The G20 compact with Africa: Overview, assessment, and recommendations for India

The ‘Compact with Africa’ (CWA) is the main pillar of a renewed G20 partnership with the continent. Its objective is to attract more private investment to Africa, especially for infrastructure. African countries face the challenge of diversifying their economies and promoting industries and services that can absorb a rapidly growing labour force. Lack of investment and Africa’s massive infrastructure gap are major obstacles to this economic transformation. Through country-specific compacts, the CWA aims to remove key bottlenecks for more investment and better infrastructure. Proponents say that the CWA represents a new approach to cooperation that can provide a push for African development. But sceptics point to shortcomings that could limit the initiative’s effectiveness. The CWA also raises the question of India’s role, and how the CWA relates to India’s and Japan’s Asia Africa Growth Corridor. Strengthening complementarities between the two initiatives can improve the G20’s partnership with Africa and, in the process, India’s relationship with Africa.

Introduction

Africa is in the spotlight at this year’s G20 summit of the world’s major economies in Hamburg in early July. The unprecedented level of attention given to the continent follows a trend towards a broadening of the grouping’s agenda beyond its initial focus on economic and financial governance. Previous summits have gradually introduced global development issues in the G20’s work. The priorities of the German presidency include, for instance, sustainable development, climate change, food security, health, digital technology, and migration. Among the central themes of this year’s summit is an intensified partnership with Africa.

The ‘Compact with Africa’ (CWA) initiative is the main pillar of the G20 partnership with Africa. [i]The initiative aims to improve conditions for private investment in Africa, especially for infrastructure. African countries face the challenge of diversifying their economies, promoting industrialisation, and absorbing a rapidly growing labour force. Africa’s massive infrastructure gap is one of the main bottlenecks in achieving this structural transformation. At the core of the CWA will be country-specific compacts: Participating African countries commit to improving conditions for private investment; in return, G20 members and international partners commit to enhancing international framework conditions, providing technical assistance and raising awareness among the private sector.

Private investment for infrastructure in Africa has been a longstanding international concern. In 2005, the G8 summit in Gleneagles led to the creation of the Infrastructure Consortium for Africa (ICA). Infrastructure and private investment have been key pillars of the G20 Seoul Development Consensus since 2010. Several other initiatives for African infrastructure exist, such as Power Africa, Africa50, and the Programme for Infrastructure Development in Africa. The CWA aspires to provide added value as a new approach to cooperation with Africa that overcomes the aid-centric relationship of the past. Proponents hope that the G20’s political clout generates the necessary push to remove major bottlenecks from Africa’s development path.

As a member of the G20, a source of investment, and a development partner for African countries, India can play a crucial role in the G20’s partnership with the continent. India’s involvement should be based on an analysis of the CWA’s potential as well as India’s own interests and comparative advantages. India’s position will also depend on the relationship between the CWA and the newly proposed Asia Africa Growth Corridor (AAGC). This brief presents an overview of the context in Africa and the main drivers influencing the CWA’s content and design. It then examines the CWA initiative. The brief closes with a discussion of India’s options for engagement in the CWA.

‘Compact with Africa’: The Context

Africa’s growth story

The CWA coincides with a turning point in Africa’s development. Between 2001 and 2014, African economies grew at rates above five percent on average. In 2015 and 2016, growth slowed down to 2.2 percent, mainly because of declining commodity prices and reduced global demand. [ii]In sub-Saharan Africa, growth slowed to the lowest level in more than 20 years. [iii]The slowdown, however, affected African economies unevenly, and commodity-exporting countries were hit harder than countries with more diversified economies. Several countries, including Kenya, Tanzania, Rwanda, Ethiopia, Côte d’Ivoire and Senegal, continue to experience high growth rates of above five percent throughout 2015-2017. [iv]This picture points to structural shifts towards more diversification and resilience in several African economies.

Growth in Africa is set to pick up again this year but is likely to remain below past trends, as it struggles to keep up with population growth. Africa is the only region in the world where the working-age population is projected to expand until 2035. Between 2015 and 2030, 29 million new entrants will join the labour market every year.[v] Yet, under current trends, less than a quarter of new workers can expect to find a regular job. [vi]Reaping the “demographic dividend” of a growing working-age population requires more job-creating industries and services, entrepreneurship, and improved education and skills.

Foreign direct investment (FDI) can be a powerful driver for structural economic change. FDI to Africa used to be concentrated in the extractive sectors of resource-rich countries. More recently, it has started to diversify and contribute to job-creating industries in countries such as Ethiopia and Kenya. Moreover, some countries, such as Ethiopia, Tanzania, and Rwanda, are expanding their manufacturing sectors after years of stagnation in manufacturing on the African continent. In a context of rapid urbanisation and growing middle-class populations, African economies have great potential to become both production sites and consumer markets. However, Africa still attracts only a small fraction of international private investment. [vii]

Africa’s massive infrastructure gap has been identified as one of the main obstacles for economic transformation. The continent ranks behind other developing regions in infrastructure development. Improvements have taken place in the ICT sector and, to some extent, in water and sanitation. Meanwhile, progress in transport and power has been disappointing. African countries have the lowest road and railway density; over 60 percent of people in sub-Saharan Africa do not have access to electricity. [viii]The CWA assumes a financing gap of ca. USD 50 billion per year. [ix]

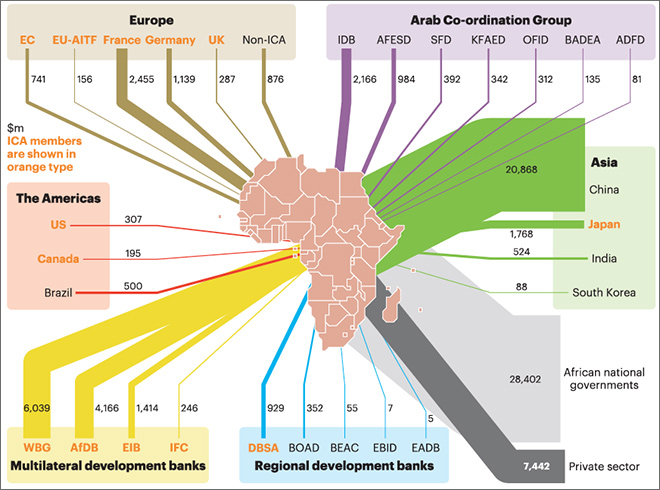

According to the ICA, USD 83.4 billion were committed to African infrastructure in 2015, increasing from USD 74.5 billion in 2014 (Figure 1). [x]African governments have been stepping up public investment in the past but have little room to improve. Public investment in infrastructure from African governments stood at USD 28.4 billion in 2015, showing a decline from USD 34.5 billion in 2014. Debt levels are rising, fiscal space is limited, and external financing conditions have tightened. Low tax revenues, weak banking systems and underdeveloped capital markets constrain the mobilisation of domestic resources. [xi]

In 2015, over half of the committed funding for infrastructure came from external public sources, including OECD countries, emerging countries, multilateral and regional development banks, and institutions of the Arab Co-ordination Group. Committed investment of external public sources increased from USD 31.9 billion in 2011 to USD 47.5 billion in 2015. The largest sources are the World Bank Group (WBG), the African Development Bank (AfDB), and official investment from China (discussed later in this brief).

Private investment committed to infrastructure stood at USD 7.4 billion or nine percent of all committed funding in 2015. Private participation in infrastructure (PPI) had increased until 2012 but stagnated subsequently. [xii]

Figure 1: Reported and identified financing flows into Africa’s infrastructure in 2015

Source:The Infrastructure Consortium for Africa, Infrastructure Financing Trends in Africa – 2015, The Infrastructure Consortium for Africa Secretariat, 2016, p. 12.

Other drivers behind the CWA

Apart from Africa’s development context, other factors explain the CWA’s content and design, and the priority it is accorded in the G20 agenda.

First, the CWA’s emphasis on infrastructure and private investment reflects shifts in the landscape of international development financing. China and other rising powers, especially the BRICS (Brazil, Russia, India, China, South Africa), have kept infrastructure high on the agenda through initiatives such as the Asian Infrastructure Investment Bank (AIIB). As the main bilateral lender for infrastructure in Africa, China has contributed to a renewed emphasis on infrastructure. Official Chinese investment in infrastructure skyrocketed from USD 313 million in 2000 to USD 4.4 billion in 2012. [xiii]China’s official funding is subject to strong fluctuations and difficult to estimate. According to the ICA, China’s infrastructure funding jumped from USD 3 billion in 2014 to USD 20.9 billion in 2015. However, the yearly average of Chinese public investment for infrastructure would still be USD 12.3 billion between 2011 and 2015. China has filled gaps left by official development assistance (ODA) from the OECD Development Assistance Committee (DAC) donors, which had reduced infrastructure funding in the 1990s.

At the same time, bilateral OECD/DAC donors and multilateral development banks have increasingly stressed the role of the private sector in development cooperation. Development finance from private sources was highlighted at the Monterrey conference on Financing for Development in 2002. In the context of the 2030 Agenda for Sustainable Development, the mobilisation of private finance gains in relevance to implement the shift “from billions to trillions” to fund the Sustainable Development Goals (SDGs). [xiv]Many donors have developed new tools and instruments to use ODA as a catalyst for private finance. [xv]Examples include the European Union’s (EU) regional blending facilities and the World Bank’s IDA Private Sector Window. The idea to catalyse private investment using public funds is a central feature of the CWA.

A second set of drivers relates to the domestic context in Germany. In the G20 format, the presidency has substantial leeway to shape the agenda. Domestic factors have played a role in making Africa a top priority for the German presidency.

The global refugee and migration crisis has had a strong impact on German and European politics. In 2015, EU member states received over 1.2 million first-time asylum applications, the biggest share being registered in Germany. [xvi]Most refugees are from Syria, Afghanistan and Iraq. However, migration from Africa made the headlines when in 2015 some 4,000 migrants drowned in the Mediterranean as they attempted to cross from North Africa. [xvii]Concerns about future migratory pressures caused by conflicts, climate change, and lack of economic perspectives in Africa have a strong influence on politics. Right-wing populism has thrived on anti-migration sentiments. Tackling the “root causes” of migration from Africa and the Middle East has become a main policy objective ahead of parliamentary elections in September 2017. German Finance Minister Wolfgang Schäuble, whose ministry had initiated the CWA, sees a direct link between the lack of economic perspectives in Africa and “geopolitical risk”. [xviii]

Three different German ministries have pitched new initiatives on Africa. The CWA has originated in the Federal Ministry of Finance and is the only one directly anchored in the G20 process. In addition, the Federal Ministry for Economic Development and Cooperation (BMZ) proposed a ‘Marshall Plan with Africa’. [xix]This proposal calls for a paradigm shift in the development partnership between Africa and Europe. It is thematically more comprehensive than the CWA, also covering peace and security as well as political governance. The plan intends to focus German development cooperation on flexible partnerships with reform-minded African countries. The plethora of German Africa initiatives is completed by ‘Pro! Africa’, an initiative from the Ministry for Economic Affairs.

The ‘Pro! Africa’ initiative points to another domestic driver: an upsurge of interest in Africa among the German business community. ‘Pro! Africa’ enlists German businesses as partners for economic development in Africa. A central objective is to increase trade and investment with Africa and improve market access for German companies. [xx]Despite being a global trading power, Germany’s economic presence in Africa is relatively small compared to other countries, such as France, China and India. The structural shifts underway in Africa towards more diversified economies and growing consumer markets make the continent more attractive for German businesses.

What is the ‘Compact with Africa’?

The contours of the CWA are laid down in a report jointly prepared by the AfDB, the International Monetary Fund (IMF) and the WBG, and endorsed at the G20 Finance Ministers and Central Bank Governors Meeting on 17-18 March 2017 in Baden-Baden. [xxi]The main objective of the CWA is to remove obstacles for long-term, private investment in Africa, especially in infrastructure.

At the core of the CWA are country-specific investment compacts. Participating African countries commit to creating an enabling environment for private investment. G20 countries, other partner countries and international organisations commit to improving international framework conditions and providing technical cooperation. Participation in the CWA is open and demand-driven. At the G20 Africa Conference in Berlin on 12-13 June 2017, which rang in the implementation phase, seven countries – Côte d’Ivoire, Ethiopia, Ghana, Morocco, Rwanda, Senegal and Tunisia had joined the initiative.

The CWA report sets out possible reforms and other measures within three different frameworks: macroeconomic, business, and financing. These frameworks are divided into modules addressing main bottlenecks to private investment. [xxii]The modules represent a non-definitive “menu of options” that can be adapted to specific country contexts. Table 1 summarises the frameworks and modules, and gives examples of mutual commitments.

Table 1: Summary of CWA frameworks and modules

Modules

Main challenge

Examples of possible mutual commitments

Macroeconomic Framework

Macroeconomic stability and debt sustainability

Growing public debt

Compact countries:maintain macroeconomic stability and build up debt management capacity

G20/partners:provide technical assistance and develop instruments to lower financing costs for public investment (e.g. de-risking sovereign securities)

Domestic revenue mobilisation

Low tax-to-GDP ratio

Compact countries:develop a strong tax system

G20/partners:capacity development and international cooperation on base erosion/profit shifting

Institutions for public investment

Loss of resources in public investment

Compact countries:strengthen public investment management frameworks

G20/partners:technical assistance

Transforming public utilities

Insufficient reach and quality

Compact countries:strengthen institutional frameworks; free up resources by making utilities commercially viable and operational

G20/partners:support transformational projects to present viable ways of reforming utilities; support regional practitioner networks

Business Framework

Reliable regulations and institutions

Unpredictable regulation and inconsistent implementation

G20/partners:support creation of SIRM and provide political risk insurance

Project preparation

Shortage of resources and capacity

Compact countries:dedicate appropriate resources to project preparation

G20/partners:allocate more international financing to project preparation, including a multi-donor facility for African infrastructure

Standardisation of contracts

Lack of commercial and legal skills, especially regarding PPPs

Compact countries:contracting authorities and PPP units use WBG recommendations on PPP provisions and engage in capacity building on standard clauses

G20/partners:capacity building and piloting of standard clauses

Financing Framework

Risk mitigation instruments

Real and perceived risks for private investment in frontier markets

G20/partners:support de-risking instruments to crowd-in private investment (e.g. IDA private sector window, EU External Investment Plan); refine principles for blended finance

Domestic debt market development

Narrow domestic investor base and lack of long-term instruments

Compact countries:enable development of domestic debt markets

G20/partners:provide technical assistance and issue bonds in local currencies to facilitate investors’ first exposure to a country

Broadening of private finance, including from institutional investors (pension funds, insurers)

Obstacles faced by institutional investors

Compact countries:improve capacities of domestic banks in project and housing financing, expand use of equity investment instruments, improve regulatory framework for institutional investors

G20/partners:relax restrictions on institutional investors

Source:Author’s compilation based on“The G-20 Compact with Africa”, a Joint AfDB, IMF and WBG Report,G20 Finance Ministers and Central Bank Governors MeetingBaden-Baden, March 17-18 2017.

The macroeconomic framework has the objective to ensure macroeconomic stability and free up public resources for non-commercial investments as a basis for private investment. Modules in this framework include, for instance, improving debt management, increasing tax revenues, and avoiding unnecessary losses in public investment. The business framework aims to provide an enabling business environment. Some African countries have made considerable progress. However, regulatory uncertainty and weak institutions still represent sizeable obstacles. The objective of the financing framework is to make investment projects fundable by increasing the availability of financing at reduced costs and risks. Modules include, for instance, the use of de-risking instruments, such as blending to crowd-in private finance, and the development of domestic debt markets.

Under each module, the report suggests possible mutual commitments. Under the macroeconomic framework, for instance, efforts by African countries to strengthen their tax systems would be reciprocated by G20 action on tax evasion and profit shifting. Another example is the mobilisation of institutional investors, such as pension funds and insurers, for infrastructure investment in Africa. Total assets of such investors are projected to reach USD 100 trillion in 2020. Investing just one percent of new institutional investments per year could fill Africa’s infrastructure financing gap. [xxiii]However, regulatory obstacles in both African and OECD countries prevent institutional investors from financing infrastructure in Africa. As a possible mutual commitment, country compacts could involve a concerted approach to reducing these barriers.

Can the CWA deliver?

Expectations as to the CWA’s prospects of success diverge. Proponents laud the initiative as a long-overdue change of course away from an aid-centric paradigm of cooperation. Sceptics warn, however, that the CWA smacks of ‘Washington consensus’ and is unsuited for the poorest countries. The CWA’s added value compared to the status quo is in the way it bundles different measures and provides high-level political backing and visibility. The initiative rests on the expectation that the political impetus provided by the G20 will help trigger reforms in African countries, coordinated measures by a range of international actors and, eventually, buy-in of the private sector. However, the CWA’s current design also suffers from shortcomings that could limit its reach and effectiveness.

First, the CWA’s focus on private investment for infrastructure is likely to be unsuited for many African low-income countries, which have the largest infrastructure funding gaps. [xxiv]Most African countries are still in a phase of their development where they typically rely on government funding and international concessional finance. Private investment tends to shy away from difficult contexts. Evidence suggests that measures proposed by the CWA might not succeed in substantially altering this fact. In 2015, more than two-thirds of all private infrastructure investment in Africa went to South Africa and Morocco, two middle-income countries. [xxv]De-risking instruments such as blending facilities tend to direct private finance to middle-income countries rather than poorer countries. [xxvi]The CWA’s geographic coverage therefore risks remaining limited. The initiative is designed to set incentives for ‘reform champions’ to emerge. Accordingly, the current group of Compact countries consists of middle-income countries and stable, fast-growing, reform-oriented low-income countries.

Second, the CWA is relatively silent on how to ensure the quality of private investment. [xxvii]Private investment entails risks for African countries, from higher debt to social and environmental risks for local populations. The responsibility for enforcing standards lies with the host country and puts a burden on the limited capacities of low-income countries. The CWA does not make suggestions for the use of investment policy frameworks suited to the needs of African countries (e.g., UNCTAD’s Investment Policy Framework for Sustainable Development). More generally, the CWA has missed the opportunity to embed private investment in Africa firmly in broader international frameworks. The CWA report mentions the 2030 Agenda for Sustainable Development and the 2063 Agenda of the African Union. However, the report does not explain how to align private investments with these frameworks. The Paris Agreement on climate change is not mentioned at all. Stronger operational linkages with these international frameworks could strengthen the CWA’s normative basis.

A third major criticism is that the CWA is not comprehensive enough to address the challenges of job creation and economic transformation in Africa. [xxviii]Addressing Africa’s jobs challenge is as much about investing in people as it is about infrastructure. However, the CWA does not refer to improving education, nor upgrading skills. Moreover, economic transformation is not an automatic result of international private investment. African countries also require the institutional capacity to conduct an active industrial strategy. The CWA stresses access for international investors but says little about supporting the domestic private sector and home-grown entrepreneurship. [xxix]As a single initiative, the CWA cannot deal with everything; the initiative requires clear and explicit linkages to other relevant areas of cooperation.

Finally, the G20’s structures might not be fully adequate. The G20’s main asset is its convening power and the ability to coordinate a diverse set of actors. The G20 has structures in place to deploy influence and engage with different stakeholders, including ministerial meetings, working groups, and dialogue forums with the business sector, civil society and research institutions. Yet, the G20’s linkages with African countries need strengthening. South Africa is a member of the G20; the African Union and the New Partnership for Africa’s Development have observer status at the Hamburg summit. However, a permanent, collective representation could strengthen African ownership and allow African countries to hold the G20 to account on international framework conditions such as trade. Moreover, a collective African representation could promote continental, regional and cross-border connectivity, which is so far absent from the CWA.

Despite these shortcomings, the CWA has the potential to address some of the most relevant challenges for African development. Investing in infrastructure and more diversified economies is a long-term effort. Effective implementation will require strong ownership by African countries and continuity in the G20’s work agenda. The success of the CWA therefore depends on the follow-up by the next G20 presidencies and other G20 members.

Options for India

During his visit to Germany in May 2017, Prime Minister Narendra Modi expressed support for the German G20 presidency. However, India has not yet publicly specified its position on the CWA. In the same month, India hosted the annual meeting of the AfDB and, together with Japan, launched plans for the Asia Africa Growth Corridor (AAGC). How India defines the relationship between the AAGC and the CWA can have a strong impact on the G20 partnership with Africa.

With rapidly growing development, trade and investment relations with African countries, India is a key actor in the G20’s partnership with Africa. The Delhi Declaration of the Third India-Africa Forum Summit (IAFS) in 2015 highlights areas of cooperation that are crucial to the CWA. For instance, India and African countries agreed to promote investment exchanges and to “support long-term capital flows to Africa to stimulate investment, especially in infrastructure”. [xxx]India is the seventh largest investor in Africa measured by FDI stocks. [xxxi]Indian investments, still predominantly executed by large public firms in the extractive sectors, have started to be more diversified with private companies promoting job-creating industries. [xxxii]About 70 percent of currently operative Lines of Credit (LoCs) supported by the Indian government and close to 50 percent of their credit volume go to African partners. [xxxiii]According to the ICA, official Indian funding for African infrastructure totalled USD 2.4 billion in the period from 2012 to 2015. [xxxiv]

The Delhi Declaration puts capacity building and skills at the heart of the India-Africa partnership. Accordingly, the AAGC stresses this aspect. [xxxv]Building on India’s and Japan’s comparative advantages, the AAGC aims to link economies from Asia and Africa not only through physical infrastructure, but also institutional, regulatory and digital connectivity. The AAGC will consist of four main components: 1) Development and cooperation projects; 2) Quality infrastructure and institutional connectivity; 3) Capacity and skill enhancement; and 4) People-to-people partnerships. The initiative’s emphasis on people-centred infrastructure also reflects India’s opposition against China’s ‘Belt and Road Initiative’ (BRI), perceived as a top-down initiative.

The CWA and the AAGC represent different approaches to investment and infrastructure in Africa. Their relationship could theoretically take the form of three options:

Coexistence: India would not become strongly engaged in the CWA and focus on the AAGC. The two initiatives could be implemented separately and without need for additional coordination.

Coordination: G20 countries could coordinate the CWA and the AAGC, with India being engaged in both initiatives. In principle, the demand-driven nature of the CWA is compatible with the principles of India’s development partnerships. Coordination between the two initiatives could be soft, flexible and focused on optimising complementarity.

Integration: G20 countries could draw on the CWA and the AAGC to craft a common, long-term partnership between the G20 and Africa. The two initiatives could constitute pillars of a joint G20 initiative, including an Africa-Europe corridor and an Africa-Asia corridor.

Option 1 would give India greater leeway in shaping the AAGC by avoiding the burden of coordination with the CWA. However, this burden would likely fall on African countries with more limited capacities. Increasing fragmentation among international initiatives would have negative consequences for development effectiveness. Option 3 would be politically difficult. The fact that different G20 members prepared the CWA and the AAGC independently from each other speaks volumes. Individual G20 countries driving the two initiatives also cling to their visibility. Finally, option 2 represents a compromise between feasibility and desirability. This option would require some form of flexible coordination to avoid duplication and improve complementarity. Given the differences between the CWA and the AAGC, the risk of duplication appears smaller than the opportunity for complementarity.

India also has an interest in showing presence in the CWA. Indian private companies in Africa share an interest in improved investment conditions. In addition to the AAGC, India could draw on the CWA as part of a strategy to diversify engagement in investment and infrastructure initiatives as a response to China’s BRI. India could limit the cost of this engagement by focusing on the comparative advantages of the India-Africa partnership and the AAGC. By doing so, India could bring in new elements and even address some of the shortcomings of the CWA.

First, India’s engagement could address the criticism that the CWA’s perspective may be too narrow. India’s focus on capacity and skills development is a missing element in the CWA. Coordination with the AAGC could also bring in other areas that complement investment in infrastructure, such as agriculture, health and entrepreneurship.

Second, the AAGC stresses the quality of investment and infrastructure more strongly than the CWA. The AAGC ‘vision document’ refers to high quality standards to reduce environmental and social risks and improve the local impact. Moreover, the document highlights the guiding role of the 2030 Agenda and promises priority for green projects. [xxxvi]

Third, the AAGC emphasises knowledge sharing between developing countries. Sharing practical development experiences could be a valuable complement to the CWA’s more technocratic tone. This element could also increase the CWA’s relevance for a broader range of African countries. India faces similar challenges in job creation and infrastructure development. The AAGC refers to Indian initiatives, such as “Skill India” and “Smart City”, as possible subjects for knowledge exchange. India could also provide inputs to specific CWA modules. India has attracted considerable amounts of private investment for infrastructure, despite sharp drops in recent years. Between 1990 and 2015, PPI in India amounted to USD 341 billion (compared to USD 169 billion in sub-Saharan Africa). [xxxvii]India’s experience includes failures from which African countries could learn. Indian experience could inform, for instance, CWA modules on public-private partnerships, the development of local debt markets, and the issuance of local currency bonds (‘masalabonds’).

Finally, India’s approach could enrich the CWA’s focus on individual compact countries by including cross-border projects and regional integration (e.g., in the framework of Regional Economic Communities). Moreover, India could be a strong voice for improving continental African representation in the G20 as the Delhi Declaration calls for a more representative global governance architecture.

The CWA and the AAGC are still work in progress. Their concrete relationship depends on many factors unknown for the moment (e.g., country overlaps between the initiatives). By engaging in both initiatives, India can have a positive impact on the G20’s partnership with Africa and strengthen the India-Africa partnership in the process. This engagement will be a long-term process, with India’s possible G20 presidency in 2019 and the next IAFS in 2020 as milestones.

Endnotes

[i]African Development Bank, International Monetary Fund and World Bank Group, “The G-20 Compact with Africa,” a joint report presented at the G-20 Finance Ministers and Central Bank Governors Meeting, Baden-Baden, 17-18 March 2017, http://www.bundesfinanzministerium.de/Content/EN/Standardartikel/Topics/Featured/G20/2017-03-30-g20-compact-with-africa-report.pdf;jsessionid=C6BC9AF27F10329BD14D53850106E33F?__blob=publicationFile&v=2

[ii]African Development Bank, OECD Development Centre and United Nations Development Programme,African Economic Outlook 2017. Entrepreneurship and Industrialisation, African Development Bank, Organisation for Economic Co-operation and Development and United Nations Development Programme, 2017: 24/160, https://www.afdb.org/fileadmin/uploads/afdb/Documents/Publications/AEO_2017_Report _Full_English.pdf

[iii]International Monetary Fund, “Sub-Saharan Africa. Restarting the Growth Engine,”Regional Economic Outlook, Washington D.C.: International Monetary Fund, April 2017, https://www.imf.org/en/Publications/REO/SSA/Issues/2017/05/03/sreo0517

[iv]World Bank Group, “Africa’s Pulse. An Analysis of Issues Shaping Africa’s Economic Future,”Volume 15, Washington D.C.: World Bank Group, April 2017: 19.

[vi]Barak Hoffman and Jean Michel Marchat, “Jobs in Africa: Designing Better Policies Tailored to Countries’ Circumstances,”The Africa Competitiveness Report 2017, African Development Bank, World Economic Forum and the World Bank Group, 2017, 35-49: 36, http://www3.weforum.org/docs/WEF_ACR_2017.pdf

[vii]Robert Kappel, Birte Pfeiffer and Helmut Reisen, “Compact with Africa. Fostering Long-Term Investment in Africa”,Discussion Paper13/2017, Bonn: Deutsches Institut für Entwicklungspolitik/German Development Institute, 2017: 33/34, https://www.die-gdi.de/uploads/media/DP_13.2017.pdf

[ix]Estimates of Africa’s infrastructure needs often go back to the following study. The estimate of USD 93 billion, with less than half of it financed, now likely represents a lower bound: Vivien Foster and Cecilia Briceno-Garmendia (eds.),Africa’s Infrastructure: A Time for Transformation, Washington DC: World Bank, 2010, http://documents.worldbank.org/curated/en/246961468003355256/pdf/521020PUB0E PI1101Official0Use0Only1.pdf

[x]The Infrastructure Consortium for Africa, “Infrastructure Financing Trends in Africa – 2015,” Abidjan: Infrastructure Consortium for Africa Secretariat, 2016, https://www.icafrica.org/fileadmin/documents/Annual_Reports/ICA_2015_annual_report.pdf

[xii]Jeffrey Gutman, Amadou Sy and Soumya Chattopadhyay,Financing African Infrastructure. Can the World Deliver?, Washington D.C.: Brookings Institution, March 2015: 18, https://www.brookings.edu/wp-content/uploads/2016/07/AGIFinancingAfricanInfrastructure_FinalWebv2.pdf

[xiv]World Bank Groupet al., “From billions to trillions. Transforming Development Finance,”Development Committee Discussion Note, Washington DC: World Bank/International Monetary Fund, 2 April 2015, http://siteresources.worldbank.org/DEVCOMMINT/Documentation/23659446/DC2015-0002(E)FinancingforDevelopment.pdf

[xv]Emma Mawdsley, “A new development era? The private sector moves to the centre,”Norwegian Peacebuilding Resource Centre Report, September 2014, https://www.files.ethz.ch/isn/183886/2a503c1ad68fd311c1d5cc210d91e803.pdf

[xvii]United Nations High Commissioner for Refugees,Global Trends 2015, Geneva: United Nations, 2016: 32, http://www.unhcr.org/576408cd7.pdf

[xviii]Wolfgang Schäuble, “Germany, the G20 and Inclusive Globalization,”Project Syndicate, 13 March 2017, https://www.project-syndicate.org/commentary/germany-g20-presidency-agenda-by-wolfgang-schauble-2017-03

[xix]Federal Ministry for Economic Cooperation and Development (BMZ), “Africa and Europe – A new partnership for development, peace and a better future. Cornerstones of a Marshall Plan with Africa,” Berlin: Federal Ministry for Economic Cooperation and Development, January 2017. https://www.bmz.de/en/publications/type_of_publication/information_flyer/information_ brochures/Materialie270_africa_marshallplan.pdf

[xx]Federal Ministry for Economic Affairs and Energy, “Pro! Africa. Promoting the prospects, taking the opportunities, strengthening the economies,” Berlin: Federal Ministry for Economic Affairs and Energy, May 2017. http://www.bmwi.de/Redaktion/EN/Downloads/strategiepapier-pro-afrika.pdf?__blob=publicationFile&v=2

[xxii]For an overview of challenges in African infrastructure, see Paul Collier, “Attracting International Private Finance for African Infrastructure,”Journal of African Trade1 (2014): 37-44.

[xxiv]Robert Kappel and Helmut Reisen, “The G20 ‘Compact with Africa’. Unsuitable for African Low-Income Countries,”Study, Friedrich-Ebert-Stiftung, June 2017, http://library.fes.de/pdf-files/iez/13441.pdf

[xxv]The Infrastructure Consortium for Africa,op. cit.

[xxvi]Harpinder Collacott, “What does the evidence on blended finance tell us about its potential to fill the SDG funding gap?”OECD Development Matters, 24 November 2016, https://oecd-development-matters.org/2016/11/24/what-does-the-evidence-on-blended-finance-tell-us-about-its-potential-to-fill-the-sdg-funding-gap/

[xxvii]Jann Lay, “The Compact with Africa: An Incomplete Initiative,”GIGA FocusNo. 2, Hamburg: German Institute of Global and Area Studies, June 2017, https://www.giga-hamburg.de/en/system/files/publications/gf_afrika_1702_en.pdf

[xxx]“Partners in Progress: Towards a Dynamic and Transformative Development Agenda,”Delhi Declaration of the Third India-Africa Forum Summit, 29 October 2015, http://www.mea.gov.in/Uploads/PublicationDocs/25980_declaration.pdf

[xxxi]United Nations Conference on Trade and Development,World Investment Report 2017. Investment and the Digital Economy, Geneva: United Nations, 2017: 44.

[xxxii]Malancha Chakrabarty, “Indian Investments in Africa: Scale, Trends, and Policy Recommendations,”Working Paper, New Delhi: Observer Research Foundation, May 2017, http://cf.orfonline.org/wp-content/uploads/2017/05/ORF_WorkingPaper_IndiaInAfrica.pdf

[xxxiii]India EXIM Bank data on operative Lines of Credit (based on the update of 8 May 2017), https://www.eximbankindia.in/lines-of-credit

[xxxiv]The Infrastructure Consortium for Africa,op. cit.:51

[xxxv]Research and Information System for Developing Countries (RIS), Economic Research Institute for ASEAN and East Asia (ERIA) and Institute for Developing Economies/Japan External Trade Organization (IDE-JETRO),Asia Africa Growth Corridor. Partnership for Sustainable and Innovative Development – A Vision Document, launched at the African Development Bank Meeting in Ahmedabad, India, 22-26 May 2017, http://www.africa-platform.org/sites/default/files/resources/asia_africa_growth_corridor_vision_ document_may_2017.pdf

The views expressed above belong to the author(s). ORF research and analyses now available on Telegram! Click here to access our curated content — blogs, longforms and interviews.

PDF Download

PDF Download