State Goods and Services Tax (SGST) and Central Goods and Services Tax (CGST). Under the new system,transactions will have both State GST and Central GST levied upon them, with ‘slabs’ of tax rates being applied depending on the type of Good or Service. The rates levied on goods and services will range from zero percent on items categorised as essential, to 28 percent on items deemed to be luxuries. [ii]The new system is expected to bring down the average costs of goods and services across the country by eliminating double taxation (see Table 1).

Table 1:Potential savings as a result of GST Implementation

Source:GST India

Along with lower average costs and elimination of double taxation, there are additional ancillary benefits that the GST offers. Under previous legislation, companies with annual revenue under INR 1.5 crore were exempted from paying indirect taxes. This threshold has now been lowered to either INR 10 or 20 lakh, depending on the geographical location of the corporate entity. The lowering of the threshold considerably broadens the tax base, effectively bringing much of what was previously considered the informal sector into the folds of the formal sector. [iii]Moreover, the GST is not applied to exported goods and services, which is expected to provide a marked boost for India’s exports [iv]. Implementation issues, however, could still cause extensive problems if they are not managed properly.

Implementation issues: Input Tax Credit

The main problem that could hamper the implementation of the GST centres on the documentation requirements for Input Tax Credits and the stage at which said credit accrues. The objective of any value added tax system (such as the GST) is the avoidance of double taxation. This is done by providing credits along every step of the production chain, effectively taxing only the extent of the value that has been added. The easiest way to illustrate this is by examining international best practices (see Figure 2).

Figure 2:

International Best Practices – VAT Input Tax Credit

In our example we will follow a 10% VAT placed on a loaf of bread along the production chain. In the first step of the production chain, a farmer grows wheat and sells it to a baker for 20 cents with a 10% tax rate (2 cents) which the farmer then sends to the government. The baker pays 22 cents for the wheat and produces a loaf of bread with it which he sells to the store for 60 cents with a 10% tax rate again (6 cents). He sends the 6 cents to the government, but receives 2 cents back (which is his Input Tax Credit for the wheat). The stores sells the loaf of bread for $1.00 with a 10% tax rate ($1.10) to the consumer and sends 10 cents to the government but receives 6 cents back as their input tax credit. In this process, each part of the supply chain is only being taxed for the value it has added to the product.

The GST will work using the same system of input tax credits along the production chain. The issue that arises under the Indian GST, however, is the onerous documentation requirement which can have a number of unintended consequences. Under Section 16 (11) of the Model GST Law, an input tax credit can only be received when:

The buyer has received a tax invoice from the supplier

The buyer has received the goods/services

The taxes charged on the purchase have been deposited/paid by the supplier

The issue with Section 16 (11) is that it puts the administrative burden associated with the tax on the buyer rather than the supplier, which can be problematic for businesses. One potential issue that could arise as a result of the administrative shift is the non-payment of taxes by the supplier. In that case, the buyer will end up having to pay for not only her share of the tax, but also for the supplier’s share of the tax under the proposed tax code. Further, problems could arise, if for some reason there are inconsistencies found in the supplier’s documentation at some later stage. Under this scenario, the buyer will be forced to pay back the tax reimbursement to the government with interest. This problem is usually fixed by market forces, however, as any non-compliant suppliers will soon find themselves losing customers as a result of their negligence. The government has also put in place a mechanism to help with the issue, by providing a publicly available compliance rating system which will allow consumers to pinpoint defaulters as the system starts to take effect over the coming years.

More problematic, perhaps, will be the short-term cash flow issues caused by Section 16 (11). Most businesses strive to have efficient working capital (i.e., the amount of cash kept on hand to bridge the period between receiving cash from their customers and paying cash to their suppliers). If an entity can keep less cash on hand for day to day activities, it can invest more in other activities, which can be as ambitious as business expansion or as simple as an interest bearing savings account.

Section 16 (11) throws a wrench in working capital calculations for Indian businesses, due to the documentation requirements. Since the input tax credit can only be released once the supplier has submitted adequate documentation, businesses will have to account for potential delays and keep extra cash on hand, thereby reducing money available for potential growth and investment activities.

Moreover, any transfer of inventory from one state to another is considered a taxable event under the GST. Effectively, the tax will be levied on the goods or services at the time of the transfer and the offsetting input tax credit will only be available for collection at the point of sale, putting a further strain on the cash requirements for businesses. [vi]It is possible that due to cash flow strains certain small businesses might even have to borrow money to fund their day-to-day activities, or in the worst case scenario, shutter their operations.

Effects on small businesses

A corollary to the documentation matching issue are the problems that could arise as a result of purchases made from vendors who are exempt from registering for the GST. As mentioned earlier, the threshold rate for registration and payment of the GST has been lowered considerably, yet businesses with an annual turnover of less than INR 10 lakh for certain North-Eastern and Hill states and less than INR 20 lakh for other states remain exempt from the GST. [vii]The GST exemption has both advantages and disadvantages for small businesses.

The most important advantage comes from not having to pay taxes on the goods and services provided by small businesses. This allows small businesses to have higher profit margins, while also permitting them to offer lower prices than larger competitors, levelling the playing field between small and large businesses to a certain extent. There is also the additional advantage of not having the working capital issues that businesses registered under the GST might have to deal with.

Unfortunately, many of these advantages are nullified by the large administrative burden that is placed on businesses buying from suppliers that are exempt from paying GST. Once again, the onus is placed on the purchaser, who has to be the one that files all related documentation on behalf of the supplier, in order to get the input tax credit. [viii]

The GST also has a provision for small businesses that do not qualify for exemption. Under Section 9 of the GST Model law, businesses with turnover under INR 50 lakh can register under the GST Composition Scheme and pay nominal tax rates ranging from .5 percent to two percent, which allows them to have the same advantages that exempt businesses have. There are some distinct disadvantages associated with registering under the GST Composition Scheme, however, including a moratorium on carrying out interstate transactions and the requirement that taxes be sent directly to the government rather than passed on to the buyer. This effectively limits the kinds of transactions carried out by GST Composition businesses while also nullifying the cash flow advantage that exempt businesses have.

Outcome

The input tax credit issues associated with the GST could have a considerable impact on small enterprises. If proper outreach and education on GST is not conducted, it will likely result in significant short-term cash flow problems in the months after implementation, especially for small businesses. Further, the cumbersome administrative burden associated with buying from exempt entities could end up providing a major disincentive for businesses looking to conduct any kind of transactions with small enterprises, leading to a crowding out of Indian small business.

Implementation issues — GSTN functionality

Another key implementation issue could stem from the proposed technology backbone of the GST system. On 1 October 2013, halfway across the world, the most powerful nation in the world attempted to implement a landmark reform using technology. After a long and arduous battle, the Obama administration had successfully managed to pass the Affordable Care Act (colloquially known as “Obamacare”). The launch of the healthcare act was marred by technology failure on the very first day when users attempted to sign up for insurance plans. Deemed by Barack Obama as one of the low points of his presidency, the failure of technology undermined the trust of the public and set the reform back by at least a year.

One of the lynchpins of the India’s GST is the integrated technology network that will allow for seamless documentation, recording of debits, and dispersal of credits. Developed by some of the country’s leading IT firms, the Goods and Services Tax Network (GSTN) is the information technology platform that will be used in order to record all GST-related transactions. An ambitious endeavour, the platform aims to hold up to 70 million user accounts. Yet, no one has been able to ascertain if it will be functional on the rollout date of 1 July.

The first area of concern lies in the registration of users for the website. According to the most recent numbers, 60 percent of the taxpayers from State Tax databases have registered themselves on to the platform. [ix]Yet, only 6.5 percent of taxpayers from the Central Tax databases had registered seven days before the 31stMarch registration deadline. Inadequate outreach on the part of the central government can be pointed to as the main culprit for the lack of registered users. A lack of timely migration can cause serious issues for the viability of the GST as the IT infrastructure is the only possible way to track and properly implement the nascent tax system.

Along with the registration challenge, the GSTN has also been dealing with an auditing issue. Ascertaining and verifying the accuracy of the data within the GSTN would seem to be a Herculean task, given its 70 million expected users. In order to do so, the Comptroller and Auditor General of India (which has been tasked with the audit), would need access to all GSTN data. Yet, the GSTN has refused data access to the CAG for auditing purposes, citing its private entity status (51 percent of the organisation is owned by private Indian financial institutions) and stating that it is only acting as the “holder” of the information [x]. Without a proper audit of the data within the platform, there is no way to ascertain the functionality of the GSTN.

Trust in the GSTN has already been brought up as an issue, with the lack of transparency into the majority privately owned organisation being cited as a crucial concern. If the delays in registering users causes a functionality issue or the GSTN is not able to properly support the rollout on 1stJuly, public trust issues could end up causing the failure of what could otherwise be a breakthrough financial reform.

Implementation issues — Anti-profiteering clause

There is another implementation issue that could prove to be a hurdle for the GST, albeit on a smaller scale than the documentation and technology factors. One of the touted benefits of the GST system is the lowering of prices for many goods and services across the economy. As illustrated in an earlier example, businesses will be able to cut down on the effects of double taxation which should then be passed on to the end user. Unfortunately, when VAT’s have been implemented in other countries, businesses have kept prices the same and used the savings incurred from a change in tax systems to bolster their own profit margins.

In order to stop undue profiteering from changes in tax systems, an anti-profiteering clause has been added to the GST [xi]. The clause requires that businesses pass any benefits from the change in tax systems to the end consumer. The clause does not, however, provide any mechanism for the monitoring of anti-profiteering activity. The clause, and any subsequent investigation, will instead be triggered by “credible complaints” according to Revenue Secretary Hasmukh Adhia. [xii]The uncertainty associated with the anti-profiteering clause can affect both businesses and consumers. The private sector fears that ambiguity in the clause will lead to “witch-hunts” as tax authorities are given leeway to make subjective judgements as to whether a business is profiteering, without any regulations or laws to back their rulings.

Box 1.

International Best Practices – Anti-Profiteering Policies

Internationally, the best example of effective anti-profiteering policies, during the implementation of a value added tax, is the Australian model. Australia’s anti-profiteering policies began a year before the implementation of Australia’s GST system in 2000, and were focused on educating both consumers and businesses. Measures included pricing guidelines, strategies focused specifically on certain sectors, and advice centres for both businesses and consumers. In addition to educating the public, the Australian government also put into place price-monitoring measures in the months before and after the implementation of the GST system. Enforcement was viewed as the ultimate fall-back option and only 11 cases were taken to court.

At the same time, consumers fear that ambiguous regulations or laws will lead to a lack of transparency and that decisions regarding the applicability of the anti-profiteering clause will be made on anad hocbasis depending on political connections or even worse,outright corruption. The lack of clarity can, once again, have a detrimental effect on public perception regarding the GST. While public perception might seem like a trivial matter, it can often spell the difference between success and failure in the case of wide-scale implementation of policy reform, as the example of Obamacare showed.

Conclusion

The Goods and Services Tax is a much needed tax reform, and if implemented correctly, can do wonders for India’s economy. Along with eliminating double taxation and lowering product price, the GST can also assimilate the informal sector into the greater Indian economy and provide a much needed boost for India’s flagging export market. Yet there are implementation issues that could be problematic for India’s small businesses and, perhaps more importantly, undermine public trust in the GST.

The issues surrounding the GSTN can be managed if more time is given for continued enrolment of taxpayers and thorough testing of the IT infrastructure. Additionally, giving more time for the CAG to conduct a thorough audit would allow for any functionality issues with the GSTN to be brought to light, preventing costly public trust issues.

Similarly, the problems with the anti-profiteering clause can be ironed out with more time and the implementation of widespread education and price monitoring policies in the lead-up to the GST. The formation of a committee to handle all complaints, creation of an audit unit specifically geared towards anti-profiteering testing, and putting in place regulations outlining what specifically constitutes “anti-profiteering” can help build corporate and public trust in the GST.

The documentation requirements and their subsequent effects on cash flow and small businesses are more difficult to sort out. Perhaps more time needs to be spent by the policymakers in the formulation of policies centred on the input tax credit and its documentation requirements.

There is a commonality that can be found in the solutions for all three of the implementation issues currently plaguing the GST — time. The GST is an ambitious plan, and Prime Minister Narendra Modi’s government has set similarly formidable benchmarks for its implementation. The wisest course of action, however, might be to delay the rollout of the GST for a few months in order to not repeat some of the mistakes that were made during demonetisation. A poorly implemented version of the GST could negatively affect the Indian economy for years to come.

Endnotes

[i]ClearTax. n.d. “cleartax.in.”Benefits of Registering under GST Composition Scheme.https://cleartax.in/s/benefits-of-registering-under-gst-composition-scheme/.

[ii]PTI. 2017. “Only Credible Plaint will Trigger GST Anti-Profiteering Clause.”Bloomberg Quint, April 4

[iii]The Hindu . 2016. “GST council sets exemption threshold for tax at RS. 20 lakh.”The Hindu, September 04

[iv]Sudhaman, KR. 2017. “GST Rollout: Big Push to Exports.”MillenniumPost, March 22.

The views expressed above belong to the author(s). ORF research and analyses now available on Telegram! Click here to access our curated content — blogs, longforms and interviews.

Dr. Aparaajita Pandey is Senior Research Associate at ShowTime Consulting &: a Ph.D. from Centre for Latin American Studies Jawaharlal Nehru University.

PDF Download

PDF Download